BBBY - Bed Bath & Beyond Q3 Earnings: Worse Than They Look

Summary

- BBBY earnings were worse than expected, showing a large drop in revenue.

- The company has inventory problems and shrinking liquidity.

- Cashflow and liquidity burn were even worse than earnings because earnings were boosted by non-cash income.

- It seems unlikely that Q4 will be as good as hoped.

Bed, Bath and Beyond ( BBBY ) announced earnings for their fiscal third quarter, which ended 11/26/22 on January 10. The earnings were announced late - they were due on January 5, and so on January 5 the company announced that the earnings and the associated 10-Q would be delayed until January 10 and also gave a brief business update (the " 1/05 Update ").

On January 10, pre-market, the company did release earnings, in a press release (the " Announcement "), followed by a brief conference call (the " Call "). However, as I write, (around 11 pm NY time on Jan 12), the 10-Q has still not been filed.

Q3 results

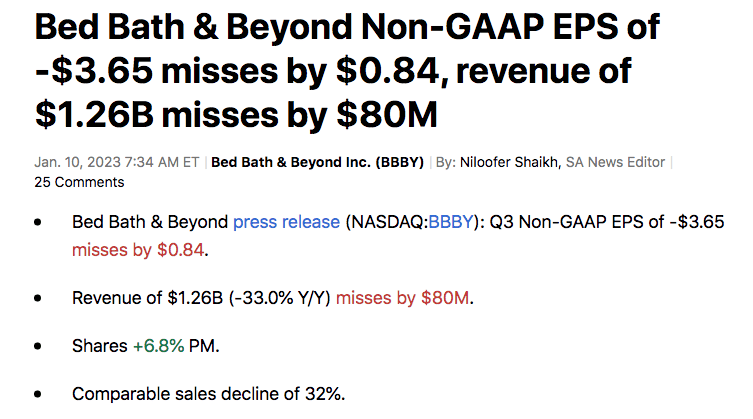

Third quarter is not traditionally BBBY's best quarter, but nor is it the worst. Their idiosyncratic fiscal year means the it includes Black Friday and half of the Thanksgiving weekend, but the rest of the holiday season is in Q4, of which more later. Analysts were expecting a $2.81 loss per share, but the results were much worse:

{kind=link}

BBBY Q3 results (Seeking Alpha)

In my opinion, the comparable sales number was worse news than the bottom line loss. This comparable sales number excludes the effect on sales of the on-going store closure program, emphasizing the problems with retaining customers and maintaining inventory referred to in the 1/05 Update.

{kind=link}

BBBY sales issues (BBBY SEC Filing)

The (not very palatable) icing on the cake was the comparable sales decline for the company's buybuy BABY brand (considered by some to be the company's crown jewel) "in the low-twenties percent range".

Non-Cash Income

An initial perusal of the Announcement shows one interesting anomaly. Operating cashflow was terrible. at negative $307.6 million. So was liquidity of $500 million (down from $850 million on 9/24 according to management on the Q2 conference call ). However the net-of-impairment loss of $292.2 million, while bad, looks less terrible, particularly when compared (as the company did in the 1/05 Update) to the Q3 '21 loss of $276.4 million. What explains this?

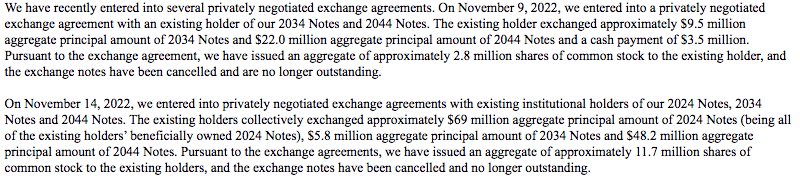

This posting is a follow-up to my recent article " Bed Bath & Beyond: Approximately 600 Million More Shares Available " wherein I pointed out that significant BBBY assets wholly were BBBY's treasury stock holdings (approximately 250 million shares) and BBBY's ability to issue, without shareholder consent, a further approximately 350 million shares. According to page 15 of a prospectus issued in November, BBBY has been using those assets to repurchase and retire some of its unsecured debt:

{kind=link}

BBBY Private Bond Exchanges (BBBY (SEC filings))

For our purpose, the important point of this disclosure is that various holders of BBBY's unsecured debt (the " Notes " they refer to) surrendered $$154.5 million which BBBY then cancelled. Cancellation or forgiveness of debt is, of course, considered as income. After an adjustment relating to the cash increment in the transaction and the 14.5 million shares issued to the Noteholders, BBBY recorded income (as "Gain on extinguishment of debt") of $94.38 million. However, (other than the relatively immaterial $3.5 million cash increment), this transaction helped only income, but not cashflow and so explains the anomaly. Without this, pre-impairment net loss would have been $386.58 million - more consistent with liquidity fall and cashflow deficit and much worse than Q3 2021 losses.

