CA - Berkshire's Cash Cow: Year-End Check On BNSF

2023-12-20 00:11:52 ET

Summary

- Warren Buffett's investment in BNSF has been highly profitable, generating over $40 billion in free cash flow and sending over $50 billion to Berkshire Hathaway.

- BNSF's financial performance in 2023 has been impacted by lower freight volumes and higher operating costs, leading to a decline in operating revenues and earnings.

- Despite the challenges, BNSF has maintained a strong earning power and a solid ability to service its debt, making it a valuable asset within Berkshire Hathaway's portfolio.

Introduction

After going over the publicly traded Class 1 railroads, it is time once again to see how Warren Buffett's Burlington Northern Santa Fe ( BRK.A , BRK.B ) has performed so far. But, as we start to cover this topic, let's start with these words Buffett wrote in Berkshire Hathaway's 2009 shareholder letter:

In earlier days, Charlie and I shunned capital-intensive businesses such as public utilities. Indeed, the best businesses by far for owners continue to be those that have high returns on capital and that require little incremental investment to grow. We are fortunate to own a number of such businesses, and we would love to buy more. Anticipating, however, that Berkshire will generate ever-increasing amounts of cash, we are today quite willing to enter businesses that regularly require large capital expenditures. We expect only that these businesses have reasonable expectations of earning decent returns on the incremental sums they invest. If our expectations are met - and we believe that they will be - Berkshire's ever-growing collection of good to great businesses should produce above-average, though certainly not spectacular, returns in the decades ahead.

Thanks to these words, I started spending time reviewing and researching capital-intensive businesses, too. And, as some of my SA readers may know, Class 1 railroads caught my attention . I currently own a large position in Canadian National ( CNI ) and two minor positions in Canadian Pacific Kansas City Limited ( CP ) and Union Pacific ( UNP ), though with the latter I am a bit disappointed by mismanagement and hope the newly-appointed CEO Jim Vena can turnaround the company.

But I have built a mind frame to assess railroads and follow them by studying Warren Buffett and his investment in BNSF. So, even though this large Class 1 railroad is not publicly traded anymore, I keep track of it and share my updates on its performance to use it as a comparison against the other 5 publicly traded Class 1 railroads. This is even more interesting because BNSF has still not implemented PSR (precision scheduled railroading) and this leads to a different way of operating.

So, without further ado, as this year wanes, I want to go over the first nine months of BNSF and see what happened. We can do this both through the data BNSF itself shares and, most importantly, through Berkshire's reports.

Warren Buffett's investment in BNSF

When Warren Buffett came to realize how capital-intensive businesses can be very good investments, he soon added to Berkshire's portfolio (BRK.A, BRK.B) a Class 1 railroad: Burlington Northern Santa FE - BNSF. To know the full story of how Buffett came across BNSF, I suggest reading pages 9 to 11 of Berkshire Hathaway's 2021 shareholder letter.

Berkshire initiated its position in BNSF in 2007, and during that year's shareholder meeting, Buffett talked about this first purchase:

It will never be a sensational business. It's a very capital-intensive business. And when you put tons of capital out every year, it's very hard to earn really extraordinary returns on capital. But if they earn a decent return on capital, it can be a good business over time, and it can be a lot better business than it was in the past.

So, the issue of capital-intensive businesses was still there, but the way to overcome it is to understand if that use of capital can lead to a "decent return". Of course, over long periods of time, decent returns compound and generate great returns.

