CA - Bonhoeffer Capital - Terravest Industries: An Attractive High Growth Play

2023-06-24 02:45:00 ET

Summary

- TerraVest Industries is a materials fabrication and service firm providing components and services for oil and gas extraction, transportation, distribution, and commercial and residential usage.

- The company has four levers for cash flow growth: buying a firm in their core or adjacent market, expanding within existing markets, paying down debt, and distributing excess cash as dividends or buying back shares.

- TerraVest's risks include operational leverage, financial leverage, and slower-than-expected acquisition growth. Potential catalysts for growth include higher-than-expected acquisition growth, faster growth in end markets, and increased local scope or purchase of local scale in new markets.

The following segment was excerpted from this fund letter.

Terravest Industries ( TVK:CA )

TerraVest is a materials fabrication and service firm providing components and services for oil and gas extraction, transportation, distribution, and commercial and residential usage. TerraVest’s products support the transportation and storage requirements for oil, natural gas, LNG, and RNG across the US and Canada. TerraVest has three market segments as:

- a manufacturer of tanks for residential oil and gas storage, furnaces, commercial oil, and water storage tanks and boilers, as well as vessels for liquid natural gas storage and truck transportation;

- a manufacturer of natural gas wellhead processing, storage, and transportation equipment; and

- an oil and natural gas services provider including fluid handling, water management, heating, rentals, and well servicing utilizing 21 servicing rigs.

TerraVest is a collection of firms competing with smaller private businesses or divisions of large firms in niche markets described above. In each of its market niches, TerraVest is the number one or number two competitor. The common theme amongst these businesses is metal bending for high value-add applications.

Management strategically acquires businesses in direct negotiation with primarily family-owned sellers or out of distress for 4-5x cash flow. By the time the business is integrated, another turn of cash flow is realized from inherent synergies. In many instances, the families that own these businesses don’t have descendants who want to take them over. About 30% of the acquisitions have been purchased in distressed financial situations. The business acquisitions are financed primarily by debt which is paid down from cash flow generated from the acquired firms. Over the past seven years, management has acquired fourteen firms. The acquired firms have ranged in size from $10 to $100 million in revenues with a median revenue of about $25 million. The size of the firm targeted (median deal size is $15 million) is below the size of most private equity firms’ interest, so the competition is less than it would be for larger deals. TerraVest’s target acquisition markets include not only their core markets, but also firms in adjacent markets such as: green energy containment and transportation (RNG and hydrogen), chemical tanks, septic tanks, air filtration and purification, and other metal fabricating applications. One of the two members of the senior management team focuses on acquisitions.

TerraVest has four levers for cash flow growth:

- buying a firm in their core or adjacent market;

- expanding within existing markets;

- paying down debt; and

- distributing excess cash as dividends or buying back shares.

The acquired firms generate cash flows in excess of what is needed to modestly grow the firm, which is used to purchase firms in its target or adjacent markets. If no firms can be found that meet management’s operational and valuation criteria, then management will buy back shares as the shares have typically traded at modest valuations reflecting organic growth but not the value of future acquisitions. Management is very selective in the firms they acquire. With a full pipeline of deal opportunities, management expects to spend 2/3 rd of its cash flow to either buy firms, pay down debt, or buy back shares. The remaining 1/3 rd will be invested in its current business, including growth opportunities which comprise about 2/3 rd of investments in the current business.

TerraVest’s predecessor was an income trust that went IPO for $24 million in Canada in 2004. TerraVest originally held two businesses—a wellhead processing equipment firm and an agricultural equipment firm. The latter was subsequently sold in 2011 for $15 million. From 2004 to 2005, TerraVest paid $88 million for firms that were subsequently sold in 2011 for $34 million. The poor decisions by previous management led to poor results, and TerraVest’s stock price declined from $15 to around $2 per share by 2011. Following Clarke’s 2010 investment, TerraVest changed management and identified core business areas (initially wellhead processing equipment and services) and divested non-core businesses. The non-core businesses generated $43 million in sale proceeds which were used to pay a special dividend, pay off debt, and repurchase 36% of TerraVest shares outstanding in 2012. In 2013, TerraVest merged with Granby to enter the fuel containment and HVAC equipment business. From 2012 to 2015, TerraVest purchased four more firms in its core markets of fuel containment and HVAC equipment and wellhead processing equipment.

