BTAI - BioXcel Therapeutics' Igalmi Commercial Launch: Not As Bad As Some May Think

2023-03-16 18:45:17 ET

Summary

- BioXcel Therapeutics, Inc. has just released results for the fourth quarter of 2022.

- Some analysts have expressed doubts about the commercial success of its Igalmi launch.

- The good growth in forms approved so far makes me very optimistic about the future evolution of BioXcel Therapeutics, Inc. revenues in the coming quarters.

BioXcel Therapeutics, Inc. (BTAI) released fourth quarter 2022 results on March 9. There was a lot of expectation for Igalmi's revenue data, since it is the second quarter for which data is available after its commercial launch. Some analysts presaged a certain pessimism, since Igalmi is currently marketed only in hospitals settings, which implies a slow and tortuous commercial process. The latest articles published in SA gave a skeptical opinion on the launch, such as BioXcel Therapeutics: IGALMI Is Likely A Dud In The Real-World, based on the difficult sales environment (hospitals) and cheaper alternative options (antipsychotics and benzodiazepines).

My opinion in this regard is that they are articles without an in-depth analysis of the agitation market in patients with Schizophrenia and bipolar syndrome. In addition, these analysts do not give Igalmi a chance to demonstrate whether it is commercially viable or not since not even a quarter has passed since its launch.

In the previous quarter, Q3 2022 , revenues of $134,000 were reported, and now the figure has been: $237,000, 77% more. Quarterly growth has been very good, but it seems the market was expecting more, as the price is down over 40% in just a few days (from around $30 to $19.60 as of today, March 15). Another clear example of market overreaction because, as we will see later, the data reported by BioXcel Therapeutics, Inc. does not justify the bump of more than 40% in a few days.

It should be said, in this sense, that the stock market crisis caused by the bankruptcy of SVB Financial Group (SIVB) has been added to the revenue figure lower than that expected by the market. This banking crisis has hit small technology and biotech companies especially hard, as many of the depositors were small companies in these two sectors.

BioXcel published a statement last Friday stating that they had no deposits in said bank in an attempt to calm the markets.

It is clear that for the market, the revenue figure has been lower than expected. I was expecting a revenue figure in the range of $220,000 to $300,000. Therefore, in my opinion, $237,000 is a very reasonable number for the second quarter after the launch of Igalmi. And my calculations are obtained from the evolution of the approved hospital's formularies in the last months: in the third quarter of 2022, the company reported 12. A little later, last fall the company announced on " Commercial Day " that they had just over 12 forms approved. Therefore, the number of forms approved as of 12/31/22 can be estimated at approximately 20.

The evolution of the number of forms approved by the P&T committees is key information for the future commercial success of any drug that begins to be marketed in the hospital setting.

Regarding the number of forms approved to date (March 9), a figure of 65 was reported, a little more than 200% than the previous quarter Q3 (20 approx.). A very good growth.

Therefore, the growth in the number of forms approved between the third and fourth quarters of 2022 (12-20) made me presage that fourth-quarter revenue could be around $240,000.

The reported revenue figure of $237,000 has not surprised; rather it has been the expected figure. And what I like most about the coming quarters is the good evolution of the forms approved so far. As reported by the company, the forms approved until March 9 are 65, so it is foreseeable that the current quarter Q1 will end with some 70/80 forms approved, which would mean a growth of more than 250% compared to Q4 2022. And what's better, there are some 600 forms ready to be reviewed by the P&T committees in the coming months. Of these, and according to the company, 400 (2/3) should finally be approved, so the number of approved forms should increase to almost 500 between Q2 and Q3 (4,000% more than Q3 2022 (12). Apart from this, the company intends to include Igalmi in another 1,100 P&T committees throughout this year. These figures make me very optimistic for the coming quarters.

Success in the commercial launch of a drug is determined by good revenue growth in the first few quarters, and I really think we'll see very good growth in the next few quarters. My forecast is that we will see increasing numbers in the coming quarters, with cumulative revenue for this year, 2023 of approximately $10 million.

My estimate of the potential maximum annual revenue for Igalmi in this indication is in the range of $150 million to $200 million per year.

