CA - Bristol-Myers Squibb Is A Great Buy But These 5+% Yielding Bargains Are Better

2023-11-28 07:10:00 ET

Summary

- Bristol-Myers Squibb Company is down 40%, while the market is up 20%. The reason is the collapse in its growth outlook created by patent cliffs.

- Despite some amazing growth in new drugs, Bristol's three super mega-blockbuster patent cliffs are creating zero-growth headwinds for the foreseeable future.

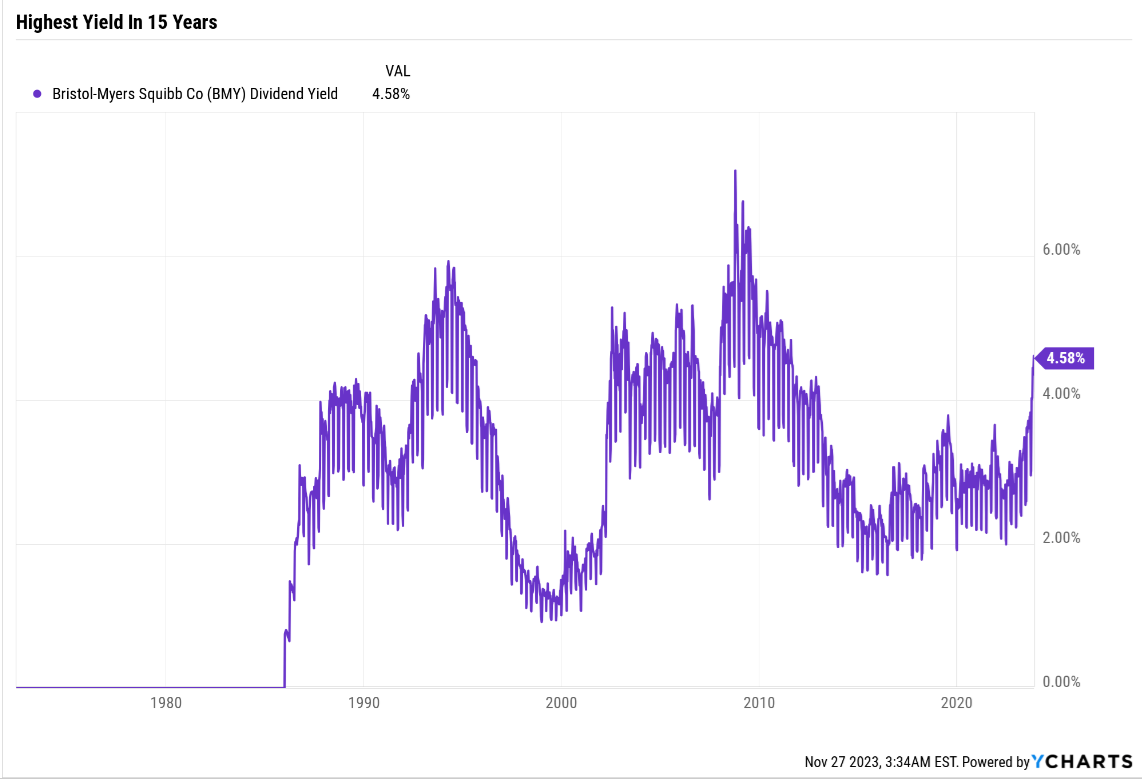

- Even without growth, Bristol-Myers is 28% undervalued, yielding the most in 15 years, and offers 50% upside return potential over the next 2 years.

- This video screening article shows how to quickly and easily screen for 5+% yielding growth superstars almost as undervalued as Bristol-Myers but offering Warren Buffett-like 20% return potential over the next decade.

- It's always and forever a market of stocks, not a stock market. For every goal, time horizon, and risk profile, there are amazing blue-chip opportunities available if you know where to look.

Investors naturally become nervous whenever a stock is hitting new 52-week lows in a strong market.

{kind=link}

In the Pharma industry sometimes exceptional booms and busts happen, including Pfizer's (PFE) COVID vaccine sales boom, resulting in a 40% bear market when the bonanza ended.

But I've been asked by several of our Investing Group members in our chat room why Bristol-Myers Squibb Company ( BMY ) is down 40% in a year when the market is up almost 20% and the Nasdaq is up almost 40%.

Is this a warning sign that Bristol is doomed to become one of the 44% of U.S. stocks that collapses and never recovers?

{kind=link}

Or is this a Buffett-style "greedy when others are fearful" opportunity to lock in the best yield in 15 years?

{kind=link}

Let me quickly show you the good and bad news about Bristol, which likely explains much of its recent weakness.

I'll show you why Bristol isn't broken, but why you might want to consider buying superior high-yield blue-chip bargains today.

