BTAI - BioXcel Therapeutics: All Eyes On Igalmi's Ramp Reiterating Hold Rating

2023-04-26 19:33:17 ET

Summary

- We are reiterating the hold rating due to Igalmi launch uncertainties around market access and the limited commercial capacity of BTAI.

- Optimistic about upcoming Tranquility 2 and Serenity 3 trial readouts in 2Q23.

- Serenity 3 is considered fairly de-risked; Tranquility 2 & 3 to support Igalmi's dementia market entry.

- Potential risks: slower Igalmi launch, unfavorable trial results, regulatory hurdles, and competition.

Bottom Line: Update to thesis

We are maintaining a hold rating on the stock due to uncertainties surrounding the launch of Igalmi. Please read our previous article for more detail about the company's platform technology and our previous rating. We are fairly optimistic about the expected readouts of the Tranquility 2 and Serenity 3 trials in the near future ( 2Q23 ). We believe the success of the Igalmi Hospital launch will determine the stock's near-term price movement. This is evidenced by the fact that the stock experienced a sell-off in the first half of 2023 after the company announced Q4 results that were lower than the market expected.

Our tepid outlook on the launch of Igalmi is mainly due to two factors. Firstly, there is an unclear risk/cost/benefit profile of the product in a hospital setting, and formulary decisions can take longer than what some investors are hoping for. Secondly, the company has limited commercial capacity and no proven track record, which adds further uncertainty to the launch.

Serenity III and Tranquility II readout expected in 2Q 23 seems fairly de-risked

We are of the opinion that the readout of Serenity 3 is relatively de-risked, given that the drug has already demonstrated robust safety and statistically significant results in bipolar and schizophrenia populations in prior trials. Therefore, the FDA will be mainly focused on safety in the at-home setting, particularly with regard to serious treatment-related side effects. As a reminder, Serenity 3 Part 1 is currently enrolling patients with schizophrenia and bipolar disorder and evaluating them at a dose of 60mcg, which is half the approved level. The primary objective of this study is to assess the efficacy of the low dose in a hospital setting. Part 2 of the study, which is expected to begin enrolling in the second half of 2023, will focus on evaluating safety with 60mg dosing in the at-home setting.

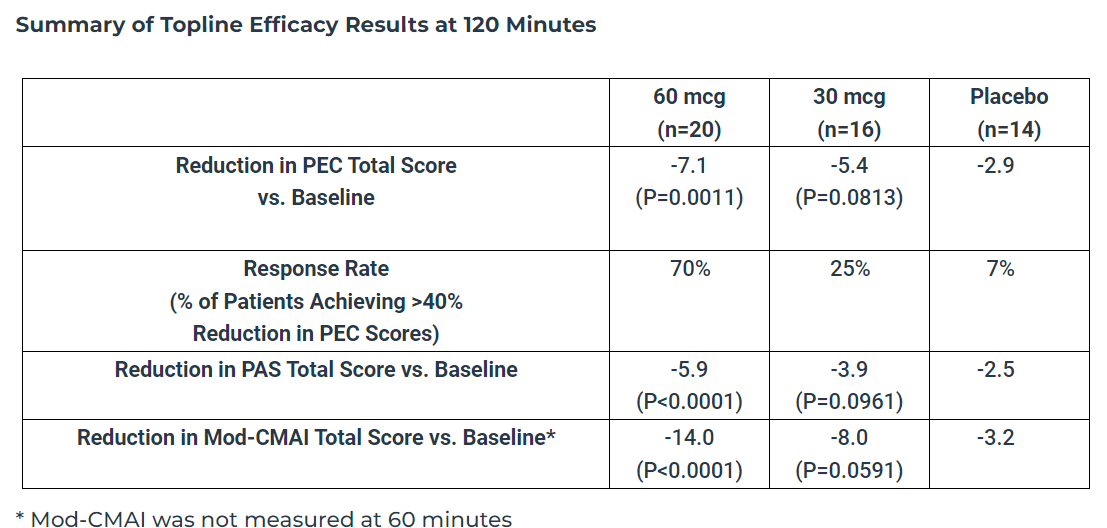

Tranquility II and Tranquility III are poised to support the market launch of Igalmi in the agitation-associated dementia market. With regard to the Tranquility II readout, we are optimistic due to the favorable data from the Tranquility I trial , which showed a PEC delta of 4.2 and a response rate of 70%, as well as the higher powering assumptions that de-risk the readout. It is worth noting that Tranquility II evaluates BXCL501 at doses of 40mcg and 60mcg in populations that require minimal assistance at assisted living facilities. On the other hand, Tranquility III (dose 40mcg and 60mcg) will focus on patients who require moderate assistance in nursing homes (dementia and nursing homes), and we expect results by the end of 2023.

TRANQUILITY 1 (Company source)

{kind=link}

Risks

-

Slower-than-anticipated Igalmi launch: Delays in getting on hospital formularies could impede revenue growth and market penetration, affecting stock performance.

-

Upcoming clinical trial results: Unfavorable data readouts from T2, T3, or S3 trials could negatively impact the stock's valuation and BTAI's growth prospects.

-

Regulatory hurdles: Potential challenges in obtaining FDA approval for new indications or at-home use could limit Igalmi's market potential and commercial success.

-

Competition: The emergence of new or more effective treatments in the agitation or dementia space could impact Igalmi's market share and BTAI's long-term growth.

Conclusion

We maintain a hold rating on BTAI due to uncertainties surrounding Igalmi's launch and the company's limited commercial capacity. However, we remain optimistic about the upcoming Tranquility 2 and Serenity 3 trial readouts in 2Q23. The success of Igalmi's hospital launch will likely drive near-term stock performance, as evidenced by the sell-off following lower-than-expected Q4 results. While we see Serenity 3 as fairly de-risked and expect Tranquility 2 and 3 trials to support Igalmi's entry into the agitation-associated dementia market, potential risks include a slower-than-anticipated Igalmi launch, unfavorable clinical trial results, regulatory hurdles, and increased competition. The company currently holds around $180M cash in its balance sheet, which in our view, is a fairly robust cash runway for 1-2 years, and we believe an equity raise in the near future (before the data readout) is unlikely.

Note: Please read our initiation article for more detail about the company's platform technology.

For further details see:

BioXcel Therapeutics: All Eyes On Igalmi's Ramp, Reiterating Hold Rating