On the other hand, the company is still waiting to report the results of the phase III Tranquility II trial for the second quarter. This will be, in my opinion, the biggest catalyst BioXcel stock will have for all of 2023 (along with the Serenity III and Tranquility III test data). The good results of this trial will have a strong impact on the share price because it is in this indication (Agitation in Alzheimer's patients) where the greatest revenue potential that BXCL501 could generate. It would be in the range of $600 million and $900 million.

Therefore, the 4Q ER allows us to affirm that everything continues as planned with very promising prospects and that it is very foreseeable to see the price above $40/$50 throughout this year, 2023.

I think that BioXcel now, with an MC of around $540 million and a price of around $19.65, presents an exceptional time to take positions.

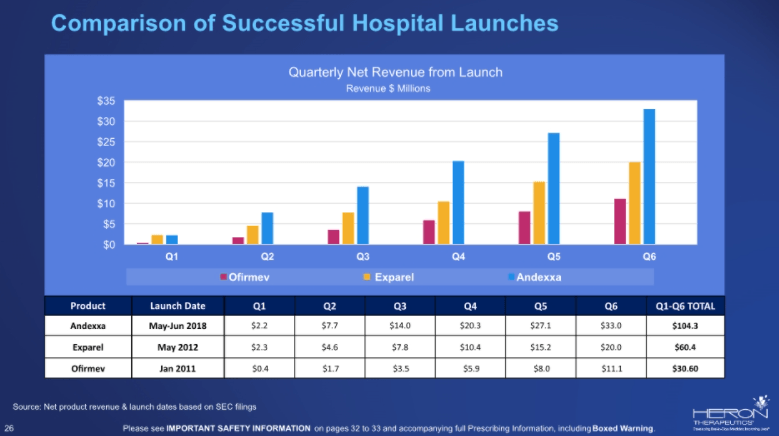

Launch of Igalmi: comparison with other successful hospital launches

A very precise way of being able to estimate whether Igalmi is showing a successful commercial launch in these first quarters is to compare the results obtained so far with the results obtained in the first quarters of launch in the hospital setting of other drugs.

So let's discuss:

-Successful Hospital Launches:

-Pacira BioSciences´s Exparel (non-opioid analgesic) (NDASDAQ:PCRX).

-Alexion´s ( ALXN ) Andexxa (anticoagulation reversal).

-Ofirmev from Cadence Pharmaceuticals (acute pain).

{kind=link}

As can be seen, all three drugs are examples of successful commercial launches, with consistent revenue growth in the first six post-launch quarters.

The estimated maximum annual revenue potential for the three drugs is around $1 billion each.

The % of the sum of the accumulated revenue in the first six quarters with respect to the maximum potential peak is located at:

-Andexxa: 10.4%

-Exparel: 6%

-Ofirmev: 3%

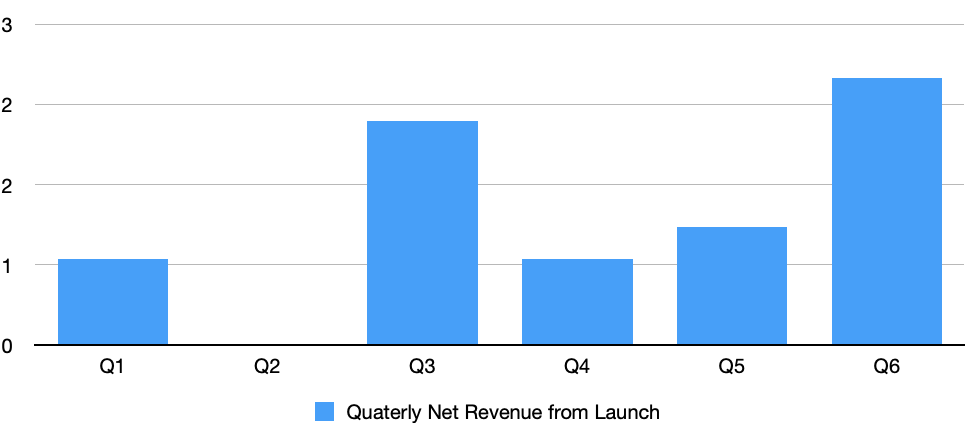

2) Failed Hospital Launch:

-Heron´s ( HRTX ) Zynrelef (postsurgical analgesia).

