CA - BCE: A Deep Value Play With An Above 7% Dividend Yield

2023-11-20 01:21:55 ET

Summary

- BCE is a Canadian dividend aristocrat in the telecommunications industry with a dominant positioning and strong profitability metrics.

- The company has a stellar track record of dividend hikes and offers an above 7% forward dividend yield, making it appealing for risk-averse investors.

- My valuation analysis suggests BCE stock is substantially undervalued.

Investment thesis

BCE Inc. ( BCE ) is a Canadian dividend aristocrat operating in a highly predictable telecommunications industry with high entry barriers. The company is the largest player in the industry, and its strong profitability metrics compared to its closest rivals suggest that BCE's dominance is safe. The company has a stellar track record of dividend hikes over the last 14 years despite substantial investments in 5G network buildup. The stock currently offers above 7% forward dividend yield, and my analysis suggests that the dividend is safe. The stock is low-volatile with around 0.5 market beta. The appealing dividend yield, together with low volatility, makes BCE an appealing investment opportunity for risk-averse investors who are seeking for higher predictability of their returns. All in all, I assign BCE a "Buy" rating.

Company information

BCE is a communications company providing wireless, wireline, internet, and television [TV] services to residential, business, and wholesale customers in Canada.

The company's fiscal year ends on December 31. BCE operates via two operating segments: Bell Communication And Technology Services and Bell Media. According to the latest annual report, BCE's largest revenue streams are Wireless and Wireline Services.

{kind=link}

Financials

BCE's financial performance over the last decade sends mixed signals to me. On the positive side, the company's profitability metrics were stable over the last ten years. The operating margin fluctuated within a narrow range of 22-24%, indicating good predictability of the company's future cash flows. The wide double-digit free cash flow [FCF] margin in seven years out of ten is also a good sign indicating the company will likely have enough resources to ensure shareholder returns and fuel future business success. However, stagnating revenue is a red flag to me, meaning the company navigates a highly competitive environment.

{kind=link}

I also have concerns regarding the management's capital allocation approach. Despite having a stable, wide, positive FCF margin, the company's balance sheet is far from being called a fortress. Cash reserves of below $500 million look relatively thin, especially compared to the massive $25 billion in total debt. The leverage ratio is high, and short-term liquidity ratios also do not look strong. The company's financial position does not give it much room to invest heavily in growth, which investors should understand. On the other hand, increasing financial leverage was inevitable given secular technological shifts which required the company to invest heavily in the 5G buildup. As the company further expands its 5G coverage, capex is poised to moderate. However, it is essential to understand that deleveraging will take a long road and substantial indebtedness might pressure the stock valuation.

Seeking Alpha

The latest quarterly earnings were released on November 2, when the company missed consensus estimates. Revenue grew by less than one percent YoY, and the adjusted EPS shrank from $0.64 to $0.59. It is important to emphasize that the EPS contraction occurred due to extraordinary items while the operating margin demonstrated resilience.

Seeking Alpha

The resilience in profitability metrics allowed the company to generate an impressive $562 million in levered FCF during the quarter, which was 62% higher than the same quarter last year. Maintaining a wide FCF margin is crucial for BCE as the company prioritizes shareholder returns, which we see from its stellar dividend growth history over the last 14 years .

The earnings release for the upcoming quarter is scheduled for February 7, 2024. Quarterly revenue is expected by consensus at $4.70, indicating a 2.8% YoY decline. The adjusted EPS is expected to stay almost flat with a one-cent expansion.

Seeking Alpha

The stock currently offers an above 7% dividend yield, which I consider very attractive. The management's commitment to strict cost control, which we see via resilient profitability metrics, suggests that dividend growth is safe in the foreseeable future. The Canadian telecom industry is inherently highly fragmented, with few big players. Entry barriers are very high as building up a network across the whole country requires massive investments in capex and long payback periods. BCE's closest rivals are Rogers Communications ( RCI ) and TELUS Corporation ( TU ).

