UNH - BME: A Solid Healthcare Fund For The Long Term

2023-04-14 11:18:53 ET

Summary

- BME continues to trade flirting at or close to premiums but remains a solid holding nonetheless.

- If you lack some healthcare exposure, BME could be one way to gain further exposure.

- The fund's distribution rate might not be as compelling as some other CEFs, but it's also one of the most steady.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on April 1st, 2023.

What does healthcare have to do with a banking crisis? Not much at all. Despite this, BlackRock Health Sciences Trust (BME) saw some declines with the latest market fiasco in March. BME even saw a small discount open up, which has become a fairly rare event for this fund.

So far, the market has looked past the turbulence we saw in March, with the broader indexes moving higher to end off the month. That being said, incorporating some healthcare exposure in one's portfolio can always be beneficial.

With BME, you also get a covered call strategy that is implemented on the underlying portfolio. Writing calls against portfolio names can help provide some small downside protection or benefit the fund even if the market is flat.

Since our last update, BME has come down some, but that came primarily from the last month. It was also due in small part to the premium coming down from where it was and now going to a slight discount.

BME Performance Since Prior Update (Seeking Alpha)

I'm not too concerned with what BME is doing over the short term, as I view this fund as a long-term holding.

The Basics

- 1-Year Z-score: -1.51

- Discount: -1.99%

- Distribution Yield: 6.18%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Assets: $576 million

- Structure: Perpetual

BME's investment objective is "total return through a combination of income, current gains, and long-term capital appreciation." They will attempt to achieve this by a pretty simple investment policy - "under normal market conditions, at least 80% of its assets in equity securities of companies engaged in the health sciences and related industries and equity derivatives with exposure to the health sciences industry." They will then implement a covered call writing strategy against positions in their portfolio.

This fund might not be as large as some of the newer BlackRock CEFs, but it can still offer plenty of daily trading volume for most investors. With no leverage, that's one less concern we have to be worried about with this fund in a rising rate environment. Additionally, that means we forgo the added volatility that comes from leverage. It seems fitting that healthcare is a defensive sector, and BlackRock doesn't add risk to that.

Performance - Discount Remains Rare

With the latest negative 1-year z-score, it tells us that the fund's current discount is actually unusual for this fund. In fact, this fund has usually traded at slight premiums for the last 3, 5 and 10 years as well. A deep and sustained discount has been quite rare for this fund in the last decade.

It was primarily during the GFC that we saw a regular discount. Which just so happened to come about shortly after the fund launched in 2005. If I could go back and invest in BME at that time, I certainly would have in hindsight. Of course, everything is much easier with the superpower of hindsight.

BME is a healthcare fund with a covered call strategy, so you wouldn't anticipate blistering returns that will make your eyes pop. Instead, moderately attractive returns seem to be more appropriate to expect.

BME Annualized Performance (BlackRock)

For the most part, you don't expect healthcare names to deliver multi-year double-digit returns but to act as a more defensive area of your portfolio. In the 2022 year specifically, BME saw a small total NAV return decline of -4.13%. Here's a look at the latest available annualized results for the fund.

On the other hand, as a CEF, the primary focus is often on distributions, which BME delivers in spades.

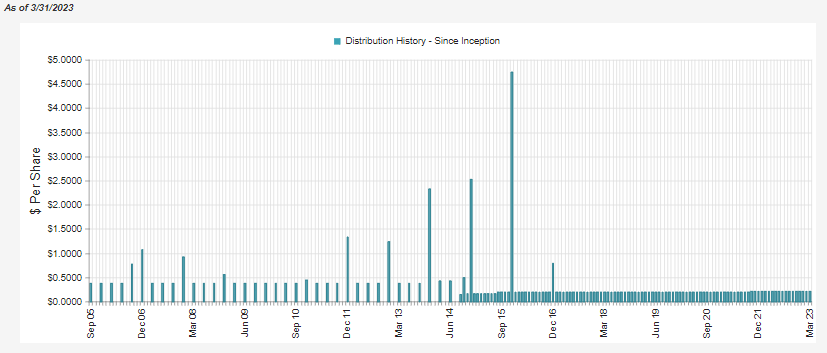

Distribution - Steady

BME is one of the only few closed-end funds that have not cut their distribution since inception AND was launched before the 2008/09 GFC. Funds that launched in the last few years or even the last decade that can boast no cuts are also fairly impressive, but funds that went through the GFC are even more impressive as it is quite rare.

