XOM - BGR: This High-Performing CEF Might Be Worth Consideration

2023-03-06 08:14:35 ET

Summary

- The traditional energy sector has greatly outperformed the market over the past year.

- BGR invests in a portfolio of energy stocks to provide income to its investors, although it has very heavy exposure to only a few names.

- The fund has slightly underperformed the U.S. energy index over the past year but the difference was not that great when you consider the higher yield paid by the CEF.

- The fund generated more than enough money to cover its distributions over the past year and appears to be on a financially strong footing.

- The fund is currently trading at a discount to the net asset value.

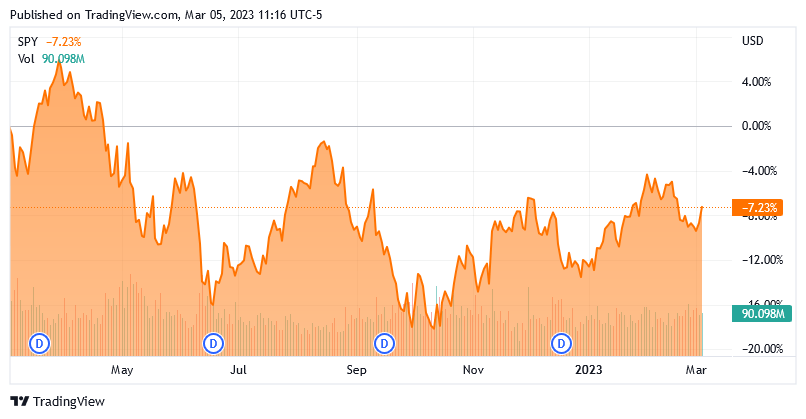

It is unlikely to be a surprise to anyone that the market has delivered a rather disappointing performance as of late. This is evident by looking at the S&P 500 Index ( SPY ), which is down 7.23% over the past year:

{kind=link}

However, some sectors have performed better than others. For example, the traditional energy sector which includes most oil and gas stocks has performed remarkably well over the period due mostly to high energy prices and improving capital efficiency that has resulted in remarkably high profits and cash flows for many of the companies in the sector. Unfortunately, it can be difficult to assemble a diversified portfolio of these companies without having access to an enormous amount of capital. One easy solution to this problem is to purchase a closed-end fund that focuses on investing in the energy sector. These funds are admittedly a somewhat underfollowed asset class, which is unfortunate because they provide investors with access to a diversified portfolio of assets that can in most cases deliver a higher yield than any of the underlying companies possesses. They also enjoy the benefit of professional management, which sets them apart from index funds and most exchange-traded funds.

In this article, we will discuss the BlackRock Energy and Resources Trust ( BGR ), which is one energy-focused closed-end fund. This fund currently boasts a 6.12% yield, which is quite likely to be attractive to many investors that want to generate some income from their portfolios. I have discussed this fund before, but a few months have passed so naturally, a few things have changed. In particular, the fund finally released its annual report so we will get an updated analysis of the fund's financial performance. This is always important for obvious reasons. Therefore, let us proceed onward and see if this fund could be a good addition to your portfolio.

About The Fund

According to the fund's webpage , the BlackRock Energy and Resources Trust has the stated objective of providing its investors with a high level of total return through a combination of current income, current gains, and long-term capital appreciation. The fact that this fund focuses on total returns is not particularly surprising considering that it is an equity fund. We can see this in the fact that fully 98.07% of the fund consists of common stock:

CEF Connect

The reason that a focus on total return is not particularly surprising considering this is that common equities are by their nature a total return vehicle. After all, most people that purchase common stock do so in an attempt to receive both dividend income and capital appreciation. Most stocks in the energy sector certainly deliver in this respect as we have seen companies such as Pioneer Natural Resources ( PXD ) and Devon Energy ( DVN ) pay out much of their free cash flow to investors as dividends over the past year or two, causing these stocks to deliver remarkably high yields even as their share prices appreciated in reaction to their improving financial performance. While we do see capital appreciation in many other sectors, we rarely see such a focus on paying out 75% or more of free cash flow as dividends among other sectors of the market.

As the name of the BlackRock Energy and Resources Trust implies, the fund can invest in natural resources companies in addition to traditional energy firms. The website specifically states that "the trust seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its total assets in equity securities of energy and natural resources companies and equity derivatives with exposure to the energy and natural resources industry." This description could therefore theoretically allow the fund to invest in things such as iron ore mines, nickel producers, or even lithium producers. However, currently, the fund is almost entirely invested in traditional energy companies as 97.37% of its assets are in this sector:

CEF Connect

We do see a very small exposure to companies outside of energy here, but that still fits in with the fund's description. Basic materials companies can be considered natural resources companies and we still see more than 80% exposure to the energy and natural resources sector in aggregate. For the most part, though, we should consider this to be a traditional energy fund, despite the fact that the description implies otherwise.

