BNGO - Bionano Genomics: A Noble Cause But A Bad Investment

2023-07-24 14:15:58 ET

Summary

- Bionano Genomics, a company that develops technology for cancer research and diagnosis, is burning through cash at an unsustainable rate, despite its high revenue growth.

- The company's total addressable market is too small to create value for shareholders, and it faces high technological risk from current and potential competitors.

- Despite being an industry leader in sales and technology, Bionano's gross margin does not match the sector's benchmarks, and I see no catalysts that could significantly alter its current situation.

Sometimes analyzing a stock can be quite challenging, especially when it comes to expressing a recommendation. But there are times, such as with Bionano Genomics ( BNGO ), when it seems quite straightforward to land on a firm opinion.

Indeed, this company is admired for the technology it has developed and its contribution to science - we're talking about a group of true innovators capable of bringing a product to market that could significantly change the world of cancer research and diagnosis, as well as other genetic diseases. Having said that, there's an important distinction between an intriguing research project and a for-profit corporation that needs to generate value for its shareholders.

Bionano Genomics has already been selling its products on the market for several years. However, despite a high growth rate, revenues remain exceedingly low, and the company is burning through cash at an unsustainable rate. I have no hesitation in assigning a SELL rating to Bionano shares, a judgment based on:

-

A Total Addressable Market ((TAM)) too small to allow the company to create value for shareholders, even under the best circumstances;

-

High technological risk, tied to competition from both current and potential players;

-

A gross margin that does not keep pace with the sector in which the company operates, deviating substantially from the medical equipment industry benchmarks;

-

A lack of catalysts that could significantly alter even one of the points mentioned so far.

As much as I would like to be wrong, I seriously doubt that I am. However, I hope that through an acquisition or other extraordinary operations, Bionano will continue to operate in the future and strengthen humanity's fight against some of the diseases we are still least capable of tackling.

The Business Model of Bionano Genomics

To explain Bionano Genomics' business model to an investor audience rather than researchers, some scientific simplifications must be made.