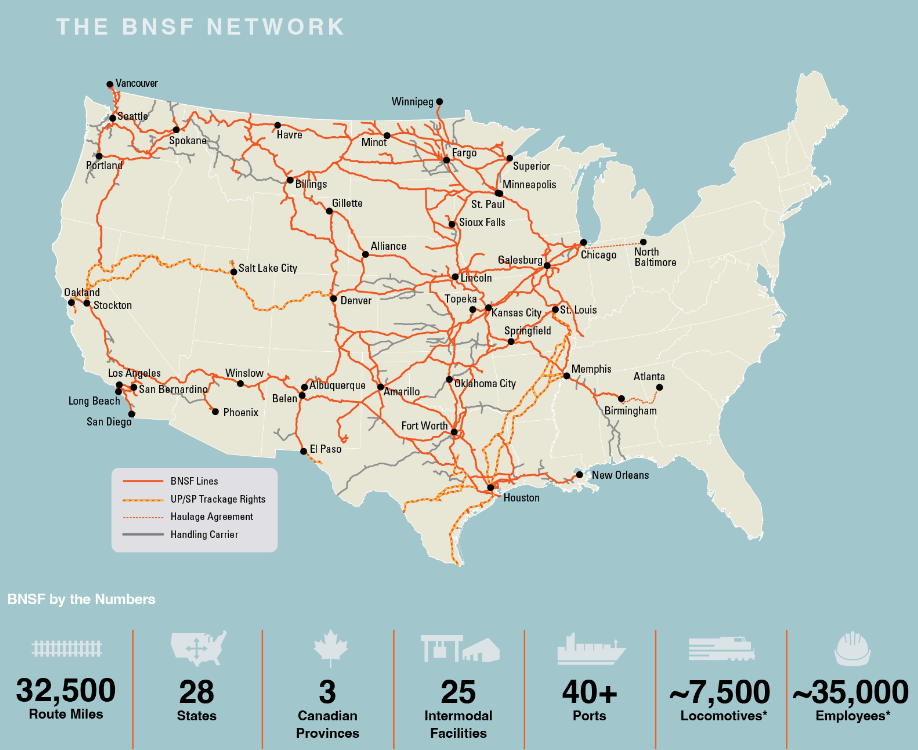

What strikes most is when Buffett decided to take hold of the entire company. In 2009, right in the middle of the Great Financial Crisis, he offered $26 billion to buy the remaining 77.4% of the company Berkshire still didn't own. The deal was signed, and Berkshire found in its portfolio a massive rail network of 32,500 route miles touching 28 states and three Canadian provinces, as we can see from the map below.

{kind=link}

In a 2010 shareholder letter, Warren Buffett pointed out three catalysts that made him bullish on railroads:

- cost and environmental advantages over trucks

- fuel efficiency which leads to lower operating costs

- increasing need for freight trains

Of course, given the nature of the business, a railroad needs massive investments for its network maintenance and enhancement. Buffett writes about this issue in the above-mentioned letter, talking about BNSF and MidAmerican Energy since they have common characteristics:

the huge investment they have in very long-lived, regulated assets, with these funded by large amounts of long-term debt that is not guaranteed by Berkshire. Our credit is not needed: Both businesses have earning power that, even under very adverse business conditions, amply covers their interest requirements. For example, in recessionary 2010 with BNSF's car loadings far off peak levels, the company's interest coverage was 6:1.

This is where I learned one of the key metrics I assess railroads with: earning power, calculated as pre-tax earnings over interest expense. Since then, you will always find in my articles on railroads a paragraph about this. It is highly important because the higher the ratio the more a company can withstand economic slow-downs without being in danger of not meeting its interest obligations. There are railroads with a ratio as high as 10, and, up until now, I haven't found one ever going below a 6. A 6 is still very high because it means a company's pre-tax earnings are six times as much as its current interest expense. In other words, its pre-tax earnings would have to decrease another 83% to match the current interest expense.

Regarding railroads being a regulated business, Buffett shared some thoughts. In fact, this issue may make many think railroads can't generate interesting profits because they are somewhat capped.

Both companies are heavily regulated, and both will have a never-ending need to make major investments in plant and equipment. Both also need to provide efficient, customer-satisfying service to earn the respect of their communities and regulators. In return, both need to be assured that they will be allowed to earn reasonable earnings on future capital investments. [...] Fulfilling our societal obligation, we will regularly spend far more than our depreciation, with this excess amounting to $2 billion in 2011. I'm confident we will earn appropriate returns on our huge incremental investments. Wise regulation and wise investment are two sides of the same coin.

These words show an important fact: Buffett's trust in America. In fact, the regulatory environment is in any case America, a favorable land for private enterprises and businesses. This allows an investor to know the regulator will usually allow a decent return as a reward for the services a railroad provides to the whole nation.

