CA - Birchcliff Energy: A 9.5% Yield While Waiting For Higher Natural Gas Prices

2023-09-12 10:30:00 ET

Summary

- Birchcliff Energy's cash flows in Q2 were weak, but the future looks better due to improved natural gas prices.

- The company's dividend is not currently covered by free cash flow, but it is expected to be covered again in 2024.

- Birchcliff offers exposure to higher natural gas prices and potential capital gains, making it an attractive investment.

Introduction

I have been following Birchcliff Energy ( BIR:CA ) ( BIREF ) for several years now. Long-term readers may remember I had a decent-sized position in the preferred shares the company used to have outstanding and shortly after those preferred shares were called (allowing me to lock in a capital gain) I established a long position in the common shares. I like the company's balance sheet, strong production estimates and multi-decade reserves. The sole issue was/is the natural gas price. And although the company has committed to its quarterly dividend of C$0.20 per share , I am not necessarily keen on a company continuing to pay a dividend that is not (fully) covered by its free cash flow.

Fortunately, the futures curve of the natural gas prices looks better than before and Birchcliff should be able to benefit from the winter prices.

I will use the Canadian Dollar as base currency throughout this article, unless otherwise indicated.

The cash flows in Q2 were weak, but the future looks brighter

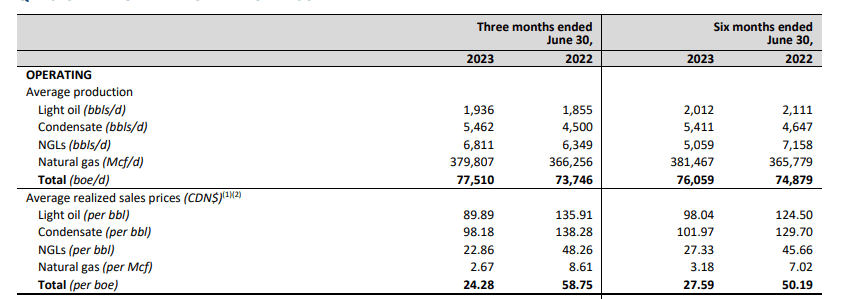

During the second quarter of the year, Birchcliff's production came in at 77,500 boe/day , and the vast majority of course consisted of natural gas with oil and condensate representing 7,400 boe/day and NGLs representing 6,800 boe/day.

{kind=link}

The average realized sales price was C$2.67 for the natural gas, and that's below the price level the company estimated it needs to cover its capex and generous dividend payment. But to calculate the exact shortfall, I will dive into the cash flow statements later in this article.

Fortunately, the oil and condensate prices remained strong and during Q2, Birchcliff's condensate price was actually higher than the light oil price. And that's important, as this C$10/barrel price difference resulted in an additional cash flow of around C$5M during the quarter. It doesn't move the needle by that much but it helped to create a 'softer' landing as the average price per boe decreased by 'just' 59% compared to the 69% lower natural gas price versus the second quarter of last year.

