CA - Brookfield Asset Management: A Potential 'Forever Hold'

2023-11-01 07:58:24 ET

Summary

- Brookfield Asset Management is a stable asset management business with high margins and a large moat around its asset products.

- BAM's earnings multiple is below financial sector averages despite the better-than-average results, which presents a value discrepancy we think should be taken advantage of.

- Management's path to value creation is simple, as the underlying business model is straightforward.

- We rate BAM stock a "Strong Buy".

As we pointed out in a recent article, being an asset manager is a great business if you find yourself in the position of being one:

It's (paradoxically) asset light, high margin, and incredibly predictable. Fees churn in quarter after quarter, no matter what is going on in the world.

However, not all asset management businesses are built the same.

In that recent article, we talked about the secular decline of T. Rowe Price ( TROW ) at the hands of passive investing giants, as TROW's core client base of baby boomers begins to die off, leaving their wealth in young, fee-averse hands.

However, when reviewing BlackRock ( BLK ), we had a different view - that the company was a long-term compounder, built for success over a massive time horizon.

Today, we're doing a deep dive on Brookfield Asset Management ( BAM ).

We'll get it out of the way before we start - we think this company has the potential to be a "Forever Hold" stock. The business is strong, the company's offerings continue to gather AUM, and the balance sheet is absolutely pristine.

Positioned to easily back a 4%+ dividend well into the future, in addition to the business's significant potential for capital appreciation, we think this stock is one to bet on.

Let's jump in.

Financial Results

For those who may be new to the story, BAM is the asset management business of Brookfield Corporation ( BN ). Recently, BN sold off 25% of its asset management business to the public markets in a transaction that created a new publicly traded entity.

It's a bit confusing, but here's a great explanation of how Brookfield looks now from a recent article by A.J. Button :

The basic structure looks like this:

On top, you have Brookfield, a holding company.

Below that, you have several operating subsidiaries in real estate, insurance and asset management. Brookfield Property Group and Brookfield Insurance are wholly owned by Brookfield, Brookfield Asset Management is 75% owned by Brookfield. Note that Brookfield Property Group is not the totality of Brookfield's real estate ventures. Some of them, such as Brookfield REIT, are publicly traded and not wholly owned by Brookfield.

One level down from that you have various listed entities like BIP and BEP. These are partially owned by Brookfield Asset Management, which is in turn 75% owned by Brookfield. For example, we can see in Brookfield's most recent 13F that it has 8.6% of its portfolio in BEP. The stake rises to 48% when you include BAM's holdings.

Just to summarize:

- Brookfield owns three segments; two outright, and then 75% of BAM (which is the company we're talking about today!)

- BAM itself then owns chunks of the various other listed Brookfield entities, like BEP and BIP .

This seems complex, and it is. However, given this unique public ownership structure, public markets investors can choose precisely which Brookfield businesses they want exposure to, which is a unique value proposition.

BAM, for its part, it a pure-play asset manager. The company's AUM recently crossed over $850 billion, and their products have seen strong inflows as their unique offerings continue to draw investors.

Brookfield is, at its core, an alternative asset manager. Unlike stocks or bonds, which is the domain of previously discussed companies like TROW or BLK, Brookfield funds own and operate high yielding, mostly hard assets like infrastructure, real estate, and renewables:

{kind=link}

This is a very high moat business, as the relationships and deal flow required to operate an asset manager in non-liquid assets often takes a long, long time to scale.

Additionally, the company has a very straightforward pitch for value creation:

We create shareholder value by increasing the earnings profile of our asset management business. Alternative asset management businesses such as ours are typically valued based on multiples of their Fee-Related Earnings and performance income.

This growth is achieved primarily by expanding the amount of Fee-Bearing Capital we manage, earning performance income such as carried interest through superior investment results and maintaining competitive operating margins.

As at June 30, 2023, we had Fee-Bearing Capital of $440 billion, of which 84% is long-dated or perpetual in nature, providing significant stability to our earnings profile. We consider Fee-Bearing Capital that is long-dated or perpetual in nature to be Fee-Bearing Capital relating to our long-term private funds, which are typically committed for 10 years+.

