VRTX - BMEZ: Attractive Discount On This Riskier Healthcare Fund

2023-04-20 12:12:30 ET

Summary

- BMEZ launched right before Covid, riding up the boost when speculative growth took off.

- In 2022, the story was much different, and the fund struggled significantly.

- This fund is much riskier than its older sister fund, BME, but it also can provide more rewards for those that can handle volatility.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on April 6th, 2023.

Not a lot of investment themes worked through 2022, but growth investments were even worse off. One name, in particular, I wanted to focus on was the BlackRock Health Sciences Term Trust ( BMEZ ) (formerly BlackRock Health Sciences Trust II ) was one of those funds that were hit hard.

We recently touched on its older sister fund, the BlackRock Health Sciences Trust ( BME ), so updating coverage on BMEZ also seemed appropriate. BME and BMEZ are both BlackRock funds, and both invest in healthcare. However, that's about where their similarities end. The underlying healthcare themes they invest in are vastly different.

We've highlighted this before , but to quickly recap, the largest difference between the two is that BME invests in more traditional healthcare names that are defensive. BMEZ invests in growth-oriented healthcare names with a heavier focus on biotech, and they also include a material portion of their portfolio in private investments. Additionally, as the new name would suggest, it is a term fund rather than perpetual.

The Basics

- 1-Year Z-score: 0.46

- Discount: 13.90%

- Distribution Yield: 10.52%

- Expense Ratio: 1.32%

- Leverage: N/A

- Managed Assets: $2.023 billion

- Structure: Term (anticipated liquidation January 29th, 2032)

BMEZ has an investment objective to "provide total return and income through a combination of current income, current gains, and long-term capital appreciation. It intends to do this through "at least 80% of its total assets in equity securities of companies principally engaged in the health sciences group of industries and equity derivatives with exposure to the health sciences group of industries."

With this, it also utilizes an options strategy. They have no leverage in the form of borrowings, which is probably a good thing considering how volatile it can be already.

Going into the more detailed investment approach included in the prospectus, we can see this included:

Equity securities in which the Trust anticipates investing include common stocks, preferred stocks, convertible securities, warrants, depositary receipts and limited partnership interests in real estate investment trusts that own hospitals. The Trust may invest in shares of companies through initial public offerings ("IPOs"). The Trust may also invest, without limit, in privately placed or restricted securities (including in Rule 144A securities, which are privately placed securities purchased by qualified institutional buyers), illiquid securities and securities in which no secondary market is readily available, including those of private companies. Issuers of these securities may not have a class of securities registered, and may not be subject to periodic reporting, pursuant to the Securities Exchange Act of 1934, as amended. Under normal market conditions, the Trust currently intends to invest up to 25% of its total assets, measured at the time of investment, in such securities.

The fund's term structure means that investors should receive NAV near the liquidation date. That's quite a ways off at this point, so not necessarily something we could look to take advantage of right away. However, it is something that should be considered before investing in this fund. The fund can go perpetual if they conduct a tender offer for 100% of shares at 100% of NAV before the termination date. If there are still $200 million in net assets after the tender offer, the fund can switch to perpetual.

In addition to that, they also leave in the usual caveats that they can extend the termination date if we are in a market crash during the time of liquidation.

Performance - Discount Narrows A Touch, Remains Attractive

Since our last update, BMEZ has held up fairly well, providing some returns since mid-2022. A lot of those gains coming in the last couple of weeks alone.

However, BMEZ continues to trade at an attractive discount. The fund's history isn't that old, so trying to gauge a historical range could be less reliable than usual. Some of the fund's discount is going to be the result of its private investments as well.

Though it remains a more speculative position given the types of underlying holdings that it carries. While there are greater risks, there are often greater rewards if things work out. As we saw shortly after the fund was launched, it crashed during Covid but rode a massive wave higher when growth was a huge beneficiary of the lockdowns. Since then, the fund struggled with the rest of the growth area when rates rose so rapidly.

