WVE - Biogen: LAQEMBI's $10 Billion Potential

2023-11-29 15:00:01 ET

Summary

- Biogen's latest Alzheimer's drug, Aduhelm, faced challenges after FDA approval, leading to concerns about efficacy and high costs.

- Biogen and Eisai's latest FDA-approved lecanemab faces similar risks; as a result, shares are down over 20% year-over-year.

- Biogen continues to trade at a significant discount to mid-sized pharmaceuticals despite a solid drug pipeline and its long-term potential from LAQEMBI.

Biogen (BIIB) is a global biotechnology company that focuses on the development and commercialization of therapies for neurological and neurodegenerative diseases. It is known for its work in the field of neuroscience and has been a key player in developing treatments for conditions such as multiple sclerosis ((MS)) and Alzheimer's disease.

One of Biogen's most important and well-known drugs is "Aducanumab," more commonly known as "Aduhelm." Aduhelm is indicated for the treatment of Alzheimer's disease. It is a monoclonal antibody designed to target beta-amyloid plaques, which are abnormal clumps of protein that accumulate in the brains of individuals with Alzheimer's disease.

However, after the FDA approval of Aduhelm, Biogen faced controversy due to concerns about the drug's efficacy, high cost, and the adequacy of clinical trial data. As a result, Biogen scaled back its marketing efforts for Aduhelm almost entirely. The challenges facing its most promising drug, might not have come at the best time for Biogen, since most of the company's top-selling products are in decline due to fresh competition.

Since reaching a high of over $400 post-approval, the stock has declined by nearly 50%, with investors expressing concerns about the drug's rollout and the company's future growth drivers. However, given its recent FDA approval of the promising Alzheimer's drug 'lecanemab', Biogen's growth drivers may be underestimated going forward.