Capex needs to generate decent returns. There is no way around it. However, part of this return depends, as we have seen, on regulators. Therefore, a need for a "social compact" arises, as Warren Buffett explains:

Our BNSF operation, it should be noted, has certain important economic characteristics that resemble those of our electric utilities. In both cases we provide fundamental services that are, and will remain, essential to the economic well-being of our customers, the communities we serve, and indeed the nation. Both will require heavy investment that greatly exceeds depreciation allowances for decades to come. Both must also plan far ahead to satisfy demand that is expected to outstrip the needs of the past. Finally, both require wise regulators who will provide certainty about allowable returns so that we can confidently make the huge investments required to maintain, replace and expand the plant. We see a "social compact" existing between the public and our railroad business, just as is the case with our utilities. If either side shirks its obligations, both sides will inevitably suffer. Therefore, both parties to the compact should - and we believe will - understand the benefit of behaving in a way that encourages good behavior by the other. It is inconceivable that our country will realize anything close to its full economic potential without its first-class electricity and railroad systems.

In other words: a country that wants a lively economy can't go without railroads. As a result, it needs to regulate the business in a way that enables private enterprises to be rewarded. After all, railroads are the "circulatory system" of the economy.

One last note: railroads have a network and their geography is not neutral. In particular, geography and demography have to go together to assess a railroad's future. Buffett was aware of this when he explained how BNSF is set to benefit from the American population shifting to the West and to the South. Both regions are well-served by BNSF, as the map shown above proves. Again, back in 2010, Buffett wrote

Rail moves 42% of America's inter-city freight, measured by ton-miles, and BNSF moves more than any other railroad - about 28% of the industry total. A little math will tell you that more than 11% of all inter-city ton-miles of freight in the U.S. is transported by BNSF. Given the shift of population to the West, our share may well inch higher.

What to look for in a railroad

From Buffett's investment in BNSF, I learned the main assessing metrics of this business. We have already talked about earning power so that under any circumstance the company can service debt.

Secondly, Buffett looks at the company's efficiency. First and foremost comes the operating ratio. But a good proxy of this is a railroad's fuel efficiency because it shows if a company's fleet is aging well or not and if it is renewed and enhanced at the right pace.

Third, we need to look at how a railroad uses its capital. Though Berkshire has received for years inflows of cash paid in the form of dividends, capital-intensive businesses should not use their capital to reward shareholders directly as the most important thing. Much more important is how the network and the fleet are maintained and improved. In fact, by investing in its operations, a railroad can become more efficient and generate more free cash flow down the road.

I have shown elsewhere that a few Class 1 railroads have used their balance sheets to take on more debt to fund their share repurchases . While this may have worked for several years in a low-rate environment, it has now led most railroads to pause their buybacks. Only Canadian National, which has usually been rather conservative with its balance sheet, has now the strength to repurchase its shares , taking also advantage of a year where its stock price was a bit depressed until the yearend rally got triggered by the FED's pivot.

