MRVL - Broadcom Q2 Earnings Preview: A Beat Incoming - Focus On AI And Apple

2023-05-30 08:40:50 ET

Summary

- Broadcom Inc. will report Q2 earnings on June 1 after the market close and looks set to beat its own outlook and the Wall Street consensus driven by software and networking.

- Broadcom continues to be an underestimated beneficiary of the AI wave, and I believe the technology will have a positive contribution to revenue from the second half of the year.

- The new multiyear agreement with Apple Inc. removes a key risk from the investment thesis and allows for a higher valuation.

- The VMware acquisition looks set to be closed this calendar year as Broadcom works with regulators to remove any objections.

- I upgrade my price target on Broadcom, but following the increase in the share price over recent weeks, I lower my rating on AVGO shares, as the upside is limited.

Investment thesis

I lower my rating on Broadcom Inc. ( AVGO ) from Buy to Hold ahead of its Q2 earnings release scheduled for post-market on June 1, as the massive jump in share price over recent weeks has resulted in shares trading around fair value, leaving only limited upside for investors. Still, the long-term outlook for the company looks promising, in part driven by the company’s exposure to artificial intelligence, or AI. Also, I do project Broadcom to beat Q2 earnings in a few days and issue a bullish outlook.

Broadcom is one of my favorite semiconductor giants due to its less cyclical product offering and business diversification efforts with the integration of software companies acquired over the years. Today, the company is more of a tech conglomerate with a very strong product offering. And this is also reflected in its performance over the last several quarters as Broadcom continues to report impressive growth. In contrast, most of its peers have started to report negative growth rates over the last year.

The networking product segment, particularly in the AI space, presents significant opportunities for Broadcom, with projected growth and increasing demand from hyperscalers. In fact, I believe Broadcom is one of the most underestimated beneficiaries of the AI boom. Furthermore, the company's focus on networking semiconductors, strong gross margins, and the introduction of AI-specific chips position it favorably in the market. Also, Broadcom's software offerings and the pending VMware, Inc. ( VMW ) acquisition provide diversification and stability to the business. Finally, the recently announced Apple Inc. ( AAPL ) licensing deal also removes a key overhang and improves the risk-reward profile.

Overall, with solid financials, a favorable position in the AI market, and ongoing diversification efforts, Broadcom is well-positioned for long-term growth. Add a solid dividend yield of above 2%, strong dividend growth, and the fact that this company is a free cash flow ("FCF") machine with an FCF margin approaching 50%, and we get a very attractive investment proposition. Yet the recent increase in share price has made shares a tough one to recommend as the upside seems limited.

In this article, I will take you through the latest developments and update my estimates and view on the company accordingly.

A quarterly update including AI, an Apple licensing deal, and the VMware acquisition

Broadcom shareholders have had an amazing couple of weeks, with the share price increasing by over 31% over the last month and up a similar 28% since my previous article. This was driven by mighty earnings reports from competitors and peers like Nvidia Corporation ( NVDA ) and Marvell Technology, Inc. ( MRVL ), as well as some really good news reports for Broadcom specifically. Yet, this has put the share price above my price target of $729, with it now trading at around $812. With Broadcom set to report Q2 earnings on June 1, now is a good time to look back at the last quarter and see what we can expect from Broadcom’s upcoming earnings report and how this could impact long-term expectations and the price target.

Let’s first quickly look back at the Q1 performance and issued outlook to put things into perspective. Broadcom reported excellent quarterly results in Q1 , which showed impressive resiliency in the business. It reported revenue growth of 16% YoY, driven by the semiconductor product segment that reported 21% YoY growth, much better than most of its peers. Yet, Broadcom did guide for growth to slow down in Q2, with a revenue expectation of $8.7 billion, up only 8% YoY. This slowdown is driven by some seasonality in particular business segments and an overall slowdown in most segments as Broadcom customers are carefully looking at the health of the economy and consumer demand. The one positive for Broadcom here is that it primarily serves enterprise customers and only has very little exposure to consumer spending, making the company somewhat less sensitive to the economic slowdown. Meanwhile, Broadcom remains focused on its bottom line and costs, which should result in gross margins expanding by 150 basis points to a mighty 75.5% industry-leading gross margin.

Especially strong is the networking product segment of Broadcom as this one is projected to keep growing at above 20% while already accounting for 26% of total revenue in Q1. Driving this is massive demand by hyperscalers as these are trying to boost computing power and efficiency to run large AI models and satisfy demand. As a result, I called Broadcom an understated beneficiary of the AI wave.