Quarterly net revenue (million $) :

{kind=link}

Source : Author

| Q1 |

| Q2 |

| Q3 |

| Q4 |

| Q5 |

| Q6 |

| Q1-Q6 Total |

| Zynrelef |

| 0.8 |

| 0 |

| 2.1 |

| 0.8 |

| 1,1 |

| 2.3 |

In the case of Zynrelef, very irregular revenue growth is observed in the first quarters without following a clear line of growth.

The estimated maximum earning potential here would be around $1 billion.

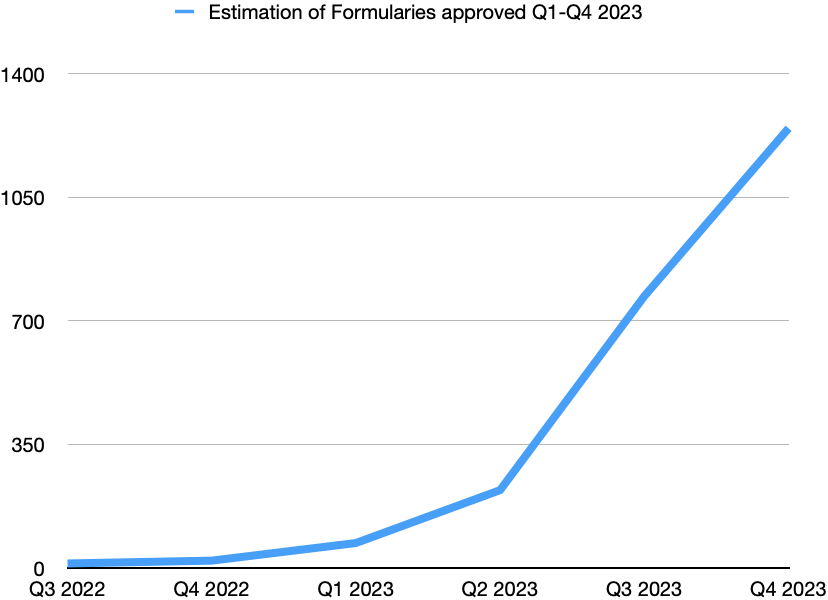

Igalmi revenue in the first two quarters after its launch and an estimation for the following quarters:

To make an estimate of Igalmi's revenue in the coming quarters, I am going to estimate the evolution of forms approved for the same period.

As of 03/09/23 we have:

Forms approved in Q3: 12

Forms approved in Q4: 20

Forms approved until March 9: 65.

Forms awaiting P&T review through March 9: 600. Assuming a 66% conversion rate (ratio provided by BTAI so far), we would have about 400 more forms approved through Q2 and Q3.

The objective is to reach 1,100 more P&T committees in the coming months with the reinforcement of the 70 new commercial representatives incorporated last December. Of those, and according to the conversion rate reported by BTAI (66%), some 726 would end up being approved in the coming months.