It's always and forever a market of stocks, not a stock market. So, let's get that fact work done for you, so that one day you don't have to.

Why Bristol-Myers Is Beaten Down

The drug industry is known for two things primarily: incredible profit margins thanks to patents, and also patent cliffs that can cause long bear markets.

{kind=link}

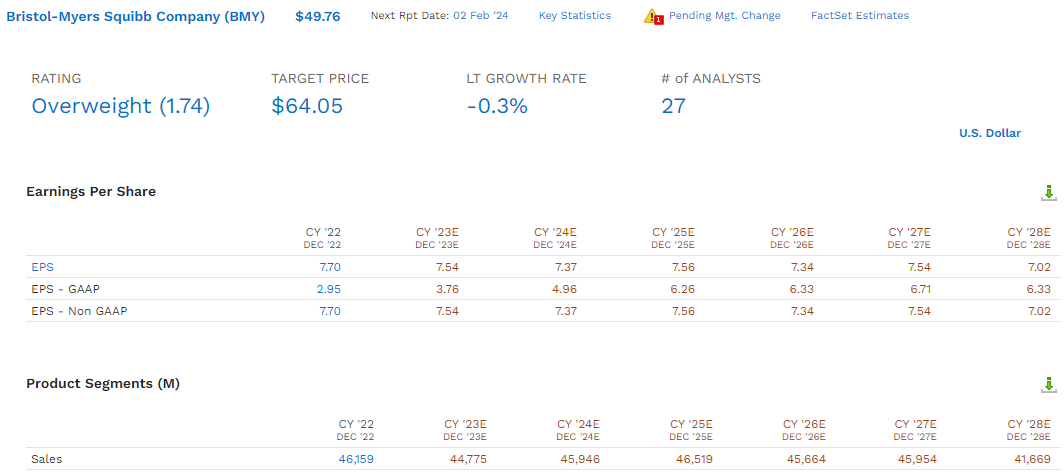

Looking at BMY's consensus outlook, we can see that growth potential has fallen off a cliff in recent years.

{kind=link}

What happened to Bristol? For big pharma, the issue is often acquisitions and drug pipelines.

Bristol-Myers bought Celgene in 2019 for $74 billion in a large debt-funded deal, but that was actually a very good deal for BMY. They bought Celgene when it was the 5th most undervalued large drug maker, and it helped to significantly boost their EPS growth in the coming years.

- 2019 growth: +18%

- 2020: +37%

- 2021: +17%.

{kind=link}

As you can see, the problem for Bristol is that one of its hottest blockbusters, the cancer drug Revlimid, which it acquired when it bought Celgene, is facing a massive patent cliff.

The primary Revlimid patent expired in 2019 and the last in 2026, and that's why analysts expect Revlimid sales to drop from $13 billion in 2021 (peak year) to just $223 million in 2028.