They paid quarterly for the first half of their life, then switched to the more attractive monthly payout schedule. It doesn't really change whether it is worth an investment or not, but investors tend to value monthly more highly. If you are a reinvestor, then it can have the benefit of compounding ever so slightly quicker too. It takes years for that to compound, but it can be a benefit if you are a long-term investor.

{kind=link}

One way to keep a distribution steady is to pay a more moderate rate rather than pushing your payout to the limit. Thus, BME's 6.18% isn't likely to be overly appealing to those that chase higher yields.

The fund will also still require capital gains to fund its distribution. In fact, the entire distribution is almost reliant on capital gains. So if we saw several years of declines in the healthcare space and an overall weaker market, it could pressure the fund's distribution.

BME Annual Report (BlackRock)

Net investment income saw a big improvement on a relative basis from the prior year, but on an absolute basis, NII coverage still only comes to 4.48%. Since the fund regularly trades at a premium, they also have an at-the-market offering in the place where they regularly distribute shares out into the open market. Selling shares at a premium to NAV is accretive to the earnings of the fund.

That's why we can see NII and the distributions paid out increase even if there is no change in the fund's distribution. Still, on a per-share basis, NII was not meaningful in the prior year, and for the latest fiscal year, it was at $0.11.

We can also see in the above annual report that the fund didn't realize enough gains in the prior year to cover its distribution either. One thing that helped contribute to the gains it did realize was the options premium it generated from writing covered calls.

BME Options Premium Gains (BlackRock)

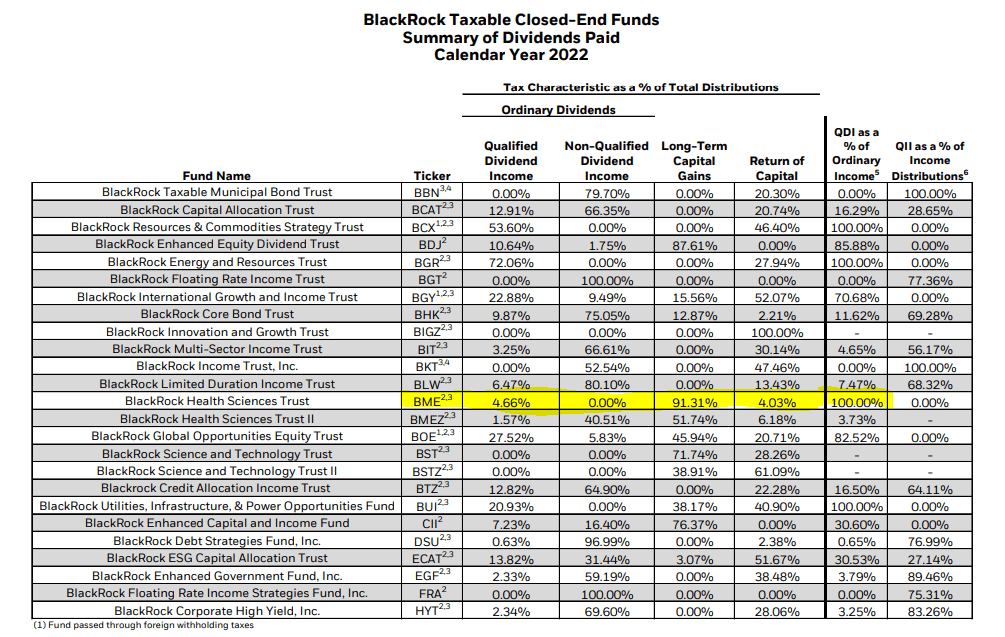

Despite what was a fairly big shortfall in distribution coverage from capital gains, the fund still only had a small portion of the distribution classified as return of capital for 2022 . The largest contributor was long-term capital gains, which both have their own tax benefits.

ROC reduces an investor's cost basis so it doesn't become taxable unless it is sold at a profit in the future. Generally, this isn't the type of fund you'd see ROC from regularly, but it can happen in weak years. LTCG also qualifies for a lower relative tax rate than ordinary income. The small portion that was identified as income was classified as qualified dividends. This can all make the fund more appropriate for a taxable account.