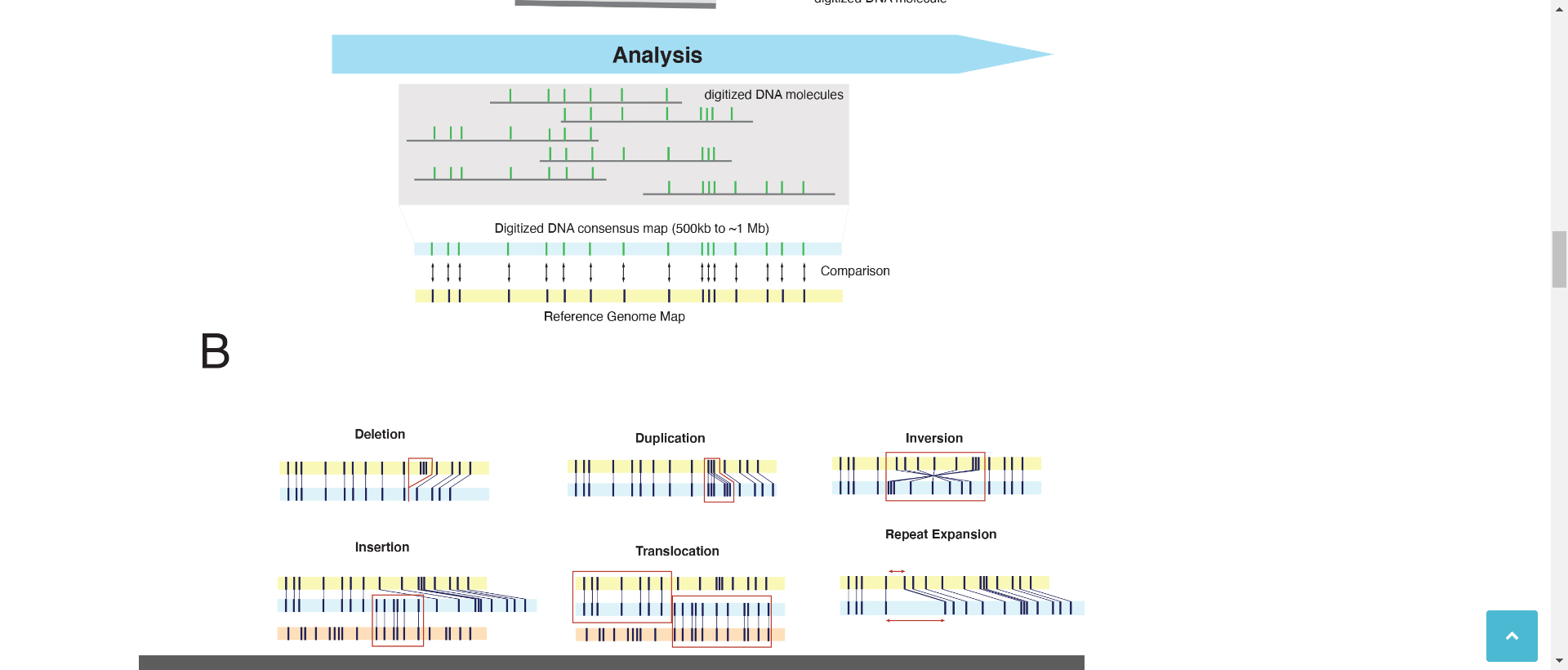

Bionano's core business revolves around equipment for Optical Genome Mapping (OGM). It's a technology that studies DNA in a manner different from products of companies like Illumina or Thermo Fisher Scientific.

Studying DNA variations, the genome, genes, and chromosomes can be useful for three main purposes:

-

Conducting research to better understand genetic diseases and various types of cancer;

-

Making precise diagnoses related to certain cancers and other diseases often associated with specific DNA traits;

-

Conducting research and development of products for agriculture, for example by studying the genes that influence a particular trait of interest and replicating them in a genetically modified organism.

Optical genome mapping is a technology that optically maps an individual's entire genome with the aim of studying the structural variants of DNA. Structural variants are types of genetic variations that can be very small (50-100 base pairs) or very large (entire chromosomes). Bionano's Saphyr® system can identify structural variants up to a resolution of 500 base pairs.

Examples of structural variants that can be studied with Bionano products include:

-

Copy Number Variations (CNVs): These are a type of structural variant where a specific section of the genome is repeated, and the number of repeats varies between individuals;

-

Deletions: A section of DNA is removed;

-

Duplications: A section of DNA is copied one or more times;

-

Inversions: A section of DNA is flipped around, so it is in the reverse order.

{kind=link}

College of American Pathologists - "Optical Genome Mapping: A ‘Tool’ with Significant Potential from Discovery to Diagnostics"

Market Strategy

Bionano has decided to commit 100% to the Optical Genome Imaging market. This is a specific niche within genetics that competes with other technologies only for certain applications; essentially, Bionano and other researchers' publications aim to prove that OGM is the best technology for studying DNA structural variations.

OGM has the unique characteristic of focusing on the "big picture," rather than studying each of the bases that make up DNA in detail.

Illumina, for instance, primarily specializes in next-generation sequencing ((NGS)) technologies. In this case, the goal is the exact opposite: to provide a very detailed reading of each individual DNA base and genetic information.

Another highly important technology, with a larger TAM than OGM, is cytogenetic testing. Cytogenetic testing is based on studying specific DNA mutations.

To make a simple yet clear parallel, Illumina and cytogenic testing aim to "zoom in" on DNA to study its microscopic characteristics. Bionano's products are designed to "zoom out" to study larger portions.

Competition

Apart from any alternative technologies that may arise over time, Bionano currently competes with OpGen, Nabsys, and PerkinElmer Genetics. These three companies also offer solutions designed for Optical Genomic Imaging.

Nabsys, in particular, developed an intriguing chip in 2021 that maintains good resolution and increases throughput by ten times compared to previous generations of chips. Now, the company is working with Hitachi to combine products and software capable of precisely identifying DNA structural variants with a sensitivity of 300 bases.

Having said this, Bionano currently remains the industry leader in sales and technology. However, given that the small size of the TAM is a serious problem for the sector, the existence of even a single strong competitor poses a significant threat.

Why the Numbers Don't Add Up

Until now, we have focused on all the positive aspects of Bionano: a business model that makes the world a better place, technological leadership, and a different positioning compared to competitors. All of this reminds me very much of InMode ( INMD ), a company that also produces medical equipment and about which I wrote a detailed analysis a few days ago.

The big difference is that, in Bionano's case, all of this isn't enough to guarantee the building of a solid company that produces positive returns for its shareholders. Below are the four main reasons why this company doesn't offer prospects for investors.

The Losses are Alarming

In just the last five quarters alone, Bionano has lost $160 million. Essentially, in just over a year, the company has incurred losses greater than the total revenue generated in over ten years of its history.

