EXPE - Booking Holdings Q2 Earnings: Still The Undisputed Leader

2023-08-07 11:39:14 ET

Summary

- Booking Holdings Inc. reported impressive Q2 results, beating revenue and EPS estimates as demand for its services remains high.

- The company's ability to capitalize on robust leisure travel demand led to stronger-than-anticipated growth across all regions, which then also drove meaningfully higher margins.

- Airbnb does not pose a significant threat to Booking's business model, as Booking has been gaining market share over the last 1.5 years.

- The company remains excellently positioned to report strong growth through 2026, which should be supported by its long-term initiatives like its connected trip vision and the integration of AI.

- I remain bullish on Booking Holdings, as its improved outlook and significant earnings beat are able to offset the 20% share price increase since my previous article. The risk-reward profile remains attractive.

Investment thesis

I maintain my buy rating on Booking Holdings Inc. ( BKNG ) and update my revenue and EPS estimates following the company’s Q2 results . Booking reported very impressive growth rates, which caused both revenue and EPS to come in far ahead of the Wall Street consensus.

Booking Holdings, a dominant player in the travel accommodation industry, continues to demonstrate its strength in the market through its impressive Q2 financial results . The company's ability to capitalize on robust leisure travel demand led to stronger-than-anticipated growth across all regions. With a total of 268 million room nights booked, Booking showcased its global strength, particularly in emerging regions like Asia. Additionally, the company's direct channel engagements through its apps continue to grow as a share of total bookings, enhancing customer engagement and loyalty.

Crucially and contrary to speculation, Airbnb ( ABNB ) does not seem to be a significant threat to Booking's business model. Booking has been gaining market share over the last 1.5 years, with a staggering 133% lead over Airbnb in reported room nights booked as of Q2.

Looking ahead, Booking remains focused on its long-term initiatives, such as its connected trip vision, integration of AI capabilities, and expansion of alternative accommodation options. By creating a one-stop platform for all aspects of travel, the company aims to increase customer engagement and drive revenue growth. The ongoing investment in AI further enhances personalization and customer experience, setting Booking apart from its competitors.

In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

Booking’s Q2 results are a testimony to its strength in the travel industry

Booking reported its Q2 financial results on August 3 and blew away the Wall Street consensus as it continued to see robust leisure travel demand, which allowed it to report stronger-than-anticipated growth across the board. Booking remains the undisputed industry leader in the travel accommodation industry and seems to be well able to fight off the competition as its market share remains relatively stable, even increasing slightly. Meanwhile, the company remains committed to its long-term initiatives, which should allow it to become even more of a travel behemoth as it keeps expanding its offering into other verticals of the travel industry. Q2 was a testimony to the company’s global strength as it silences the bears.

Booking reported a total number of room nights booked of a whopping 268 million, up 9% YoY and a few percentage points higher than anticipated. This growth was primarily driven by emerging countries as Asia grew 40% YoY due to the reopening of China and increased travel movements in the Asia Pacific region. This growth for Asia is expected to remain strong in Q3 as well. Growth in the rest of the world (everything outside of Asia, Europe, and North America) was also resilient in the low double digits. Meanwhile, Europe was up only a few percentage points and the US was down slightly due to these lapping the incredible recovery quarter of last year. Both are expected to show stronger positive growth in Q3 again due to an expected record summer.

Also worth mentioning regarding the room nights booked is that 48% of these bookings were done through Booking’s apps, which is up 6 percentage points YoY, a significant increase and an acceleration from Q1. This is important, as these direct channel engagements allow Booking to create higher customer engagement and loyalty, which should bode well for future growth. As this percentage grows, this is a positive sign for Booking’s attractiveness to customers and their future growth predictability.

