RWAY - BDC Weekly Review: Why Are BDCs Issuing Expensive Debt?

2023-07-01 21:18:47 ET

Summary

- We take a look at the action in business development companies through the fourth week of June and highlight some of the key themes we are watching.

- BDCs reversed their rally as broader markets cooled from the recent strong run.

- BDCs have been issuing fixed-rate bonds at 8%+ coupons - a relatively high level over the past decade which can compress their net income if the Fed cuts rates.

- BXSL hiked the dividend by 10%, something we suggested was likely in the previous update.

This article was first released to Systematic Income subscribers and free trials on June 24.

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company ("BDC") sector from both the bottom-up - highlighting individual news and events - as well as the top-down - providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the fourth week of June.

Market Action

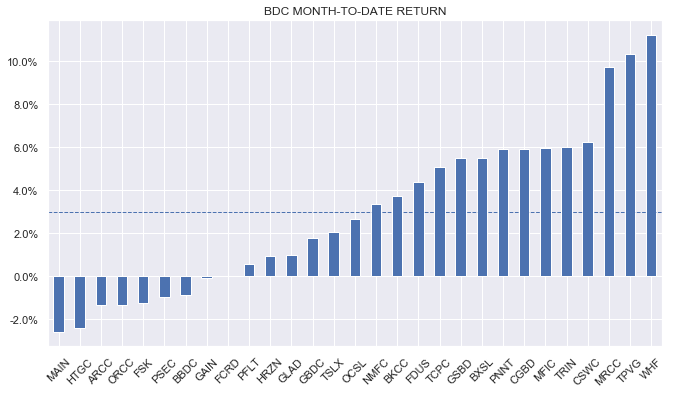

BDCs were down in the week with a total return of -3%. Only one stock in our coverage rallied - the Blackstone Secured Lending Fund ( BXSL ) - which hiked its dividend during the week.

Month-to-date, however, the sector is still up around 3% on the back of the recent improvement in risk sentiment.

{kind=link}

The average BDC valuation in our coverage fell to around 93%. This is close to 10% below the longer-term average and is in the fair-value range in our view.

Systematic Income

Market Themes

A theme we have noticed recently is that BDCs continue to issue bonds at current yields. For example, Saratoga ( SAR ) issued a 8.5% 2028 bond ( SAZ ) recently while Runway Growth ( RWAY ) issued an 8% 2027 bond ( RWAYZ ).

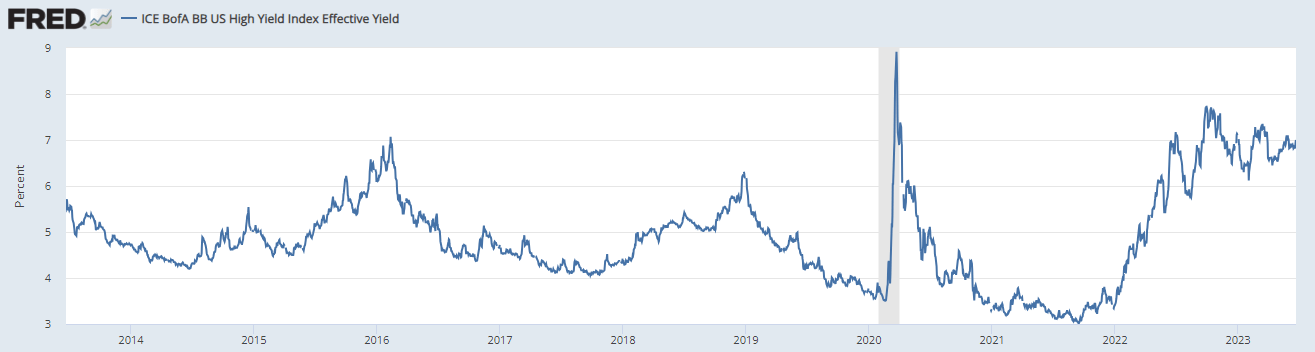

On the face of it, it seems odd that BDCs are happy to lock in a high level of interest expense. As the following chart shows, BB corporate yields (roughly where many BDC baby bonds would be rated) are trading close to their decade high levels.

{kind=link}

There are a couple of reasons why BDCs may be going down this path. One, is that while bond yields are high, the yields on credit facilities are not attractive at the moment given the steep inversion of the yield curve. The 1-month / 5-year Treasury yield curve is inverted by more than 1% which is 2% below its historic average. In other words, raising leverage via a credit facility is than 2+% more expensive than via a bond issuance in the context of historic norms.

Systematic Income

Can BDCs simply avoid adding new debt at current high levels? In some cases no, as existing debt is maturing. We should also remember that at current interest rates, issuing fixed-rate longer-duration debt while making new private loans at short-term rates is actually favorable from a net income perspective. This is because it takes advantage of the very inverted yield curve.

The key risk for BDCs is that short-term rates fall significantly, leaving them with high locked-in rates on the debt. That said, neither markets nor the Fed expect this to happen very soon. And even if it does, the amount of recent bond issuance is small.

However, if this trend of refinancing to higher longer-term interest rates continues and the Fed eventually moves the policy rate significantly lower, then we could see the risk of a sizable step-down in BDC net income levels for an extended period of time.

Market Commentary

As highlighted above, BXSL increased its dividend by 10% to $0.77. As we discussed in the last update, having coverage of 133% in an environment where short-term rates are still rising is not sustainable.

Our view was that the company would introduce a new supplemental dividend to protect its base dividend in the future, something they mentioned was important to them. Recall they had several special dividends shortly after the IPO in order to support the stock price through its lock-up expiries.

Instead they bit the bullet and just increased the base dividend despite some mild protestations previously. However given the continued increase in base rates, coverage should still be around 120% which will leave them a lot of room to hike in the future.

It’s also interesting that they decided to raise the dividend shortly after the Fed disclosed that they expect a couple of more hikes to come. This likely freed up management’s hand to raise as it became clear that short-term rates aren’t falling anytime soon.

The price got a nice pop yesterday on the news. The stock is trading at the highest valuation in over a year.

Systematic Income

It's also trading at a valuation more than 10% above the sector average (104% vs 93%).

Systematic Income

Unfortunately, the days when BXSL valuation traded at a discount to the sector, when we first allocated to it, may be behind us. We will likely look to rotate from BXSL to other more modestly high-performing companies in the coming days.

For further details see:

BDC Weekly Review: Why Are BDCs Issuing Expensive Debt?