Every quarter, an average of $30 million in cash is burnt. All this with no prospect of improvement: we're not talking about a young biotech company that may or may not succeed in patenting a new drug with a potential market worth tens of billions of dollars. We're talking about a company that has been on the market for years with a product that is technologically leading in its sector but still bills less than $30 million per year.

The Market is Too Small

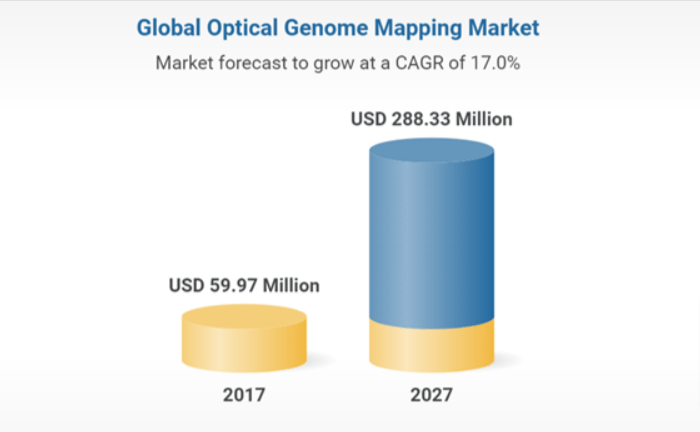

Regarding the TAM, the good news is that Optical Genome Imaging is growing rapidly: according to a TechSci Research report , the estimated growth rate between 2021 and 2027 is 19.73%.

The bad news is that it's not enough. Indeed, this is a market that was worth, according to the same source, $60 million in 2017 and will reach a value of $288 million in 2027. Given that Bionano isn't even the only company operating in this sector, and there are no positive catalysts on the horizon, it's really hard to see how the company can become profitable.

{kind=link}

Research and Markets - "Global Optical Genome Mapping Market"

The Margins are Too Low

Let's look at Bionano's revenue, gross profit, and gross profit margin over the past few years (data sourced from SeekingAlpha):

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| TTM |

| Revenue |

| 12 |

| 10.1 |

| 8.5 |

| 18 |

| 27.8 |

| 29.5 |

| Gross profit |

| 3.3 |

| 3.4 |

| 2.8 |

| 3.9 |

| 5.9 |

| 7.2 |

| Gross profit margin |

| 27.50% |

| 33.66% |

| 32.94% |

| 21.67% |

| 21.22% |

| 24.41% |

Regardless of the increase in revenue, the margins have not improved. In fact, they have worsened. The average gross profit margin over the last 5 years has been 26.90%, which is enough for us to make a simple calculation. Assuming that fixed costs remain stable at the same level as in 2022, we would find ourselves in a situation like this:

| Gross profit margin |

| 26.90% |

| Operating expenses |

| 114.5 M$ |

| Revenue to “break even” |

| 425.6 M$ |

Essentially, Bionano's revenues would need to grow more than 14 times - without increasing fixed costs by a cent - just to offset operating expenses. The simple fact that the TAM is below the revenues needed to cover expenses is enough to convince me not to buy the stock, especially in the absence of major prospects for change in the sector in the future.

The Technological Risk is High

The only hope for shareholders is that the CAGR of Optical Genomic Imaging is much higher than expected and that Bionano retains the leadership position long enough to repay shareholders for all past losses.

Even assuming that this scenario could occur, the TAM would not be enough to justify the costs the company operates to work in the sector until 2029-2030. We're talking about 7 years in which any current competitor could outpace Bionano; any competitor in the broader world of genetics could produce a better product, especially larger companies like Illumina that have more resources; a new startup could find an alternative technology for studying DNA structural variants.

Let's consider that we're not talking about a consolidated sector with a technology that has remained relatively stable for twenty years. We're talking about a sector in which new generations of products are released at an impressive rate, where all competitors are still small and ramping up research and development expenditures.

Conclusions and Final Thoughts

I would define Bionano as an extremely interesting research project, with a positive impact on the world. At the same time, it lacks the characteristics - especially financial ones - of a for-profit company listed on the stock exchange. Costs are excessive, margins are too low, growth prospects are limited. If the market were larger or the margins significantly better, there would be room to invest.

2023 will be another year of significant losses, even considering that the company has released a revenue forecast of $35-38M for the current year. Moreover, this forecast also indicates a slowdown in the company's growth curve.

No change in the situation is expected for at least the next 5 years. After that, it will likely be technological evolution that tells us where Bionano could be headed and, more generally, where OGM technology could be headed. Until that time, I can't imagine a single novelty that could make me change my SELL rating.

For further details see:

Bionano Genomics: A Noble Cause But A Bad Investment