To illustrate the sheer size and competitive position of Booking, this sat 133% above the number reported by Airbnb, Booking’s closest competitor. This also indicates that Booking has been gaining market share over the last 1.5 years against at least Airbnb as this difference back at the end of FY21 stood at 105%, meaning Booking has been able to grow at a meaningfully faster rate over this period. Now, I do not want to make this article a comparison between the two, but it is essential to highlight through these recently reported quarterly financials from both companies that the speculation of Airbnb being the disruptor completely destroying the Booking business model is not holding up today. Yes, Airbnb is a fantastic company with a differentiated approach in the travel industry, but there clearly is room for both of them and Booking has shown over the last 1.5 years that it does not even have to be the one that loses market share, despite its already massive size and industry position. So, at the start of this article, I just wanted to have that argument out of the window. In short, Airbnb is not a threat to Booking.

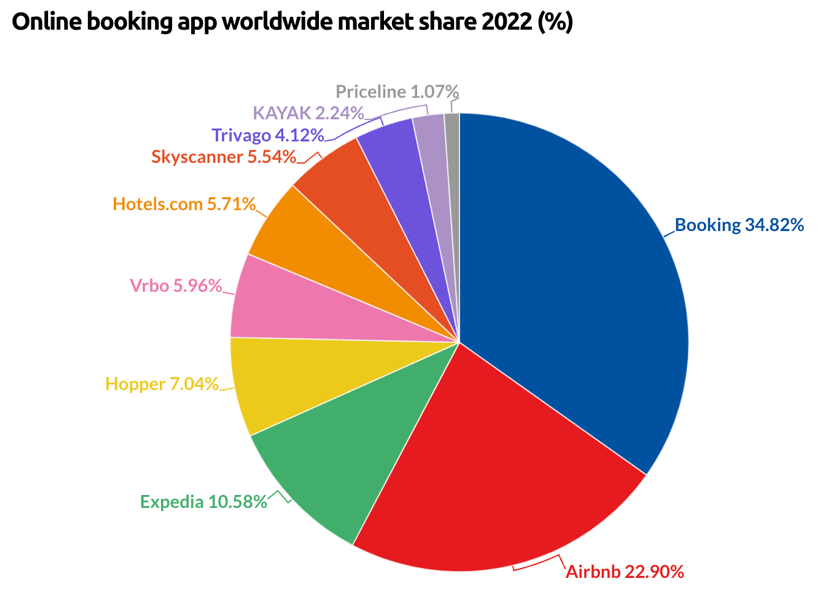

Taking a further look into the market share of Booking and its competitors, data shows that as of 2022, the company holds a market share of 35% (closer to 40% when including all traveling platforms that fall under the booking banner), up slightly from 2021. Meanwhile, Airbnb has seen its market share fall by about one percentage point and Expedia has expanded its share by about 2.5 percentage points.