I think providing a good comparison between the differences in BMEZ and BME can be summed up in the performance charts below. Initially, BMEZ had done incredibly well, while BME provided a slow and steady type of recovery. BME then remained rather steady even in the face of significant interest rate increases through 2022, while BMEZ crumbled under pressure.

Ycharts

With that being said, that's some of its appeal now. The Fed's higher interest rates are starting to slow the economy and jobs, as well as getting an uptick in bankruptcies . While the Fed can't come out and say that's what they want, that's precisely what starts to kill inflation. If rates stabilize or even fall later in the year or early 2024, that could see BMEZ as the beneficiary.

As we already saw with that idea in place, the fund's discount started to narrow as the fund's share price started performing better than its NAV. I believe that is in anticipation of what could come. Thus, why the fund's 1-year z-score is now pushing nearly 2. Now, I'm not saying it's going to be a smooth ride, as a recession is likely to make things very bumpy.

Distribution - Attractive, But Coverage Is A Concern

They have continued to maintain the same monthly $0.145 distribution that they bumped up to during 2021. That was despite cutting some of their other growth-oriented funds at this point, specifically BlackRock Innovation and Growth Term Trust ( BIGZ ) and BlackRock Science and Technology Term Trust ( BSTZ ) (formerly BlackRock Innovation and Growth Trust and BlackRock Science and Technology Trust II, respectively, which were also renamed recently.)

That said, with the fund's NAV distribution rate at 9.31% and reliance on capital gains, this is the type of environment where it could be at risk for a cut.

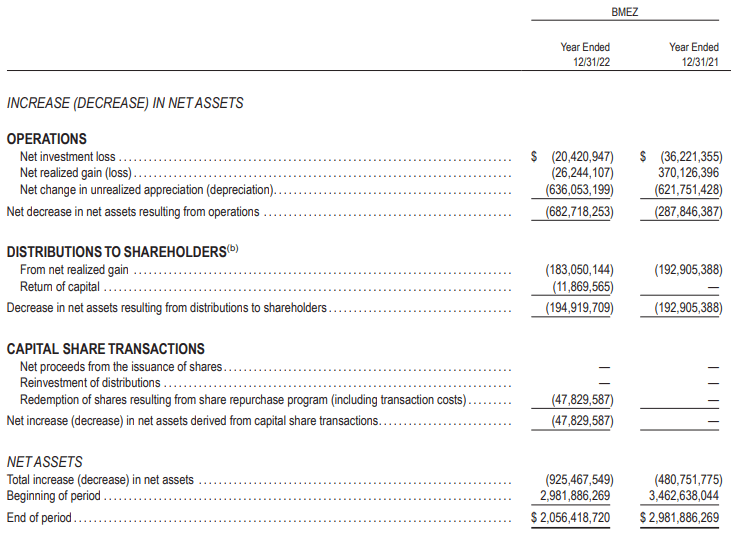

One of the silver linings is that the fund's options writing strategy has generated a fair bit of realized capital gains for the fund. That helped offset a large portion of the realized losses on the portfolio. Of course, with massive unrealized losses, it hardly made a dent for the prior year against the decline in the NAV. Had it not been for the option writing, losses would have been even worse.

BMEZ Realized/Unrealized Gains/Losses (BlackRock)

It isn't unusual to see an equity fund rely on capital gains to fund its distribution, but in the case of BMEZ, it is solely responsible for covering the distribution. The fund doesn't provide any net investment income. Even total investment income came to less than $9.2 million in the prior year. For the size of the fund, that is only a minuscule amount. This is precisely because of the fund's focus on growth and private investments.

