BVS - Bioventus Stock: Improving Outlook Keeps It Interesting

2023-10-11 17:44:42 ET

Summary

- Bioventus Inc. is attempting to move forward from disappointing results in recent years including the failed acquisition of "CartiHeal."

- The company expects growth to reaccelerate into 2024 as recent pricing pressures stabilize.

- We expect Bioventus Inc. shares to remain volatile but see an upside as earnings improve going forward.

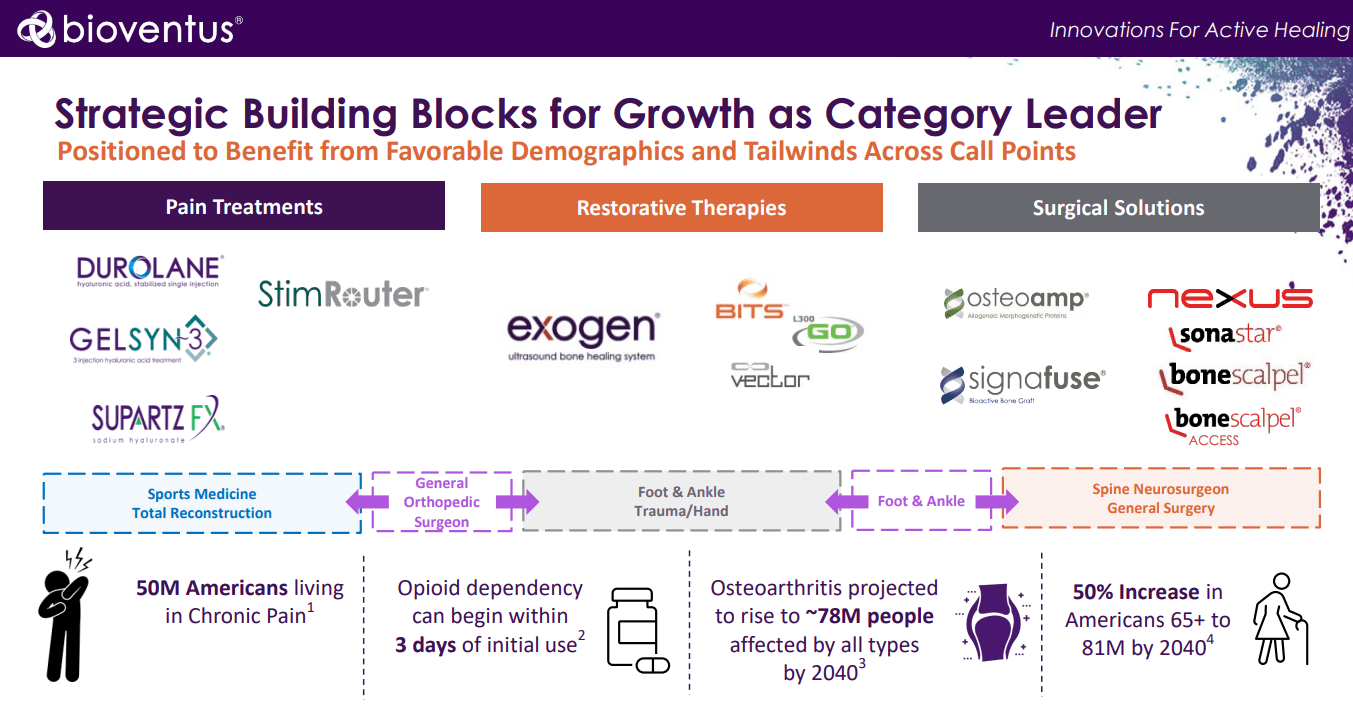

Bioventus Inc. ( BVS ) specializes in orthopedic pain treatments, restorative therapies, and related surgical solutions within the medical devices industry. The company's line of FDA-approved hyaluronic acid ((HA)) injections including "Durolane" and "Supartz" are recognized as market leaders in treating knee osteoarthritis. The attraction here is a long-term opportunity amid climbing demand for minimally invasive pain treatments globally.

That being said, financial results over the past year have been mixed going back to the company's failed acquisition of "CartiHeal" which led to a broader restructuring and even a new CEO back in Q1. The story has been otherwise disappointing growth in recent quarters.