{kind=link}

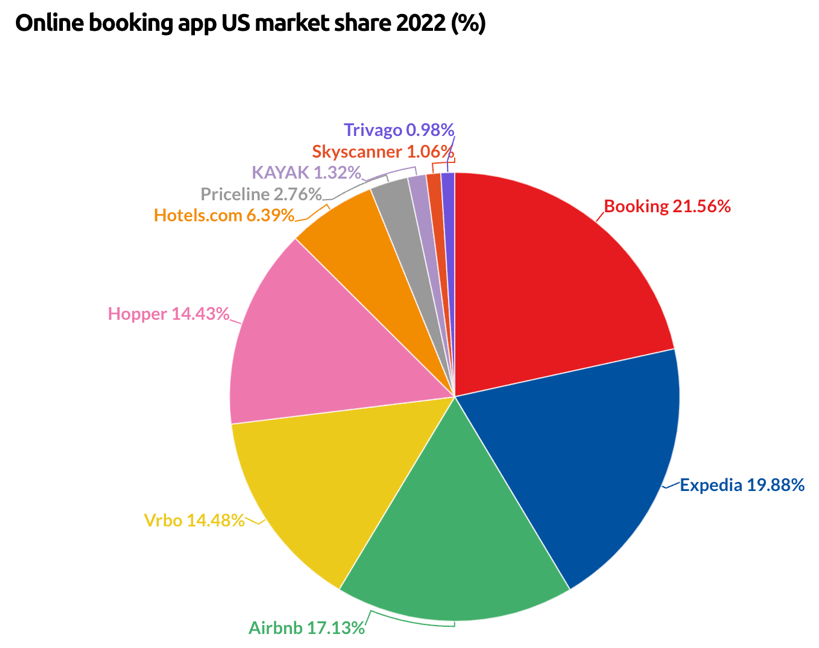

Booking has also been able to keep its U.S. market share relatively stable and to appear as the largest travel platform in the country once more. In 2021, Airbnb had taken this lead but has since lost four percentage points in market share, primarily to Expedia ( EXPE ), which has now taken the number 2 spot in the country. Still, overall, Booking remains the undisputed worldwide travel accommodation leader.

{kind=link}

Moving back to the quarterly results, as a result of the solid 9% increase in nights booked and the higher prices for consumers due to high inflation, gross bookings grew by a more pronounced 15% YoY to reach another all-time high of $39.7 billion. Q2 bookings take rate was up 130 basis points YoY and sits in line with 2019 levels, indicating that Booking can maintain its platform strength and importance for suppliers.

Booking reported Q2 revenue of $5.5 billion, beating the consensus by $330 million. The company continued to report very impressive growth of 27% YoY, which is a significant slowdown from the 40% growth reported in Q1, but still, a very impressive performance as this is on top of the 99% reported revenue growth in the one year ago quarter. The company is now lapping very strong COVID recovery quarters from last year, in which travel restrictions were already fully lifted, making this a really incredible performance, especially when compared to the 18% revenue growth reported by its most significant rival, Airbnb .

The significant top-line growth outperformance compared to previous estimates, in combination with the improved marketing efficiency, as marketing expenses, a crucial one for Booking but also a highly variable one, was up only 4% YoY, also allowed Booking to report strong bottom-line results. The adjusted EBITDA was up by 64%, far ahead of the 35% growth expectation, as this totaled $1.8 billion or 33% of revenue, up seven percentage points from the year-ago quarter.

EPS in Q2 was $37.62, beating the consensus by $8.46 or a stellar 29%. This once more highlights the incredible performance of the company in the second quarter as it massively outperformed the consensus.

Q2 free cash flow was $1.6 billion or 29% of revenue. This, in combination with $1.9 billion of debt issuances, caused an increase in total cash on the balance sheet to $15.7 billion, up from $15.3 billion at the end of Q1. Yet, long-term debt was also up to $13.2 billion from $12 billion at the start of 2022. Still, the company maintains a solid net cash position and remains well-capitalized for further investments.

Also, the company continues to reward its shareholders as it bought back another $3.1 billion in shares in Q2, bringing the FY23 total to $5.1 billion or a decrease of 5% of outstanding shares. Management still has $19 billion in combined authorization left and expects this to be spent within four years, meaning the company aims to further reduce the number of outstanding shares by 17% through the start of 2027. So, while the company might not yet be offering a dividend, these share buybacks definitely are a nice extra for Booking investors.

Booking remains focused on executing its long-term initiatives

The company remains focused on its long-term initiatives like its connected trip vision, the integration of AI capabilities, and growing alternative accommodations options. The company continues to invest in these initiatives while remaining cost-conscious and so far has found a good balance between the two.

Going through all of these crucial initiatives once more to get a better understanding of the company’s growth drivers and developments, this is how I explained the connected trip vision of management in my previous article :

What this means is that Booking Holdings aims to improve the entire booking experience by making it easier, more enjoyable, more personal, and delivering better value. Booking aims to do this by focusing on bringing together and connecting all aspects of your desired traveling experience by expanding its offering of other travel verticals other than accommodations. Therefore, the company has been heavily focused on integrating flight opportunities and it released Priceline Experiences to enable customers to quickly search and book more than 80,000 activities in over 100 countries.

