RTX - BIL And The Inflation Outlook: Unpacking The December FOMC Meeting Minutes

2024-01-04 14:44:31 ET

Summary

- The FOMC minutes reveal a focus on managing inflation and achieving long-term objectives.

- Participants view the policy rate as likely at or near its high, leaving the option for further hikes but with a base case of no further hikes and possible easing.

- Committee sees economy slowing and job market cooling off, but relieved by weakening inflationary pressure and balanced jobs market.

The Fed minutes were released yesterday, January 3rd, and they provide a lot of background information on the interest rate decision made by the FOMC in December. The gist of it is widely reported, but I think it is worth reviewing the minutes yourself, given it was viewed as a pivotal meeting.

The FOMC continues to focus on managing inflation and achieving its long-term objectives(i.e., 2% inflation and full employment). The December meeting notes lean more optimistic regarding inflation (which isn't surprising, as it has been trending down without abate).

It is much clearer compared to the prior meeting that participants view the policy rate as likely at or near its high. The market inferred this from Powell's press conference and immediately started pricing in by buying up bonds. The committee is leaving itself the option to continue hiking if inflation starts trending in the wrong direction, but the base case is now clearly for no further hikes and possible easing.

In terms of the economy, the FOMC generally views the economy as slowing and likely to continue to slow. The members also view the job market as cooling off. But they don't seem worried about employment. It's more that they seem relieved this inflationary pressure is weakening and the jobs market is now more "balanced."

In general, I do view the committee as very focused on inflation, and if it starts trending upward again, I think it is very unlikely they would make cuts while that's happening.

Something that stood out to me in particular was this observation by the Fed's staff:

The risks around the forecast for economic activity were viewed to be tilted to the downside. In particular, the additional monetary policy tightening that could be put in place if upside inflation risks were to materialize, with the potential for a greater tightening of financial conditions, represented a downside risk to the projection for economic activity.

Basically, they are calling out their own tightening as introducing an asymmetric economic risk. I interpreted this as a warning further tightening could really hurt the economy. Especially in scenarios where inflation comes back, the expected response could really hurt their projections. This implies they don't think wrongly easing is as great a risk at this stage.

The FOMC also reviews what the stock market did after its last meeting, what junk & investment grade bonds did as well as how bonds behaved. In that light, I thought the following passage was interesting as well (emphasis mine):

Many participants remarked that an easing in financial conditions beyond what is appropriate could make it more difficult for the Committee to reach its inflation goal. Participants also noted other sources of upside risks to inflation, including possible effects on global energy and food prices of geopolitical developments, a potential rebound in core goods prices following the period of supply chain improvements, or the effects of nearshoring and onshoring activities on labor demand and inflation.

Then there's this passage where the members discuss their dot plots and why they believe it is likely appropriate to start easing in 2024 (the market appears to be pricing in a lot more easing).

In their submitted projections, almost all participants indicated that, reflecting the improvements in their inflation outlooks, their baseline projections implied that a lower target range for the federal funds rate would be appropriate by the end of 2024. Participants also noted, however, that their outlooks were associated with an unusually elevated degree of uncertainty and that it was possible that the economy could evolve in a manner that would make further increases in the target range appropriate.