Still, there are several reasons for investors to look up. Management is offering positive guidance with an expectation for a re-acceleration of the business. Efforts at cost controls and a focus on core strengths support a more positive outlook that we believe should be positive for shares.

BVS Financials Recap

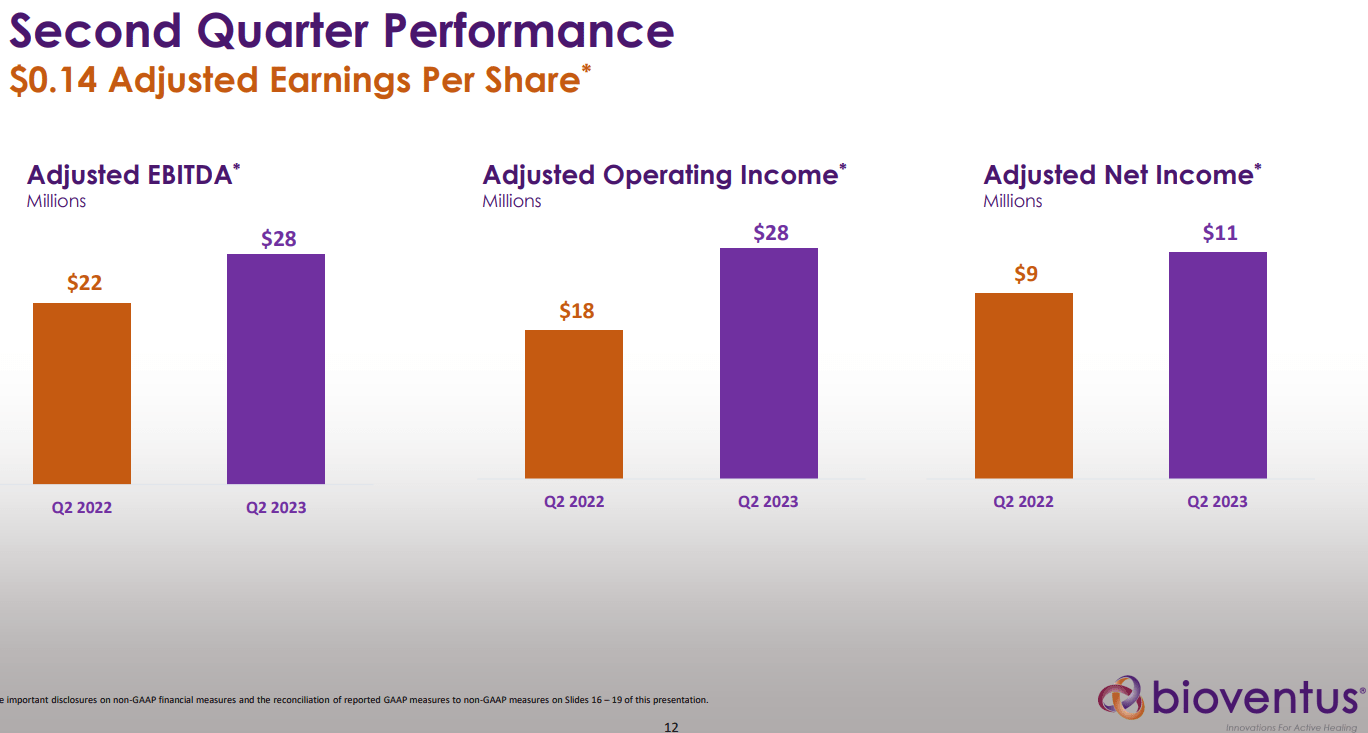

BVS last reported its Q2 results in August with a non-GAAP EPS of $0.14, compared to 0.10 in the period last year. Revenue of $137 million was down by -2.3% y/y but did come in ahead of consensus estimates.

The adjusted gross margin at 74% in Q2 is down from 76.8% considering a shifting product mix and some pricing pressures. Q2 adjusted EBITDA at $28 million was up from $22 million in Q2 2022, in large part based on an effort at expenses reduction.

