CA - Brookfield Asset Management: Nice Yield And Lots Of Growth

2023-05-17 08:00:00 ET

Summary

- Brookfield Asset Management Ltd. is a high-quality company positioned for lots of growth.

- Brookfield Asset Management has delivered compelling Q1 results, especially considering the tough macro environment.

- Brookfield Asset Management offers a nice yield that should grow meaningfully going forward.

Article Thesis

Brookfield Asset Management Ltd. ( BAM ), the newest spinoff of the Brookfield empire, offers a nice dividend yield and should generate compelling business and earnings growth over the coming years. This combination makes BAM shares attractive, I believe.

The Newest Brookfield Entity

The Brookfield empire, headed by Brookfield Corporation ( BN ), is vast and somewhat hard to understand, as there are many different entities where there is, at least in some cases, an ownership interest between them.

The most recent entry in this empire is Brookfield Asset Management, an asset-light asset management pure-play that was partially spun off by the head of the empire, BN. BN still retains an equity stake of 75% in Brookfield Asset Management, however. Things are further complicated by the fact that Brookfield Asset Management and the related "BAM" ticker were previously used for the "mothership" (i.e., the new BN), which has since changed its name and ticker. This has resulted in a situation where some investors in BAM weren't sure what exactly they own now, which has resulted in selling pressure following the partial spinoff. This resulted in a great buying opportunity, and we first covered the new BAM last December . Since then, shares returned almost 20%, but they are still attractive today, I believe.

Like Brookfield Renewable Partners ( BEP , BEPC ), Brookfield Infrastructure Partners ( BIP , BIPC ), and Brookfield Business Partners ( BBU ), Brookfield Asset Management is a publicly traded daughter of Brookfield Corporation that is available to outside investors. The difference is that BN owns a particularly large stake in BAM. This can be seen as a positive, I believe -- BN might feel that BAM is the most promising and highest-growth entity among these, and thus prefers to own an especially large stake in this daughter entity.

