CA - Boardwalk REIT: Compelling REIT At A Not So Compelling Price

2023-09-18 11:43:45 ET

Summary

- Boardwalk REIT has been the best performing residential REIT in Canada and the US since September 2022.

- Alberta's strong population growth has led to leasing spreads of 10-14% on new leases and 8-9% on renewals, benefiting BEI's portfolio.

- The valuation is too rich given the headwinds it will realize from higher rates and expenses. I am taking a pass.

Introduction

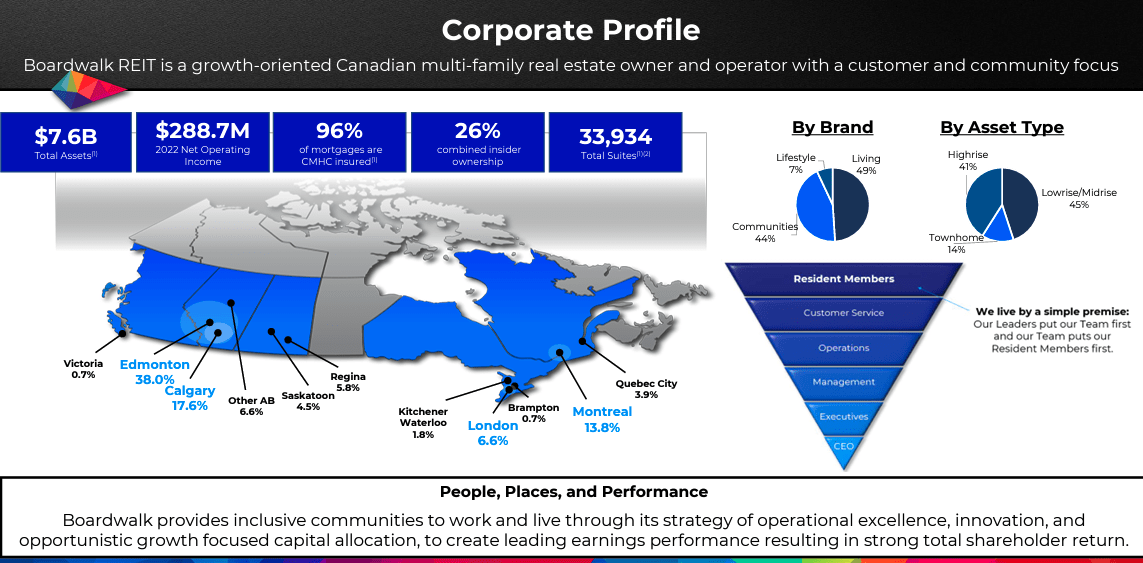

Boardwalk REIT ( BEI.UN:CA ) owns and operates multi-family rental communities predominantly in Alberta but with some properties in Ontario, BC, Quebec and Saskatchewan. BEI provides homes in more than 200 communities, with over 33,000 residential suites totaling over 29 million net rentable square feet. BEI operates under three tiered and distinct brands which include Boardwalk Living, Boardwalk Communities, and Boardwalk Lifestyle, which cater to a large diverse demographic and has evolved to capture the life cycle of all Resident Members. The living brand accounts for 49% of their assets which is more "affordable value" housing.

{kind=link}

BEI has been far and away the best performer out of all larger Canadian and U.S residential REITs since September 2022 despite facing the challenges of higher interest rates and rising wage costs. I discuss how this REIT has gained so much favour and whether this is still a good investment choice or not at the current price point.