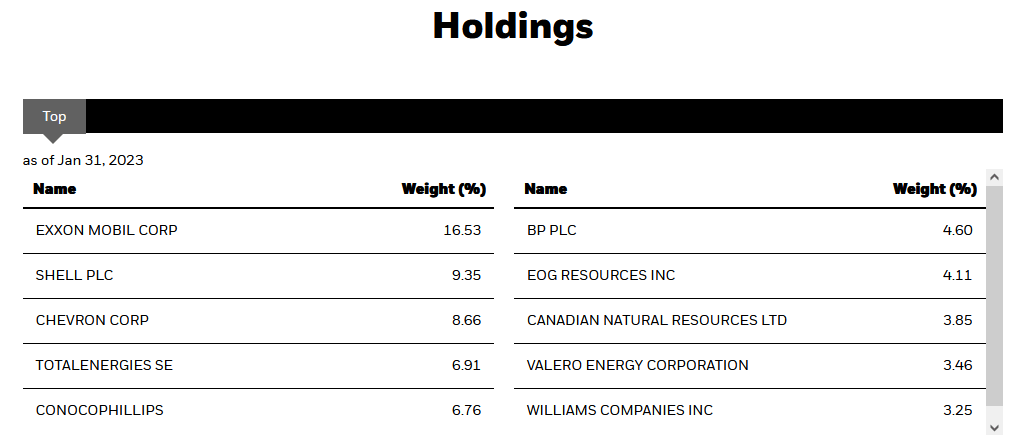

As would likely be expected, the largest positions in the fund are occupied by companies in the fossil fuel energy industry:

{kind=link}

As long-time readers are no doubt well aware, I have devoted a considerable amount of time and energy toward discussing traditional energy companies here at Seeking Alpha over the past several years. This includes most of the companies on the above list. Indeed, Valero Energy ( VLO ) is the only company that I have never written about. It is the only pureplay refiner on the list, which is rather nice as we see a nice combination of integrated majors, upstream producers like ConocoPhillips ( COP ) and EOG Resources ( EOG ), a midstream company in The Williams Companies ( WMB ), and a downstream company in Valero Energy. Thus, we do see all three segments of the fossil fuel energy company represented here. With that said though, it would be nice to see some smaller producers represented here as some of them could offer better opportunities than the giant integrated firms. Admittedly, though, it is rare to see the shale producers and other small independents among the largest positions in any energy fund so their absence here is not a complaint specific to this fund.

As my long-time readers on the topic of closed-end funds are no doubt well aware, I do not generally like to see any individual position in a fund account for more than 5% of the fund's total assets. This is because that is approximately the point at which the asset begins to expose the portfolio to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, then it will not be completely diversified away. Thus, the concern is that some event may occur that causes a company's stock price to decline when the market in aggregate does not and if that company accounts for too much of the portfolio, then it may end up dragging the entire fund down with it. As we can see above, there are five companies that each account for more than 5% of the portfolio, and one of them is well over three times that level. Thus, any potential investor in this fund should be willing to take on the risks of these companies individually before taking a position in the fund.

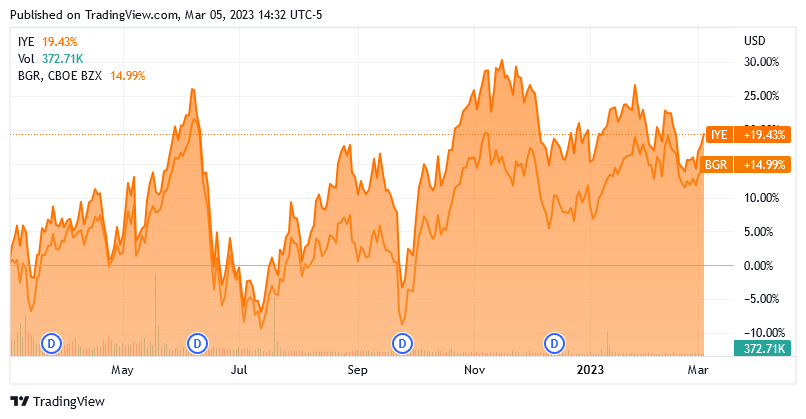

There have been surprisingly few changes to the largest positions list since we last looked at the fund in October. The only major change is that Enbridge ( ENB ) was removed and replaced with Valero Energy. Naturally, though, the weightings that each company represents in the portfolio have changed, but this can easily be explained by one stock outperforming another in the market. The fact that, overall, there have been relatively few changes here could lead one to believe that the fund has a very low turnover. However, the BlackRock Energy and Resources Trust had an annual turnover of 61.00% last year. That is about average for an equity closed-end fund, but it is substantially higher than an index fund. The reason that this is important is that it costs money to trade stocks or other assets, which is billed directly to the fund's shareholders. This creates a drag on the fund's performance and makes it more difficult for management. After all, the fund's management will need to deliver sufficient excess returns to cover the trading expenses and still provide the investors with an acceptable return. This is a very difficult task that very few management teams are able to consistently accomplish. This fund is no exception as the BlackRock Energy and Resources Trust did underperform the iShares U.S. Energy ETF ( IYE ) over the past year:

{kind=link}

With that said, the closed-end fund does have a much higher yield, which closes the gap between the two funds somewhat. An investor in the index fund would still have slightly more than any investor in the closed-end fund if both of them purchased the same amount at the same time a year ago, however.