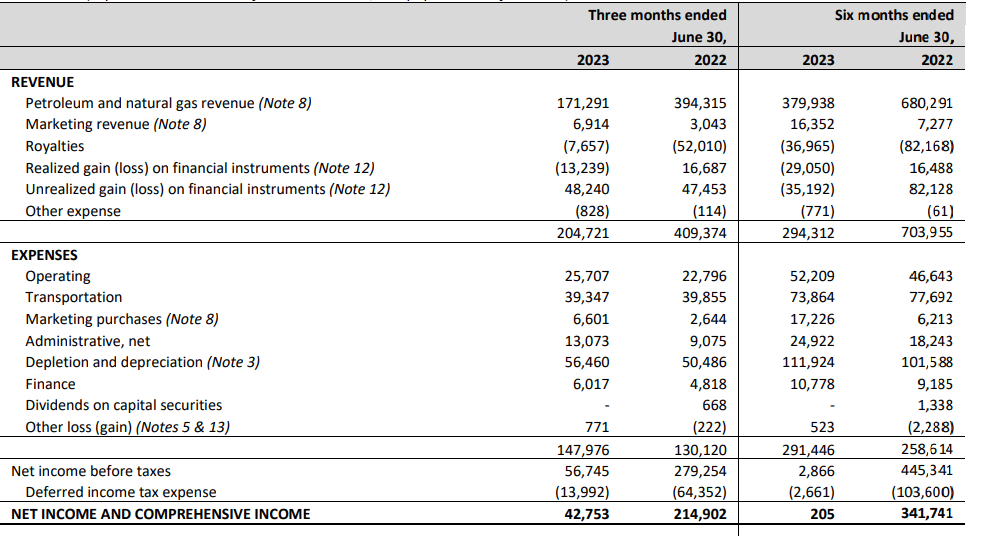

The total revenue from the sale of oil and gas dropped to C$171M but the total reported revenue was slightly higher at C$205M thanks to a net unrealized hedging gain of C$35M. As you can see below, the operating expenses remain very low and despite the low natural gas price, the pre-tax income was C$56.7M which resulted in a net income of C$42.8M or C$0.16 per share.

{kind=link}

Definitely substantially lower than the EPS of C$0.81 in the second quarter of last year, but given the relatively weak natural gas price of C$2.67, the reported EPS was actually still pretty decent. But it is clear the C$0.20 quarterly dividend is not covered.

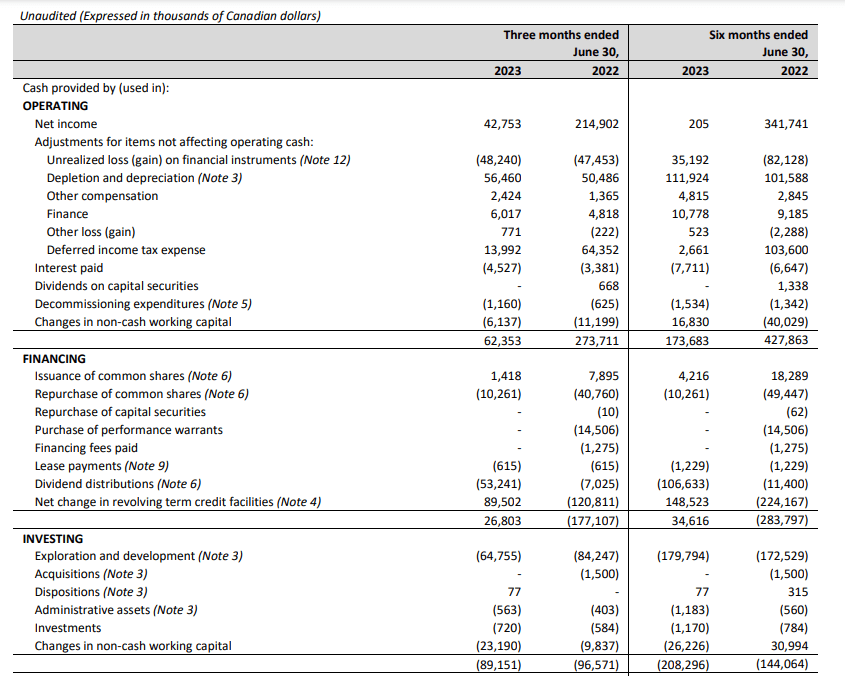

I also wanted to double check the company's cash flow statement to make sure the cash flows were also insufficient to cover the dividend . As you can see below, the reported operating cash flow was C$62.4M, but this includes a C$6.1M investment in the working capital while the C$14M tax bill was entirely deferred. Including the tax deferral, the underlying cash flow was C$68.5M. Excluding the deferral, the operating cash flow would have been just C$54.5M.

{kind=link}

This does include a realized loss of C$13.2M on the hedge portfolio and excluding that loss, the underlying operating cash flow would have been C$67.7M. That would have been sufficient to cover the C$64.8M capex but clearly would not have been sufficient to cover the C$53.2M in dividend payments.

