CA - BlackBerry: Overvalued With Success Priced In

Summary

- Our view is that economic weakness will not materially impact the business, as Corporates consider Cybersecurity to be a key investment going forward.

- Both Cybersecurity and IoT are growing well due to the digitization of society and data. Opportunity is high and BB provides services in many segments.

- The problem with the business is that although their services have shown value, their competitors are investing more and developing faster.

- BB is not showing any growth in their financials, suggesting their Cybersecurity segment is already struggling. At a 3.3x revenue multiple, growth and profitability is already priced in.

Company description:

BlackBerry ( BB ) provides intelligent security software and services to enterprises and governments worldwide. The company operates through three segments: Cybersecurity, IoT, Licensing, and Other.

The company's primary offering now is a full suite of cybersecurity solutions from AI and machine learning-supported solutions, to monitoring and prevention, to critical event management. The business is looking to be a one-stop shop for a host of enterprise cybersecurity solutions.

BlackBerry is a historically important business, which at one point was a market-leading mobile phone manufacturer. Like many mature businesses throughout time, the business failed to innovate and fell behind. Unlike many, however, it's still here. It hasn't collapsed and it hasn't been taken over. The business is now a cybersecurity and IoT service provider.

BB stock has declined from an all-time high of c.$140-a-share just before the financial crisis to c.$4 now. Such a colossal decline has justified the creation of a Hollywood movie which was released recently. The last decade has been a gradual decline as investors have lost hope in where the business is headed following the failure of the mobile business ( IP was sold in Jan22 ).

The objective of this paper is to assess where BlackBerry is today. Much of this paper will consider how BB looks on the assumption that it still has much development to go. Services they offer, such as those targeted at the IoT industry, are still in their infancy.

Negative sentiment around the business is high and its brand is wholly tarnished. This can give the impression that there is no value, and yet the business trades at 4x revenue. There is clearly some faith in the long-term viability of the business. We will consider macroeconomic conditions and how they will interact with BlackBerry's current segment offering. We will look at recent quarterly performance to see if there is any evidence that the business is transitioning toward growth and finally, we will look at what a business like this might be worth long-term.

Economic consideration:

Global demand began to slow in 2022 as inflation took hold. Excessive money printing in '20/'21, the Russian invasion of Ukraine and supply chain issues are all contributing factors to this rapid increase in inflation. This has a negative impacting both consumers and many businesses as costs have increased.

The monetary response has been to raise interest rates to cool demand and bring inflation back to a manageable level. This has been slow in taking effect, but the US has now seen several months of declining inflation , suggesting we may see the end of this in the coming year.

We believe that growth will continue to trend downwards in 2023, as inflation remains persistent. The issue is that although it is trending downwards, it is not doing so in any meaningful manner. Looking at 1-Y inflation expectations, it still remains above the targeted 3%.

Interest rates will need to increase further in 2023, with a level in the region of 5% looking likely. This will continually drive down demand, negatively impacting both consumers and businesses. A recession is not out of the question currently.

This is likely to harm BB, as Corporates look to cut back on expenses to buffer the impact of falling demand / rising costs. Gartner ( IT ) has found that CEOs of MSEs generally look to cut costs rather than invest in their current operations during economic downturns, with most CEOs stating that they would look to increase prices and then assess opportunities to optimize costs.

This said Cybersecurity is a service that a modern-day business cannot live without. New businesses may look to delay an initial investment but current businesses in the eco-system are unlikely to stop spending. Therefore, we would expect that demand remains relatively sticky, but growth will slow.

Cybersecurity:

Gartner is forecasting cybersecurity spending to increase by 11% in 2023, following a 7% rise in 2022. They are of the view that this will be driven by application, cloud, and infrastructure security.

Cybersecurity market (Gartner)

With continued digital transformation initiatives by Corporates, as they seek efficiency and flexibility, there is a heightened risk of cybersecurity breaches. This contributes to greater demand for security services in these areas. The average data breach in 2022 costs $4.35M and so spending tens/hundreds of thousands is a no-brainer.

With an industry this important and thus lucrative, the level of competition is very high. Further, the level of technical capabilities is very high as hackers are constantly innovating. Most businesses look to specialize in a segment of the overarching industry, developing deep expertise and getting ahead via innovation.

BlackBerry has done relatively well to innovate in this industry and capture market share. As the list below shows, BlackBerry has several enterprise services that are generally well-regarded by Gartner reviewers.

BlackBerry services (Gartner)

Further, BlackBerry acquired Cylance in 2019 for $1.4BN , intending to specialize in AI Cybersecurity. CylancePROTECT is an AI-based endpoint protection platform that is highly regarded relative to peers.

