SAM - Boston Beer: A Great Company With Excellent Leadership But Too Expensive

Summary

- SAM is led by an impressive leadership team, and together, the leadership team owns a significant portion of the company's stock.

- Some of SAM's recent struggles can be attributed to the recent declines in the Hard Seltzer category.

- SAM does not appear to be undervalued at its current share price based on a DCF and comparative analysis.

Background

Boston Beer Co. ( SAM ) is a publicly traded craft brewery in Boston, Massachusetts. The company was founded in 1984 by Jim Koch, who developed the recipe for the company's flagship Sam Adams brand while working as a management consultant. In the company's early years, Boston Beer Co focused on producing high-quality craft beer using traditional brewing techniques and ingredients. The Sam Adams brand quickly gained popularity, and the company began expanding its distribution across the United States.

SAM's business model focuses on producing, marketing, and distributing various craft beer brands, including its flagship Sam Adams brand. The company has a wide range of beer styles, including lagers, ales, stouts, and pilsners, and distributes its products through a network of distributors and retailers.

In addition to its core beer business, Boston Beer Co also produces and sells hard cider, malt beverages, and hard seltzer under the Angry Orchard, Twisted Tea, and Truly Hard Seltzer brands, respectively. The company also operates a network of a company-owned and franchised brewery and tasting rooms, known as the Samuel Adams Brewery Experience, which provide a unique and immersive experience for beer enthusiasts. The company generates revenue from the sale of its products to distributors, retailers, and consumers, as well as from the sale of merchandise and other related products and services.

SAM strongly focuses on innovation and regularly releases new and unique beer styles, experimenting with different ingredients and brewing techniques. The company also strongly emphasizes sustainability and has implemented several initiatives to reduce its environmental impact, including using renewable energy sources and recycling spent grains.

Track Record

SAM is led by an impressive leadership team. Jim Koch is the founder and chairman of the company. The Harvard graduate founded the company in 1984 after he quit his consulting job and began brewing beer in his kitchen. His first batch was Boston Lager, and he began selling the beer door-to-door at Boston bars and restaurants. Koch has been known as the founding father of the American craft brewery movement and has played a vital role in SAM's growth and success over the years, taking the company public in 1995.

Today, SAM's current President and CEO is David A. Burwick, who has held the position since April 2018 . Before holding these roles, Burwick was President and CEO of Peet's Coffee & Tea, a company that sells specialty coffee and tea. Burwick has held those roles since 2012 and led the company through significant growth and expansion. Burwick has a strong track record of driving growth and innovation in the consumer-packaged goods industry and is well respected for his leadership and strategic vision.

The year before Burwick took over as President and CEO of SAM, the company reported $862 million in sales following two straight years of revenue declines. Since then, revenue has snowballed to $2.4 billion over the last 12 months. Overall, SAM's revenue growth was impressive over the last decade, growing by 313%.

Data by Stock Analysis

Even more impressive is how operating income has more than quadrupled since Burwick took over after three years of declines. Over the trailing 12 months, SAM recorded $491.95 million in operating income, up 416% for the decade.

Data by Stock Analysis

Unfortunately, SAM's free cash flows have not followed suit, up just 29% since Burwick took over as CEO in 2018 but over the longer-term free cash flows are up 358% for the decade. Investors should be pleased if the current management team can duplicate these results over the next ten years.

Data by Stock Analysis

To see the substantial revenue and operating income growth since Burwick took over as CEO is encouraging. However, there are other critical areas for investors to be excited about. For example, over the past 12 months, gross margins have been the highest since 2018, and operating margins are the highest in a decade.

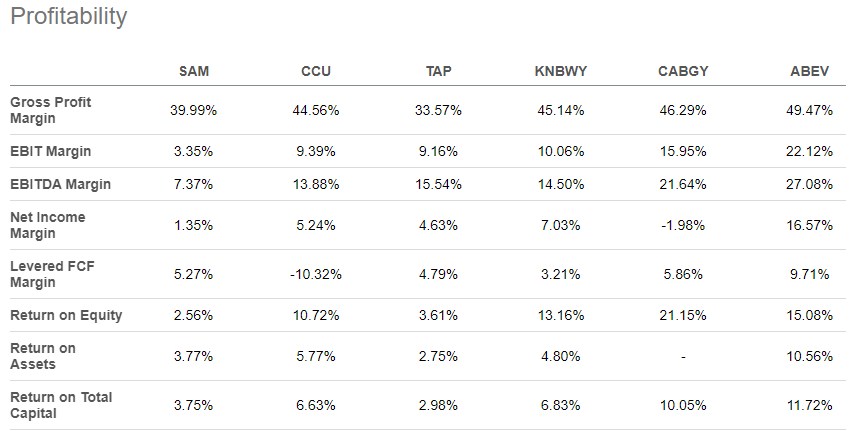

However, some other areas need some work. For example, return on equity and invested capital are at the lowest levels seen over the past 10 years. As a result, SAM is basically in last place in these vital profitability metrics compared to industry rivals.

{kind=link}

Overall, SAM has a strong management team, and together insiders own 22.28% of the company. Therefore, investors should be encouraged to see that SAM's leadership team has a significant stake in the company's success.

Growth Moving Forward

Some of the recent struggles can be attributed to the recent declines in the Hard Seltzer category, which SAM is particularly exposed to because of its Truly brand, the number two hard seltzer brand in the industry. In the most recent earnings report , SAM reported a 15% decline in the Hard Seltzer category on a volume basis through the first nine months of 2022, and Truly was down 21% over the period.

