BKR - Berry Corporation: An Old Rig Rat Goes West

Summary

- Workovers using existing wellbores that do not require "new well" permitting are enabling a workaround to California's ban on permitting.

- Berry Corporation has the right management and physical assets to carry out workovers in-house.

- The company should be attractive at or just below current levels to investors looking for income.

Introduction

Berry Corporation ( BRY ) is ignored by the market because of its location. Quite honestly, if the company operated anywhere but California, its shares would be significantly higher. Move it to Peace River, the steam flood capital of Canada, and you would have a much higher price. Move it to West Texas and you'd have another HighPeak Energy ( HPK ). Even with all the enviro "rhetoric" companies have to trudge through in Canada and West Texas, it's way better in those places than in California. But, in California, it is stuck and recently one of its big fund investors pulled the plug. Oaktree Capital bailed with a buyout from BRY itself.

{kind=link}

Who knows why Oaktree wanted their money back, but speculation that they were tired of getting bashed by their investors about the nasty oil BRY produces, likely wouldn't run amiss.

I think they missed a bet, and will tell you why.

The short story is I think BRY is attractive near current prices and has implemented a strategy to successfully navigate the perilous political environment in California. It started with hiring Fernando Araujo a couple years back. Then they bought their own well servicing company in 2021 out of the C&J bankruptcy . When you put Araujo with a well servicing company, you have a winning combination

Management matters

Fernando Araujo is moving up to CEO, and that prompted me to take a deeper look into his background. I knew he was ex-Schlumberger ( SLB ), but that only begins to tell the tale. If you were looking for a CEO - as BRY obviously was - to guide Berry through the next few years, the search would deliver him. Every time. Here are the bullets from his LinkedIn profile:

- Executive Director SLB Production Management

- President and GM of Apache Canada

- Asset Team Leader-Repsol-Egypt

- Shell Production Engineer-Bakersfield, Cali

Araujo knows production and well stimulation, and that's exactly how BRY will maintain production until permitting loosens up, as I believe it must.

Well servicing

If you have been a reader of my work for any amount of time, you know that bringing in a well is a tricky business. Sometimes things don't go as planned and you have to fix a broken well. That falls under the remit of well servicing. There is also the aspect of applying chemical treatments to stimulate well production. You could also pick up drill pipe to drill to a new spot. And, that is the key to the program. I will explain.

Here's a dirty little secret about oil production-particularly in California. There hasn't been much technology applied to it. Kern county-where most of the production is just missed out on being an oil sands mining operation, similar to Canada. The oil in California's Kern River Basin is buried just deep enough that it's accessed with "post-holes" about 1,200-1,500' in true vertical depth typically. Drilled with the cheapest mud - a little clay for viscosity, some caustic soda to raise the pH, and maybe a little barite to get the weight up for hole stability ( I know this from personal experience ) and completed with a perforated liner-a piece of casing with holes in it, you can get a gravel pack that consists of little more than dumping sacks of sand down the well. I am exaggerating that last part but not by much .

Here is a what I envision to be a typical workover scenario. A reservoir engineer determines that a few hundred feet away from an existing completion, there is essentially "virgin" reservoir that hasn't been properly stimulated by steam. The answer is to P&A the existing completion, set a plug and kick-off a "sidetrack" to this pristine section of the reservoir. Apply just a teensy bit of modern technology and you essentially have a new well. Using the original wellbore enables this sidetrack to be accomplished for a fraction of the cost of the new drill, but the key is that permits for workovers are much easier than for new drills. Fernando Araujo, CEO discusses workovers in the Q-3 report:

In Q3, we allocated additional resources to workover activity, which is our most efficient use of capital. So far this year, we have completed 235 workover jobs with a rate of return greater than 100% for the program. We have a lot of wells in California, a lot of them are going to be hopefully destined to work over activities or sidetracking activities. I don't have that number yet but it's in the hundreds.

Workover permitting

Araujo confirmed in the Q-3 call that the company is getting workover permits from CalGEM with 50 in hand, and another 150 in the permitting process. Araujo expressed confidence that as a combination of workovers, and sidetracks, it would be able to carry out its 2023 program to maintain output.

We have been getting permits for workover activity and sidetrack activity with no issues at all. For our 2023 activity, we have received over 50 permits in California. So we have got those secured. And in addition to that, we have submitted on the order of 150 permits that will be approved by CalGEM over the next few weeks and months. So we have got plenty of permits in hand and submitted to be able to take care of our 2023 activity and beyond. So in short we don't expect to have any issues with permits in order to execute our 2023 program.