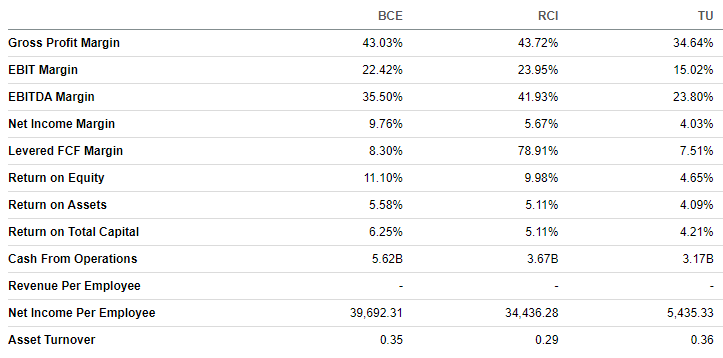

While BCE's position as the largest player in the industry is still undisputed, we see that TELUS has been closing the gap rapidly in recent years. This could have been a risk for BCE if TELUS' growth had been multiplied by strong profitability metrics. But this is not the case, as TU's stellar revenue growth in the highly-penetrated industry seems to be too costly. BCE's profitability metrics are substantially stronger than TU's and are about the same level as RCI's. Profitability metrics reflect operational efficiency, and in the table below, we clearly see that BCE in RCI is doing well in controlling costs. Over the long term, the most efficient business wins the competition. Given RCI's soft revenue dynamic over the last decade and TU's unsustainable long-term "growth at all costs approach," I think that BCE's market share is safe.

{kind=link}

To conclude, I believe that the above 7% forward dividend yield offered by BCE at the current stock price levels is safe on the horizon for the next several years as the company's dominant position in the Canadian telecom industry is safe. The stock has a low market beta of around 0.5, which means the stock is not volatile. Stability in the stock price, the attractive dividend yield, and consistent dividend hikes over the last 14 years look like an appealing opportunity for risk-averse investors.

Valuation

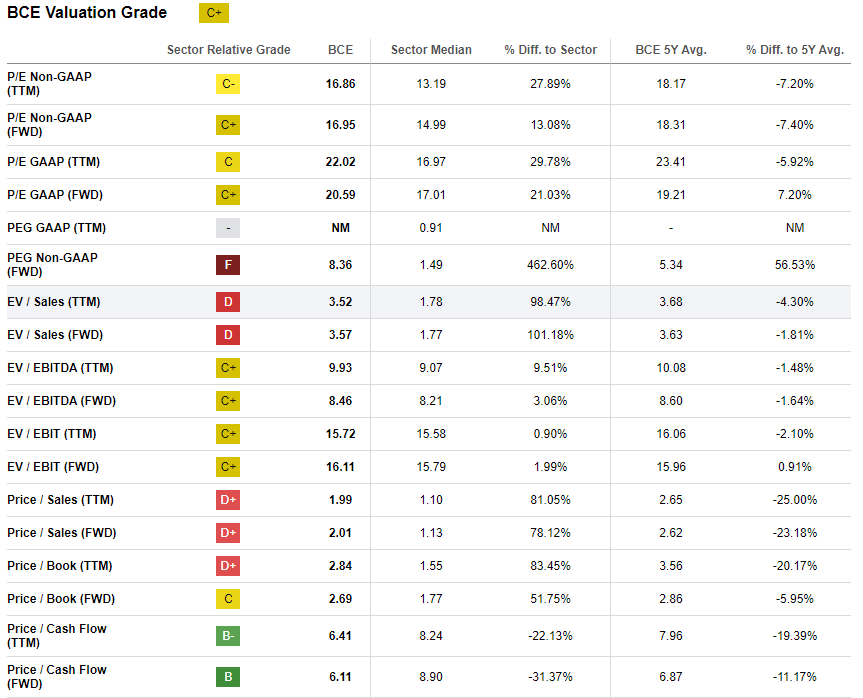

The stock price declined by 10% year-to-date, significantly underperforming the broader U.S. market. BCE also underperformed the iShares MSCI Canada ETF ( EWC ) this year. The current valuation ratios of BCE are slightly lower than the company's historical averages, which might indicate undervaluation. I do not compare BCE's valuation multiples to the sector median due to the company's unmatched dominant position in the Canadian market.