{kind=link}

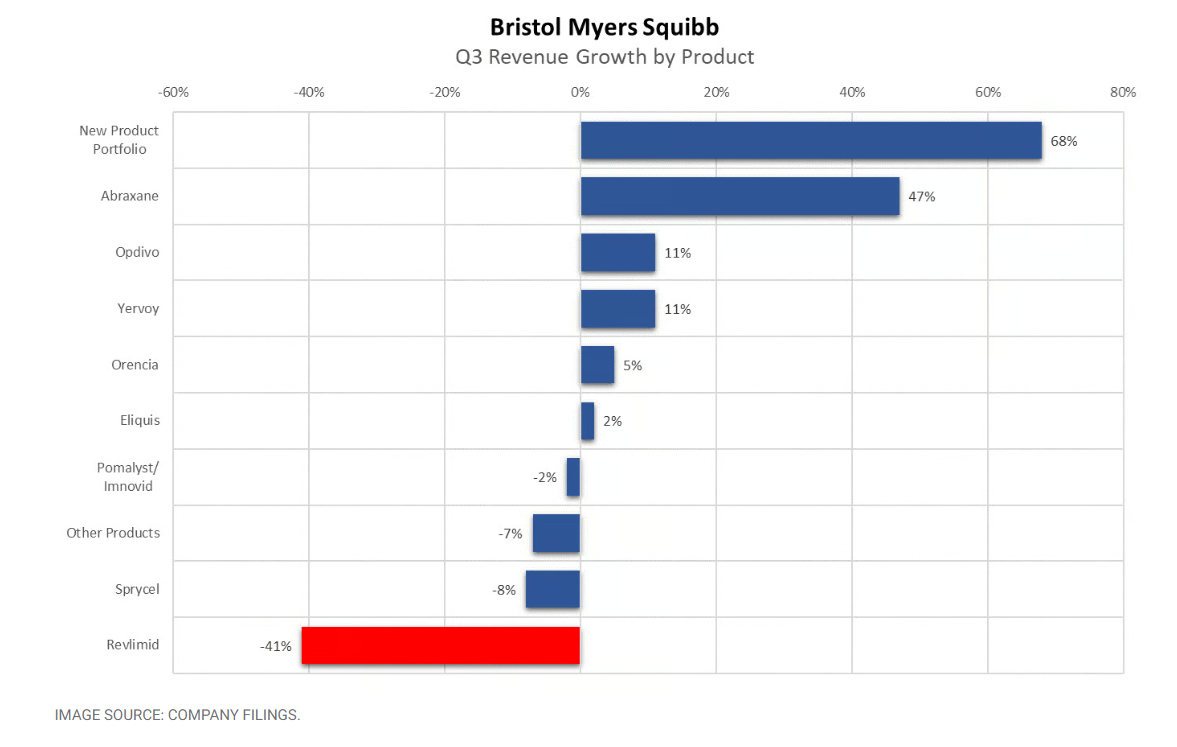

The good news for Bristol is that while Revlimid sales tanked 41% YOY in Q3, it has strong blockbusters like anti-clotting drug Eliquis (#1 seller at $2.7 billion this quarter) and cancer drug Opdivo, which is still growing at double-digits.

Opdivo sales are $2.3 billion per quarter, and its patents expire in 2028.

However, the problem for Bristol is that Opdivo's sales of $9.1 billion in 2023 are expected to be close to peak sales of $12.6 billion in 2027 and 2028, and then the patent cliff is expected to hit.

And Eliquis won a major court battle in which the court blocked any generic competition until 2028.

Immunology drug Sotyktu and rare cardiometabolic drug Camzyos are growing, but the launch trajectories are below our expectations. We believe management's increased spending guidance through 2025 partly reflects a need to increase marketing support behind these new drugs. On the positive side, blood treatment Reblozyl continues to post steady gains, and the recent label expansion into earlier lines of therapy should bode well for the drug longer term. Total sales fell 3% operationally in the third quarter, and we expect fairly flat growth over the next five years. " Morningstar (emphasis added).

As we've seen, analysts tend to agree with Morningstar.

That's not to say that BMY doesn't have a lot of great drugs in its portfolio pipeline.

Cancer drug Opdualag just doubled sales and is expected to hit $2.5 billion in sales by 2028.

- up from $252 million in 2022 = 58% annual growth.

Zeposia, which treats relapsing multiple sclerosis, grew sales by 78% in Q3 and is expected to hit sales of $1.5 billion in 2028.

- up from $250 million last year or 43% annual growth.

For Bristol, the law of large numbers is hitting it hard, because in 2021, the year of peak sales of $46.4 billion, it had a golden trio of blockbusters.

- Revlimid $13 billion

- Eliquis $11 billion

- Opdivo $8 billion

- Total: $32 billion = 70% of company sales.

Bristol did a great job buying Celgene on the cheap, growing earnings by almost 70% as a result. But its current drug pipeline just can't overcome the medium-term patent cliffs that are causing growth to stall.

Why Bristol Is a Potentially Very Strong Buy In The Short Term

Investors are worried about Bristol, but historically it always manages to find ways to grow.

Bristol Historical Growth Rates

FactSet Research FactSet Research FactSet Research

Bristol has never been through a period, at least not in the last 20 years, where it failed to grow for 5 years.

But that doesn't mean that Bristol is necessarily a bad business.

Bristol Is A Wonderful Business Even Without Growth

{kind=link}

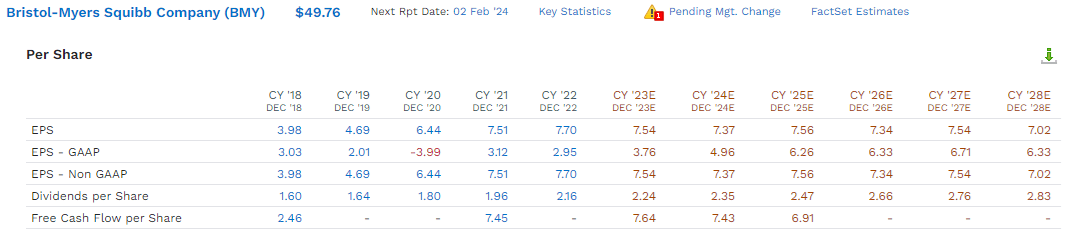

In 2021, its peak year, BMY generated $17 billion in free cash flow. That free cash flow is expected to fall to $14 billion by 2028 due to patent cliffs, increased marketing spending, and $8 to $9 billion in annual R&D spending.

But that's still $90 billion in free cash flow through 2028, making handling its debt easy.