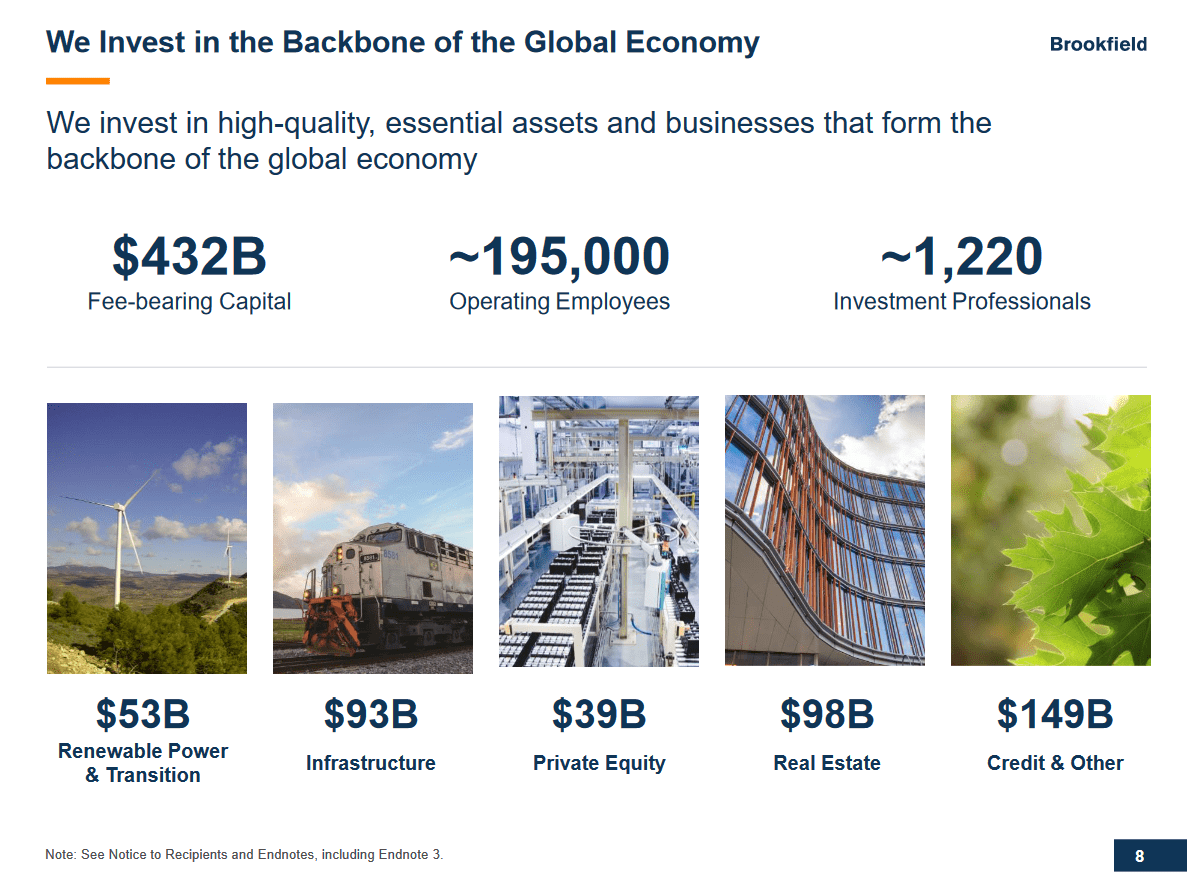

Unlike BEP and BIP, Brookfield Asset Management does not own a large array of real assets such as power generation facilities, pipelines, and so on. Instead, Brookfield Asset Management is asset-light and makes its money via fees that it receives for its management of funds from outside investors. This is, in general, comparable to how other asset managers operate, but there is an important distinction: The money that BAM manages is not deployed into exchange-traded funds ("ETFs") or other financial assets primarily, but instead, it's invested in real assets, such as the following:

{kind=link}

While there is some exposure to credit due to Brookfield's stake in Oaktree Capital Management, the majority of the assets that Brookfield manages are in infrastructure, real estate, renewable power facilities, and so on. These "hard assets" have several advantages: They oftentimes provide attractive returns, relative to the not overly attractive returns that investors can get from treasuries and other fixed-income assets, for example. The returns from infrastructure, real estate, and so on are also not closely correlated with the returns from equity and fixed-income markets. This makes an allocation towards these real assets attractive for institutional investors, for example, as it can help reduce portfolio volatility during uncertain times.

And last but not least, real assets generally provide solid inflation protection -- when inflation is running high, the actual assets that investors can invest in via Brookfield climb in value as well. And yet, institutional investors are underinvested in these attractive real assets, which is why Brookfield believes that institutional investors will increase their allocations meaningfully in the coming years and decades. This should provide compelling growth potential for alternative asset managers with a "real/hard asset" focus such as Brookfield. In recent years, we have seen Brookfield generate attractive inflows and fundraising activity has been strong as well, which underlines that substantial growth potential for the company due to (institutional) investors seeking to increase their allocation to real/hard assets due to their attractive characteristics shown above.

Brookfield Asset Management profits directly from this growth in the assets it manages, as fees are closely correlated to its assets under management, or AUM. Most of Brookfield Asset Management's earnings are fee-based and thus low-risk. Due to the asset-light business model, Brookfield Asset Management does not use any debt and can opt to pay out most of its profits via dividends.

The dividend yield, based on current prices, is exactly 4.0%. This is attractive in absolute terms, and also relative to what one can get from the broad market, as the S&P 500's (SP500) dividend yield is less than 2% today. But Brookfield Asset Management's real attractiveness comes from the growth potential for its dividend going forward. Brookfield believes that Brookfield Asset Management's fee-related earnings can grow by 15%-20% per year going forward, driven by rising values for existing assets and by new inflows. While there is no guarantee that Brookfield will be able to achieve that target, it should be noted that Brookfield has historically outperformed the goals set for its other daughter entities BEP and BIP -- the company thus does not have a history of overpromising. Instead, the company has a history of executing very well versus the goals it sets.