Effect and sustainability of the bond exchange transactions

There is one important positive from the bond exchange transaction. The Notes come in three maturities - 2024, 2034, and 2044. The 2024 tranche is crucial because it must be reduced to below $50 million by May next year in order to avoid acceleration or default of BBBY's up to $1.505 billion of secured debt. (Readers who wish to see a full explanation of this issue, together with links to all the relevant filings are referred to my October article " Bed Bath & Beyond: Potential Acceleration Of Largest Debt Tranche Could Cause Liquidity Crisis ".) The bond exchange reduced the 2024 tranche by approximately $69 million. However, according to the last data provided , the outstanding is still $215,403,000, so there is still a long way to go.

Can the bond exchanges continue, and would it help if they did? Cashflow is crucial for BBBY right now and, as discussed above, the bond exchanges do not really help with that. The interest saved on the canceled bonds certainly helps both income & cashflow, but even if the whole $1 billion of unsecured debt were cancelled, that's only $49 million annually of interest - hardly material for a company losing $300 million each quarter. And even if the bond exchanges could bring the remaining $215 million of the 2024 debt down to $50 million, that would only postpone the repayment of the secured debt to the currently scheduled 2026.

BBBY Unsecured Notes (BBBY SEC filings & author's calculations)

In my view, if BBBY could return to operationally cashflow positive, and if retail shareholders maintain their current level of enthusiasm, continuing bond exchanges could significantly help in returning the balance sheet to a state where lenders would consider refinancing or extending the 2026 scheduled debt facilities. The latter is unknowable, so let's look at the former.

Q4

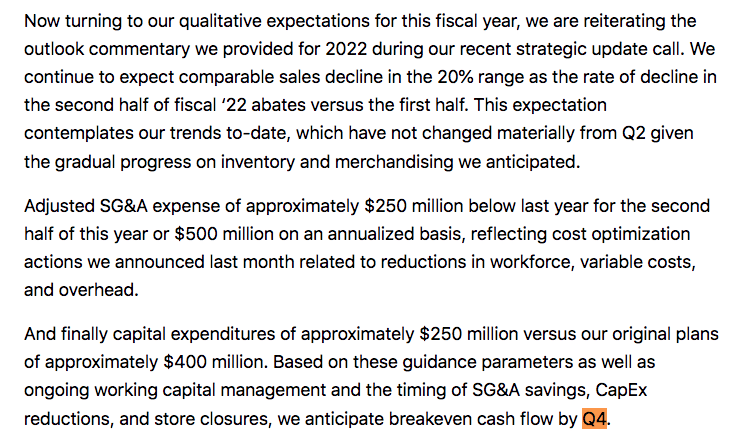

Q4, which extends for BBBY from 11/27/22 to 2/26/23, will be make-or-break for the company. This quarter encompasses Christmas, Cyber Monday, part of the Thanksgiving season, and the January sales. Since BBBY's troubles became widely known around August, the company has anticipated break-even operational cashflow in Q4. The CFO, Laura Crossen, said on the Q2 earnings call :

{kind=link}

BBBY CFO on 9/29 (SA Transcripts)

Of course, Q4 is not over, and we have no results yet. But the holiday portion of Q4 is the first half of Q4, which IS over, and so the company will have a pretty clear idea of how the quarter is going to turn out.

There have been no further references (that I can find) to break-even cashflow, and one very clear piece of evidence (not proof) that things are not going well.

I discussed the "going concern" language in both my previous articles " Bed Bath & Beyond: Approximately 600 Million More Shares Available " & " Bed Bath & Beyond: Potential Acceleration Of Largest Debt Tranche Could Cause Liquidity Crisis ", and I will not reiterate the whole discussion here. The important point to note is that the company made the, in my view, crucial change from "believes that cash [etc.]....should enable the Company to meet presently anticipated cash needs for at least the next 12 months" in the Q2 10-Q to "substantial doubt about the Company's ability to continue as a going concern" in the 1/05 Update, the holiday portion of Q4 was almost over. Is it likely, readers may wonder, that BBBY would have come to such a dire conclusion if Q4 as going as they hoped/anticipated?

Because BBBY declined to have the usual Q&A session on the Call, analysts were unable to ask questions about Q4. It is understandable that at this stage the company would prefer to release any Q4 information only in writing and after full review by lawyers & bankruptcy advisors.

Conclusion

I believe that the situation at BBBY is going from bad to worse, and I anticipate a bankruptcy filing in the near future. Investors with a high degree of risk tolerance AND sophistication should consider entering hedged short positions while the market capitalization continues to be at current elevated levels.

The reason why I specify hedged shorts is that unhedged shorts are exposed to (i) potentially unlimited loss whenever the stock spikes up (as we have seen over the last couple of days with the stock spiking back to levels last seen in October), and (ii) recall of the borrowed stock without notice (particularly likely in a stock where high turnover and low institutional holdings make share availability unpredictable). I would therefore prefer either short positions combined with OTM call options, or even better, option spread transactions like that outlined in my previous article. Of course, the limitation of risk with these hedged strategies will also reduce the potential reward.

For further details see:

Bed Bath & Beyond Q3 Earnings: Worse Than They Look