Investment Thesis

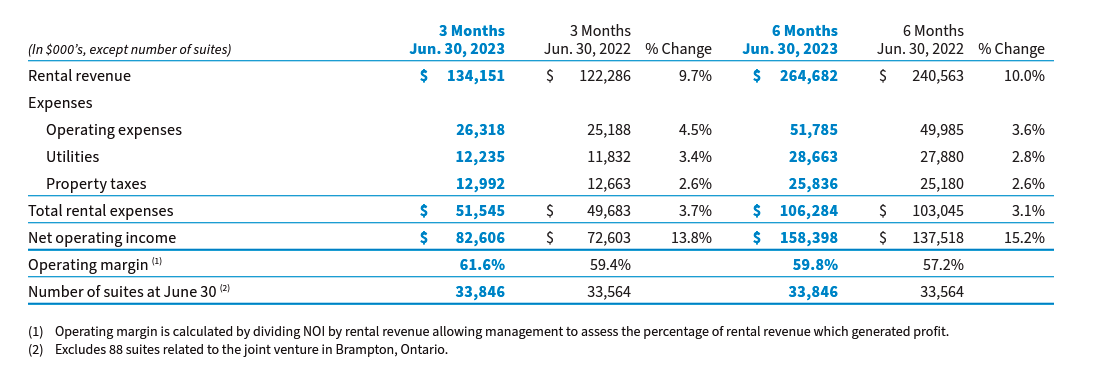

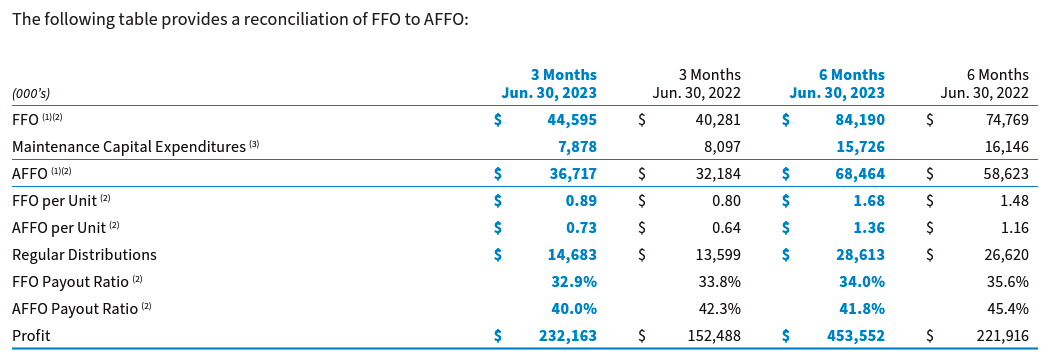

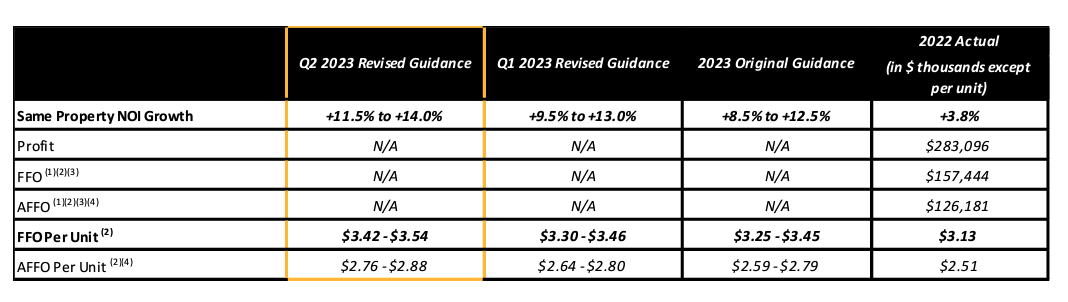

Despite interest expenses increasing ~15% and operating expenses increasing ~4% through the first six months of 2023 relative to 2022, NOI, AFFO, and AFFO per share increased ~15%, 19% and 17% respectively.

{kind=link}

{kind=link}

The increased rental revenue more than offset these increased expenses as the increase in rental revenue was due to higher renewal/re-leasing spreads, lower vacancy loss, and lower incentives offered, as well as the addition of new acquisitions during 2022 in Alberta and Ontario and the new acquisition in April 2023 in BC. BEI was able to reduce incentives by 37.2% year-over-year, while also reducing vacancy losses by 57.5%.

