CA - Boardwalk: It Is Time To Sell

Summary

- Boardwalk reported Q4-2022 results and hiked the dividend again.

- FFO came in ahead of consensus and guidance for 2023 is good.

- We tell you why we still consider this a sell at the current price.

Note: All Amounts Discussed Are In Canadian Dollars

When we last covered Boardwalk Real Estate Investment Trust ( BEI.UN:CA ) ( BOWFF ), we gave it due credit for navigating the complex challenges it faced. At the same time we were not ready to issue a buy, especially when there were better suited candidates. Specifically we said,

The bulk of Boardwalk's portfolio is also insulated from rent control markets and it can hike rents at will. If there is a bearish slant here, it comes from trying to figure out where 4.00% cap rates fit in a world where risk-free rates are higher. This remains a difficult question to answer and one that is best done using a wide margin of safety and stress testing investing assumptions at 6% cap rates. It would also not be unusual to see it trade at 12-13X FFO in this climate. Boardwalk looks ok here, and we think there are a couple of better relative bargains in Canadian space. We rate it a hold and would get excited if we saw it under $45.00.

Source: Navigating Higher Rate Challenges

Boardwalk of course decided to go in the other direction and outperformed the markets handily.

Seeking Alpha

That's ok. As investors can see, we are very, very picky with our buy points and there is only one green dot on the chart above. With Q4-2022 results out , we took a look to see how the REIT was progressing.

Q4-2022

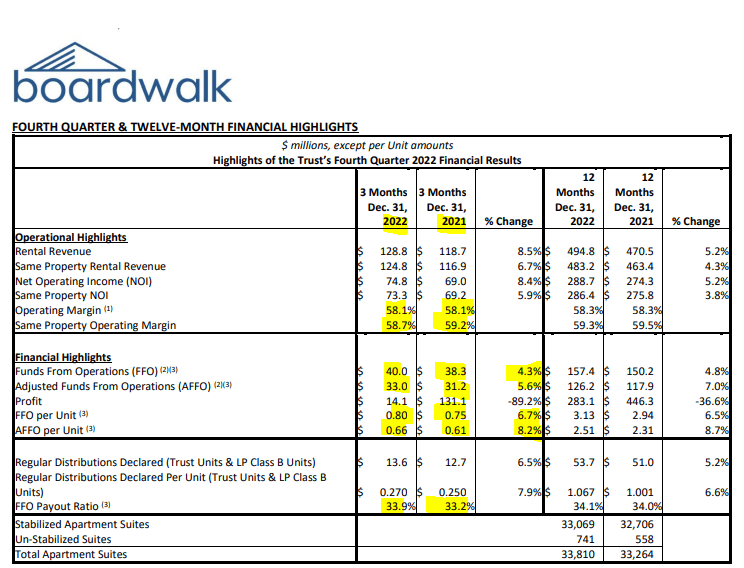

Boardwalk beat consensus estimates with funds from operations ((FFO)) coming in at 80 cents for Q4-2022. Revenues and net operating income ((NOI)) rose strongly from Q4-2021 levels.

Boardwalk Q4-2022 Financial Results

{kind=link}

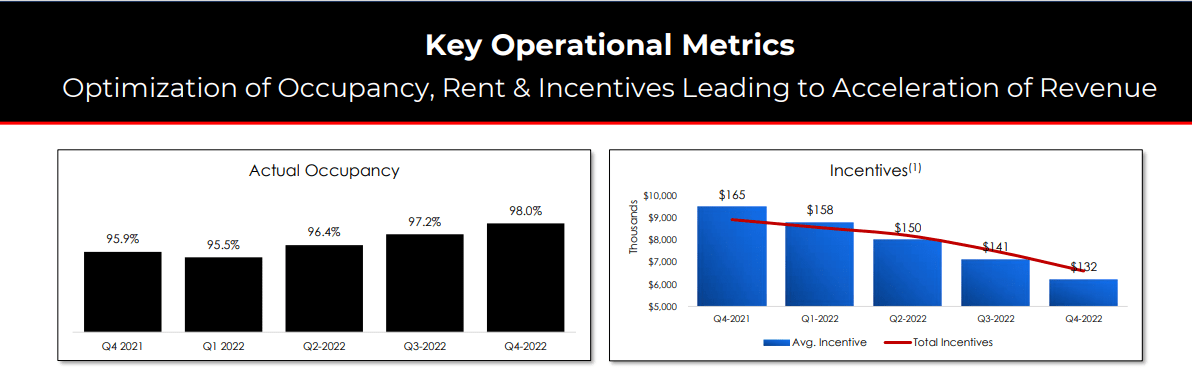

There were a couple of spots of weakness here as we saw that total FFO rose less than rental revenues and same property operating margin declined a bit. Through this upcycle Boardwalk has been powering gains on to FFO by operating leverage and financial leverage, and we are seeing early signs that both are reversing. Why are both reversing? Well the same property NOI is driven by the revenue to expense ratio and the very high inflation and labor shortages are likely beginning to hurt over there. You are also reaching a point of diminishing returns on occupancy and on rental incentives.