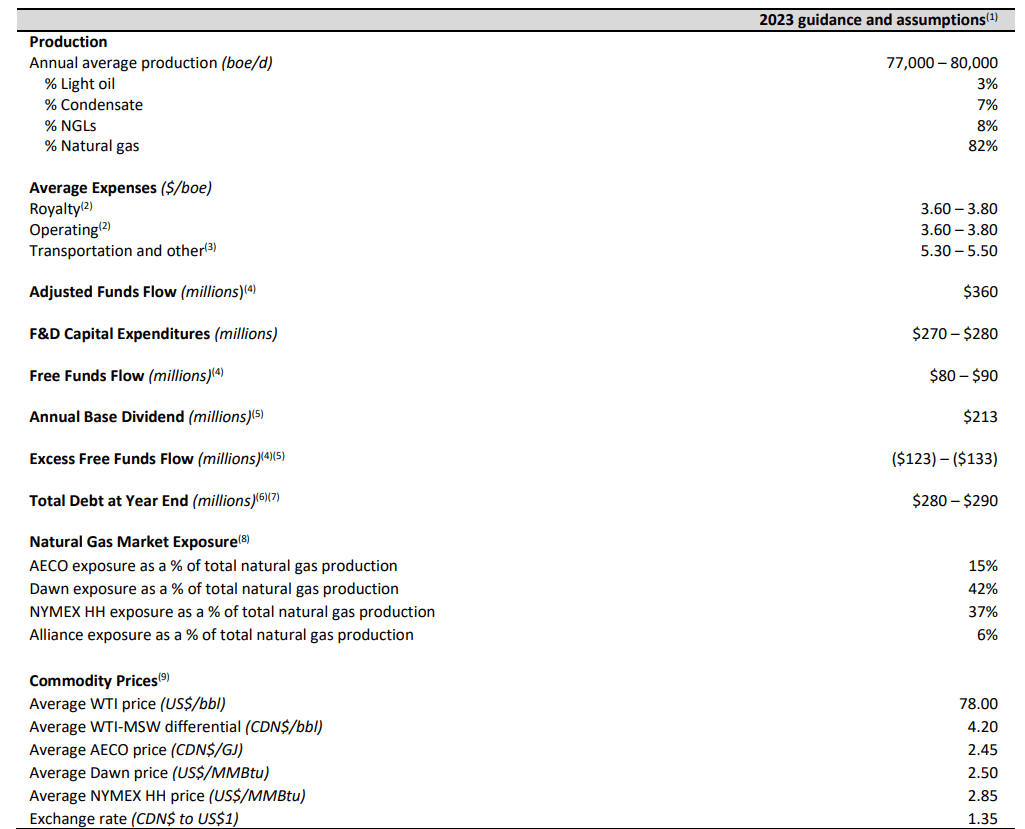

And that shouldn't be a surprise. Even the company's official guidance does not expect the dividends to be covered as the anticipated free funds flow based on C$2.45 AECO, US$2.50 Dawn and US$2.85 Henry Hub is just C$80-90M while Birchcliff would need C$213M to cover the current dividend payments.