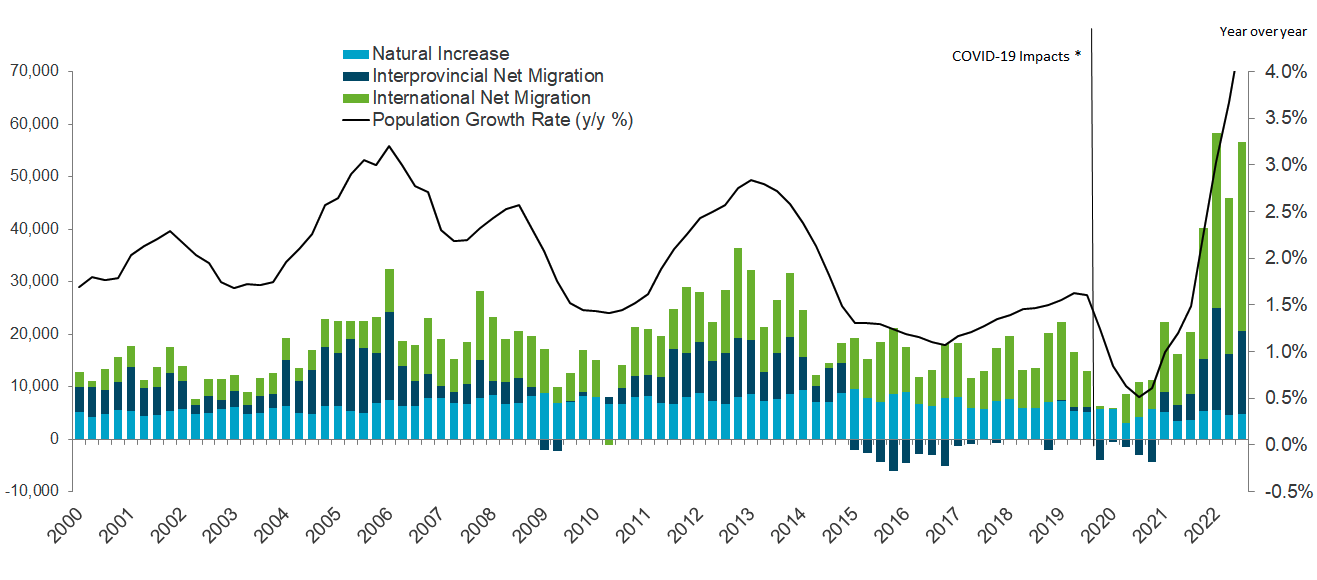

A few years ago I might have been sheepish on BEI's concentration in Alberta due to the province's weaker economic growth relative to most other parts of Canada as landlords were almost giving properties away to get them rented. Nothing could be further from the case today. As Alberta has witnessed the highest population growth over the past four quarters in Canada driven in large part from international migration. Alberta's population grew 4.46% between April 2022 to April 2023. The increases in population growth are attributable to the improving economy that is largely driven by oil and gas prices which have been on the rise, but also the affordability in its larger cities like Edmonton and Calgary relative to other large cities like Vancouver or Toronto.

Alberta components of population change, 1st quarter of 2023 (Alberta.ca)

{kind=link}

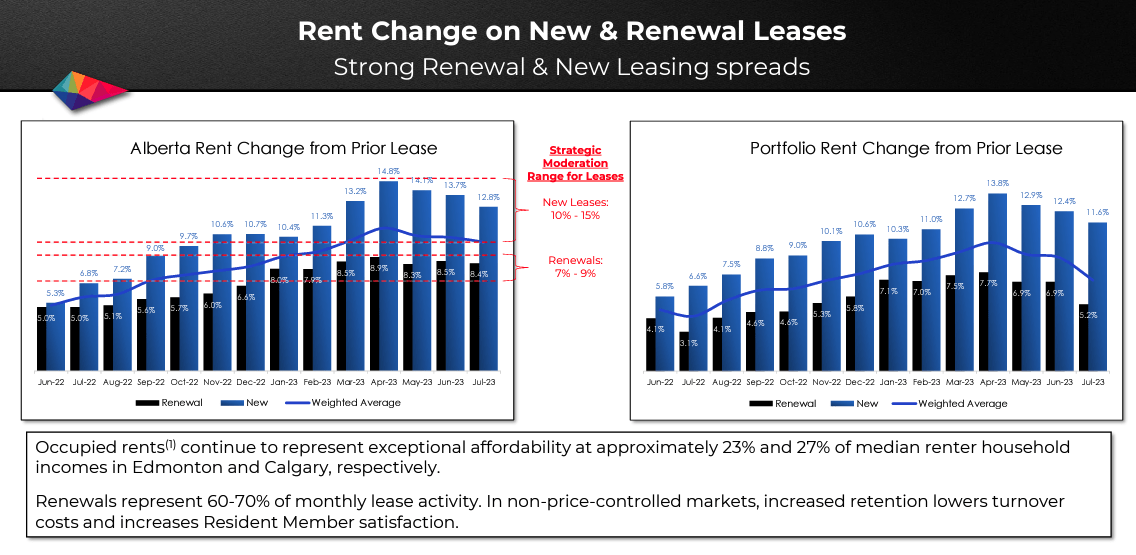

The result of this higher than average population growth has led to leasing spreads of 10-14% on new leases and 8-9% on renewals. I should point out that Alberta provincial laws are less restrictive on renewal caps than BC and Ontario which has greatly impacted residential REITs operating in those provinces, most notably Canadian Apartment REIT ( CAR.UN:CA ).