{kind=link}

BME's Portfolio

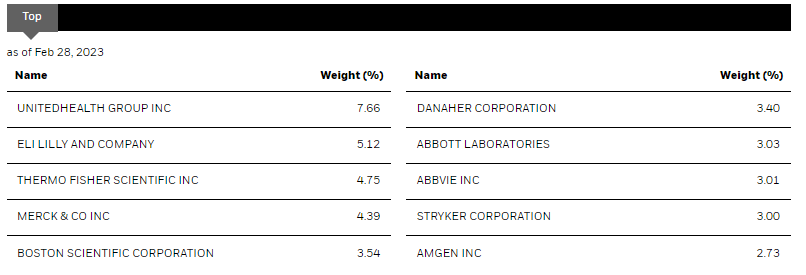

Despite what has been a fairly active portfolio in the last few years, with a 41% turnover rate in 2022, the fund's top holdings stay fairly consistent.

{kind=link}

UnitedHealth Group ( UNH ) continues to dominate the top spot as a health insurance behemoth. That being said, the weighting in this position has come down from the 10.11% we had seen previously. It looks like some of this was from trimming the position from what were 105,815 shares at the end of September 2022 to the annual report for the period ending December 2022, showing 97,235 shares.

The top ten listed above are as of the end of February 2023, but we don't have visibility into the precise number of shares the fund may be carrying. UNH was also included in the fund's call-writing strategy, so some of the shares could be called away through that strategy if they aren't closing out the contracts or rolling.

Thanks to UNH's allocation slimming down, the top ten represent 40.63% of the portfolio. That's still a material weighting in the fund, but it is down a bit from the 43.49% it represented previously.