Broadcom is an understated beneficiary of AI and financials should soon reflect this

On the note of AI, I already spent some time discussing the AI opportunity for Broadcom in my previous article, but today there is a little more clarity on the subject after Nvidia released a stellar Q2 outlook and Marvell spoke about the massive opportunity in AI it sees for its business. While Nvidia might be taking the most headlines here, it is actually the comments made by Marvell’s management that I find more interesting when looking at Broadcom, as both companies compete in the networking industry. Also, both of their networking business segments are the main contributor to their revenues while offering excellent growth potential driven by AI.

Simply put, networking semiconductors are crucial for AI applications as they enable the fast and efficient communication that is necessary for processing large amounts of data quickly and accurately. In reality, without top-performance networking solutions, AI models with billions of parameters would not be able to work. And still, current advanced AI systems are limited by the available bandwidth. This is how Marvell's management explained this during the earnings call :

To give you an idea, the latest dual CPU server in the cloud data center today can drive up to 200 gigabits per second of IO and contains the network interfaces to support that bandwidth. In contrast, an example of an advanced AI system containing 8 accelerators can drive close to 30 terabits of full duplex bandwidth.

Looking at Broadcom’s networking segment, this reported revenue of $2.3 billion last quarter, up 20% and now accounting for 26% of Broadcom’s revenue. And we should expect this to increase as a share of total revenue over the next several years as the fast growth and many investments from hyperscalers to support AI demand will function as a massive tailwind for this segment. Putting this into perspective, the hyperscaler market is expected to grow at a CAGR of 28.52% until 2030, according to Precedence Research. This is what I previously wrote about the role of networking semiconductors in hyperscalers:

Networking semiconductors are a crucial component for hyperscalers as these are responsible for managing the flow of data between servers, storage devices, and networking equipment. Hyperscalers rely on high-performance networking hardware to enable fast and reliable communication between their servers, which is essential for running their complex workloads. With Broadcom being the frontrunner in high-end networking semiconductors, this positions them favorably.

As a result, I believe the networking segment of Broadcom should see similar growth of around 20% over the next several years as well, to support this hyperscaler growth. Putting this into a bit more of a financial perspective, last quarter, Broadcom estimated that $800 million worth of Broadcom products would be deployed in AI systems by the end of the year, up 4x from $200 million in 2022, showing impressive growth. On top of this, Marvell management indicated during its latest earnings call that it sees dramatically improved demand for AI-related networking solutions YoY, resulting in the expectation of AI-related revenue to at least double in its fiscal 2024 and again in 2025, resulting in an AI revenue CAGR of 100% from its fiscal 2023 to 2025. Simply staggering expectations as the outlook looks solid and demand is high.

Contributing to this is something mentioned by Marvell during its recent earnings call in which management pointed out that the massive networking speed needed to power the AI infrastructure will also drive rapid advancements in networking equipment. Therefore, it projects the technology refresh happening at 18 months to 24 months versus four plus years in standard infrastructure. As a result, the revenue potential for Broadcom here is massive as long as it stays on top of its game. With hyperscalers cutting the technology refresh rate in half, the revenue potential for Broadcom doubles and it will be noticing this as early as the second half of this year.

As explained earlier, there is also the contribution of the increasing number of optical interfaces needed per AI system that drives demand. To support the full bandwidth available from GPU-powered datacenters, more of these optical interfaces are needed, driving up demand and revenue potential. And it is all these factors combined that should drive solid growth for Broadcom for years to come and we could see an impact as early as this quarter, although probably more profound in the second half of the year.

To support these hyperscaler networking needs, Broadcom already started shipping AI-specific chips under the name Jericho3-AI . According to Broadcom, the chip is capable of bringing together 32,000 GPUs, while bringing down the completion time frame by 10%, allowing AI accelerators to run 10% more efficiently compared to any alternative. Without getting too much into the technical details, Microsoft Corporation ( MSFT ) is currently running its GPT training runs using older systems with half the speed offered by this new Broadcom chip, making switching to this system very attractive for Microsoft. According to The Next Platform , no technical limitations should prohibit Microsoft from switching to this new Broadcom system. I believe this could be a meaningful catalyst for Broadcom’s AI-related revenue with the current high demand for any products that improve AI functionality in datacenters.

Overall, with the AI market expected to grow at a CAGR of 37.3% until 2030, there is plenty to be optimistic about and the research laid out above makes me believe Broadcom is in a solid position to benefit from it. The latest outlooks from Nvidia and Marvell show that we do not have to wait long for this revenue potential to be realized. As a result, I am very excited about Broadcom’s Q3 outlook, although I am not necessarily expecting similar fireworks here.