{kind=link}

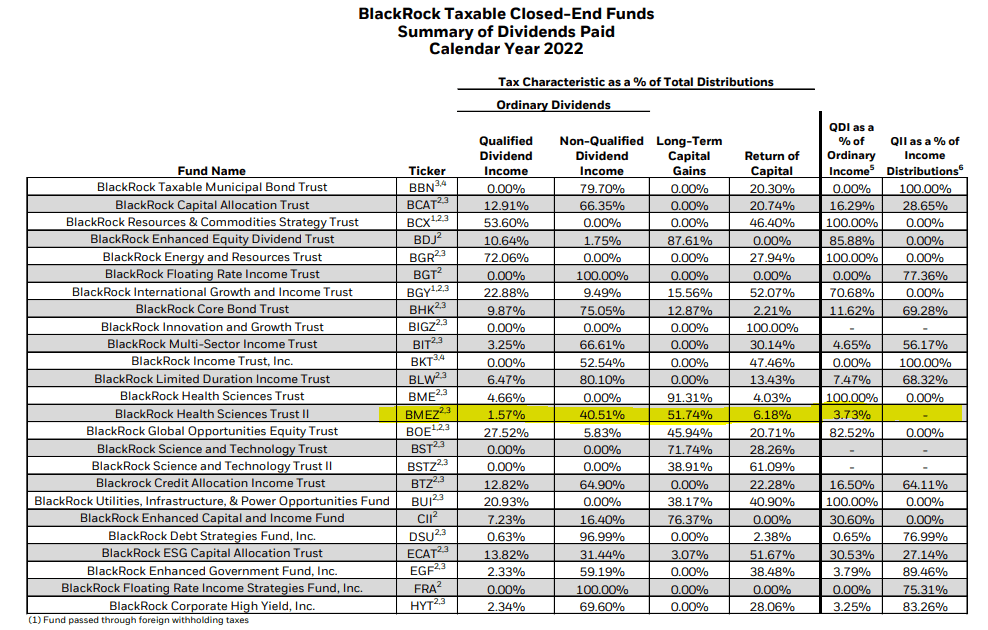

Given the sizeable losses in the prior year, it might come as a bit of a shock that most of the distribution isn't classified as return of capital. Only a small portion is, with the larger allocation being long-term capital gains and non-qualified dividend income. That would be vastly different from the coverage metrics we see above.

{kind=link}

This is a good reminder that tax classifications aren't representations of actual distribution coverage as so many investors seem to believe. While they can tend to correlate, they are two separate data points to consider and interpret. In the case of BMEZ, it would appear that realized long-term gains from the prior year being so large were pushed into this year.

BMEZ's Portfolio

The fund listed nearly $180 million in securities in its portfolio as restricted, which is around 8.7% of the portfolio. Despite that, BMEZ's turnover is fairly high at 63% in the last fiscal year.

The fund had a target to invest 25% of the fund's assets in private investments. They achieved that mark, but since a significant part of those names went public since investing, at the end of 2022 , their private allocation stood at 8%. That was through only 18 private investments. That's in a portfolio that lists around 400 holdings in total.

Part of the reason that a discount can open up on funds that focus on private investments is due to skepticism about its valuation. However, with a more minimal allocation to private investments at this point, the discount seems to be excessive.

{kind=link}

We can also see that in 2022, they put no capital to work in any private investments. However, they noted that "the team continues to perform due diligence on multiple new opportunities and expects to further increase exposure to private assets over the coming quarters..." Ultimately, with a target of 25%, they are well under that target at the moment. Given the environment has been incredibly tough for start-ups and growth companies, 2023 could also remain a year of slim investing on the private front.

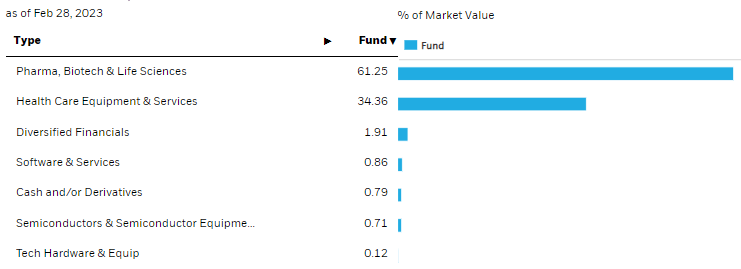

With a quick glance through the list of private investments they had or are invested in, we can see that biotech is a significant part of their approach. This makes sense as well, as that's the growth industry within the healthcare space. So it might not be too surprising to see that the portfolio is just over 40% in biotechnology, commanding a dominating overweight position relative to the other sub-sectors.