Earnings Overview

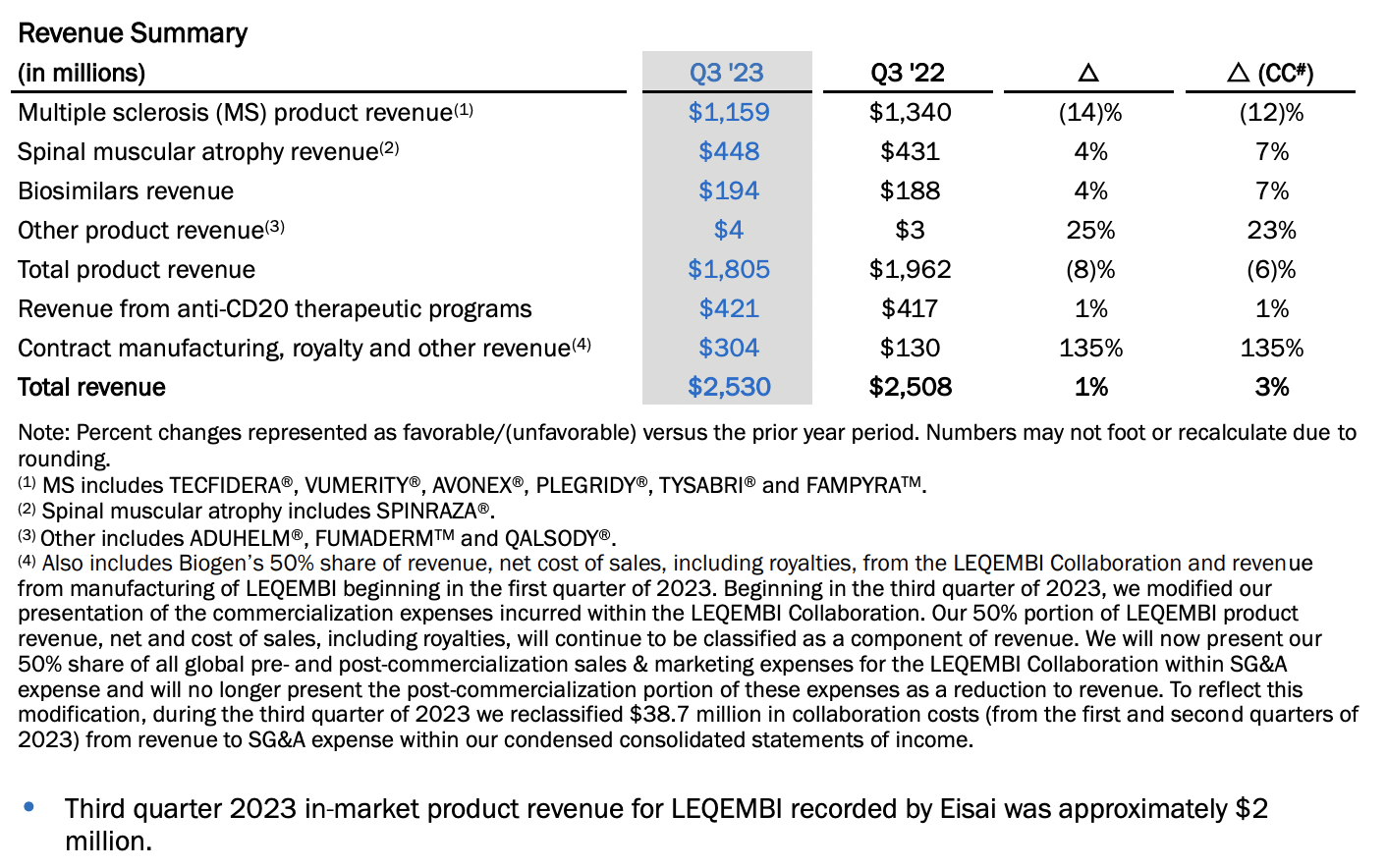

Biogen's total revenue in the third quarter of 2023 was $2.53 billion, beating estimates by $130 million and showing a year-over-year increase of 0.8%. Biogen's Q3 Non-GAAP EPS was $4.36, surpassing expectations by $0.37. The company's FY23 outlook indicates an anticipated low-single-digit percentage decline in total revenue year-over-year. It also lowered its projected Non-GAAP EPS for the fiscal year is between $14.50 and $15.00, compared to the consensus estimate of $15.23.

Biogen's free cash flow remained healthy in Q3 with a net cash flow from operations of $592 million. Capital expenditures amounted to $74 million, resulting in a free cash flow of $518 million. As of September 30, 2023, there was $2,050 million remaining under the share repurchase program authorized in October 2020.

{kind=link}

Biogen's most prominent drug group, multiple sclerosis, saw revenues decrease by 14% year-over-year (YoY), while spinal muscular atrophy revenue and biosimilars revenue each increased by 4% YoY. Other product revenue saw a 25% increase, which includes its previously approved Alzheimer drug 'Aduhelm', although it constitutes a minor part of the total revenue.

Most notably, contract manufacturing, royalty, and other revenue surged by 135%, which includes Biogen's 50% share of revenue from the LEQEMBI Collaboration with Eisai ( OTCPK:ESAIY ). Still, the increase from LEQEMBI was not sufficient to offset its total product revenue, which decreased by 8% in total.

Drug Pipeline Update

Biogen's promising drug pipeline spans various therapeutic areas, including Alzheimer’s Disease and Dementia, Neuromuscular Disorders, Neuropsychiatry, Specialized Immunology, Neurovascular, Parkinson’s Disease and Movement Disorders, and Genetic Neurodevelopmental Disorders.

1. ZURZUVAE for post-partum depression (approved in the U.S.):

Biogen and Sage Therapeutics ( SAGE ) recently announced that the U.S. Food and Drug Administration (FDA) has granted approval to ZURZUVAE (zuranolone) 50 mg, a novel treatment for adults with postpartum depression (PPD). With the extensive prevalence of PPD, affecting hundreds of thousands of women, and the treatment priced at $15,900, ZURZUVAE's market potential is projected to spiral into the hundreds of millions in terms of revenue.

2. Alzheimer's Disease and Dementia - Aducanumab (Phase 4) :

Aducanumab has the potential to generate up to $10 billion in annual sales. Competitors include Eli Lilly ( LLY ) with Donanemab and Roche Holding AG ( OTCQX:RHHBY ) with Gantenerumab.

3. Neuromuscular Disorders - Tofersen (Phase 3) :

The market for Tofersen is estimated to be $200 million to $1 billion. Competitors include Wave Life Sciences ( WVE ) and Roche Holding AG with their respective ALS therapies.