An improving software outlook and a VMware update

In addition to AI, improving demand for the company’s software offerings in Q2 should be a positive catalyst. Broadcom expects to grow its infrastructure software revenues by low to mid-single digits in Q2 after reporting a 1% revenue decline in Q1. This market is slowly accelerating again, which will positively affect margins for Broadcom as well, as the software products segment holds margins above 90%, meaningfully boosting overall margins for Broadcom.

While I am not overly impressed by the company’s software offering and continue to view semiconductors as my bull case driver, I do like the diversification in the business. Especially as the semiconductor industry tends to be quite cyclical, the software offering by Broadcom could offset such a slowdown ever so slightly, creating stability in addition to stellar gross margins.

Broadcom

In Q1, software accounted for 20% of total revenue as growth in the semiconductor segment has been much more impressive in recent years, bringing down this percentage. Yet, the pending VMware acquisition could increase this percentage to 44% while adding a dominant software platform to the offering. As a result, I am very much liking this potential acquisition. I am not overly worried about the debt this would add to the balance sheet as Broadcom has shown in the past that it is very good at integrating these businesses, resulting in the tech conglomerate it is today. I see no reason to change a winning strategy. Also, Broadcom’s excellent cash-generation ability (with an FCF margin approaching 50%) should be able to drive down debt pretty quickly again after the acquisition is completed. The one downside I see for this is somewhat lower shareholder contributions in the following couple of years, although without endangering the dividend.

So where does this acquisition stand today? In the Q1 earnings call, CEO Hock Tan stated that he still expected the transaction to be completed this year, which illustrates that management has confidence in completing this deal despite regulators continuing to scrutinize the deal. Seeking Alpha reported earlier this month that Broadcom has reportedly offered some remedies to European Union regulators to assuage antitrust concerns. I already didn’t see many reasons for an antitrust suit from regulators and with Broadcom now offering some remedies to alleviate any concerns, I really see no reason for this deal not to be closed. EU regulators now extended their deadline for a decision to July 17 while Broadcom and VMware have now moved the deal termination date to August 26 , and this could be extended further to November if the deal is not completed before then.

The new Apple licensing deal was expected but is still a meaningful catalyst for Broadcom

On May 23, Broadcom and Apple announced a new multiyear, multibillion-dollar agreement. The current licensing agreement was set to expire in July, so it was a matter of time for this news to come out as Apple was not ready yet to replace these Broadcom components with in-house manufactured alternatives. Apple will first aim to replace Qualcomm Incorporated ( QCOM ) equipment with in-house manufactured solutions before it focuses on replacing Broadcom due to the value of the components and the relationship between the companies.

The new deal means Broadcom will continue to develop 5G radio frequency and cutting-edge wireless connectivity components, including FBAR chips that are part of a radio-frequency system that helps iPhones and other Apple devices connect to mobile data networks.

The details of the deal were not released, but UBS analysts believe the deal will run through 2026 and likely is valued at more than $15 billion. Going by the growing number of iPhones sold and Apple’s revenue contribution in 2022, I expect the deal value to be closer to $20 billion.

Most importantly, the deal means Apple will not replace Broadcom components before 2027, removing a key overhang for the stock as Apple is responsible for a little under 20% of Broadcom revenues. This percentage has been trending down over recent years with other segments growing faster and Broadcom diversifying the business by acquiring software companies. Therefore, the impact of losing Apple as a customer by 2027 will most likely be no more than 3-4% of FY27 EPS.

Overall, the new deal takes away a meaningful risk, allowing for a higher valuation multiple due to an improved risk-reward profile.

Outlook & AVGO stock valuation

Broadcom is projecting revenue of $8.7 billion, up 8% YoY, and a slight margin improvement of 150 basis points to 75.5% in Q2. Considering the current economic environment, this is simply impressive. We should not forget that most large semiconductor companies like Nvidia, Advanced Micro Devices, Inc. ( AMD ), and Intel Corporation ( INTC ) are still reporting YoY declines, while Broadcom continues to expect high-single-digit growth. Also, I still see plenty of room for Broadcom to beat current estimates, as I expect AI to positively impact revenue from the year's second half onwards. For Q2, I am projecting Broadcom to report revenue of $8.77 billion and EPS of $10.18, which is slightly above the consensus estimates as I expect software and networking to perform somewhat better than anticipated. EPS is adjusted accordingly.