{kind=link}

| Q3 2022 |

| Q4 2022 |

| Q1 2023 |

| Q2 2023 |

| Q3 2023 |

| Q4 2023 |

| Estimation of formularies approved (from Q1 2023-Q4 2023) |

| 12 |

| 20 |

| 75 |

| 220 |

| 770 |

| 1246 |

| % increase formularies approved quarter to quarter |

| 66,66 % |

| 250 % |

| 193 % |

| 250 % |

| 61,81 % |

Source : Author

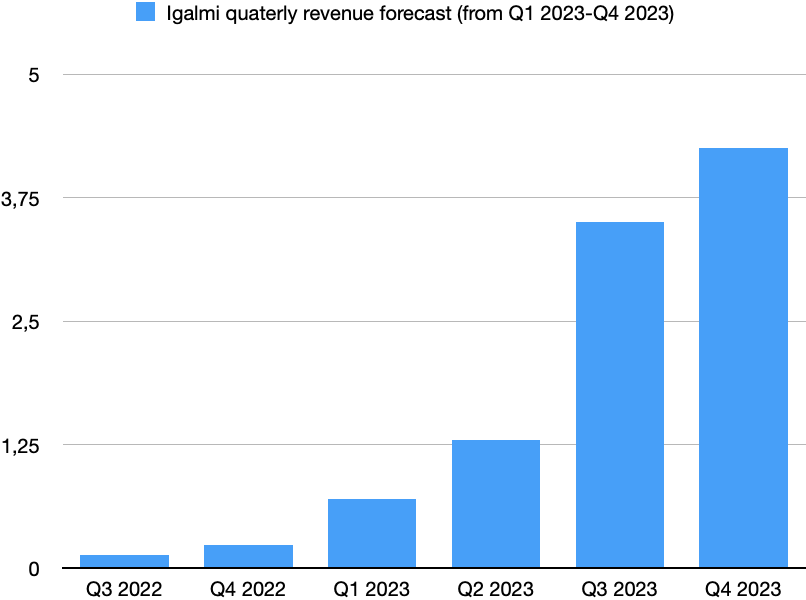

Quarterly revenue forecast for IGALMI Q1-Q4 2023 (millions of $)

To estimate Igalmi's revenue between the first and fourth quarters of 2023, I will use the estimate previously made from the approved forms. Thus, revenue growth will be determined by the growth in forms, applying a reduction coefficient of 25% to offset the effect of hospitals that do not repeat orders.

| Q3 2022 |

| Q4 2022 |

| Q1 2023 |

| Q2 2023 |

| Q3 2023 |

| Q4 2023 |

| Forecast quarterly revenue Q1-Q4 2023 |

| $0,137M |

| $0,237M |

| $0,622M |

| $1,3M |

| $3,5M |

| $4,25M |

| % increase revenue estimated |

| 162 % |

| 109 % |

| 169 % |

| 21 % |

{kind=link}

As you can see, my revenue forecast for the next few quarters of 2023 shows good consistent growth. Total cumulative revenue for the full year of 2023 would be $9.67 million. This represents 4.8% of the maximum potential annual that Igalmi can generate in the long term ($200M). We previously looked at the revenue generated by three drugs that have been examples of commercial success at launch. Earning percentage for the first four quarters is 3-10% of total potential peak earnings. Igalmi, with an estimated 4.8% for this year, would be in line with these drugs.

From all of the above, it can be deduced that, although they are estimates based on the data provided by the company to date, Igalmi's revenue prospects for the coming quarters are very promising.

Some skeptical opinions expressed lately about the success of the commercial launch of Igalmi I believe to be unfounded and carried out very prematurely. Time will tell if that skepticism was really well founded, or on the contrary, as I expose here, Igalmi will generate good revenue growth rates in the first months after its launch.

Cash Status

Cash and cash equivalents totaled $193.7 million on December 31, 2022, compared to $233 million on December 31, 2021. The company believes that the full execution of the strategic financing with Oak Tree and the Qatar Investment Authority would result in a cash runway into 2025.

Risks

As in any biotech company, there are risks that every investor must take into account:

-The commercial launch of Igalmi ultimately fails.

-The results of the phase III trials that are about to be published are not promising.

Conclusion

BioXcel Therapeutics, Inc. has just released results for the fourth quarter of 2022. There was a lot of excitement for Igalmi's revenue this quarter, the second for which revenue data was reported after its commercial launch. Some analysts have expressed doubts about the commercial success of the drug launch. The data presented has not sat well with the market, and the price has plummeted 40% in just a few days. A totally exaggerated punishment since, with only two-quarters revenue it is still premature to judge the commercial success/failure of the launch of any drug, especially one like Igalmi marketed in hospital settings.

I have made an income forecast for Igalmi this year, 2023 based on the data reported by the company to date of forms approved by the P&T committees. The good growth in forms approved so far makes me very optimistic about the future evolution of revenues in the coming quarters, so I expect a cumulative revenue figure for this year, 2023 of around $10M.

On the other hand, the results of 3 phase III trials are expected to be published in the coming months. These are very important catalysts for stock prices.

With a current market capitalization of just $540 million, IGALMI revenue set to grow in the coming quarters, and Phase III trial results for three BXCL501 indications with peak revenue potential of more than $1 billion, BioXcel Therapeutics, Inc. currently presents an excellent time to take positions.

For further details see:

BioXcel Therapeutics' Igalmi Commercial Launch: Not As Bad As Some May Think