{kind=link}

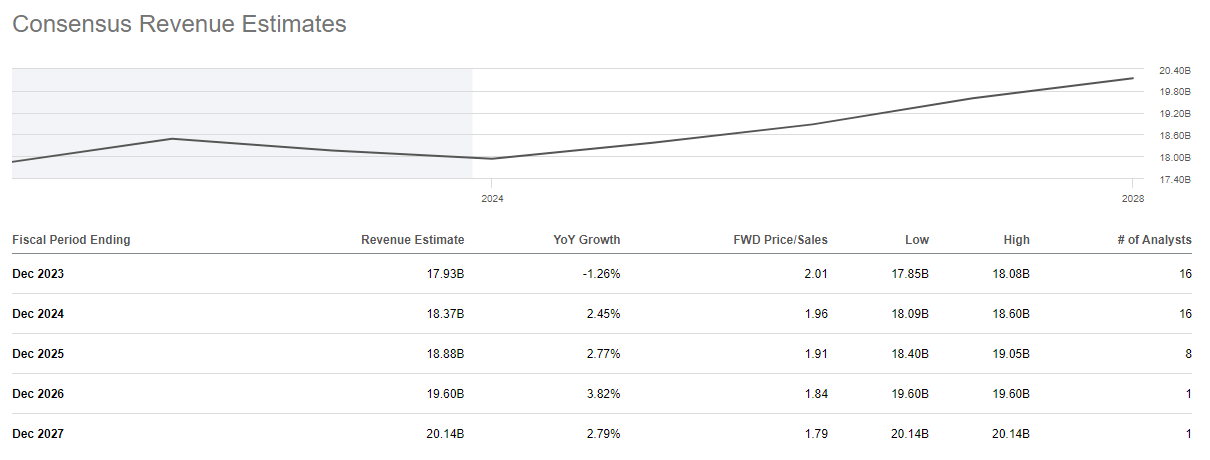

Since BCE is consistently paying out dividends and is considered a Canadian dividend aristocrat , I prefer to proceed with the dividend discount model [DDM] simulation. Consensus dividend estimates project an FY 2024 payout at $2.93, which I use for my DDM formula. I use the last decade's dividend growth rate, which is 2.16%. Given the company's dominant position in the Canadian market, I use a low 8% WACC for discounting.

Author's calculations

According to my DDM calculations, the stock's fair value is slightly above $50. This indicates a solid 27% upside potential for the stock price. Therefore, the stock is very attractively valued, especially considering also an above 7% forward dividend yield.

Risks to consider

Since my valuation analysis relies heavily on dividend growth, it is crucial to warn potential investors that the payout ratio is at 120%. The payout ratio above 100% means that the company is paying out more in dividends than it is earning. Having a payout ratio over 100% is not sustainable over the long-term horizon, and investors should be aware that there is a significant risk of struggles with dividend growth over the long term. On the other hand, it is essential to underline that the management targets to maintain a non-GAAP dividend payout ratio of 65%-75% of the FCF, which is sustainable but still has limited potential to expand significantly over the long term.

The stock does not look like a good bet for growth investors, given BCE's shale revenue growth prospects, which are projected by consensus. Investors seeking a high-risk, high-reward play with a moonshot capital appreciation will find the stock less appealing. Potential investors should understand and consider a conservative growth outlook when evaluating BCE for their portfolio. As BCE operates in a highly penetrated industry, it is difficult to expect rapid revenue growth for any of the industry players in the Canadian telecom market.

{kind=link}

Bottom line

To conclude, BCE is a "Buy". The stock is a good choice for investors who are seeking a low-risk and high-yield opportunity. The company's strong profitability and dominant positioning in the Canadian telecom industry give me high conviction that the current yield is safe. Moreover, the valuation looks very attractive, indicating a solid upside potential for the stock.

For further details see:

BCE: A Deep Value Play With An Above 7% Dividend Yield