We seek to increase our Fee-Bearing Capital by growing the size of our existing product offerings and developing new strategies that cater to our clients’ investment needs.

But how has the new asset management company fared after breaking apart from BN?

In short, quite well.

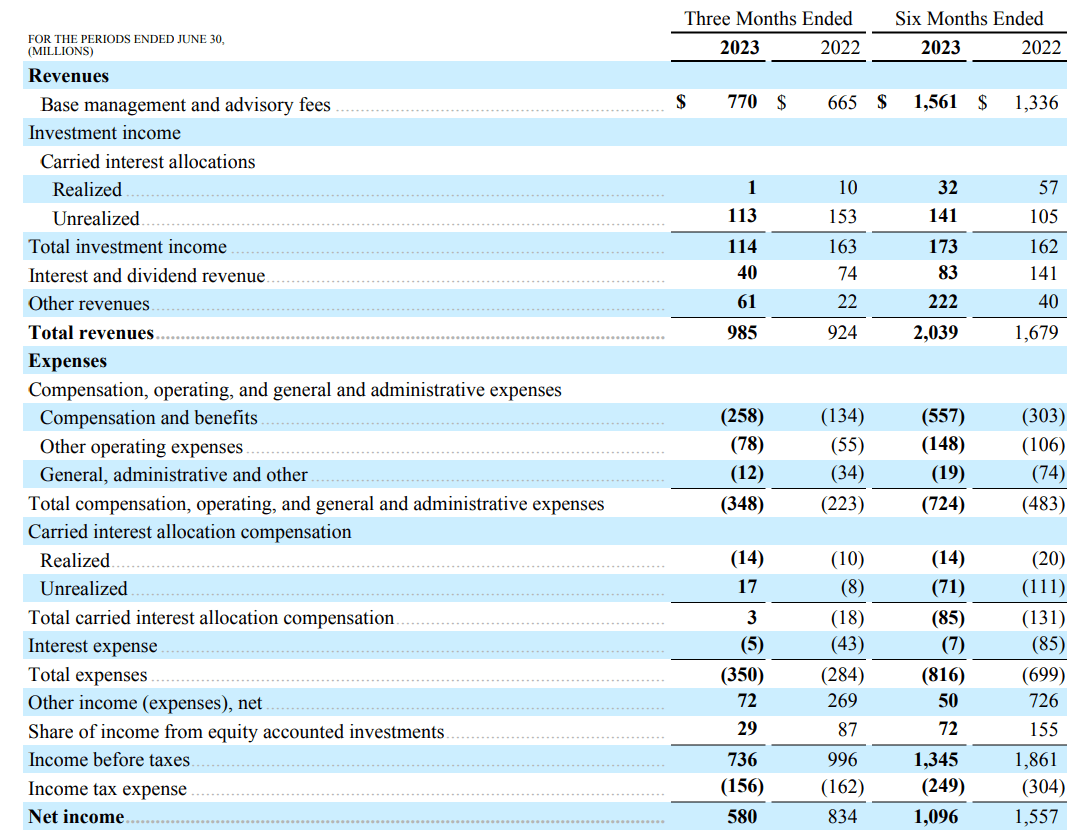

The company has '100%' gross profit margins, which reflects the lack of cost surrounding the core products. BAM also has 60%+ operating margins, reflective of the company's only real expenses around admin and operations:

{kind=link}

Then, much of that flows through to net income, after taxes are taken off the top.

This margin-thick business model is rare, even for asset managers, and represents a unique proposition in the asset management space, especially at this scale.

Valuation

But how is the company valued? Is it expensive?

Right now, the valuation looks relatively cheap.

If you extrapolate the first six months of this year into a FY23 measure, then BAM is trading at a 3.8x revenue multiple and a 5.45x net income multiple.

This seems nominally low vs. the average S&P 500 constituent but is in line with where the financial sector sits more broadly; around 2.1x sales and 8x earnings.