While these figures are "fine," the trends are well below peak levels from 2021 when Bioventus was generating double-digit growth. The overall slowdown in organic operating trends explains much of the weakness in the stock over the period.

{kind=link}

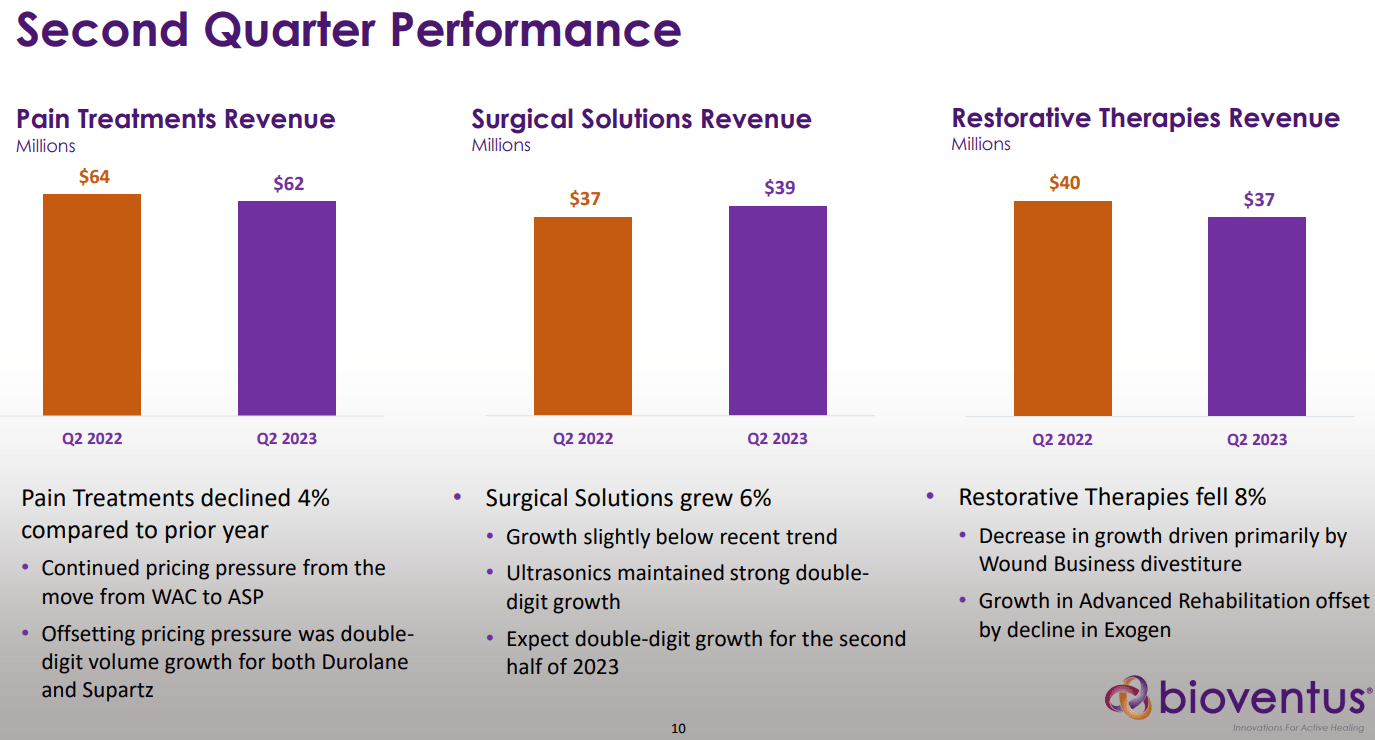

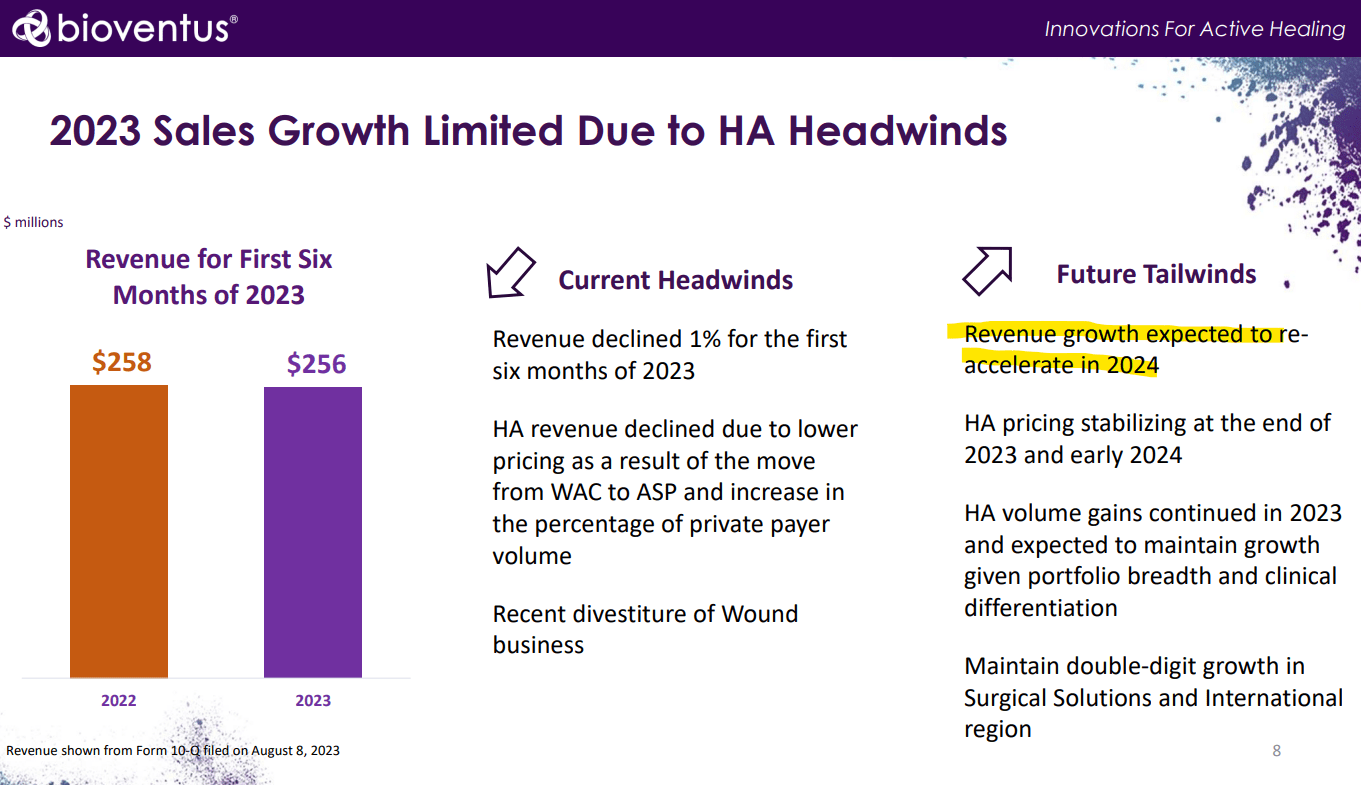

This quarter, pain treatment revenues fell by 4% y/y considering a switch between an accounting change utilizing wholesale acquisition cost ((WAC)) to average sales price ((ASP)) in alignment with insurance coverage practices. The main difference is that ASP does not factor in discounts and rebates. Favorably, volumes for both Durolane and Supartz are up including momentum international.

The trends in surgical solutions have been more positive, with revenues climbing by 6% y/y. This segment captures what has been a strong market response to the company's Ultrasonics portfolio with management seeing room for more upside into the second half of 2023.

{kind=link}

In terms of the Restorative Therapies segment, revenues fell by -8% y/y including the impact of the wound business divestiture . On this point, the sale of "TheraSkin" and "TheraGenesis" earlier this year marked a bottom for the stock with shares rallying in the period since. Bioventus raised a total consideration of $85 million, including $35 million cash at the close which has helped stabilize the balance sheet and liquidity position.

On the other hand, a current net leverage ratio of 4.3x at the end of the quarter remains elevated, which we believe is a headwind for the stock. The expectation is that there is room for further debt reduction as the financial performance strengthens into 2024.