Ideally, Booking Holdings Inc. wants to offer a platform to its customers that allows them to arrange every aspect of their trip on a single platform to increase customer engagement and loyalty to the platform over time.

Today, Booking is the only one with a platform and brand strong enough to realize a one-stop shop for all that is traveling. If the company could get all its customers to book more aspects of their travel through the Booking platform, like flights, rentals, and experiences, this would massively grow the company’s gross booking potential. We are already seeing this today with new aspects like flights growing rapidly. In Q2, airline tickets booked were up 58% YoY, driven by the continued expansion of Booking.com’s Flights offering.

Through this vision, the company is simply expanding its total addressable market, or TAM, and already has the customer base to leverage. Furthermore, it is not just benefitting Booking but also creates a more useful platform for supplier partners to offer every single travel product on this platform, increasing their revenue potential. This could then drive more travel suppliers (as we will call them for now) to the Booking platform, further cementing Booking's industry leadership.

Though the realization of this vision will not happen overnight, but Booking will consistently expand its product offering and increase customization options and the overall customer experience through technology. AI stands at the forefront of this and is seen as the center of its vision by management. Eventually, Booking wants to leverage the capabilities of AI to allow for a more personalized booking experience. As the customer experience is crucial to maintaining and growing customers on the platforms, Booking is heavily investing in AI. It is already testing its first generative AI booking assistant on its Priceline platform, highlighting the progress the company is making here, which should allow it to move further ahead of the competition.

Moving to the final long-term growth initiative, the number of alternative accommodation nights booked outgrew the overall number, although only marginally, reporting 11% growth YoY and representing 34% of all nights booked. This percentage is up 2 points from the 32% reported in the same quarter last year, which should be seen as a positive development and improved revenue mix. I am saying this because the alternative accommodation market is expected to grow at a much faster rate ( 16.5% CAGR through 2030 ) over the next decade compared to the overall travel accommodations industry ( 11.3% CAGR through 2031 ). As Booking's exposure to this faster-growing vertical increases, this should benefit Booking's reported overall growth.

Outlook & BKNG stock valuation

During the earnings call , management already hinted at another strong Q3 as it revealed that growth in bookings accelerated in July to 20%, much faster than the 9% growth reported for Q2. Also, this was once more driven by all regions as Asia was up 45% in July, the rest of the world 20%, and the U.S. and Europe up mid-single digits and mid-teens, respectively.

As a result, management expects room nights to be up low double digits YoY, assuming growth to moderate from July onward. Therefore, I project room nights up around 11% YoY to 266 million. I am not expecting many last-minute bookings and a slightly higher cancellation rate, to stay conservative. Still, this would mean a very strong holiday quarter. Also, this should lead to around 18% growth in gross bookings to approximately $37.88 billion, as management expects this to sit seven percentage points above room night growth.

Management projects revenue to sit at 19% of gross bookings, slightly up YoY. Using my estimates, this would result in Q3 revenue of $7.2 billion, up 18% YoY, slowing down further from 27% reported growth in Q2 and 40% in Q1. Still, reporting 18% growth on top of 27% growth in the same quarter last year is nothing to complain about. Furthermore, as marketing expenses as a percentage of revenue are expected to decrease further, the adjusted EBITDA is expected to grow 20% YoY as the EBITDA margin further strengthens. This should result in an adjusted EBITDA of $3.2 billion or 44.3% of revenue. I believe this should result in a non-GAAP net income of $2.5 billion, 34.7% of revenue, or an EPS of $68.45.

Following the very impressive growth in H1 and as this is expected to remain for Q3, management has updated its FY23 expectations as well and now expects to report gross booking growth of slightly over 20%, up from low teens growth. This would put room night growth in the mid-teens, according to Booking. Furthermore, revenue as a percentage of gross bookings is expected to be up 20 basis points, down from the previous 50 for several reasons.