In addition to a continued solid performance, the company continues to diversify its revenue stream by investing in software initiatives and acquisitions, making the business more stable and less sensitive to cyclical downturns in the semiconductor industry. Add to this the fact that the company is an understated beneficiary of the shift towards AI integrations, and it's not hard to see that this business is in an excellent position for long-term continued growth.

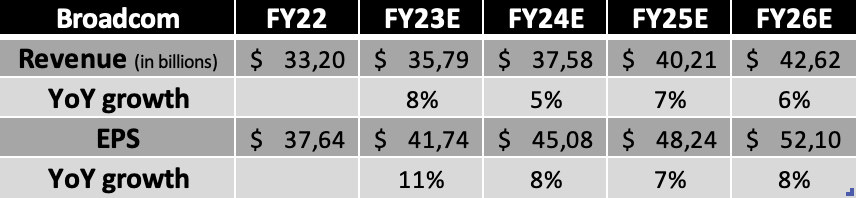

Following the outlook from management for its Q2 results, to be reported on June 1, and my deep dive into the business, I arrive at the following long-term projections.

Broadcom outlook (Daan Rijnberk)

{kind=link}

(Q2 revenue of $8.77 billion and EPS of $10.18)

Shortly explaining these estimates, I now project Broadcom to report revenue of $35.79 billion for FY23, driven by continued positive growth in the second half of the year, which is slightly above the current analyst estimates. I expect Broadcom to guide for a surprisingly strong Q3 with revenue of $8.8 billion, meaningfully above the analyst consensus and driven by a better-than-expected performance in networking and software. As explained before, networking revenues will be driven by high investments from hyperscalers, driven by the integration of AI across industries. The newly introduced AI-specific chip from Broadcom will also positively contribute to this.

As a result, I expect EPS to be up by double digits for the full year and revenue to remain resilient at high-single digits. For the following years, I project somewhat slower growth from Broadcom but EPS to outpace revenue growth due to further margin improvements and a higher share of revenue coming from software sales. Of course, just how impactful AI can be for Broadcom is still a huge question, but I do expect the networking semiconductor segment to continue to grow as a share of total revenue and maintain a growth rate of around 20%, driving growth for Broadcom. Overall, these estimates are still somewhat conservative and leave room for further improvement.

Moving to the valuation, this one has become quite a bit trickier after the massive share price jump over recent weeks, pushing its forward P/E to over 19x. Yet, this increase in share price was not unjustified as the new Apple agreement removed a key risk and stock overhang. Also, the VMware deal looks set to be completed later this year, while Broadcom continues to report above-industry growth rates in FY23 and could be a key beneficiary of the AI boom. As a result, I believe a higher valuation is justified for this high-quality semiconductor giant that has been trading at a significant discount for a long time. Today, it looks to be finally trading around fair value again.

Considering everything discussed in this article so far, I believe Broadcom deserves to be valued at a forward P/E of 19x (up from 16x) as this would still offer an attractive risk-reward profile considering the little risk involved in the investment today, putting it around fair value. Therefore, based on my FY24 EPS projection and a 19x P/E, I calculate a target price of $857 per share, leaving investors with an upside of slightly over 5%. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

Conclusion

I expect Broadcom to beat the Q2 analyst consensus and issue a bullish outlook for the third quarter after some positive AI commentary. Broadcom is in a great position today, diversifying its revenue stream, announcing a new multiyear Apple agreement with a value approaching $20 billion, the VMware deal looking to be completed this year, and the company consistently outperforming its peers.

Yet, this does not mean it is a buy today, ahead of its quarterly results. The undervaluation of the shares we have seen over the last six months has been largely corrected over recent weeks with shares jumping up over 30%, resulting in these trading around fair value. Also, I am not expecting Broadcom to issue a similarly impressive outlook as we have seen from the likes of Nvidia and Marvell. Some AI commentary and a solid outlook could potentially drive the share price somewhat higher, but the current valuation does not offer much upside for long-term investors.

With only a 5% upside to my price target, I am lowering my rating on Broadcom Inc. to hold, despite my share price target having increased by almost $100. Most AI fantasy and upside seem to be priced in today, with shares now trading 35% above their 5-year average.

The long-term outlook for Broadcom Inc. remains promising and I am incredibly confident in the ability of Hock Tan & Co to steer this one in the right direction to benefit from the AI wave and deliver double-digit yearly returns to investors. Therefore, I am now holding on to my shares and will look for the share price to drop below $770 before buying some more Broadcom Inc.

For further details see:

Broadcom Q2 Earnings Preview: A Beat Incoming - Focus On AI And Apple