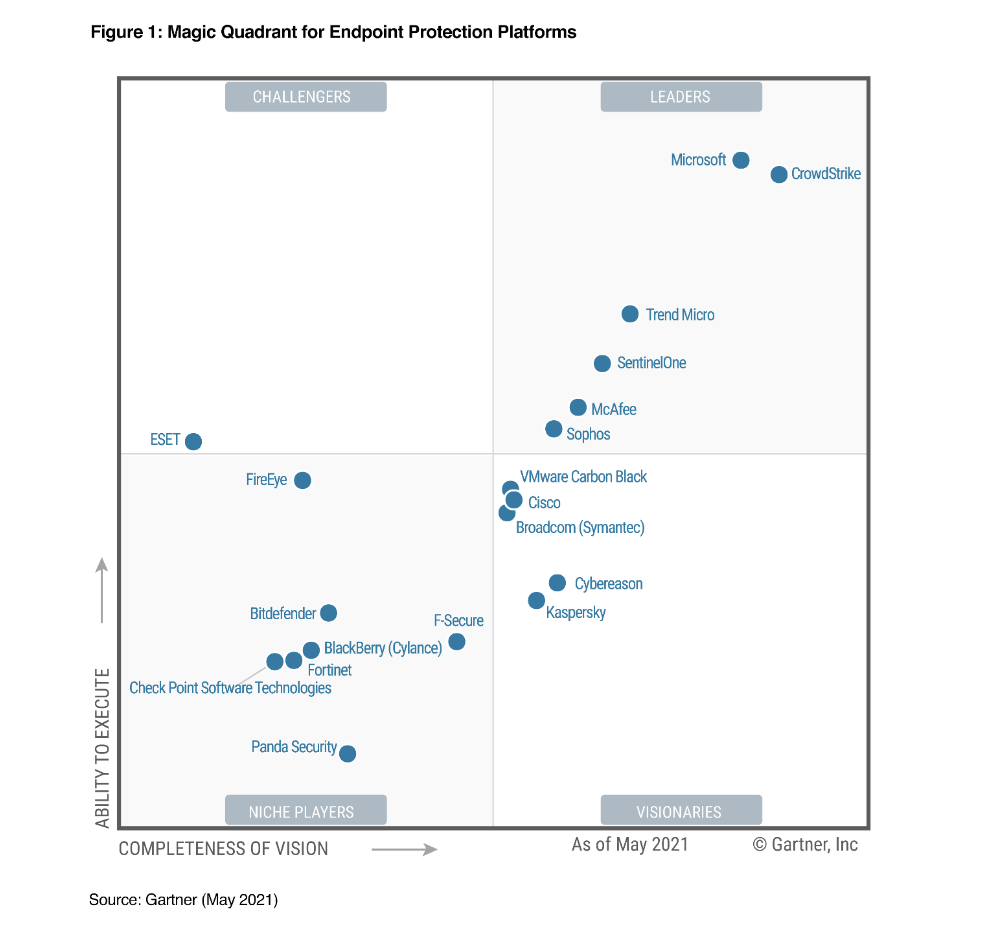

BB has done a commendable job in expanding into the Cybersecurity industry, especially given its relative resources. Fortinet ( FTNT ) and Palo Alto Networks ( PANW ) are 2 of the largest specialists in the space and have over 10x BB's market cap. If we look at Gartner's magic quadrant (The best businesses in a segment of a market) for Endpoint Protection Platforms in 2019 and 2021, we see BB outperforming both.

2019 Magic Quadrant (Gartner) 2021 Magic Quadrant (Gartner)

{kind=link}

We do have long-term concerns, however. BB's relative competitiveness and scope to grow may be limited. There is a reason the 2022 Gartner Magic Quadrant is not above, BB was replaced. The larger businesses will naturally be able to innovate faster, and this will reflect in the difference in growth. The idea that BB can capture any material level of market share is highly unlikely and it will most likely remain a niche player.

IoT:

The term Internet of Things refers to the idea that everyday products are connected to the Internet and are able to communicate with one another. This market has grown incredibly quickly as tech is incorporated into every facet of society. This is another area into which BB has expanded. Similar to the above, BB has done a good job in developing its foundations in the market, with its flagship QNX software ( Acquired in 2010 ). This allows for networked devices to have a computer embedded within them. The use case spans multiple devices, such as medical equipment and cars. QNX is used in 215M cars worldwide, which shows the breadth of services provided already. Further, in Q2'22 BB announced that they had reached an agreement with AWS to offer QNX on the cloud, further expanding the reach of this service.

Licensing:

BB holds an array of legacy IPs that it licenses to other businesses. This is by far the smallest revenue generator and is not considered a material aspect of the company's go-forward or attractiveness in our view.

