UNH - BCAT: Good Strategy And Price But The Distribution May Not Be Sustainable

2023-05-01 15:13:21 ET

Summary

- Investors are desperately in need of income due to the rapidly-rising cost of living in the United States.

- BlackRock Capital Allocation Term Trust invests in a portfolio that is split between common equity and fixed-income securities in order to produce both capital gains and income for investors.

- The BCAT closed-end fund supplements its common stock holdings with covered calls in order to boost its income further.

- The CEF boasts a very attractive 10.12% yield, but it does not appear to be sustainable.

- The fund is trading at a reasonably attractive valuation right now.

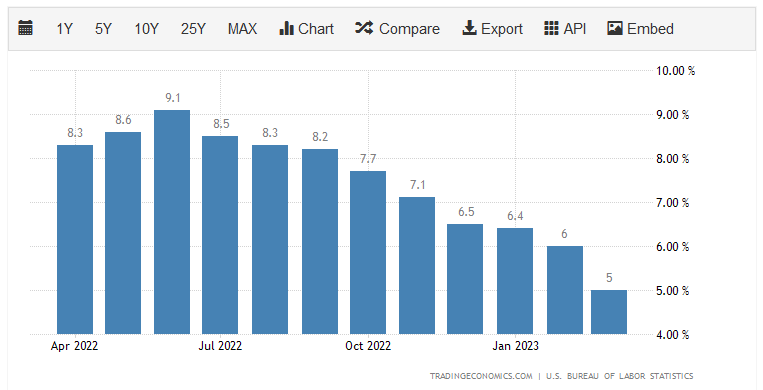

There can be little doubt that one of the biggest problems facing the average American household today is the incredibly high inflation rate that has been dominating our economy. This is illustrated with the consumer price index, which has shown at least 6% appreciation year-over-year during eleven of the past twelve months:

{kind=link}

As the majority of this inflation was caused by rising food and energy prices, everyone has been affected regardless of whether they are rich or poor. This is a big problem for those of lesser means as wages have not grown nearly fast enough to keep up with inflation, and April marked the 24th straight month of negative real wage growth. This is the biggest reason why many consumers have been taking on second jobs, drawing down their savings, or increasing their revolving credit card balances. I discussed this in a recent blog post . The only real conclusion that we can draw from all of this is that people all across the country are desperately in need of additional sources of income.

As investors, we are certainly not immune to this. After all, we have bills to pay and require food just like anyone else. We do, however, have other means available to us to increase our incomes. For example, we can put our money to work for us earning an income. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are not very well followed in the financial media and unfortunately not many financial advisors are familiar with them. This is quite unfortunate as these funds offer a number of advantages over open-ended funds or exchange-traded funds. One of these is that closed-end funds are able to employ a variety of strategies that have the effect of boosting their yields well beyond that of any of the underlying assets in the portfolio. That is a characteristic that is very compatible with income-seekers.

In this article, we will discuss the BlackRock Capital Allocation Term Trust ( BCAT ), which is a closed-end fund that can be used by investors that are seeking an income. This is evident in the fund’s current 10.12% yield, which is substantially higher than just about anything else in the market. I have discussed this fund before, but a significant amount of time has passed since then so obviously several things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the BlackRock Capital Allocation Term Trust has the stated objective of providing its investors with a high level of total return and current income. This is a surprising objective considering the nature of this fund. The website provides further information:

“BlackRock Capital Allocation Term Trust’s investment objectives are to provide total return and income through a combination of current income, current gains, and long-term capital appreciation. The trust invests in a portfolio of equity and debt securities. Generally, the trust’s portfolio will include both equity and debt securities. At any given time, however, the trust may emphasize either debt securities or equity securities. The trust utilizes an option writing (selling) strategy in an effort to generate current gains from options premiums and to enhance the trust’s risk-adjusted returns.

BCAT has a twelve-year limited term, subject to extension, with a contingent feature to convert to perpetual.”