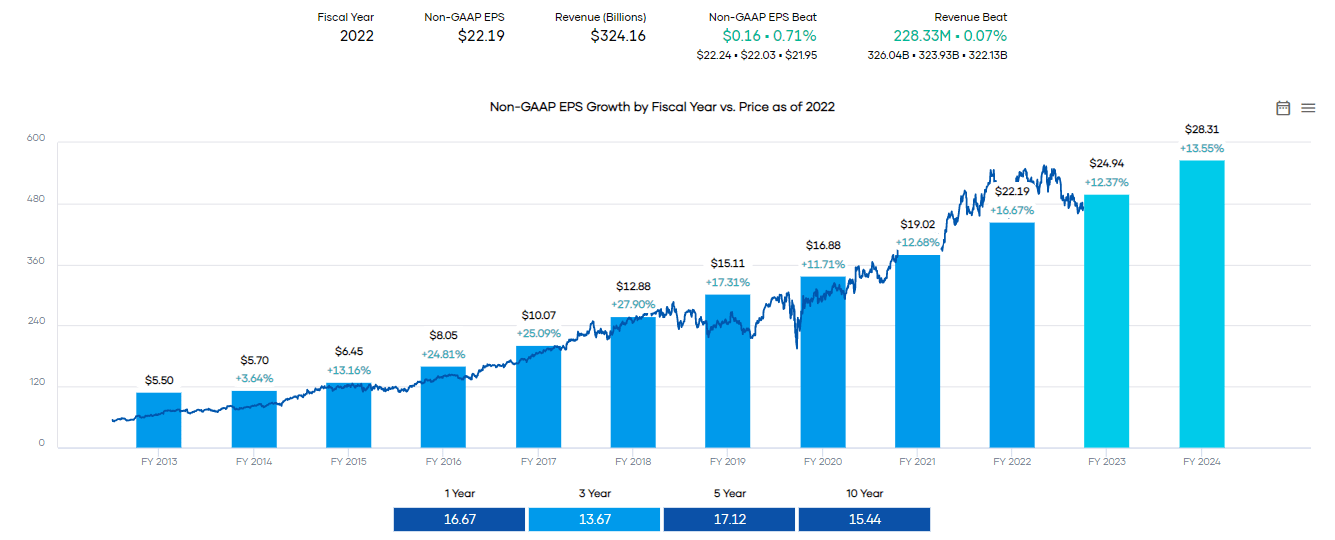

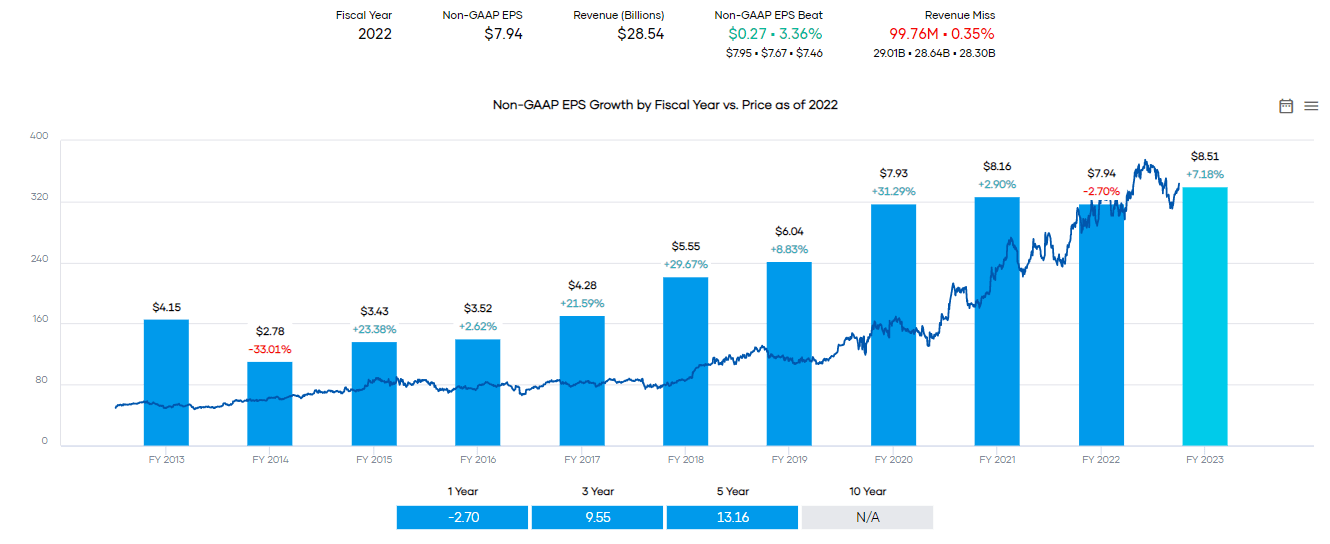

UNH has consistently shown strong earnings growth, so it makes sense it could become such a large position in the fund through accident or on purpose. Below is a look at their historical non-GAAP EPS growth and analysts' expectations for the next two years. The chart also displays the share price, which has been trending up for as long as the growth has been trending up. It was more in the last year. It seemed to have to get ahead of itself before correcting a bit lower. At a lower valuation now, it would appear there could be more growth going forward.

{kind=link}

Although, I might be a bit biased on UNH because I am also a shareholder of this name, and it has delivered solid results. That said, the growth is expected to continue, and that has provided strong growth in their dividend as well.

Eli Lilly and Company ( LLY ) has been less steady in terms of its earnings, but its share price has delivered impressive gains nonetheless. Here's a look at the historical non-GAAP EPS growth with next year's expectations from analysts.

{kind=link}

Overall, LLY also gets a lot of attention from analysts who rate it a buy and have an average price target of nearly $376. However, on a historical P/E ratio, it appears overvalued.

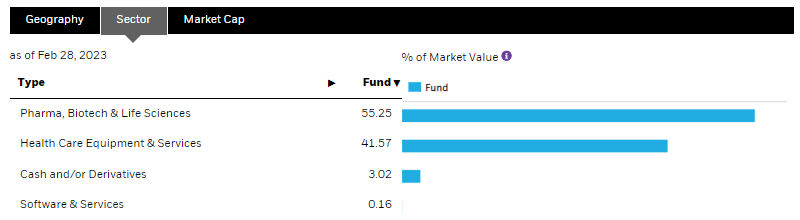

All this said, for BME, despite a fairly concentrated group of holdings at the top. The fund's website doesn't have a great visual breakdown of each industry as they lump them together into broader categories. Still, we are getting a fair bit of diversification spread across the sub-sectors of healthcare.

{kind=link}

Conclusion

BME is continuing to trade near premiums but has recently shown a slight discount. If this fund can be snagged at a discount, almost any discount, it's historically been a good time to buy. If we get some more market volatility kicking up due to unrelated concerns, it could present a strong time to consider adding this boring but usually extremely steady fund.

For further details see:

BME: A Solid Healthcare Fund For The Long Term