Financials:

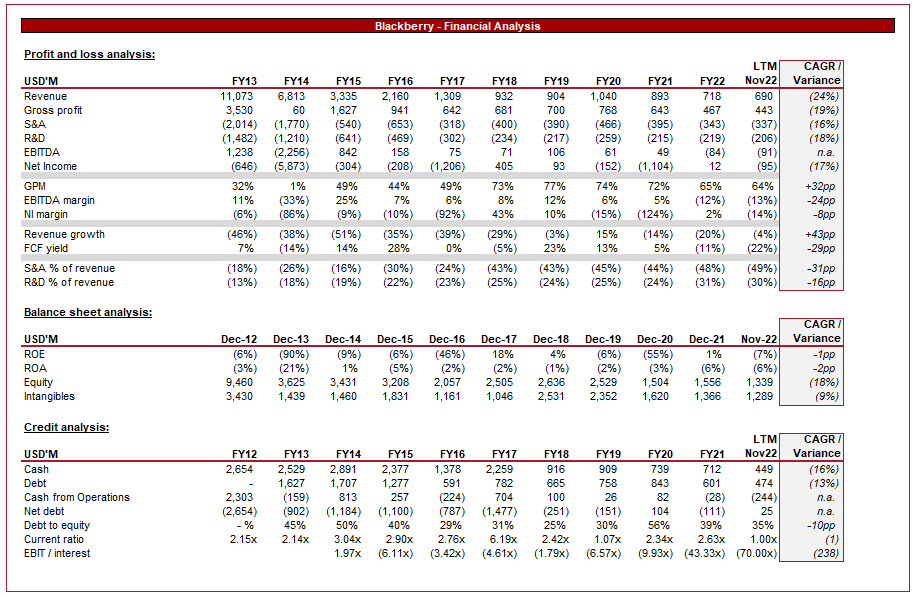

BB Financials ( TIKR Terminal)

{kind=link}

BB's historical financials are quite the sight, with a 24% rate of annual decline in revenue, translating to 17% net income. The reality is most of the P&L is not worth looking at as the business has completely changed.

Currently, BB is investing aggressively in S&A and R&D, intending to drive growth. This is critical as the business has developed the performance of its current service offerings, but this has yet to translate into improving Group revenue. With an EBITDA margin of 13%, the business should be able to transition to profitability if strong growth is achieved. For this reason, we are not too concerned about the business being loss-making.

The company has a debt/equity ratio of 35%, which is very good given its turbulent past. This will allow the business the optionality to grow further through M&A if the opportunity presents itself. This said the company is not yet cash flow positive and so further cash may need to be raised as early as this year to sure up their balance sheet.

Revenue:

Revenue mix (Quarterly financials)

Looking further into revenue, we observe our biggest issue with the business. There is no evidence of the turnaround occurring, by that we mean sustained growth. Between Feb21 and Nov22 Group revenue has declined, due to a decline in both cybersecurity and L&O. Had it just been L&O, we would not be concerned in the slightest, but CC too is very concerning. This seems to align with what we have observed in the Gartner MQ, with BB slowly losing market share as it is out-developed by competitors. IoT looks to be a gem in the rough, however, with a mammoth 80% GPM and healthy growth. Even this has flatlined in recent months, which could either be cracks beginning to show in this segment or a reflection of slowing economic activity.

Outlook:

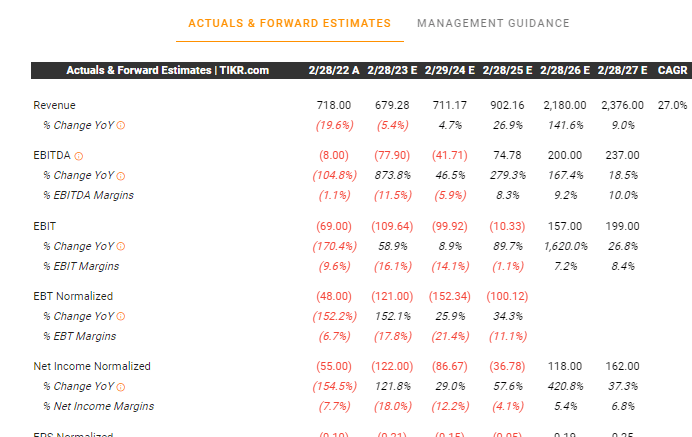

Analyst forecast ( TIKR Terminal)

{kind=link}

Analysts look to be forecasting the unlikely renaissance of BB, with revenue returning to the billions and a return to profitability in 2026. This will likely be driven by a turnaround of the CC business but more so by continued growth in IoT. The reason we suspect this is due to the forecast GPM of 72%, which means CC becomes a far smaller segment of total revenue.

Valuation:

Valuation ( TIKR Terminal)

With BB being EBITDA negative, we will consider a revenue multiple as a means of assessing the company's fair value.

BB is currently trading at 3.3x revenue, which is slightly below its peers. Of said peers, only Everbridge ( EVBG ) is not profitable, trading at a similar level (c.3.8x). Based on this valuation, our belief is that BB is currently overvalued. It is difficult to justify a buy when VMware ( VMW ) is only slightly more expensive.

Conclusion:

The sheer degree of BlackBerry's decline is impressive and any return to profitability would be equally so. We believe that there is certainly potential here, not for anything groundbreaking, but for healthy high-single-digit growth and profitability. The problem with investing now is that there is little in the way of tangible evidence of this coming to fruition. Further, at 4x revenue, you are pricing in high levels of profitability in the future and strong growth. Seeking Alpha's quant rating concurs with our assessment, rating the stock a hold.

We rate this stock a sell.

For further details see:

BlackBerry: Overvalued With Success Priced In