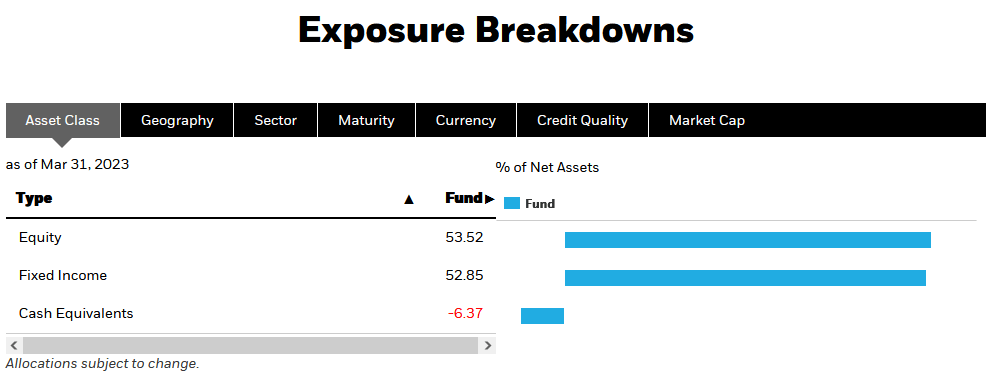

Usually, when a fund’s name implies that it has a limited lifetime, it is a fixed-income fund. This is because fixed-income securities only have a limited duration themselves, so the fund can easily structure its holdings around its own end-of-lifetime. However, this one is different in that it can include both equity and debt securities. In this light, the fund’s emphasis on total return makes a bit more sense. Currently, the fund is almost perfectly split between debt and equity:

{kind=link}

At this point, you will almost certainly notice that the fund has a negative allocation to cash. This comes from the fact that this fund employs leverage as a way to boost its returns, which we will discuss later in this article.

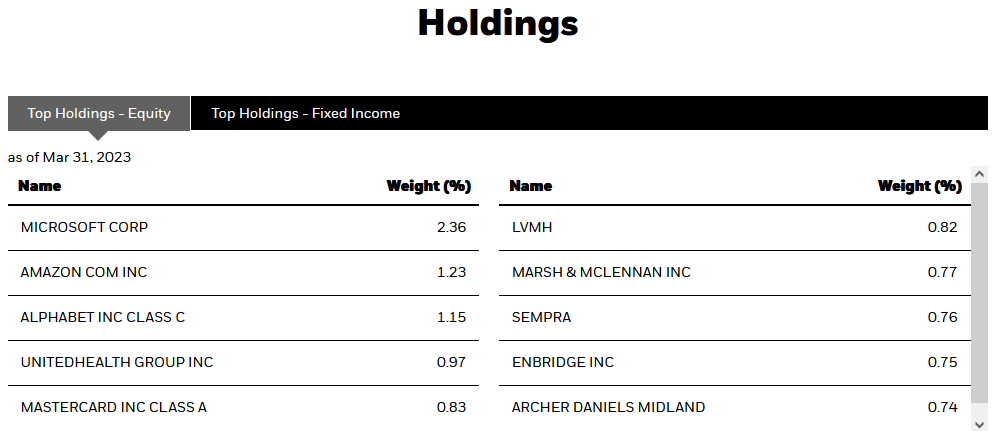

The fact that the BCAT fund is focused on total return makes a great deal of sense, as equity is by its very nature a total return instrument. After all, anyone buying common equity is typically interested both in the direct payments that the stock will make to its investors via dividends as well as the capital appreciation that accompanies the growth and prosperity of the issuing company. This is exactly what this fund is seeking through its common equity holdings, although it is also using a covered call writing strategy to generate a synthetic yield from its holdings. This is important because several of the fund’s largest positions have either no yield or a very small one. Here are the largest holdings in the fund’s portfolio:

{kind=link}

This is a rather unusual portfolio that includes a number of companies that we do not usually find in most closed-end funds. This is rather nice from a diversification perspective since it means that the fund should be able to reduce an investor’s concentration risk. Concentration risk comes from the fact that many funds hold very similar positions. For example, many equity-focused closed-end funds have substantial exposure to the four mega-cap American technology companies. This one does as well, but the weightings here are not nearly as high as we see in most other funds. The problem with this is that an investor may think that they have a diversified portfolio because they are holding several different funds, but their portfolio is actually not diversified because all the funds are holding the same assets! The fact that this one has numerous assets that we do not often see in a closed-end fund means that adding this fund to a portfolio should help to reduce an investor’s overall exposure to any individual asset. For example, Marsh & McLennan ( MMC ), LVMH ( LVMHF ), and Archer-Daniels-Midland ( ADM ) are not often seen in the largest positions of an equity closed-end fund.

As stated though, the yields of most of these stocks are quite low. We can see this here:

| Company |

| Current Yield |

| Microsoft ( MSFT ) |

| 0.89% |

| Amazon.com ( AMZN ) |

| 0.00% |

| 0.00% |

| UnitedHealth Group ( UNH ) |

| 1.34% |

| MasterCard ( MA ) |

| 0.60% |

| LVMH |

| 1.60% |

| Marsh & McLennan |

| 1.31% |

| Sempra ( SRE ) |

| 3.06% |

| Enbridge ( ENB ) |

| 6.64% |

| Archer Daniels Midland |

| 2.31% |

A money market fund is yielding 4.50% to 4.65% today, so all of these companies are less than that except for Enbridge. Enbridge is also the only company on this list that has a positive real yield. This is a fairly good indication that the stock market as a whole is still at inflated levels despite the disappointing performance over the past year. However, it also shows the importance of the fund’s covered call-writing strategy, which allows the fund to artificially earn more income from a common stock than the stock’s yield. The extra money coming in from the option premiums does ultimately boost the fund’s total return and income as well, so long as the stock does not get called away.

The fund also generates income via the fixed-income allocation that makes up about half of its portfolio. This makes sense since these securities are designed to deliver their investment return through direct payments to their investors. In fact, if an investor purchases a brand-new bond and holds it until maturity, that is literally the only return that the investor will receive since bonds always repay their face value at maturity. These securities have no inherent link to the growth and prosperity of the company since a company will not increase the amount of interest that it pays its creditors just because its profits go up. Thus, these securities will not have capital gains in the same way as common stocks.

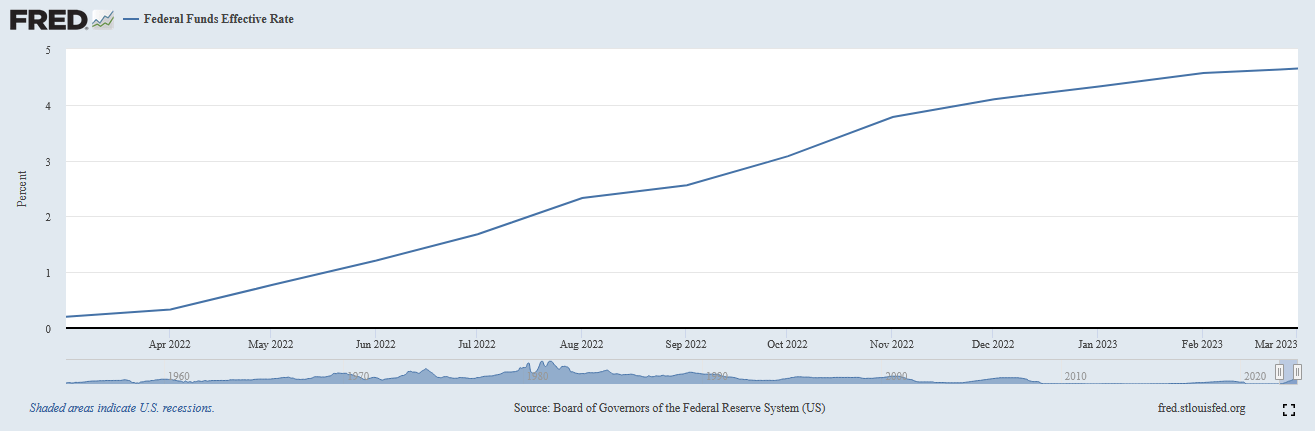

With that said, it is possible to earn capital gains from fixed-income securities because their market value fluctuates with interest rates. It is an inverse relationship, so when interest rates go up bond prices go down and vice versa. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates over the past year in an effort to combat the incredibly high inflation rate that is dominating the economy. In March 2022, the effective federal funds rate was 0.20% but it is 4.65% today:

{kind=link}

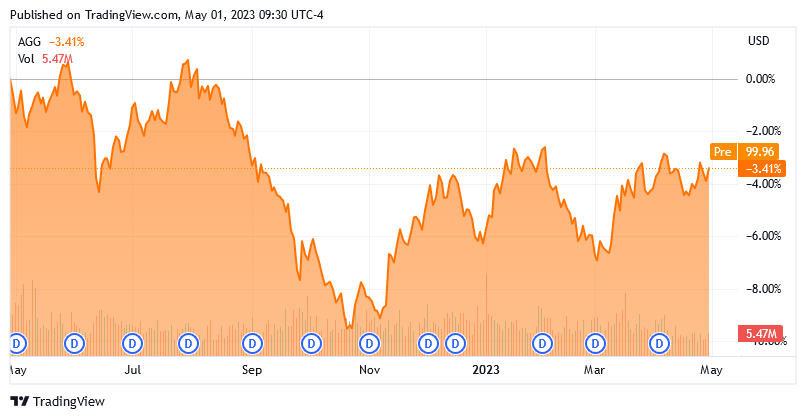

This has had a devastating effect on bond prices, with the Bloomberg U.S. Aggregate Bond Index ( AGG ) down 3.41% over the past year:

{kind=link}

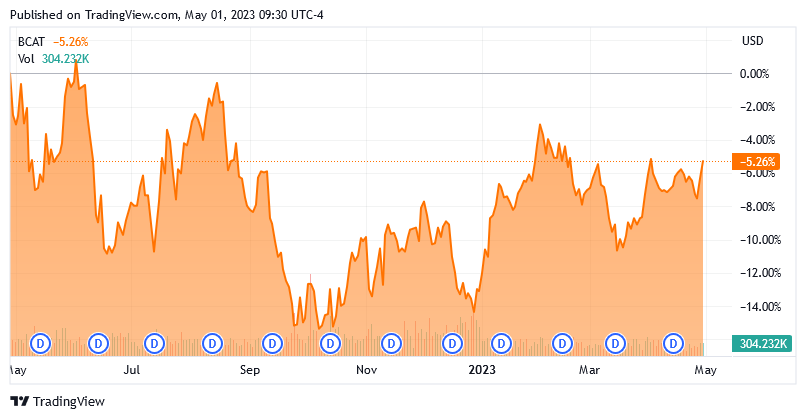

The BlackRock Capital Allocation Term Trust has certainly not been spared from this carnage as it is down 5.26% over the same time period:

{kind=link}

It is important to note though that the BlackRock Capital Allocation Term Trust has a much higher yield and when we take this into account, it managed to outperform the index over the period. This is not exactly surprising though, since the closed-end fund is not exclusively a bond fund. The stock portion of the portfolio helped to improve its performance, especially the options strategy since call option-writing strategies tend to outperform during flat markets.