{kind=link}

Rating agencies consider 3X debt/EBITDA safe and BMY is at 2X and on its way to 1.5X next year.

It has $13 billion in liquidity available and a well-staggered bond maturity portfolio.

{kind=link}

We have an A+ stable credit rating, implying a 0.6% 30-year bankruptcy risk and the bond market is willing to lend to BMY until 2097, an impressive 74 years for less than 7% interest rates.

FactSet Research Terminal

CDS are credit default swaps. They are insurance policies that are traded and represent real-time fundamental risk (default) estimates from the most risk-averse investors on earth.

The smart money on Wall Street says BMY's fundamental risk has been steady over the last 6 months, despite what the stock price might lead you to believe.

{kind=link}

Bristol has a 16-year dividend growth streak and has not cut its dividend in 52 years. Analysts expect about 4% to 5% dividend growth through 2028 and a 40% payout ratio up from 30% this year.

60% is a safe payout ratio, and BMY could keep growing the dividend at 4.5% annually through 2037 before hitting the 60% payout ratio.

- assuming zero growth for that long.

{kind=link}

Bristol growing at a flat rate, is worth 9.3X earnings, Ben Graham's 8.5X plus a modest premium for its wide-moat business and proven M&A ability to generate good growth.

- BMY could buy its way out of its growth problems.

So BMY, even with no long-term growth prospects, is potentially capable of a 50% upside within two years or a Warren Buffett-like 22% per year.

{kind=link}

The S&P has an 18% upside potential in the next two years if we avoid recession (the bond market says we won't).

BMY has the highest yield in 15 years, and is 28% undervalued, offering incredible return potential in the next two years.

However, long term that return potential is currently 4% to 5%, a bond-like return potential, and that's why I'm screening for superior-high yield bargain opportunities.

Finding 5+% Yielding Super Growth Bargains Better Than Bristol

Here is how I have used our DK Zen Research Terminal to find the best high-growth high-yield blue-chip bargain alternatives to Bristol.

From 505 stocks in our Master List to the best blue-chip aristocrat bargains.

All in one minute, thanks to the DK Zen Research Terminal. This is how I find all my investment ideas.

| Screening Criteria |

| Companies Remaining |

| % Of Master List |

| 1 |

| Blue-Chip Quality (10,11, 12, and 13 quality scores) |

| 467 |

| 93.40% |

| 2 |

| BHS Rating "reasonable buy, good buy, strong buy, very strong buy, ultra value buy." |