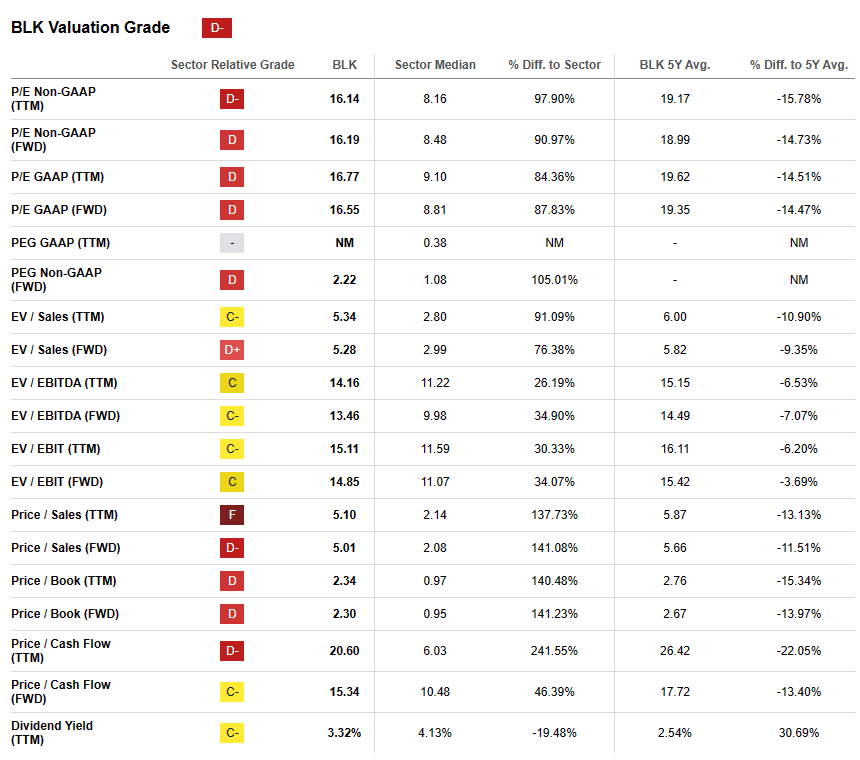

BlackRock, for context, trades at a 5.1x sales multiple and an 18x earnings multiple, which is on the higher side:

{kind=link}

Thus, when taken into account with the simplified operating structure, the pitch for investing into BAM at this juncture is simple:

- Brookfield Asset Management is a stable business,

- with incredibly high margins,

- boasting a large moat around its asset products,

- trading at a discount to industry averages.

The path to value creation is simple, and management has a strong track record of returns. Before BAM was separated from BN - inclusive of dividends - investors were up more than 3,000% since the year 2000.

Risks

Despite our positive outlook on the BAM's business and valuation, there are several risks with our thesis worth pointing out.

Slowdown In Demand For Infrastructure / Renewables : If demand dries up for alternative investments, then BAM is set to suffer. While the company has a large percentage of committed capital in its strategies for long periods of time, no significant investments into new funds would likely hurt growth, and thus, the multiple.

Operational Issues : BAM is exposed to the risk of losses due to operational failures, such as fraud, cyberattacks, or human error in relation to its underlying hard assets. This risk is particularly high given that BAM operates in a number of different industries, and with a number of complex deal structures.

Market Risk : If the market begins pricing BAM's underlying assets at a lower valuation, then fees go down, which ultimately hurts the multiple. Thankfully, the majority of BAM's assets are not traded live, and thus irregularly marked. This reduces this risk considerably.

Summary

Overall, Brookfield Asset Management looks like it could be a "Forever Hold" stock given the strong, simple business model, thick margins, high moat, and currently discounted valuation. The path to value creation is also simple, which means that understanding how the business is doing is straightforward.

While there are some end risks around the company's asset management activities, BAM has built a strong franchise that has mitigated them successfully to this point.

Overall, we rate BAM a "Strong Buy".

Cheers!

For further details see:

Brookfield Asset Management: A Potential 'Forever Hold'