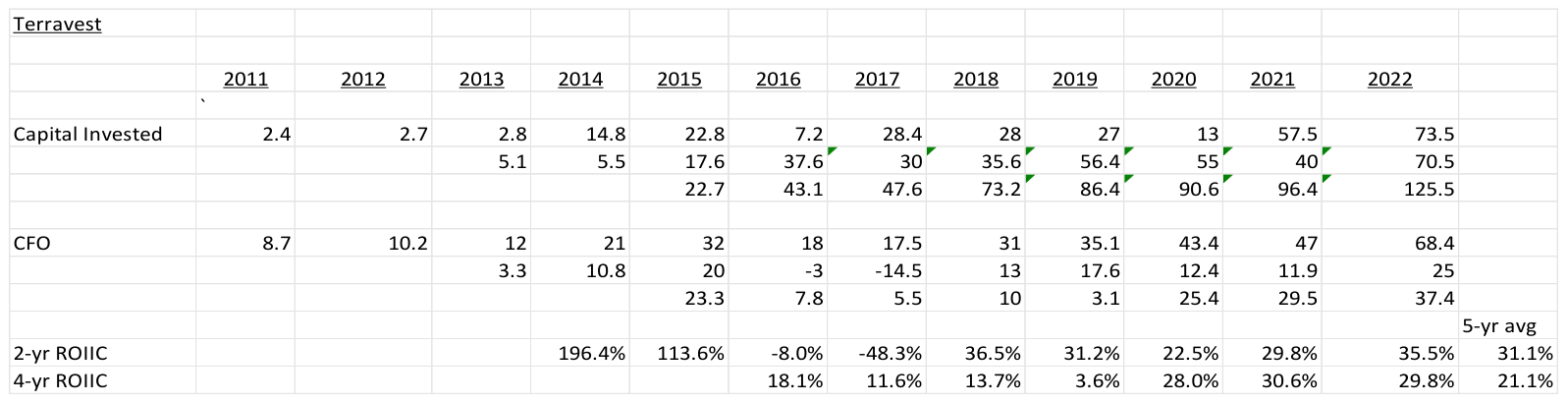

In 2013 and 2014, the current management team of Dustin Haw ((CEO)) and Mitchell Gilbert ((CIO)) joined TerraVest to continue its consolidation strategy of firms in its core markets. From 2016 to 2023, TerraVest purchased nine firms in its core fuel containment and HVAC and wellhead processing equipment markets. From 2013, the portion of TerraVest’s sales associated with cyclical oil and gas services declined from 45% in 2013 to 16% in 2022. These sales were replaced with more recurring sales associated with wellhead and transportation storage products, as well as HVAC equipment and compressed natural gas storage equipment. Most of the competitors in the target markets are smaller, privately held businesses. Mr. Gilbert is focused on acquisitions and has developed a network of private owners of core market firms as potential acquisition candidates. Given how central M&A is to TerraVest’s strategy, the focus of a senior executive is very important. The investment has paid off, as TerraVest has a robust pipeline of deals and can selectively choose the firms it acquires. Subsequent to Mr. Haw and Mr. Gilbert’s arrival, TerraVest has made eleven acquisitions in its core markets and increased CFO before working capital from $18 million to $68 million—a 25% CAGR. The average post-synergy price of these acquisitions has been 3.5x pre-tax free cash flow. The resulting unlevered RoIIC (see calculation below) has been around 30%, which includes returns from both organic growth initiatives and acquisitions.

The business sectors in which TerraVest competes are subject to economies of scale from related products and have route density characteristics due to shipping costs. TerraVest’s recent acquisition of a trucking carrier should reduce the advantages local firms have in the sale of equipment in target markets.

Industry Segments

TerraVest competes in the HVAC equipment and fuel containment markets in Canada and in the Northeast and Great Lakes regions United States. These businesses have been purchased over the years by TerraVest’s management. The company is a market share leading participant in the residential and light commercial oil storage tank and dispenser market in both steel and fiberglass product lines. In addition, TerraVest provides bulk LPG transport trailers, LPG delivery trucks, and furnaces and boilers. Most commercial customers buy these products directly and generate repeat business over time. Residential customers purchase equipment through distributors. This market is a slow-growing GDP growth type of business. This is a fragmented market and competition is primarily from private businesses and divisions of larger companies. In 2023, TerraVest generated 56% of revenues in the fuel containment and HVAC equipment segments.