| 312 |

| 62.40% |

| 3 |

| Non-Speculative (No Turnaround Stocks, investment grade) |

| 277 |

| 55.40% |

| 4 |

| 5+% yield |

| 41 |

| 8.20% |

| 5 |

| 11+% long-term return potential |

| 25 |

| 5.00% |

| 6 |

| Sort By Long-Term Return Potential |

| 0.00% |

| 7 |

| Top 5 In Build Watchlist Tool |

| 5 |

| 1.00% |

| Total Time |

| 1 minute |

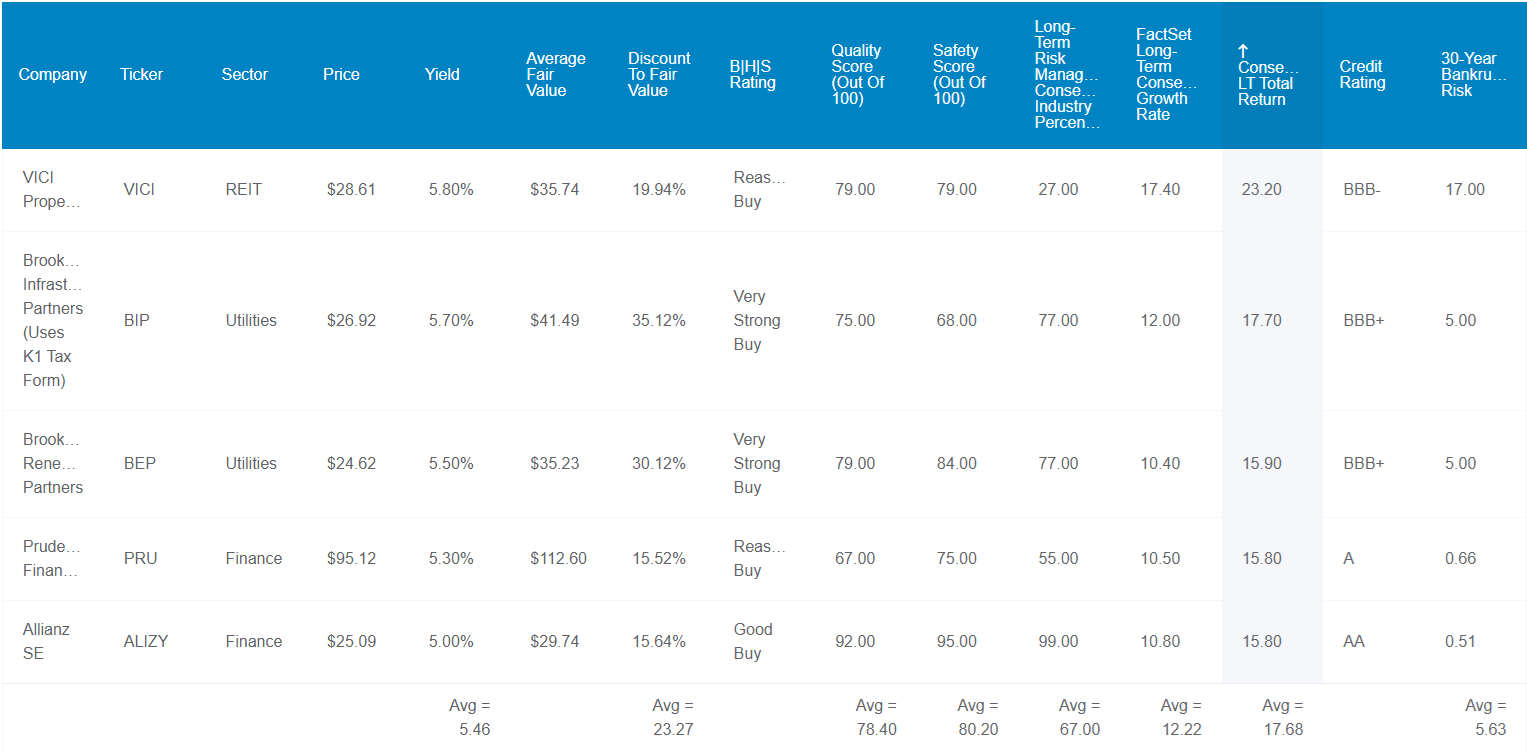

Here is the bottom line up front on these top 5 Bristol alternatives.

Fundamentals Summary

- yield: 5.5% (3X S&P 500 and above SCHD or VYM)

- dividend safety: 80% safe (2.3% dividend cut risk)

- overall quality: 78% low-risk SWAN

- credit rating: BBB+ stable outlook (5.63% 30-year bankruptcy risk)

- S&P LT Risk management global percentile: 67th = low risk (good risk management)

- long-term growth consensus: 12.2%

- long-term total return potential: 17.7% vs 10.2% S&P 500

- discount to fair value: 24% discount (potential good buy) vs 11% overvaluation on S&P and 28% undervalued BMY

- 10-year valuation boost: 2.8% annually

- 10-year consensus total return potential: 5.5% yield + 12.2% growth + 2.8% valuation boost = 20.5% vs 9% S&P and 7.6% BMY

- 10-year consensus total return potential: = 545 % vs 134% S&P 500 vs 108% BMY.

Bristol could soar 50% in 2 years, and in a decade double your money even with no growth thanks to its attractive valuation and dividend.

But these five anti-Bristol high-yield growth champions offer Buffett-like return potential for the next decade, potentially beating the S&P by 4X and turning $1 into $6.45.

{kind=link}

I've linked to articles about each company for further research.

- VICI Properties ( VICI )

- Brookfield Infrastructure ( BIPC ) ( BIP ) - K1 tax form (none from BIPC)

- Brookfield Renewable Corp ( BEPC )

- Prudential Financial ( PRU )

- Allianz ( ALIZY ).

Consensus Total Return Potential Through 2025

- if and only if each company grows as analysts expect

- and returns to historical market-determined fair value

- this is what you will make.