BNSF performance 2010-2022

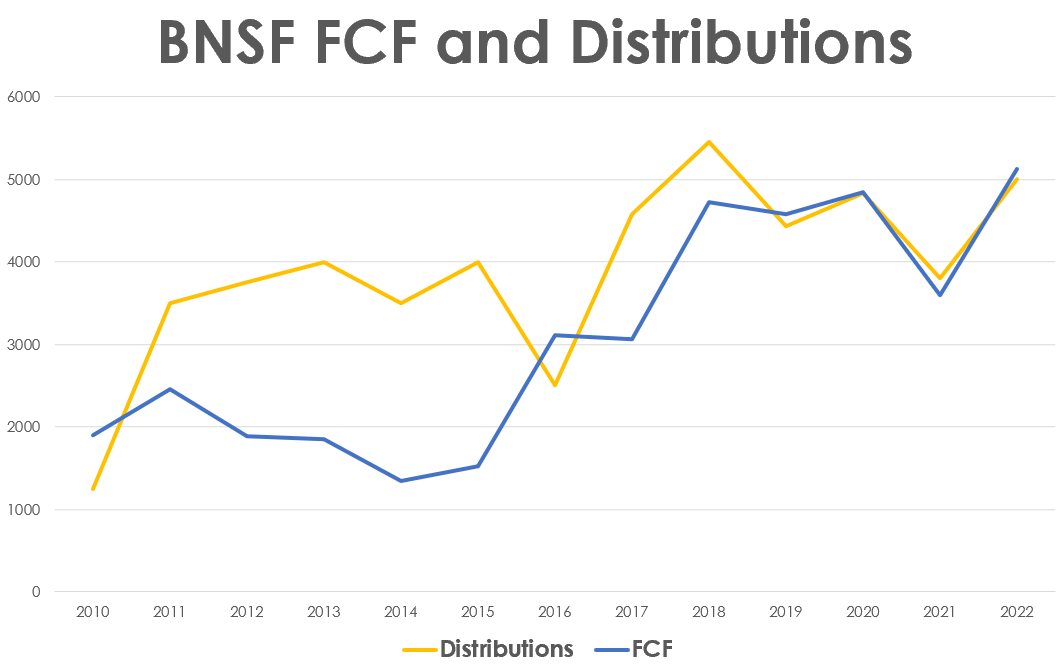

To get an idea of the total returns Berkshire has made thanks to BNSF, we can look at this graph I made.

{kind=link}

We see how BNSF has been a cash cow for Berkshire, generation $40 billion in FCF and sending to Berkshire over $50 billion. The difference of $10 billion comes from what happened between 2010 and 2015 when BNSF took on LT debt to raise additional cash to be distributed to Berkshire. The operation is quite simple: Berkshire moved some of its debt out of its balance sheet into BNSF's. Moreover, Berkshire has a higher return on capital than BNSF itself, therefore, the capital that was moved from BNSF to Berkshire has probably compounded better.

Considering Buffett spent around $33 billion for the acquisition, he has already been paid in dividends more than what he spent. In addition, he owns an asset whose worth could be around $100 billion, which is about 3x the original price.

Latest BNSF Financials

Let's now take a look at 2023 and how BNSF has performed in a tough environment for railroads. In fact, until September, rail traffic was down YoY and fuel surcharges were decreasing too, impacting the top line of every railroad.

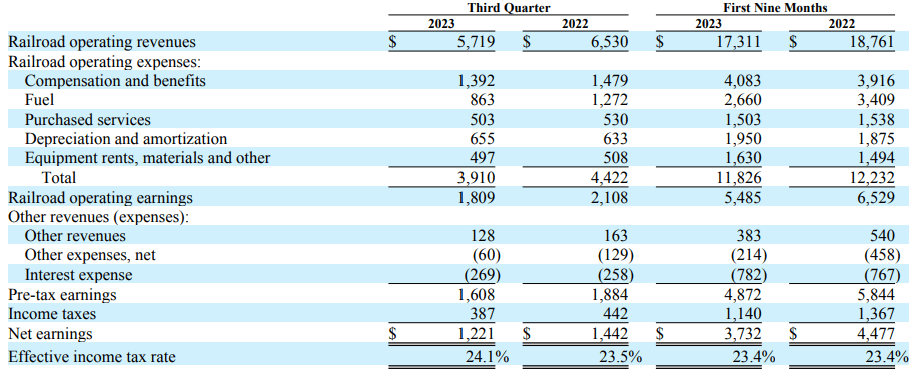

If we read Berkshire Hathaway's Q3 report , we find a lot of detailed financial data about BNSF.

In the first nine months of the year, BNSF's operating revenues declined to $17.3 billion from $18.8 in the prior year. This is a 7.73% decrease YoY.

If we look only at Q3, revenues were down even more: -12.4% to $5.7 billion from $6.5 in Q3 2022.

The decrease was attributable to lower freight volumes. But higher operating costs also kicked in, leading to an even bigger earnings decline. For the first nine months, BNSF's operating earnings were $5.5 billion vs. $6.5 billion reported in 2022. This is a 16% decline. These results mean in 2023 the operating profit was 31.7%.

Since, railroad operating expenses were $3.9 billion in the third quarter and $11.8 billion in the first nine months of 2023, we have an operating ratio of 68.3% for the first nine months. For the industry, it is rather high. Part of this is because BNSF has not implemented PSR yet, nor it seems planning to do so soon. Moreover, BNSF's traffic has a little issue. Much of it moves loads in one direction with empty cars returning (it is the case with crude and sand). This is why BNSF prefers investing in logistic centers, rather than in PSR.