{kind=link}

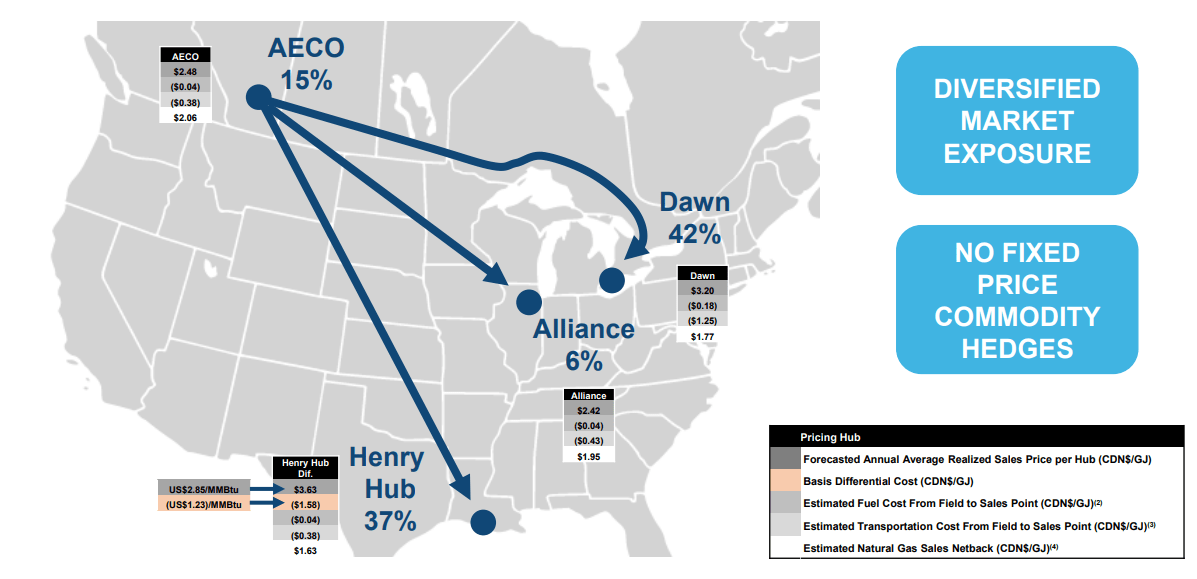

Fortunately, the situation looks better for 2024. As you can see below, almost 40% of the natural gas is based on the Henry Hub prices with about 15% generated based on AECO natural gas prices.

{kind=link}

The average Henry Hub price for 2024 is approximately US$3.40 while the average AECO natural gas price is C$3.15 for 2024. This should already provide a substantial boost to the cash flow and help the dividend coverage ratio.