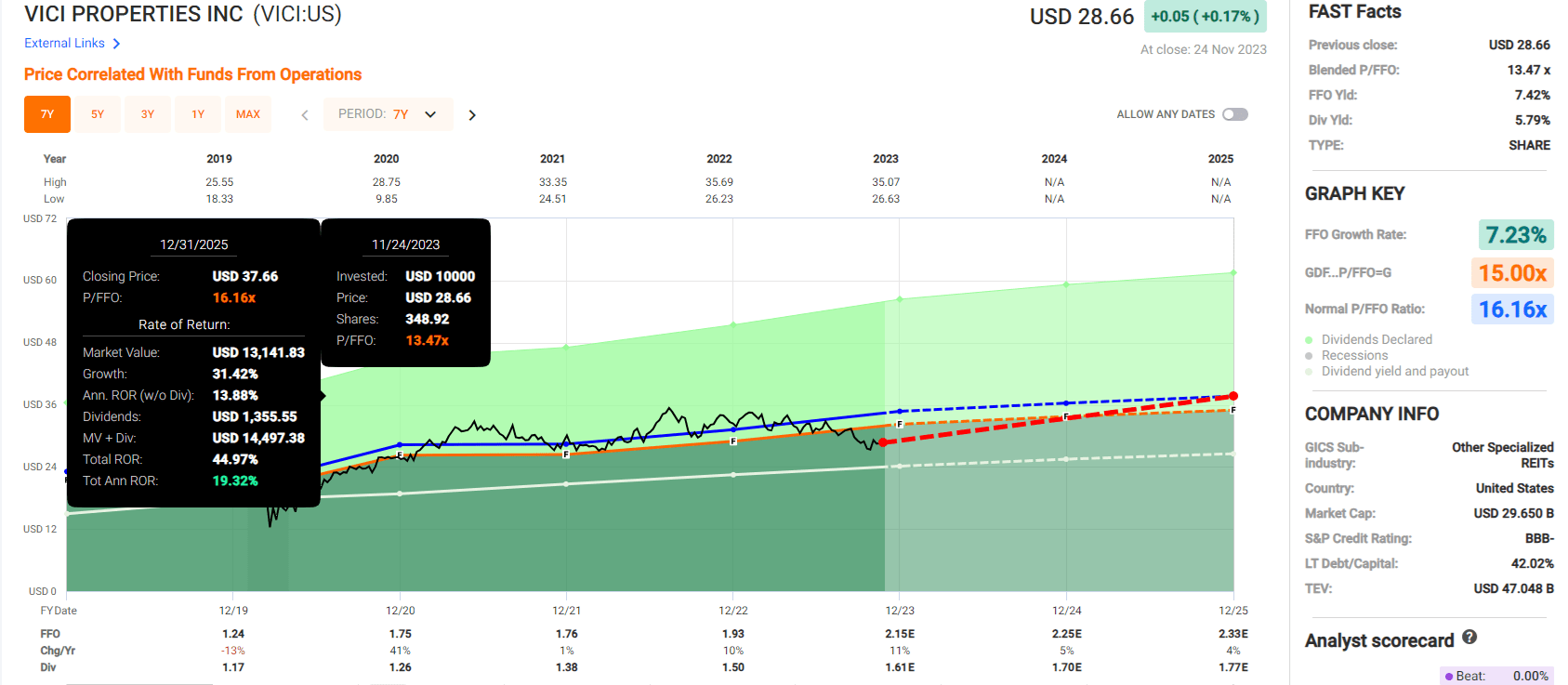

VICI

{kind=link}

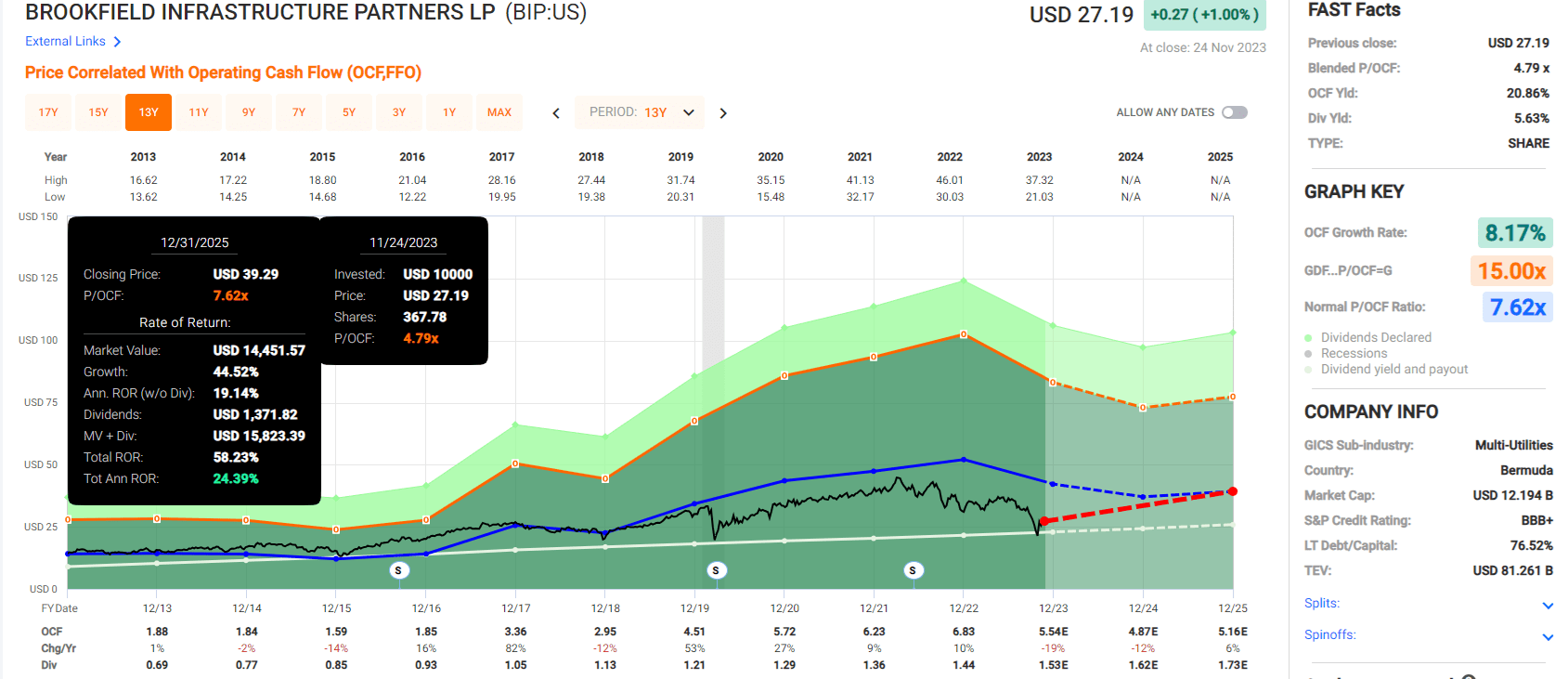

Brookfield Infrastructure

{kind=link}

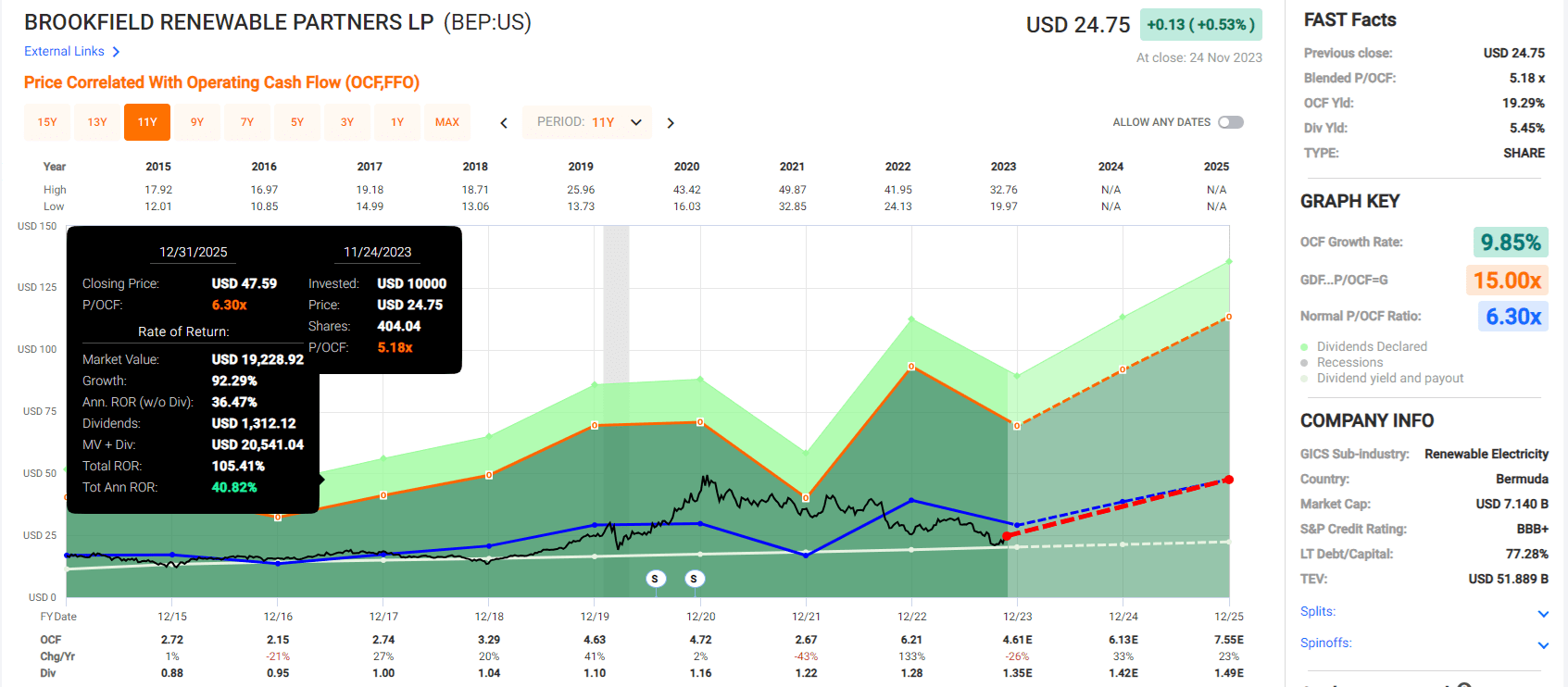

Brookfield Renewable Corp

{kind=link}

Prudential

{kind=link}

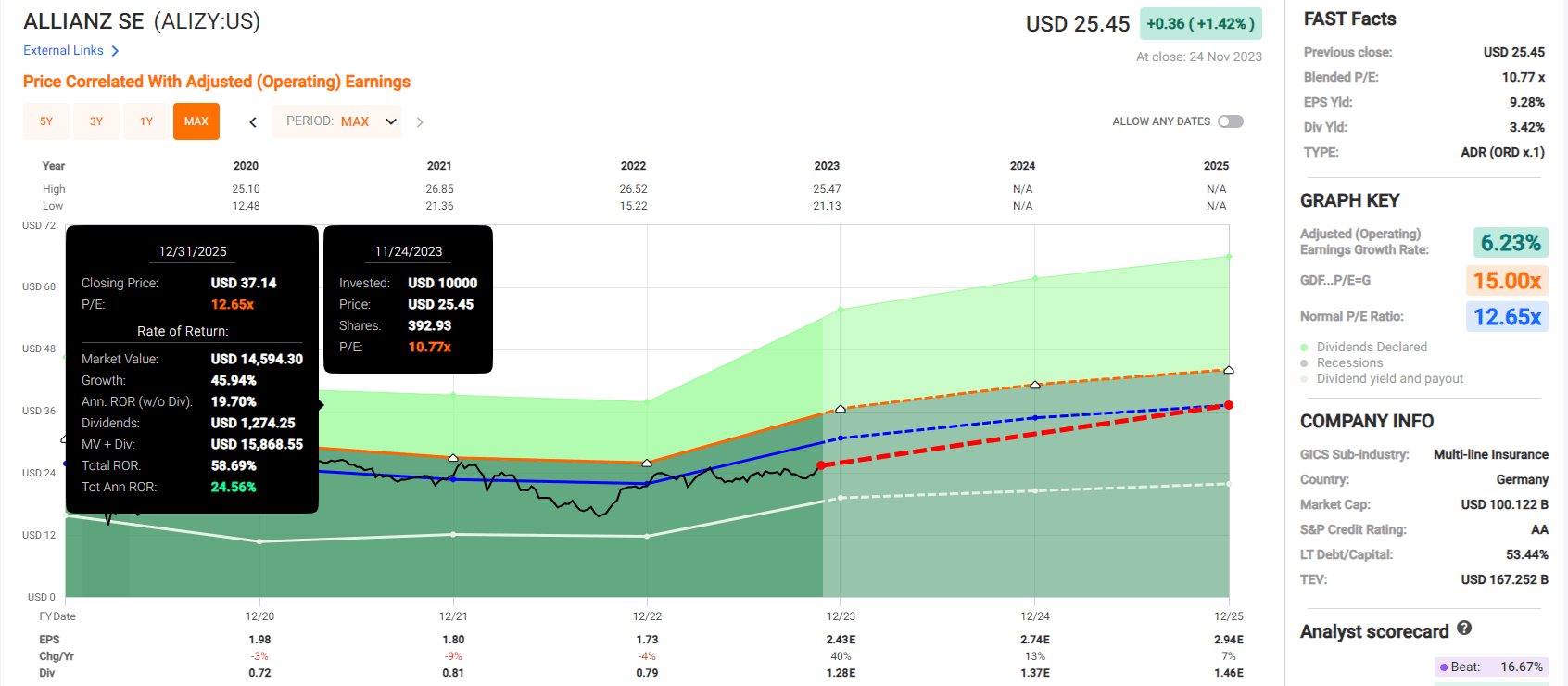

Allianz

{kind=link}

S&P 500

Bristol Is A Bargain, But Super Growth High-Yield Alternatives Are Available

Bristol-Myers Squibb Company is undervalued; there is no denying that at 7X earnings.

It is priced for -3% long-term growth, and analysts expect flat growth for the foreseeable future.

BMY has a great history of smart M&A, including buying Celgene, which boosted earnings by 65% over three years.

Do I think BMY will never grow again? No, I think it will be able to grow due to M&A.

Would I buy BMY today? I would not, despite the 50% upside potential over two years.

Not when VICI, BIPC, BEPC, PRU, and ALIZY represent much faster-growing, higher-yielding blue chips that collectively offer Buffett-like return potential for the next decade.

Bristol-Myers Squibb Company is a potentially strong buy in isolation for new money today, but investing should never be done in a vacuum.

For further details see:

Bristol-Myers Squibb Is A Great Buy, But These 5+% Yielding Bargains Are Better