Boardwalk Q4-2022 Financial Results

{kind=link}

There is not much room to expand occupancy and very little room to reduce rental incentives. On the FFO front, interest expenses are ballooning faster than the rate at which NOI is rising. Interest expenses were up 16% year over year. Boardwalk continued its tradition of a having a very low payout ratio, but hiked its distribution once more, this time by 8.3%, starting with the March payment. This is the minimal payment required to stay within REIT guidelines.

Outlook

The FFO guidance for 2023 was set at $3.25 to $3.45 per unit. That is a solid 7% increase over 2022 levels at the midpoint. Some of this growth per unit is also coming via the opportunistic buybacks during 2022. While that creates yet another year of growth, we see risks with this outlook, especially as we move into Q3 and Q4 of 2023. Even the stated numbers are not too far ahead of the Q4-2022 run-rate of $3.20 per year. We are late in the cycle and you have to be careful to not extrapolate growth rates into infinity as analysts are too fond of doing. In case you have doubts about that logic here are Boardwalk's 2014 FFO numbers.

Boardwalk 2014 Annual report

Not sure how many of you were following the company at that time but if someone told you that the 2023 FFO would be lower than this $3.37 what would you have said back then? So late cycle logic is that you have to be careful and pick your spots to go long. This isn't one of them in our opinion and the reason is that there are two major risks. The first being that a small decline in occupancy alongside flatlining rents would create quite a drag on the FFO. The second is that interest costs are still rising quite sharply and Boardwalk is quite levered.

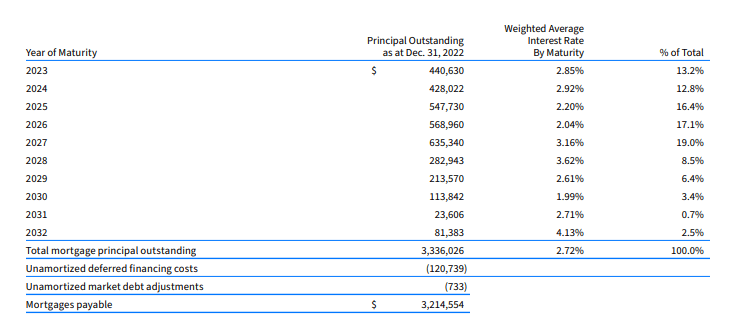

In the fourth quarter, Boardwalk renewed $161.5 million of its maturing mortgages at a weighted average interest rate of 4.48% while extending the term of these mortgages by an average of 3.8 years. In 2023, the Trust anticipates $440.6 million of mortgages payable maturing with an average in-place interest rate of 2.85% and will continue to renew these mortgages as they mature. Current market 5 and 10-year CMHC financing rates are estimated to be 4.25% and 4.00%, respectively. To date, the Trust has forward-locked or renewed the interest rate on $42.2 million or 9.6% of its maturing mortgages in 2023 at an average interest rate of 4.49% and an average term of 3.3 years.

Source: Boardwalk Q4-2022 Financial Results

Boardwalk's total outstanding mortgages have a weighted interest rate of 2.72%. The comparatives for 2023 and 2024 are actually better as there are about $869 million at a weighted rate of 2.88%.

Boardwalk Q4-2022 Financial Results

{kind=link}

Here we mean "better" as in the prevailing rates will create less of a bump up on those mortgages at renewal time. Those are still big jumps and any kind of occupancy drops or flattish rents, or even NOI dropping due to poor expense controls, will bring this to the forefront.

Verdict

Yes, if you want to hold on the Boardwalk today or any other REIT for that matter, you can always find comfort in the NAV. Despite the nice run-up, the stock trades at a discount to NAV, so can make the case that it is still cheap.

We of course don't think that and for us the NAV is a small guide post and not the entire map. The cap rates are likely to expand here, especially with the risk free rates now at 4%. The direction of NAV is very important and we go back to our decade long flat FFO example. Even NAV is about flat over the last decade.

The REIT is trading at $59.32 as we type this and at 17.7X FFO. The dividend yield despite the recent hike remains extremely small and near 2%. We see more risks than rewards at this point and we are downgrading this to a Sell rating. Our fair value remains about $50-$52 and at the top end of that range is where we would consider upgrading it back to neutral, assuming fundamentals remain unchanged.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Boardwalk: It Is Time To Sell