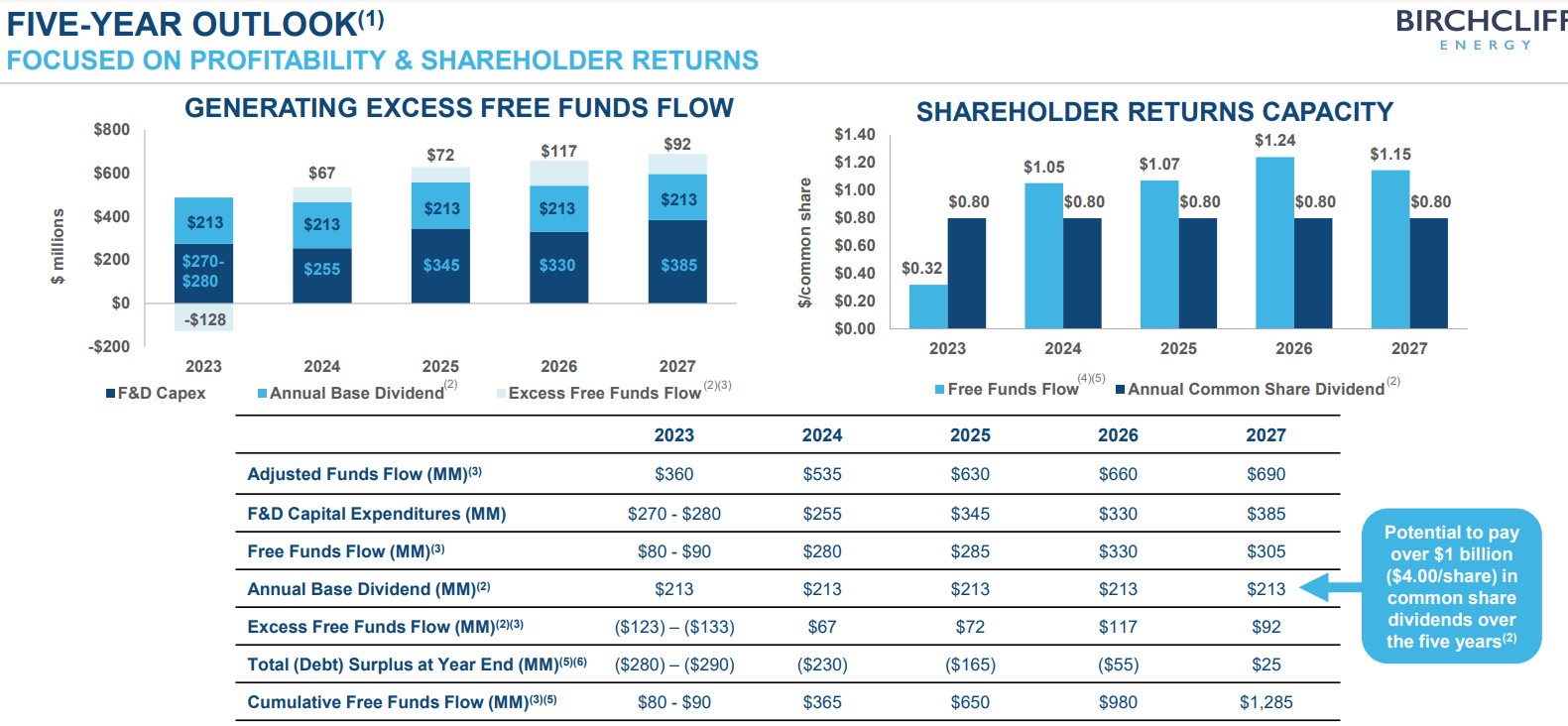

While the company published its 5 year plan before, it understands the market needs to see more details on the short-term front as well. I found the 2024 guidance particularly interesting. As you can see below, the company anticipates approximately C$40-50M in free funds flow after taking care of the capex and the dividend.

Birchcliff Investor Relations

Interestingly that cash flow expectations are based on C$3.15 AECO and US$3.60 Henry Hub while the Dawn natural gas price is estimated at US$3.45. Those prices really are a coincidence as I calculated the average prices today, September 11th, while the company published this guidance over a month ago. I consider the anticipated prices for 2024 to be realistic, but it is too bad the free cash flow Birchcliff expects to generate in 2024 are not sufficient to cover the anticipated net debt increase this year as the 2023 shortfall will likely exceed C$100M.

The company remains optimistic for 2025 and beyond. Using a natural gas price of C$4.20 for AECO, US$4.20 for Dawn and a US$4.30 Henry Hub natural gas price for 2025-2027, it expects to generate free cash flow of C$72M in 2025 and C$117M in 2026 as it expects the production rate to increase to 80,000 boe/day in 2025 and 83,000 boe/day in 2026.

{kind=link}

The production growth projections also indicate the capex includes investments in growth. The normalized sustaining capex will likely be relatively stable at C$250-260M. So if Birchcliff would decide to suspend its growth plans, the underlying free cash flow would likely be C$150M and C$180M in 2025 and 2026 (assuming the natural gas prices used by the company can be realized).

Investment thesis

I don't like companies that are paying a dividend they cannot afford, and Birchcliff clearly cannot afford its dividend at the current natural gas price. That's not an opinion, that's a fact, as Birchcliff's own full-year guidance shows a cash flow deficit. A slightly higher natural gas price should solve this issue and based on the current forward curve of the natural gas price, Birchcliff's dividend should be covered again in 2024 while there also should be some excess free cash flow.

And that's why I continue to hold my position in Birchcliff. I don't care too much about the dividend, but the company offers excellent exposure to higher natural gas prices. That would mean the dividend will be fully covered, but I'm also interested in the potential capital gains. Based on the projections for 2024, the free cash flow result (before dividend payments) should come in at C$1.05 per share, and that makes the current share price of around C$8.50 pretty attractive.

I already have a full position in Birchcliff Energy, but I could still add on weakness. I also continue to write out of the money put options, but I expect those options to expire out of the money.

For further details see:

Birchcliff Energy: A 9.5% Yield While Waiting For Higher Natural Gas Prices