BMEZ Sector Breakdown (BlackRock)

The fund's website lists a fairly broad sub-sector classification to see the breakdown for the portfolio. However, it's as of the end of February 28th, 2023. So updated more recently than the above breakdown that was reflected in the fund's Q4 commentary.

{kind=link}

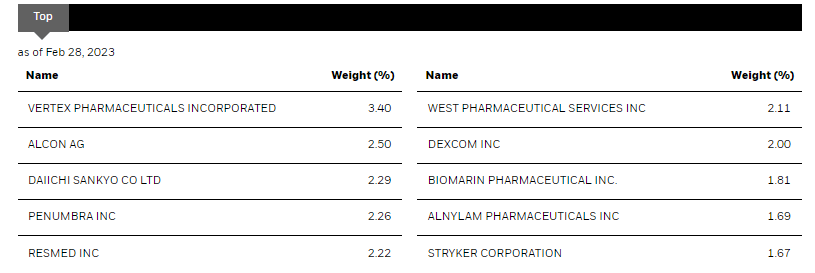

The fund lists just over 400 holdings in the entire portfolio, but a few of the larger positions in the funds top ten make up a fairly large size given the number of holdings.

{kind=link}

Vertex Pharmaceuticals ( VRTX ) is a publicly traded biotech company. This was formerly the largest position as well at the end of June 2022, and it has since expanded its allocation from the 3.12% it was previously. Helping to achieve this expanded position and to retain the top spot was that we saw a pretty good performance in the last year.

In fact, every top ten position in BMEZ is a publicly traded company at this time, which is another reflection of being light on their private investment target.

Ycharts

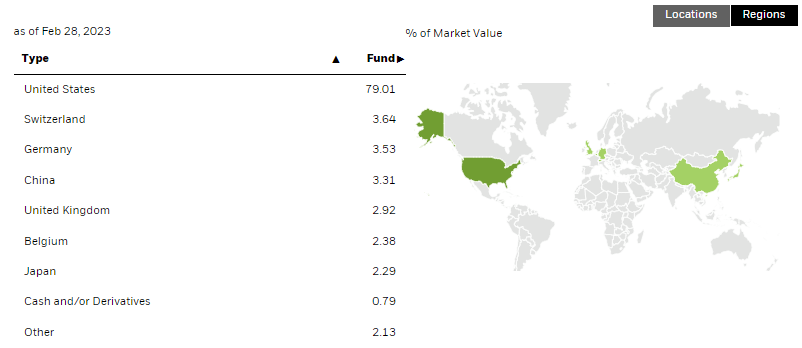

While VRTX's performance was relatively strong, Daiichi Sankyo ( OTCPK:DSNKY ) was a top performer in the last year. This is a Japanese pharmaceutical company that trades on the pink sheets. This was the fifth largest exposure that BMEZ had in the June 2022 update list, and it had a 1.74% position. Naturally, we've seen that allocation expand as well. Most of the portfolio is allocated to U.S. holdings, but that still leaves room for exposure to other countries. At this point, DSNKY appears to represent the entirety of the Japan exposure.

{kind=link}

The worst-performing top-ten position in the last rolling 1-year period was West Pharmaceutical ( WST ). This position was not actually one of the largest positions in our last update, meaning it was a new name to the top ten despite the weaker relative performance. That being said, at the end of June 2022 , it was a position that BMEZ held with 39,055 shares. The fund ramped up the number of shares to 134,085 by the end of 2022. The next annual report should be posted in about a month and a half and would give us an idea if they expanded their position even further in Q1 2023. WST is a life science healthcare name located in the U.S.

Conclusion

BMEZ remains an attractive fund to consider if an investor can withstand relatively higher risks. For investors looking for a more boring healthcare allocation, BME could be a better fit. BMEZ is a bumpier ride, but that can also provide a better reward at the end. If interest rates stabilize or even are cut in the next year or so, that could bode well for the whole growth space, and BMEZ should be a beneficiary of that as well. While the distribution could be cut, as a CEF, it's highly likely that it will continue to pay at least some distribution going forward.

For further details see:

BMEZ: Attractive Discount On This Riskier Healthcare Fund