4. Specialized Immunology - Dapirolizumab pegol (Phase 3) :

The market for Dapirolizumab pegol is estimated to be $1 to $3 billion. Competitors include GlaxoSmithKline ( GSK ) with Benlysta and AstraZeneca ( AZN ) with anifrolumab.

5. Neuropsychiatry - ZURANOLONE (Phase 3) :

If approved, Zuranolone addresses a $2 to $5 billion market. Competitors include Sage Therapeutics and Johnson & Johnson ( JNJ ) with esketamine.

6. Neurovascular - BIIB131 (Phase 2) :

BIIB131 targets a market, which is estimated to be worth $1 to $4 billion. Potential competitors include Genentech (Roche) with alteplase as well as Boehringer Ingelheim with tenecteplase.

7. Parkinson’s Disease and Movement Disorders - BIIB122 (Phase 2): The potential addressable market is estimated to be between $3 to $7 billion. Competitors in this area include Denali Therapeutics ( DNLI ), and Pfizer ( PFE ) with their LRRK2 inhibitors.

Valuation

During the Biotech Bubble in 2015, Biogen's market cap briefly surged above $100 billion, trading at roughly 9x Price to Sales. While the company's sales were increasing quickly at the time, its valuation significantly contracted since then and now trades at a similar valuation level to 2011. Thus, Biogen currently trades at just 3.3 times Price to Sales, and just 2.3 times Price to Book, as most of Biogen's profits have been booked to its balance sheet.

While Biogen may not appear particularly cheap compared to big-pharma companies such as Pfizer, Bristol-Meyers Squibb ( BMY ), or Gilead Sciences ( GILD ), trading at even lower multiples, I consider Biogen a mid-cap pharmaceutical due to its relatively low revenue of $10 billion and headcount of just 9000 employees. Compared to large-cap pharmaceuticals it is therefore more capital-light, which is also visible in its margin profile, with EBITDA margins in the range of over 50% in the past few years. This is comparable to companies such as Vertex Pharmaceuticals ( VRTX ) and Regeneron ( REGN ) as demonstrated in the chart above.

Its EBITDA margins have recently dropped due to its acquisition-related charges incurred in connection with the recent acquisition of Reata ( RETA ), including stock-based compensation expense associated with the accelerated vesting of stock options previously granted to Reata employees. It also incurred higher R&D expenses related to the LEQEMBI Collaboration and approximately $37 million in close-out costs relating to the EMBARK trial for ADUHELM. Furthermore, restructuring costs pressured its recent EBITDA margins.

However, over the long term, I believe that Biogen should be able to return to EBITDA margins of over 40%. Furthermore, due to Biogen's relatively low market cap of just $33 billion, it is easily digestible by big pharma. For example, AbbVie agreed to acquire Allergan ( AGN ) for $60 billion in 2019. As mergers and acquisitions (M&A) continue to be prominent , Biogen could potentially be an acquisition target.

Since Biogen never paid a dividend its cash flows were booked to its balance sheet, which has continuously grown over the years. Recently, Biogen utilized some of its cash to acquire Reata Pharmaceuticals for $7 billion in cash. The deal will give Biogen control over Reata's recently FDA-approved "Skyclarys", the first drug approved to treat Friedreich's ataxia ((FA)) in adults and adolescents aged 16 years and older. With an impressive price tag of $370 thousand, the drug could generate up to $1 billion in sales. Nevertheless, Biogen will also aim to increase shareholder value through stock buybacks. Here, Biogen still has over $2 billion left from its $5 billion share repurchase authorization in 2019.

Takeaways

The euphoria of the approval of LEQEMBI has already faded, before Biogen even began commercializing the treatment. After all, LEQEMBI remains the only FDA-approved treatment for Alzheimer's, with cases expected to more than double by 2050. While growth from LEQEMBI may be slow in the beginning as the drug continues to roll out, it could generate over $10 billion in sales for Biogen and Eisai. I believe, at Biogen's current valuation, the potential success of LEQEMBI and pipeline candidates is not fully appreciated by the market.

For further details see:

Biogen: LAQEMBI's $10 Billion Potential