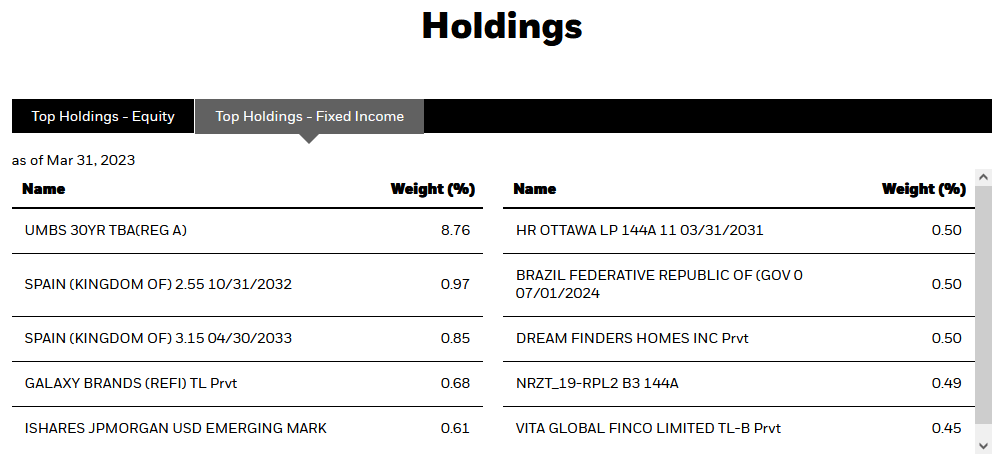

The BlackRock Capital Allocation Term Trust’s bond holdings are also significantly different than the Bloomberg U.S. Aggregate Bond Index, which will naturally have an impact on performance. We can see this quite clearly by looking at the largest bond positions in the portfolio:

{kind=link}

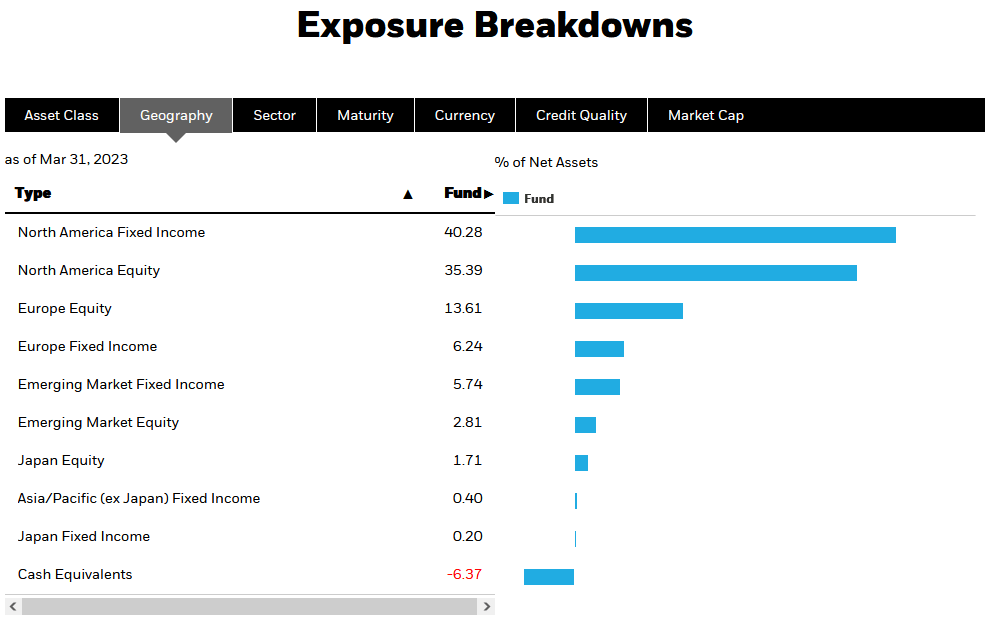

The biggest thing that we notice here is that the fund includes a number of bonds issued by foreign nations and other entities. This is very different from the bond index which only includes bonds issued by American entities. This immediately tells us that this is a global fund that seeks out investments from all around the world. That was true with the fund’s common stock portfolio as well, since we saw a few foreign companies among the fund’s largest stock positions. This global focus extends across the portfolio in the aggregate, as this fund has fairly significant exposure to issuers in Europe as well as some emerging market exposure:

{kind=link}

This is something that is very nice to see as it provides us with some protection against regime risk. Regime risk is the risk that some government or other authority will take an action that has an adverse impact on a company that we are invested in. The only realistic way to protect ourselves against this risk is to ensure that only a relatively small percentage of our portfolio is exposed to any individual nation. This fund is doing that to a certain degree, although it does still have greater exposure to North America than this region’s actual representation in the global economy. This is not exactly unusual though as most global funds have outsized exposure to the United States. This is because most funds are run by managers in North America and America has outperformed most global markets over the past decade. As a result of this, you should ensure that you have some ex-US funds in your portfolio to ensure that your portfolio as a whole enjoys sufficient global diversification.