In terms of guidance, management is targeting full-year sales between $490 and $505 million. This level represents a decline of 2% from 2022, but is also flat excluding the wound business exit. A forecast for adjusted EBITDA in the range of $75 to $80 million compares to $66.3 million last year.

What's Next For BVS?

There's a lot to like about Bioventus with a sense that the company is emerging from what had been a turbulent period with some operational and financial setbacks. What we know is that the underlying business is profitable.

The understanding is that its product ecosystem in this segment of "active healing" including orthobiologics captures what is estimated to be a $15 billion addressable market.

{kind=link}

Data shows that there are 50 million Americans currently living with some form of osteoarthritis and chronic pain, a level to climb toward 78 million by 2030. An aging population simply translates into an expanding market opportunity for the company's products.

The strong point here is the expectation for revenue growth to rebound by next year, capturing some volume gains and also lapping the pricing headwinds. Momentum in international markets and through surgical solutions should be positive for the top and bottom line.

{kind=link}

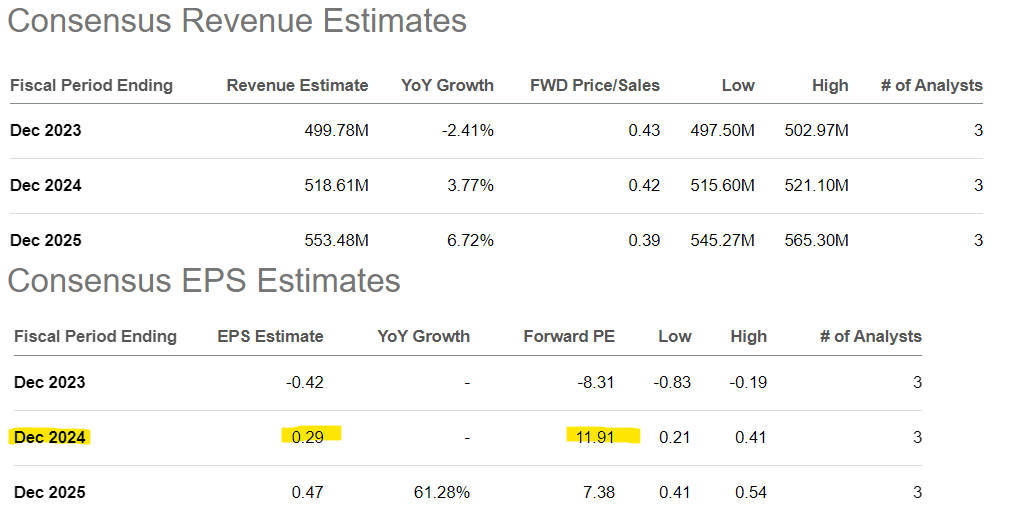

This backdrop is reflected in the current consensus estimates, where there is a forecast for EPS to reverse an EPS loss of -$0.42 this year to reach $0.29 in 2024. The bullish case for the stock is that there is some upside to these estimates, particularly if the macro picture cooperates.

We'd also say that valuation with shares trading at an EV to forward EBITDA multiple of just 8x based on management 2023 guidance or 12x on the 2024 consensus EPS is attractive in our view for a market leader.

{kind=link}

Final Thoughts

We rate Bioventus Inc. stock as a buy with a price target for the year ahead at $4.00, representing 15x 1-year forward P/E on the 2024 EPS estimate. We'd say we are cautiously bullish on Bioventus Inc. stock considering lingering uncertainties regarding the turnaround with the next few quarters as critical to confirm a rebound in sales momentum. The expectation is for continued volatility over the near term.

It will be important for management to continue executing its financial performance with an effort at savings and firming margins. The high debt position is a current headwind that should keep shares volatile but also offers an opportunity for the stock to reprice higher with further deleveraging going forward.

The risks to consider start with the potential that results come in weaker than expected. Evidence that the brand momentum in HA injections is slipping against competitive pricing pressures could open the door for a deeper selloff. While a date has not yet been confirmed, Bioventus is likely to report its Q3 financials in early November where metrics like cash flow and the gross margin will be key monitoring points.

For further details see:

Bioventus Stock: Improving Outlook Keeps It Interesting