Some of the reasons for these declines are the novelty of the Hard Seltzer category has diminished. This is also a crowded segment. There are too many Hard Seltzer SKUs which has caused confusion for the customer and made the segment hard to shop. Also, with the difficult macroeconomic environment, consumers are shifting away from Hard Seltzers to less expensive premium light beers.

These recent Truly woes are not going unnoticed, and management has plans to reignite the brand through a major product reformulation that will add real fruit juice for a smoother, easy-to-drink refreshing taste. A new ad campaign and increased media investment will also support this reformulation.

SAM has also launched several new products in this space, with Truly Margarita being the top innovation this year with a 4.1% volume share. Though management expects the Hard Seltzer segment to further decline by 15-20%, they are bullish on the long-term potential of the Truly brand and expect it to outperform the category in the long term.

Another area of growth within the industry is the emerging ready-to-drink spirits category. Through the first nine months of 2022, this category grew 79% in measured off-premise channels. SAM is in an excellent position to succeed in this category with its award-winning Dogfish Head canned cocktails. In addition, SAM recently launched a Truly Vodka Seltzer, which has received positive feedback from wholesalers, retailers, and consumers thus far.

Finally, SAM is investing heavily in its supply chain. The company has significantly invested in equipment, capacity, and improved systems and processes. I think these efforts will help improve supply chain performance and inventory management and expand SAM's gross margins and service levels.

Valuation

When I estimate a company's intrinsic value, I like to use a couple of different valuation techniques to ensure I get as close an estimate to the company's intrinsic value as possible. First, I like to use a comparative approach, where I look to see what analysts are expecting the company's next year earnings to be and then apply those earnings estimates to different multiples that the market has paid for the company in recent years to get a bull, bear, and base case scenario for the stock.

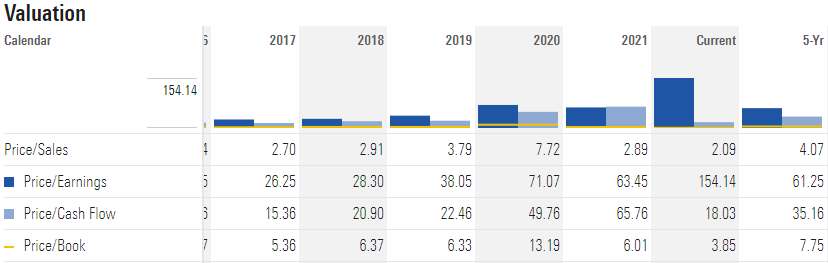

Unfortunately, this approach only works well when the company's earnings are stable. When the companies' earnings fluctuate widely, so do the multiples that the market has paid for the company, which distort the different valuation scenarios. For example, when a company's earnings fall close to zero, but the share price does not follow proportionately, this results in a sky-high P/E ratio, but this doesn't mean that the market is exceptionally bullish on the company.

SAM is one such company that has not enjoyed stable earnings of late. For example, in 2020, the company reported $15.53 in EPS, and other the last 12 months, the company reported just $2.20. Therefore, the company currently has a P/E ratio of 154.14, which is unusually high for SAM.

Therefore, I will use 2017, 2018, and 2019 multiples paid for SAM to get a bear, bull, and base case scenario, as these are more normal P/E ratios for SAM as of late. I will also look at the SAM's sector median multiple as a bonus scenario.

{kind=link}

The table below shows a breakdown of these scenarios.

| Scenario |

| P/E |

| Next Year's Earnings Estimate |

| Intrinsic Value Estimate |

| % Change |

| Bear Case |

| 26.25 - SAM's 2017 P/E ratio |

| $11.91 |

| $312.63 |

| -6.22% |

| Base Case |

| 28.30 - SAM's 2018 P/E ratio |

| $11.91 |

| $337.05 |

| 1.09% |

| Bull Case |

| 38.05 - SAM's 2019 P/E ratio |

| $11.91 |

| $453.17 |

| 35.92% |

| Sector Median Valuation |

| 20.73 |

| $11.91 |

| $246.89 |

| -25.94% |

It's important to understand that these are just estimates of SAM's intrinsic value, and these estimates are not exact. This exercise is meant to give us an idea of if SAM is undervalued at its current price. Based on the results, SAM does not strike me as obviously undervalued. Even in the bull case, we can only estimate a 35% upside to SAM's current share price. This is not a wide enough margin of safety in my opinion.

We'll run a discounted cash flow analysis for the second valuation technique. First, we'll take the average of SAM's last five years of free cash flows, which is $70 million. Next, we'll use a 7% growth rate over the next 10 years. We cannot reliably predict the free cash flow growth ten years into the future but based on the rule of 72, we'll find that a 7% growth rate will double SAM's free cashflow in ten years, which I think SAM can do based on its strong leadership team and strong brands. Then to figure out the terminal value, we will use a growth rate of 2.5% into perpetuity. Finally, we will use a discount rate of 10%. I use this discount rate because it's my personal required rate of return.

With these inputs, we land at an intrinsic value of $115.38 per share for SAM. Once again, SAM does not appear to be undervalued at its current share price based on the DCF and comparative analysis.

{kind=link}

Summary

There's a lot to like about SAM. The company is led by a talented and experienced leadership team, and SAM has strong brands that put the company in a position to succeed as new industry trends emerge. Unfortunately, the company does not appear to be undervalued by a wide enough margin of safety. Keep SAM on your radar, but this is not the best time to invest. If you disagree, please let me know in the comments section below.

Thank you for reading!

For further details see:

Boston Beer: A Great Company With Excellent Leadership, But Too Expensive