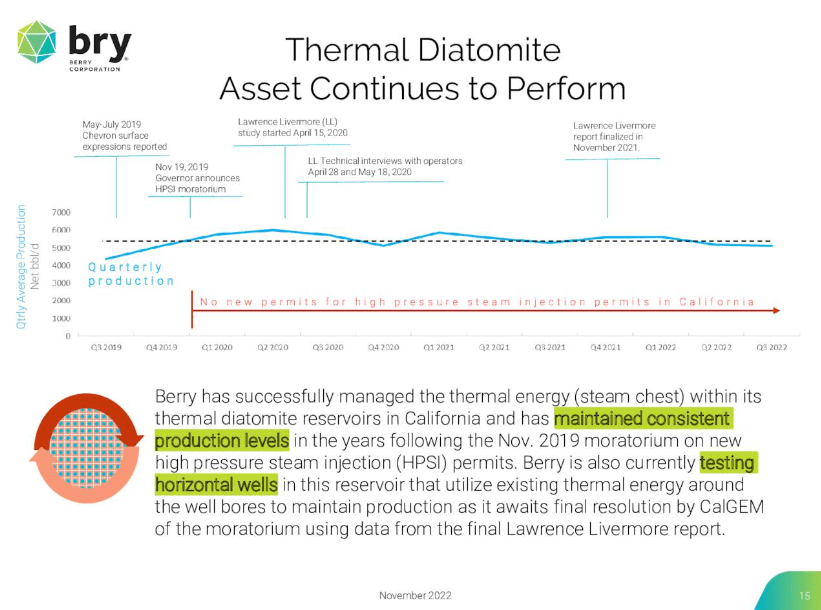

The Thermal Diatomite Experiment

In 2019 California stopped issuing new permits for "steam fracking." This was a major deal for BRY as the Thermal Diatomite is a core asset. The company has managed to side-step the full impact of this decision by drilling a couple of horizontal wells that use existing thermal energy in the reservoir. The company report success in this novel approach to producing this asset.

{kind=link}

According to Araujo , the concept has been proven and the company will be optimizing this technique:

We have secured permits to drill additional wells next year and we will be testing different theories around lateral direction, landing zone and other issues as well.

And then at the same time, we are also evaluating additional technologies to be able to produce the Thermal Diatomite resource, which is a huge resource that we have in our field. So the results so far are very good and we will be following up those results with activity next year.

I can only speculate what these other technologies might be. My first thought is solvent/surfactant techniques. Baker Hughes ( BKR ) has some very effective chemistry that might be employed here. Micro-Cure has been used successfully to reduce viscosity and boost production. Other service companies also have chemistry to attack this problem.

The larger point here is that BRY has engineered their way around an obstacle meant to shut them down. This is a good step that enables continued production from the key resource for the foreseeable future.

The reason to invest in Berry

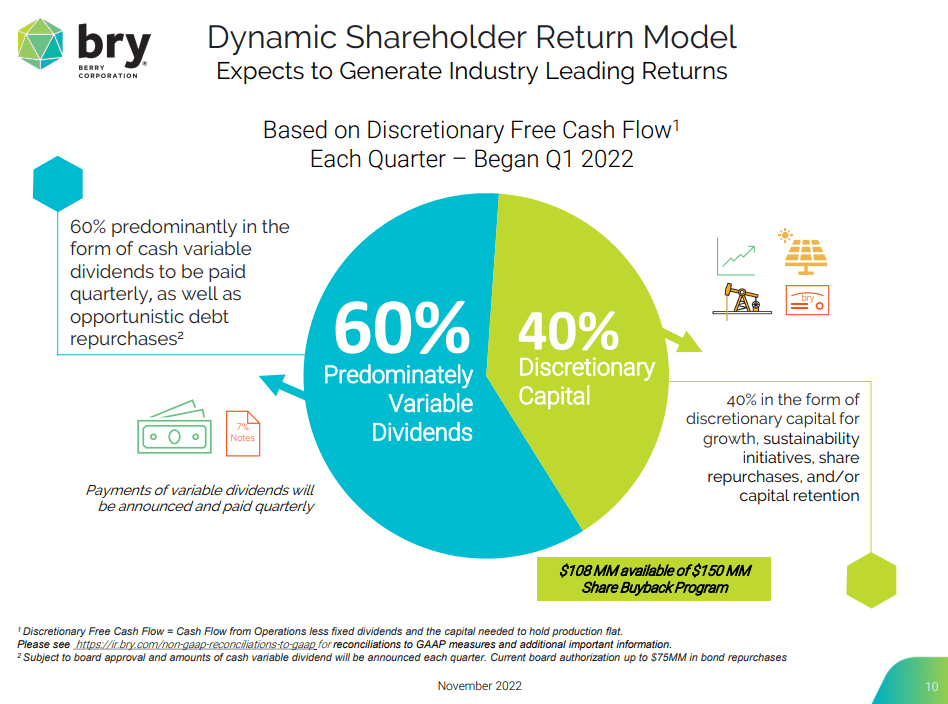

This is it. At least in the short term. Over the next three years, at current Brent prices, Berry expects to deliver the current capitalization of the company back to shareholders. From that point, you're riding free.

{kind=link}

We all need income. It's the reason a lot of us are here. It was my reason for beginning this blog, and I expect the outsize returns that oil investments have brought in recent years, are the reason many of you follow along.

I think there is also a scenario that at some point-I have no idea when, the market will revalue the company higher based on its reserves and production. On a flowing barrel basis, BRY trades far under other producers at $36K per flowing barrel. Another California discount. For reference most of the Permian shale players are trading in the $90,000's or more per flowing barrel.