Leverage

In the introduction to this article, I mentioned that closed-end funds like the BlackRock Capital Allocation Term Trust have the ability to employ a variety of strategies that boost their yields well beyond that of any of the underlying assets. One of the strategies that is employed by this fund is leverage. Basically, the fund borrows money and then uses that borrowed money to purchase income-producing assets like bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed funds, this strategy works pretty well to boost the effective yield of the portfolio. This fund is able to borrow money at institutional rates, which are significantly lower than retail rates, so this will usually be the case.

However, the use of leverage in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, the fund’s portfolio performance will be more volatile than a similar portfolio that does not employ leverage. Due to this, we want to ensure that the fund is not using too much leverage because that would expose us to too much risk. I generally like to see a fund’s leverage remain below a third as a percentage of its assets for this reason. Fortunately, this fund satisfies this requirement as its leveraged assets currently sit at a scant 5.24% of the portfolio. Thus, the balance between risk and reward is very acceptable here. Indeed, this fund could probably take on a bit more leverage in order to boost its performance further and still strike an acceptable balance between risk and reward.

Distribution Analysis

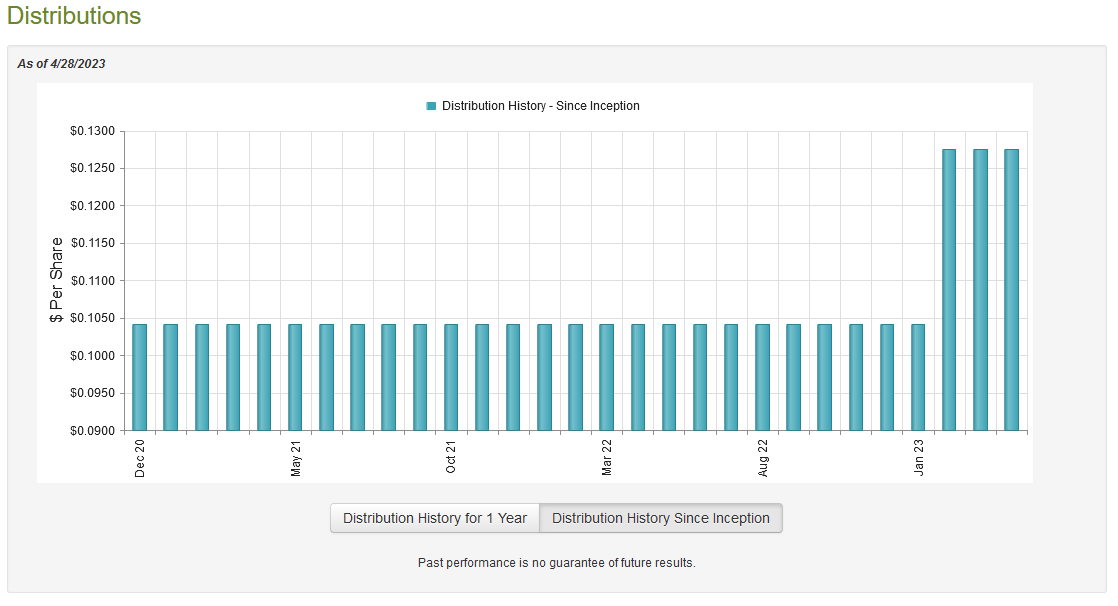

As mentioned earlier in this article, the BlackRock Capital Allocation Term Trust has the stated objective of providing its investors with a high level of current income and total return. In order to accomplish this, the fund assembled a portfolio of both fixed-income and common stocks, alongside an option-writing strategy. The fund aims to pay out all of its returns from this strategy and maintain a stable share price, just like most closed-end funds. To this end, this should result in the fund having a remarkably high distribution yield. That is certainly the case as the fund currently pays out a monthly distribution of $0.1275 per share ($1.53 per share annually), which gives the fund a 10.12% yield at the current price. The fund has not only been remarkably consistent with its payout over its relatively short life, but it actually increased it in February:

{kind=link}

This makes this one of the few funds that was able to increase its distribution this year, as many closed-end funds suffered such devastating losses in 2022 that they were forced to cut their payouts. The fact that this one has a reasonably strong distribution history is something that is likely to appeal to any investor that is seeking a safe and secure source of income that can be used to pay their bills and finance their lifestyles. As is always the case though, it is critical that we ensure that the fund can actually afford the distribution that it pays out. After all, we do not want to be the victims of a distribution cut since that would both reduce our incomes and almost certainly cause the fund’s share price to decline.

Fortunately, we do have a very recent document that we can consult for the purposes of our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2022. This report should therefore give us a pretty good idea of how well the fund navigated the challenging conditions in both the equity and fixed-income markets last year. It is also a much newer report than we had available to us the last time that we discussed this fund, so that is something that is very nice to see and should be helpful for our purposes. During the full-year period, the BlackRock Capital Allocation Term Trust received a total of $20,632,657 in dividends along with $66,928,415 in interest from the assets in its portfolio. When this is combined with a small amount of income from other sources, the fund had a total investment income of $87,111,636 over the period. The fund paid its expenses out of this amount, which left it with $55,631,648 available for the shareholders. This was, unfortunately, not enough to cover the $138,209,273 that the fund actually paid out in distributions over the period. At first glance, this is something that is very likely to be concerning as the fund lacked sufficient net investment income to cover the costs of its distributions.

However, the fund does have other methods through which it can obtain the money that it needs to cover its distributions. For example, the fund might have capital gains or option income, which can be classified as either a capital gain or a return of capital depending on the circumstances. Unfortunately, the fund generally failed miserably at this task over the year. The fund reported net realized losses of $79,620,786 and had another $298,534,539 in net unrealized losses. Overall, its assets declined by $511,634,594 over the period after accounting for all inflows and outflows. In this light, it is difficult to understand why the fund would increase its distribution in February. Its press release likewise sheds no light on the reasoning here, particularly since the fund did not manage to fully cover its distribution in 2021 either and that was a much stronger year for the markets. It is possible that management is treating the fund much like an annuity and intends for all of the assets to be distributed by the end of the twelve-year term of life, but I can find no evidence of this in the official releases. Regardless, the distribution is not sustainable unless the fund’s returns improve significantly.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Capital Allocation Term Trust, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 28, 2023 (the most recent date for which data is available as of the time of writing), the BlackRock Capital Allocation Trust had a net asset value of $17.04 per share but the shares only trade for $15.14 each. This gives the fund’s shares a discount of 11.15% to the net asset value at the current price. This is a very reasonable discount that is reasonably in line with the 11.41% discount that the shares have had on average over the past month. Overall, the current price certainly appears to be reasonable.

Conclusion

In conclusion, there are certainly a few things to like about the BlackRock Capital Allocation Trust. In particular, the fund’s mix of common equity and fixed-income securities provides a certain amount of stability because these two asset classes typically move inversely to each other, but this was unfortunately not the case in 2022. The fund’s option-writing strategy should also allow it to outperform in relatively flat or declining stock markets like we have seen over the past eighteen months.

Unfortunately, it does not appear that BlackRock Capital Allocation Term Trust can sustain its distribution unless it manages to boost its returns considerably. The price does allow for a certain amount of market weakness as it is currently trading for well below the value of its assets. As such, it might be worth buying today as long as you are willing to take on the risk of a distribution cut.

For further details see:

BCAT: Good Strategy And Price But The Distribution May Not Be Sustainable