As for my FY23 guidance, I believe this should result in FY23 room nights booked of 1011, up 13% YoY, and gross bookings of $146 billion, up 20.5% YoY. Going with a take rate of 14.3%, this would result in FY23 revenue of $20.88 billion, up 22% YoY. Furthermore, a FY23 net income margin of 24% should be achievable, resulting in a net income of $5 billion or EPS of $143. All these financial estimates sit significantly above my prior estimates.

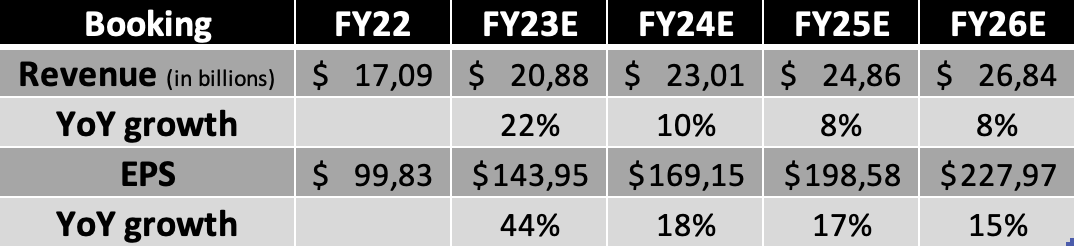

Following the Q2 financial result, guidance for Q3, upward revised guidance for FY23, and the underlying industry developments and business developments, I now project the following financial results through FY26. I have upgraded both my long-term revenue and EPS estimates as underlying industry growth will remain strong and Booking has the capabilities to largely maintain its market share while expanding its TAM by increasing its exposure to other travel verticals. Also, continued share repurchases and margin improvements through the increased integration of AI and other automation technologies should boost growth in EPS further.

Financial estimates (By Author)

{kind=link}

Moving to the valuation, shares are currently valued at slightly over 21x my FY23 EPS estimate, which is roughly in line with its 5-year average and only slightly higher than the 20x when I last covered the stock as the improved outlook has largely offset the 20% share price increase since.

Really, there is only one peer to which we can compare Booking, and this is Airbnb, which is valued much higher on every single metric. Granted, Airbnb has a better revenue growth outlook, but the EPS growth expectations are very comparable. Looking at the forward P/E for this year and three years forward, Airbnb’s valuation premium over Booking increases from 57% to 87%, indicating that based on the EPS growth outlook, either Airbnb is incredibly overvalued or Booking is undervalued. Honestly, I believe it is a bit of both.

Taking into account the cyclical risk of the travel industry and Booking’s incredible market share and growth potential, I believe it deserves to be valued at a forward P/E of at least 22x. Based on this belief and my FY24 EPS estimate, I calculate a target price of $3720, leaving an upside of around 21.5% based on a share price of $3063.

Conclusion

Booking reported another impressive quarter that blew away the consensus and outperformed all its peers. The company continues to see strong demand for travel accommodation, which allows it to report impressive growth rates despite lapping the strong recovery quarters from last year. Furthermore, recent industry data shows that Booking is able to hold onto its market share despite the increased competition from especially Airbnb. This is a massive positive, and it should remove one of the most prominent arguments against Booking. There clearly is enough room for both of these industry giants to grow.

I remain very bullish on Booking and believe the company remains incredibly well-positioned for impressive long-term growth. Its connected trip vision, the integration of AI, and focus on alternative travel options are efforts I can get behind and which can be significant growth and margin drivers for the company as well as factors that can strengthen its competitive position.

As the growth outlook improves and the company remains committed to returning cash to shareholders, the company remains an attractive investment despite a 20% share price increase since my previous article in March and 50% YTD. Using my target price of $3720 and going with an annual return of 10%, a fair share price sits around $3200.

With a 21.5% upside to my target price and the current share price sitting below fair value, I maintain my buy rating on Booking Holdings Inc. as I believe the current risk-reward profile remains favorable.

For further details see:

Booking Holdings Q2 Earnings: Still The Undisputed Leader