TerraVest also competes in the natural gas processing and the LPG and ammonia storage and transportation equipment markets. TerraVest provides: wellhead processing equipment and tanks; wellhead sanding units; central facilities processing equipment; NGL, LPG, and ammonia storage tanks; bulk NGL, LPG, CNG, and ammonia transport trailers; and customized processing equipment. Most of these products are made of subcomponents assembled into final products by TerraVest. This segment’s customers include upstream and midstream energy companies, fertilizer and propane distribution companies, and liquids transportation companies. Customers buy these products directly and generate repeat business over time. This is a fragmented market and competition is primarily from private businesses and divisions of larger companies. In 2023, TerraVest generated 28% of revenues in the processing equipment segment.

TerraVest also competes in the oil and gas services market. TerraVest services include fluid hauling, water management, environmental solutions, heating, rentals, and well servicing. TerraVest provides these services via 21 oil and gas servicing rigs located in Saskatchewan. In 2023, TerraVest generated 16% of revenues in the oil and gas services segment.

Sources of growth for TerraVest include organic and acquisition growth in the fuel containment and HVAC equipment and processing equipment segments. Organic growth in these segments is expected to be 2% annual growth rate with any other growth coming from identified growth projects, acquisitions (the largest portion of growth historically), or share repurchases.

TerraVest operations have become better over time, as Dustin and Mitchell implemented a value-added acquisition strategy utilizing economies of scope and production density. The return on assets have increased from 11.7% in FY2013, to 13.4% in FY2023; and the return on equity increased from 14.3% in FY2013, to 27.0% in FY2023. The drivers included increases in net income margins from 6.4% in FY2013, to 7.1% in FY2023, and increases in fixed asset turnover from 3.1x in FY2013, to 3.5x in FY2023. Leverage also increased slightly from 2.2x, to 2.4x EBITDA.

The incremental return on invested capital over the past five years is close to 30%, which has increased TerraVest’s RoIC over the past five years. See the calculations below.

{kind=link}

Downside Protection

TerraVest’s risks include both operational leverage and financial leverage. Operational leverage in the fuel containment and transportation equipment market is based upon the fixed vs. variable costs of the operations. There are some moderate economies of scope in terms of related product development and local economies of scale, as the business is primarily located in New England/Eastern Canada, the Great Lakes, and Western Canada. A recent acquisition in the South should expand TerraVest’s geographic footprint.