{kind=link}

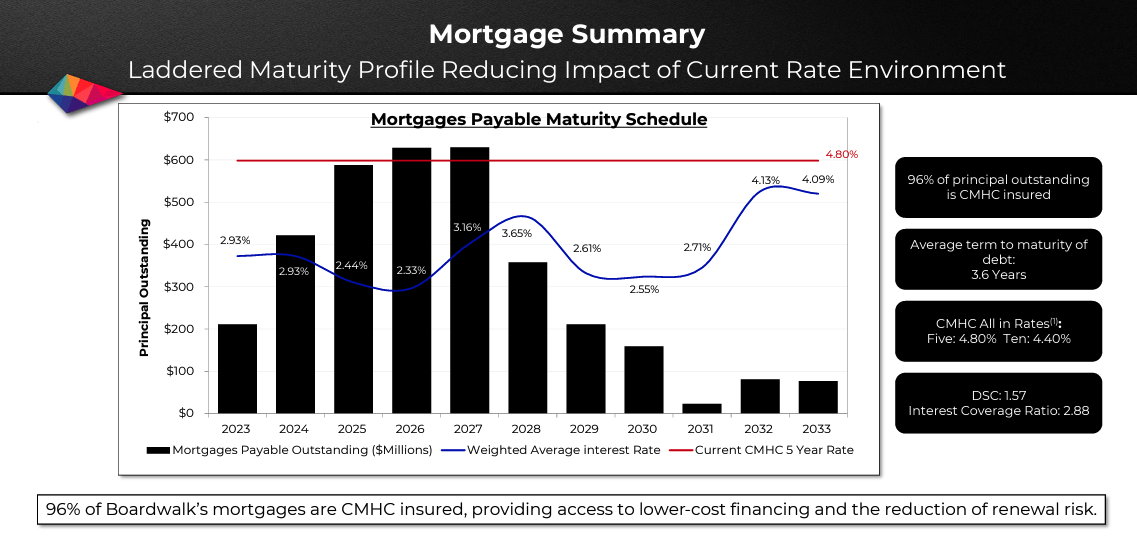

The portfolio also sports a ~99% occupancy rate so not a whole lot to not like until we move onto the debt side. I'm not the biggest fan of their staggered maturity schedule in a rising rate environment. The weighted average interest rate as at June 30, 2023, was 2.87% compared to 2.72% as at December 31, 2022, and as mentioned previously, interest expense has risen 15% YoY so the impacts of rate increases are already making an impact. The REIT only has $42MM in cash and $93MM in unencumbered assets so they are $75MM short in liquidity to fully repay their 2023 debt maturities which total $210M, so it will need at least $75MM in refinancing. $106MM has already been refinanced at a weighted average rate of 4.42%, for an average term of five years. Therefore, it would not be outside the realm of possibilities to see annual interest expense increase by $10MM over the next two years. The ace BEI has up their sleeve is that their payout ratio is only 42% even at the lower end of AFFO guidance so the dividend seekers who hold the stock need not worry too much about a cut.

{kind=link}

{kind=link}

Valuation

Despite the robust portfolio, BEI's relative valuation appears a little too rich. With an EV/EBITDA of ~24X which is high even compared to its Canadian peers never mind its U.S. peers which trade at 16-19X their 2023 EBITDA. The even more perplexing thing is its U.S. peers carry half the leverage that the larger Canadian REITs do and still have the lower valuation. Some could argue BEI's debt is less risky due to the CMHC backing, but a multiple turn of 7-9X greater is a stretch.

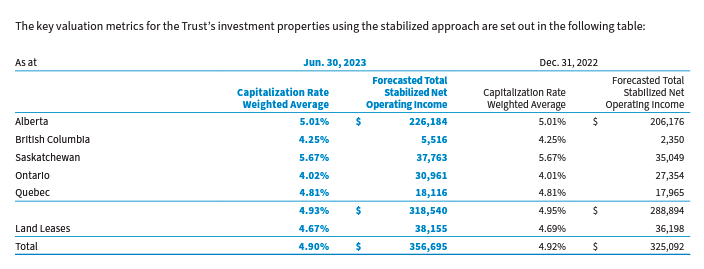

The REIT has calculated a NAV of ~$81/unit which would imply it is trading at a 13% discount from the current price of ~$70/share. The capitalization rate for which it is valuing its Alberta properties seems a little too low which makes a big difference in the valuation given the high leverage. At least 49% of properties are considered "affordable value" or layman's terms for "budget property" it's hard to see how these properties could demand a cap rate of less than 5.25%. In addition, the implied capitalization rate on the portfolio using the current market price and trailing NOI is 4.6%. This is not that impressive compared to the yields currently being offered in the residential market or even the 5-year Government of Canada Bond Yield which is currently ~4.0%.

{kind=link}

{kind=link}

{kind=link}

Conclusion

I deem the fair price per share to be $50/unit using annualized NOI for 2023 and a 5.25% capitalization rate on its assets, which goes to show how sensitive the NAV is to changes in capitalization rates. Those who say using 2023 NOI as a guideline is too conservative given the lifts they can realize on re-leasing need to remember that Q1 and Q4 are where the highest expenses are realized. Natural gas prices were fortunately lower than usual in the early part of the year but all signs are pointing to an upward trajectory for the next few months, never mind the increasing interest expense to be expected as well.

{kind=link}

I'm taking a pass on this stock as there are better risk/reward profiles on other residential REITs such as Dream Residential REIT ( DRR.UN:CA ) that I have discussed on this forum.

For further details see:

Boardwalk REIT: Compelling REIT At A Not So Compelling Price