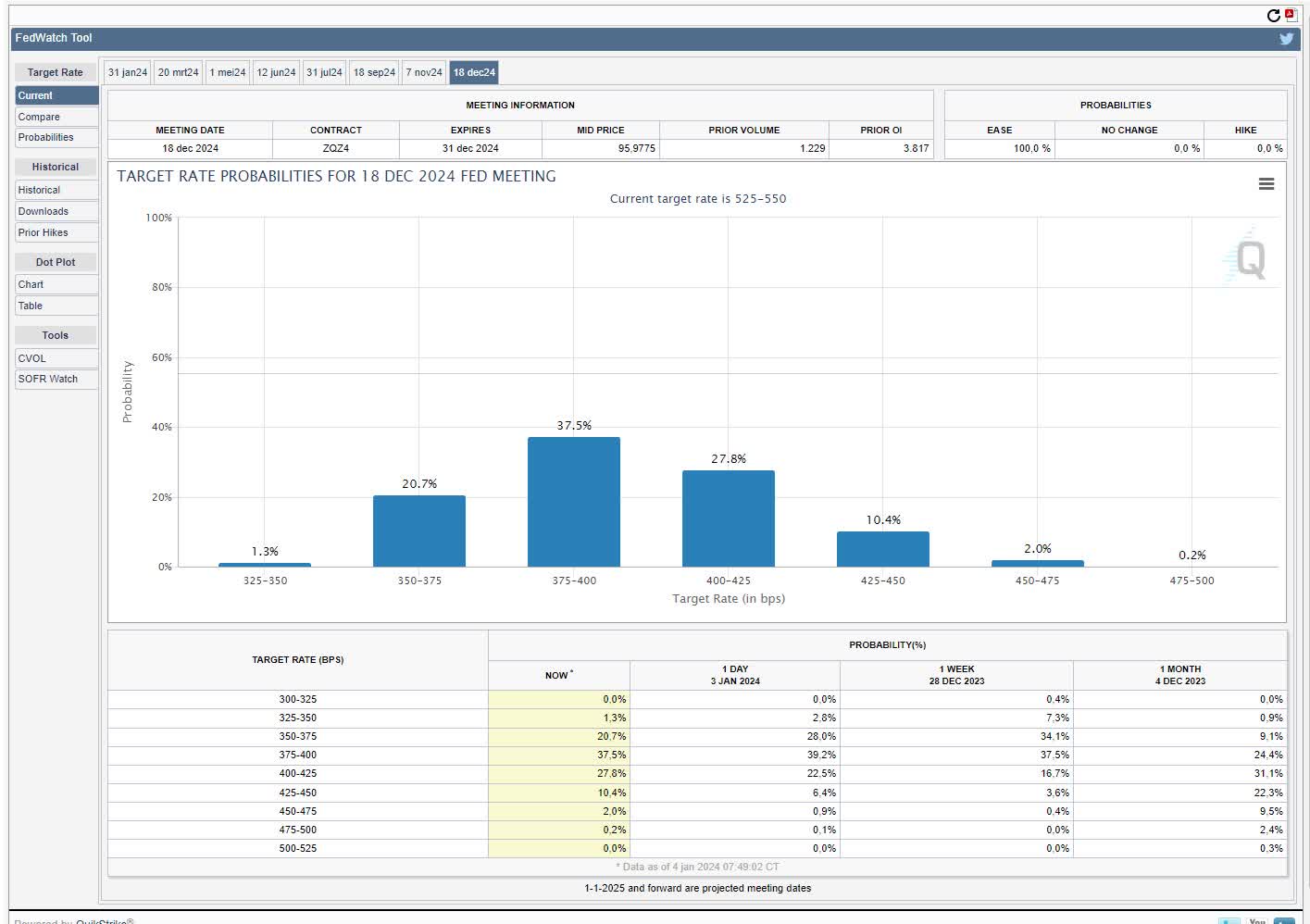

This is notable because the CME FedWatch Tool basically puts a probability of 0% on the Fed funds having increased by the end of 2024:

{kind=link}

To be fair, the meeting was more tilted toward participants, carefully advocating for a "higher-for-just-a-little-longer" policy, like here:

A number of participants highlighted the uncertainty associated with how long a restrictive monetary policy stance would need to be maintained, and pointed to the downside risks to the economy that would be associated with an overly restrictive stance.

It is not just interest rates that participants started to think about easing though. At the last press conference, Fed Chair Powell sort of highlighted the continued run-off of the balance sheet as evidence they're still tightening in effect, and I came away with the impression this was likely to continue. The minutes show that that's not all that certain:

These participants suggested that it would be appropriate for the Committee to begin to discuss the technical factors that would guide a decision to slow the pace of runoff well before such a decision was reached in order to provide appropriate advance notice to the public.

I've recently written a few articles about bond positions. In December, I favored the short end because the yield is relatively high and it is comparatively attractive vs junk bonds, investment grade or long bonds given these all have much larger credit and interest rate risks. That said, duration risk could be attractive because when the Fed pivots (and it sort of has) the trend tends to turn the other way. The rate cuts priced in by the market seem aggressive but historically Fed cutting is fast and furious. It's not a slow process where they're cutting 25bps at a time.

In the last few years, there has been a lot of talk about supply chains and how this sent inflation screaming higher (and then lower). Now we're dealing with Panama canal issues and Red Sea issues , and this could result in renewed supply chain pressures or at least higher freight rates as ships are taking alternative (longer) routes.

Overview global shipping locations (Marinetraffic.com)

{kind=link}

Energy prices also seem to have more upside risk because of the unrest in the Middle East. In the last few days, it has been trending up. My personal view is that oil prices are an underestimated component of inflation. At the same price, we're at current prices because OPEC has chosen to restrict supply. It is politically increasingly difficult for OPEC countries to restrict supply further but comparatively easy to increase production. I'm also inclined to believe Red Sea disturbances are going to be addressed vigilantly by lots of different countries and shouldn't lead to permanently elevated energy prices. At the same time, it is always possible the Israel-Palestine conflict will broaden. To me, it's not a base case.

I'm less convinced about the prospects of long bonds. Especially 10yr and up after reviewing the minutes and the recent Red Sea news and oil prices moving strongly upwards.

Here is the current yield curve vs historical yield curves:

U.S. yield curve (Investing.com)

{kind=link}

It still seems to me like short-dated bills are the best spot(that's why it was among my top-5 positions for 2024 ). The downside is you could hold something better. However, 1-3 month bills are yielding well above 5%. The SPDR® Bloomberg 1-3 Month T-Bill ETF ( BIL ) offers a yield-to-maturity of 5.38%. There is minimal risk (credit or interest rate). Sure, with bonds you can make more if interest rates are eased. The problem is that you likely take losses if cuts don't materialize while you're receiving less interest payments.

High-yield bonds are another reason why I like T-Bills. If you look at the iShares iBoxx $ High Yield Corp Bd ETF ( HYG ), it offers a SEC yield of 7.27% vs 5.19% for BIL. It has an expense ratio of 0.49% vs 0.14% for BIL. Is the ~2% extra worth all the extra credit and duration (duration of 3.36) risk? The market thinks so, but T-Bills just look so juicy in comparison. Perhaps it won't last long... That's the reinvestment risk. So far the yield curve has remained inverted for quite some time now.

I'm staying bullish on short-term paper after seeing the minutes. I own the SPDR® Bloomberg 1-3 Month T-Bill ETF with an expense ratio of 0.1356%. Duration of 0.14 and holding U.S. treasury bills with the associated negligible credit risk. I haven't made up my mind on longer-term bonds definitely yet (see my article on the 10-year of 2 weeks ago here ), but with the inverted curve, the price for that uncertainty seems quite favorable.

For further details see:

BIL And The Inflation Outlook: Unpacking The December FOMC Meeting Minutes