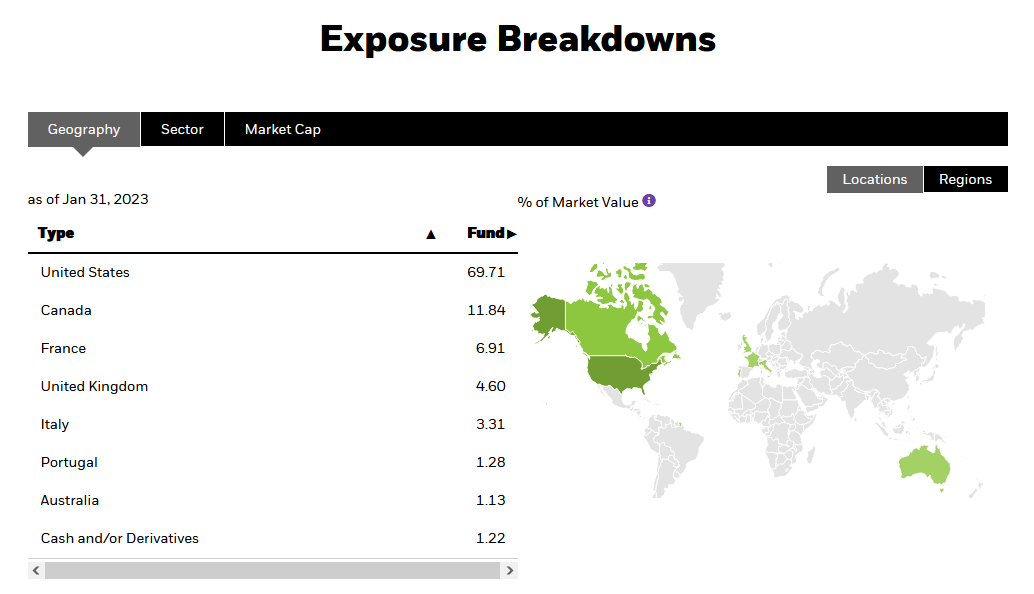

With that said, the closed-end fund and the index fund are not perfectly compatible. One reason for this is that the BlackRock Energy and Resources Trust is a global fund. We can guess this considering that there are several foreign companies on the largest positions list. In fact, only 69.71% of the fund is invested in American companies:

{kind=link}

The United States only accounts for a bit less than 25% of the global gross domestic product, so the fund is still substantially overweighted to this country based on its actual representation in the global economy. However, some of the companies that occupy a large weighting in the fund, such as Exxon Mobil ( XOM ) and Chevron ( CVX ) have sufficient operations outside of the United States that they provide a certain amount of international diversification that is not reflected simply by looking at their national origin. The reason why international exposure is important is because of the protection that it provides against regime risk. Regime risk is the risk that some government or other authority will take some action that has an adverse impact on a company that we are invested in. The only real way to protect ourselves against that risk is to ensure that only a small proportion of our portfolios is exposed to any individual nation. This fund is accomplishing that to a limited degree, but investors will still want to make sure that they have sufficient foreign exposure from elsewhere in order to be properly diversified.