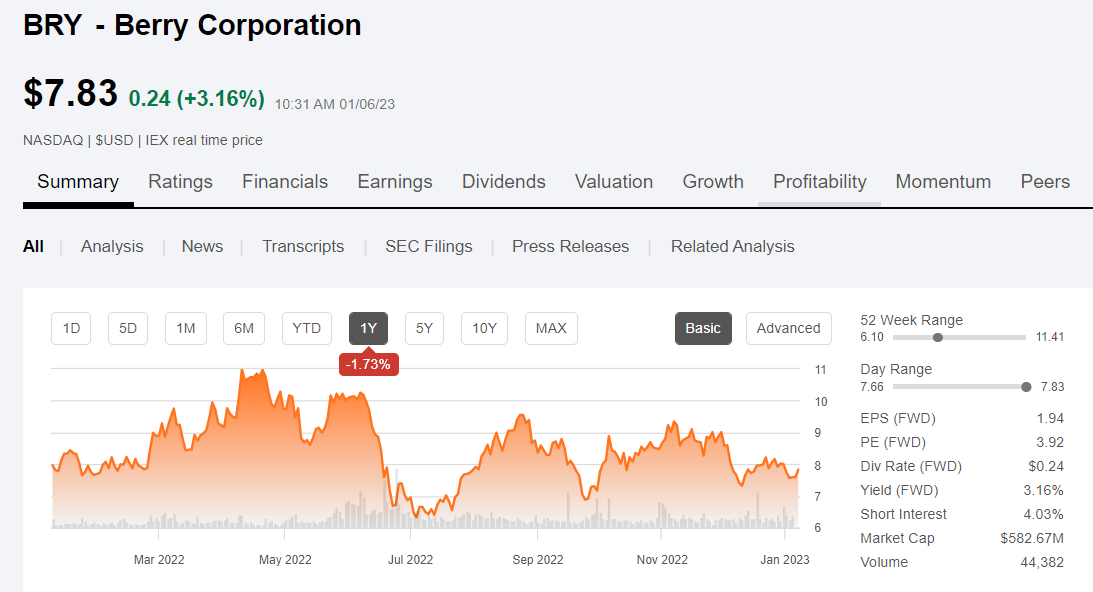

I wouldn't hold my breath waiting on BRY to get a higher multiple. It's traded between the mid-$11's and the mid-$6's over the last year, pretty much in line with spikes in Brent. If trading is your thing, that's a pretty good range. Largely though I am presenting BRY as a reliable dividend payer.

Risks

Let's face it, the current political leadership of California is implacably opposed to oil production, even having set a date for phasing it out completely in 2045 . This is pure fantasy in my humble estimation. It will never happen, but we are still stuck with it putting a damper on shares of BRY. The good news is it's largely priced in, in my view.

Permitting could also get worse. I don't really know how, but the intrepid Governor of the Bear State seems to make the rules as he goes along, and nothing is off the table really. If he has Liverwurst for lunch one day...who knows?

Finally, Berry is a child of higher prices for cash flow. It's faced considerable fluctuation in input prices to run steam generators, and has taken steps to control this cost. Moving its Uinta production to Kern is an outstanding adaptation to circumstances in my view. BRY also has hedges in place to control costs.

{kind=link}

Your takeaway

Berry Corporation generated $95 mm in OCF for Q-3, 2022. I expect realizations will be down 10% in Q-4, in line with mid-$80's Brent that's prevailed for most of Q-4, 2022. This probably accounts for the decline in the share price as much as anything else, as it will impact the size of the variable dividend to be announced in early Feb, 2023. The company is trading at less than 3X OCF, which is a substantial discount to peers.

My guess is the variable dividend will come in at $0.35-38 for this quarter, which if my thesis about a rebound in oil prices in Q-1, 2023 comes true, will represent the bottom. When you add the fixed dividend of $0.06 in we should net $0.42-3 for a roughly 5.3% yield on cost. Later quarters should be more reflective of Q-3 where the combined payout was $0.47.

I don't know if this yield alone is enough to justify investing, given this week's T-bill rate is 4.5% . Given that, if you are considering Berry, you need to have a longer view toward a time, perhaps not that far in the future, when the market properly values its production. Higher oil prices will improve the payouts, compensating you for risk if you enter in the sub-$7.00 range.

The stock has been holding in the high $7's pretty solidly, so opportunities for significantly lower prices appear limited. I haven't let that keep me from putting in an "end of the world" buy order at $6.5 per share. If I see it dip toward $7.00 I would probably adjust this order to the market to close the deal. I consider BRY a long term position in my portfolio and would like more-at the right prices.

In summary, I am convinced that a Berry Corporation plan that was put into place several years ago with the hiring of Araujo and the acquisition of C&J Well Servicing is a viable one that will keep production at current levels. This provides a bridge to a time when sanity returns to California's plans for oil-as I believe it must. A tall order I know, but craziness has its limits. Even there. I hope.

For further details see:

Berry Corporation: An Old Rig Rat Goes West