Now, going back to our financials, as we move to the bottom line, BNSF's net earnings are down a bit more: -16.6% YoY. But for the quarter they are down a bit less: -14.3%.

{kind=link}

From this data, we can easily calculate BNSF's earning power. The company's 9M pre-tax earnings are $4.872. During the same period, BNSF paid $782 million in interest expense. This is a 6.2 ratio during a tough year for railroads, meaning the company can service well its debt.

Now, zooming in on BNSF's traffic, we see that over the first nine months, all four main segments were down, with a particularly strong decline in consumer products. According to Berkshire, BNSF's volume decreases were "primarily due to lower intermodal shipments resulting from reduced west coast imports, the loss of an intermodal customer and competition from lower spot rates in the trucking market, which has impacted our domestic intermodal demand".

Interestingly, in Q3, industrial products were positive YoY, though by just a hair (0.7%). This is another sign showing that manufacturing and industrial production seem to be gaining a bit of traction after very lull months.

{kind=link}

Overall, we are before an 8.7% volume decline YTD, with the good news Q3 was down only 4.8% and is thus actually contributing to improving this comparison.

With railroads, we have to take into account traffic cyclicality. What matters more is the average revenue per car. BNSF reported that in its case it decreased 7.1% in Q3. This was expected for two reasons: lower volumes mean car rates decrease because of lower demand and fuel surcharge revenues are down because of declining fuel prices.

Considering BNSF's balance sheet , we know that at the end of Q3, its outstanding debt was $23.5 billion, flat YoY. This makes sense even considering that, in June 2023, the company issued $1.6 billion of 5.2% debentures due in 2054, but during the same period, it repaid approximately $1.5 billion of term debt.

Regarding its cash flows, BNSF was able to generate $6.3 billion of operating cash. Subtracting $2.6 billion of capital expenditures, we have $3.7 billion in FCF over the first nine months of the year. This is further cash that will eventually be returned to Berkshire.

Peer comparison

Overall, BNSF performed in line with the industry and the railroad seems ready to catch increasing traffic as this year ends with an economy in better shape than previously expected.

But to get a real idea of how BNSF is performing we need to compare it to its other peers. More in detail, let's take a look at the industry through the lens of three of Buffett's metrics: earning power, operating ratio, and ROIC.

In the first nine months of this year, we see how Canadian National is on top of the industry, with the highest earning power, the best operating ratio, and the highest ROIC.

Norfolk Southern has performed very poorly because of the $1 billion impact linked to the Ohio incident.

BNSF seems to be performing more or less in line regarding its earning power. Its ROIC is rather good and it comes in second place. Regarding its OR, we have already said why it is closer to 70% rather than 60%.

| 9M23 |

| Earning Power |

| Operating Ratio |

| ROIC |

| CNI |

| 8.8 |

| 61.3% |

| 17.0% |

| CP |

| 5.0 |

| 66.4% |

| 7.7% |

| CSX |

| 6.2 |

| 61.4% |

| 6.2% |

| NSC |

| 3.2 (ex Ohio 5) |

| 77.5% (ex Ohio 74.6%) |

| 7.1% (ex Ohio 11.3%) |

| UNP |

| 6.0 |

| 62.8% |

| 10.4% |

| BNSF |

| 6.2 |

| 68.3% |

| 11.7% |

So, what should we think? Though it may have had a slower year, BNSF keeps on being able to run at a profit and make billions in FCF that will be returned to Berkshire. Though the company's efficiency may still improve, it keeps on being decent.

Considering we are before a railroad whose annual revenues should be around $23-25 billion, we can easily value the company at 4x its sales, which gives us a rough valuation of almost $100 billion.

We can't assess Berkshire with the sum-of-the-parts method because Berkshire simply owns too many businesses. But currently, Berkshire has a market cap of $785 billion and I would argue that BNSF alone can't be worth almost 13% of Berkshire. Therefore, though Berkshire is near its ATHs, I still think it trades at a very decent valuation and I keep on rating it as a buy.

For further details see:

Berkshire's Cash Cow: Year-End Check On BNSF