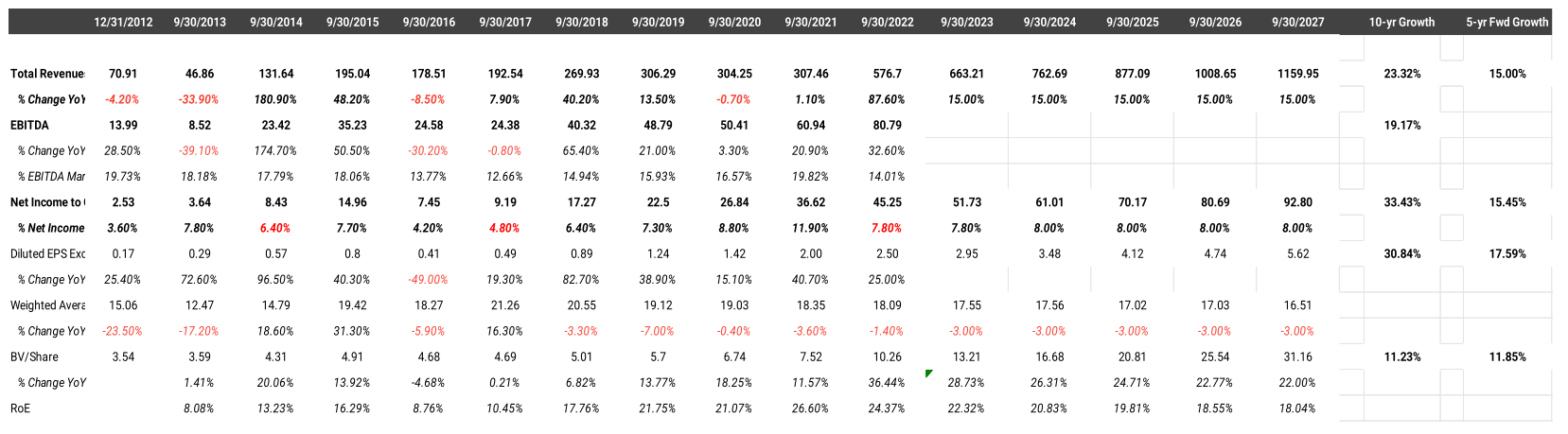

Financial leverage can be measured by the debt/EBITDA ratio. TerraVest has below-average net debt/EBITDA of 2.2 versus other metal fabricating industrials (like Trinity, Worthington, and Chart) and versus TerraVest’s history. The history and projected financial performance for TerraVest is illustrated below.

{kind=link}

Management and Incentives

TerraVest’s management team has developed an M&A engine and operationally efficient firms in profitable niches of the material fabricating industry. They perform M&A when targets are available at the right price partially financed by debt, pay down debt, and return capital via buybacks when there are not opportunities to invest organically or via M&A.

The base compensation for the management team (top five officers) is roughly the same from C$270k to C$320k per year. The CEO and CIO have the highest total compensation, C$2.5 million collectively, primarily due to their option holdings. Over the past three years, their total compensation was about $600k per year, about 1.3% of net income per year. The CEO and CIO currently hold 1.09 million shares and options (worth C$6.8 million), which is more than 7.8 times their 2022 salaries and bonuses of C$867k. The CEO’s compensation is structured to include a C$270k base pay and up to a C$214k performance bonus. All of the senior executives’ base compensation was reduced by 20% for six months in 2020 due to the uncertainty of how the Coronavirus would affect operations. Non-options-based incentive compensation for the executive team is set and approved annually by the board of directors.

Board members have a significant investment in TerraVest. Charles Pellerin, who was the original activist from Clarke, owns 3.5 million shares, and the retired CEO, Dale Laniuk, owns 2.1 million shares. Option grants, provided to the CEO and CIO, were equal to 2% per year of the shares outstanding over the past three years.

Valuation

| Senstitivity Table |

| Price |

| Upside |

| Current Earnings |

| $2.95 |

| 7-year Expected EPS Growth Rate |

| 15.0% |

| 0.5% |

| $28.03 |

| 0.1% |

| Historical EPS Growth Rate |

| 35% |

| 5.0% |

| $54.58 |

| 94.9% |

| Current AAA Bond Rate |

| 4.3% |

| Growth Rate |

| 10.0% |

| $84.08 |

| 200.3% |

| Implied Graham Mutiplier * |

| 38.50 |

| 15.0% |

| $113.58 |

| 305.6% |

| Implied Value |

| $113.58 |

| 20.0% |

| $143.08 |

| 411.0% |

| Current Price |

| $28.00 |

| 25.0% |

| $172.58 |

| 516.3% |

| * (2*Growth Rate + 8.5) |

The key to the valuation of TerraVest is the expected growth rate. The current valuation implies an earnings/FCF increase of 0.5% in perpetuity using the Graham formula ((8.5 + 2g)). The historical 10year earnings growth has been 35% per year including acquisitions and the current return on equity of 24%.

A bottom-up analysis based upon market growth rates of TerraVest’s markets’ (HVAC and fuel equipment, gas processing equipment, and oil and gas services) results was used to estimate an organic growth rate of 2% for TerraVest. This is based upon the revenue growth assumption for the 2022 goodwill impairment and the historical five-year organic revenue growth rate of 3%. This does not include any future acquisitions. If we include 13% growth for acquisitions, then the base EPS growth rate is 15%. Historically, TerraVest’s EPS growth rate was 35% per year driven by 14 acquisitions over seven years. If we assume half of the number of acquisitions over the next seven years and a forward return on equity of high-teens to low-twenties, declining from the current rate of 24%, retaining 85% of earnings, then the incremental 13% growth per year is conservative. Using a 15% expected growth rate, the resulting current multiple is 39x of earnings, while TerraVest trades at an earnings multiple of 10x. If we look at metal bending comparables, which are larger but have slower growth prospects, they have an average earnings multiple of 16x. If we apply 16x earnings to TerraVest’s estimated FY2023 earnings of $3.04, then we arrive at a value of $49 per share, which is a reasonable short-term target. If we use a 15% seven-year growth rate, then we arrive at a value of $113.58 per share. This results in a five-year IRR of 32%.