Distribution Analysis

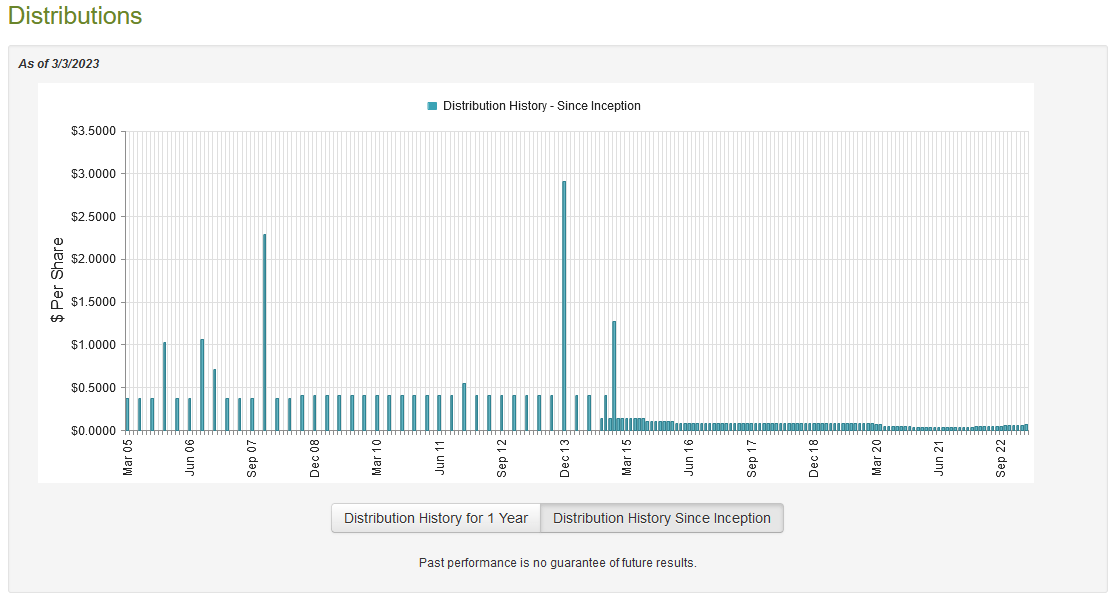

As mentioned earlier, there are several companies in the energy industry that have opted to pay out a large proportion of their cash flow to their investors in the form of dividends. This is due at least in part to the market not properly rewarding fossil fuel companies for their strong financial performance in recent years. In fact, as I have discussed previously , pretty much everything in the energy industry is undervalued today. This has resulted in these companies boasting fairly impressive yields. As of the time of writing, the iShares U.S. Energy ETF yields 3.39%, which is not too bad in today's environment. However, the BlackRock Energy and Resources Trust has the generation of current income and current gains as one of its investment objectives so it does even better as it can collect these high yields and also pay out capital gains. It currently pays a monthly distribution of $0.0657 per share ($0.7884 per share annually), which gives it a 6.12% yield at the current price. The fund has, unfortunately, not been particularly consistent with its distribution over the years:

{kind=link}

The fact that the fund's distribution varied quite a bit over the years is unlikely to be surprising considering that we have seen some fairly wide swings in crude oil prices over the past decade. It did increase its distribution three times in the past twelve months though, so its recent distribution history is not too bad. The fund may still lack a certain amount of appeal for an investor that is seeking a stable and secure source of income to use to pay their bills. However, anyone buying the fund today will receive the current distribution at the current price, so the fund's history is not exactly the most important thing. Thus, we want to investigate how well the fund can afford its current distribution.

Fortunately, we do have a very recent document that we can consult for this purpose. The fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. This is a much more recent report than we had available the last time that we looked at this fund and it should give us a great idea of how well it handled the volatile market conditions in 2022. During the full-year period, the BlackRock Energy and Resources Trust received a total of $16,828,579 in dividends. Once we net out foreign withholding taxes, we see that the fund brought in a total income of $15,983,162 from its portfolio. It paid its expenses out of this amount, which left it with $12,071,039 available for shareholders. That was not nearly enough to cover the $16,501,763 that the fund actually paid out in distributions during the period, however. At first glance, this is likely to be somewhat concerning as the fund is not producing enough income to cover its distribution.

However, the fund does have other methods through which it can earn the money that it needs to pay out the distribution. For example, it might have a substantial amount of capital gains. As might be expected from the strength in the energy sector last year, the fund was quite successful at this. It reported net realized gains of $34,809,940 and had another $66,906,553 in net unrealized gains. That was more than enough to cover the distributions and still gave the fund a great deal of money left over. After accounting for all inflows and outflows, the fund's assets increased by $84,989,114 during the full-year period. Thus, the distribution appears to be quite safe. The fund is on very strong financial footing.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Energy and Resources Trust, the usual way to value it is by looking at the net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of March 3, 2023 (the most recent date for which data is currently available), the BlackRock Energy and Resources Trust had a net asset value of $14.43 per share but the shares traded for $12.89 each. This gives the shares a 10.67% discount to the net asset value at the current price. That is relatively in line with the 10.18% discount that the shares have had on average over the past month. Overall, the price seems quite reasonable here.

Conclusion

In conclusion, the BlackRock Energy and Resources Trust appears to be a reasonable way to invest in the energy industry and generate a relatively high yield at the same time. With that said, it would be nice if the fund had a bit more exposure to some of the high-performing and yielding shale producers as these companies might deliver a better total return than the major integrated firms that account for a large proportion of the portfolio. Overall, though, this fund has delivered a similar total return to the American energy index over the past year and the fact that it is trading at a discount only adds to its appeal. It might be worth considering today.

For further details see:

BGR: This High-Performing CEF Might Be Worth Consideration