Growth Framework

{kind=link}

Another way to look at growth and the valuation of companies is to estimate the EPS five years into the future and see how much of today’s price incorporates this growth. Using the same revenue described above results in a 2027 EPS of $6.25, or 4.5x the current price. If we assume a steady-state growth rate from 2026 on of 7%, then this results in a fair value Graham multiple of 22.5x or $140.71 per share, similar to the five-year-forward valuation above of $113.58 per share.

Comparables and Benchmarking

Below are the fuel containment and storage and natural gas processing equipment firms located in the United States and Canada. Most of TerraVest’s competitors are private firms. Compared to these firms, TerraVest has debt on the low end of the range and has better growth prospects and a below-average multiple. TerraVest also has the highest RoEs and the highest five-year growth rates.

| TerraVest Comparable Firm Analysis |

| Price |

| Book Value |

| Earnings |

| FA Turns |

| EBITA Margin |

| 5-Yr EPS Growth |

| RoE |

| P/E |

| P/BV |

| EBITDA |

| Int Coverage |

| Chart Industries |

| 121 27 |

| 64.00 |

| 5.94 |

| 3.81 |

| 12.8% |

| 24.0% |

| 9.3% |

| 20.4 |

| 1 89 |

| 5.00 |

| 3 80 |

| Enerflex |

| 8.1 |

| 12.55 |

| 1.12 |

| 1.59 |

| 10.0% |

| 1.0% |

| 8.9% |

| 7.2 |

| 0.65 |

| 2.32 |

| 3 30 |

| TerraVest Industries |

| 28 |

| 10.26 |

| 2.59 |

| 3.80 |

| 11.7% |

| 35.0% |

| 25.2% |

| 10.8 |

| 2.73 |

| 2.57 |

| 6.67 |

| Trinity |

| 22.78 |

| 12.48 |

| 1.02 |

| 4.60 |

| 9.6% |

| 0.0% |

| 8.2% |

| 22.3 |

| 1 83 |

| 9.10 |

| 2 34 |

| Worthington Industries |

| 59.93 |

| 32.61 |

| 4.18 |

| 7.80 |

| 6.3% |

| 18.0% |

| 12.8% |

| 14.3 |

| 1 84 |

| 1.40 |

| 9.46 |

Risks

The primary risks are:

- slower-than-expected acquisition growth (currently projected to be 50% of the historic acquisition growth rate);

- lower-than-expected growth in TerraVest’s end markets of natural gas and oil processing, storage, and transportation and HVAC equipment replacement (currently projected to grow at 2% per year); and

- a lack of new investment opportunities (mergers and acquisitions) coupled with higher stock prices making buybacks less accretive.

Potential Upside/Catalyst

The primary catalysts are:

- higher-than-expected acquisition growth;

- faster growth in TerraVest’s end markets; and

- increased local scope or purchase of local scale in new markets.

Timeline/Investment Horizon

The short-term target is $49 per share, which is almost 75% above today’s stock price. If the continued acquisition/consolidation thesis plays out over the next five years (with a resulting 15% earnings per year growth rate), then a value of $125 (midpoint of the two methods described above) could be realized. This is a 35% IRR over the next five years.

Disclaimer

This letter does not contain all the information that is material to a prospective investor in the Bonhoeffer Fund, L.P. (the “Fund”). Not an Offer: The information set forth in this letter is being made available to generally describe the philosophies of the Fund. The letter does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services. Such an offer may only be made to accredited investors by means of delivery of a confidential private placement memorandum, or other similar materials that contain a description of material terms relating to such investment. The information published and the opinions expressed herein are provided for informational purposes only. No Advice: Nothing contained herein constitutes financial, legal, tax, or other advice. The Fund makes no representation that the information and opinions expressed herein are accurate, complete or current. The information contained herein is current as of the date hereof but may become outdated or change. Risks: An investment in the Fund is speculative due to a variety of risks and considerations as detailed in the Confidential Private Placement Memorandum of the Fund, and this letter is qualified in its entirety by the more complete information contained therein and in the related subscription materials. No Recommendation: The mention of or reference to specific companies, strategies or instruments in this letter should not be interpreted as a recommendation or opinion that you should make any purchase or sale or participate in any transaction.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Bonhoeffer Capital - Terravest Industries: An Attractive, High Growth Play