{kind=link}

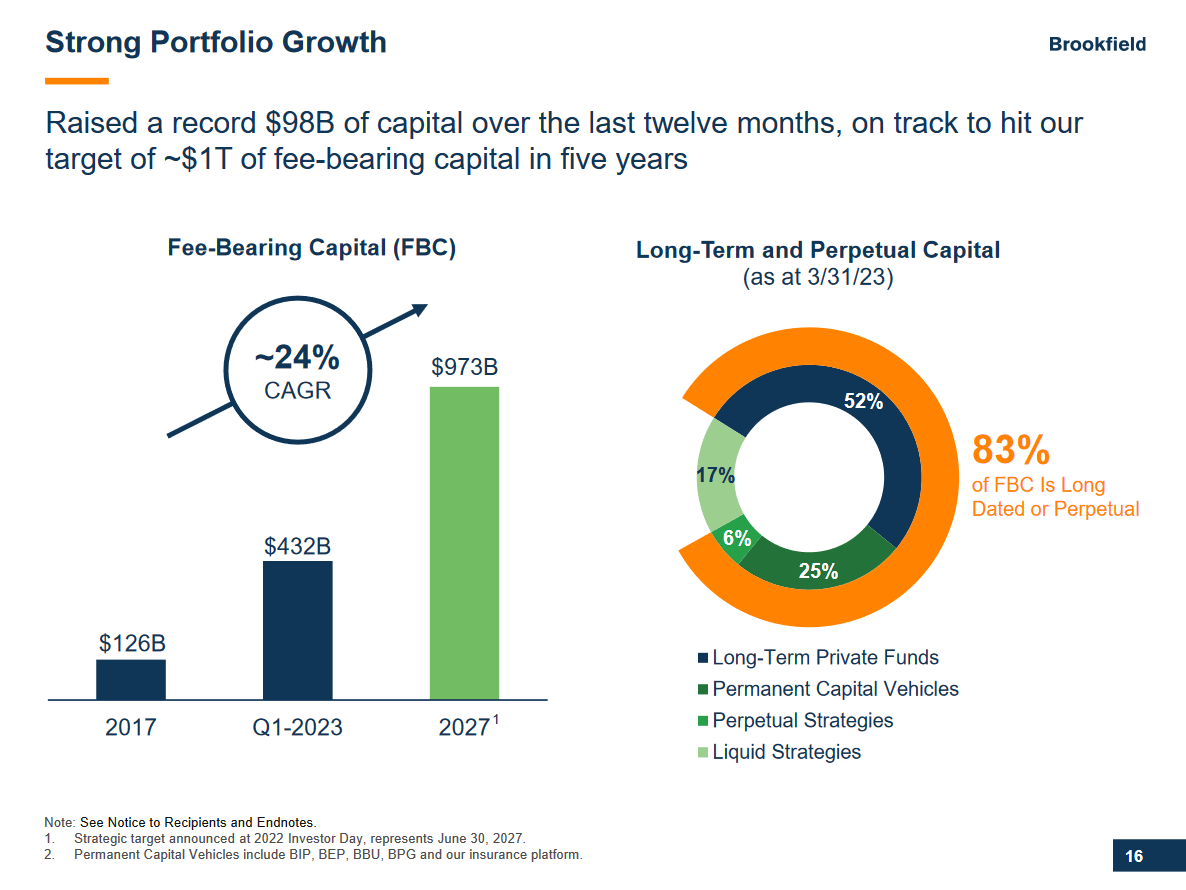

Fee-bearing capital has grown at a very attractive pace over the last five years, and even though relative growth will slow down to some extent -- maintaining a very high relative growth rate forever is impossible -- the company should continue to benefit from strong growth. Recent fundraising activity has been compelling, as the last four quarters were Brookfield's best period in absolute terms. The company says it's on track to see its fee-bearing capital grow to around $1 trillion by 2027, which would be a little more than twice as much compared to the end of the first quarter. With annual fundraising in the $100 billion range (and possibly growing further), and with some underlying growth from existing assets, that seems like an achievable goal. In turn, this suggests that the fee-based earnings growth estimates could be achievable as well.

The good news is that Brookfield Asset Management should be a very solid investment even if earnings grow a lot less than expected. If the company delivers annual profit growth in the 8-9% range instead of in the 15%-20% range, i.e., half as much as expected, then total returns could still be in the 12%-13% range as BAM would deliver a high single digit earnings and dividend growth rate and since the dividend already yields 4% today. I like investments where the total return outlook is reasonably compelling even if the company substantially underperforms market expectations and management guidance, as this makes for a built-in margin of safety.

Of course, it's possible that there will be no earnings growth at all, or that earnings even decline going forward, but I believe that this is highly unlikely based on the growth tailwinds for the industry and Brookfield's strong position and great track record. I believe that profit growth in the high single digits would already be a reasonably bearish assumption, and it would still make for a very solid dividend growth investment.

Final Thoughts

Brookfield Asset Management Ltd. generated compelling first-quarter earnings results . During that period, the company generated sales growth of close to 30% and raised $19 billion in new capital. This made Brookfield Asset Management's fee-related earnings rise by 10% year over year. That's a little below expectations for the long-term growth rate, but considering the massive market uncertainties and turmoil over the last year, where many asset managers saw their profits decline, that's still a comparatively strong result.

In better times, I expect Brookfield Asset Management's earnings growth to come in ahead of the rate seen during the first quarter, likely closer to the target rate of 15%-20% per year.

Distributable earnings were up by 13% year-over-year, which was a very compelling result as well, considering the macro headwinds and the struggles seen by other asset managers. For the last twelve months, Brookfield Asset Management saw its distributable earnings per share grow at a double-digit rate as well, showcasing that the Q1 performance was not an outlier and that BAM is positioned to deliver compelling business growth even during tough times.

Today, Brookfield Asset Management trades at around 23x this year's expected net profit. That's not a low valuation in absolute terms, but considering the strong growth outlook and the attractive dividend yield, one can, I believe, definitely argue that a low 20s earnings multiple is justified here.

In the long run, I believe that there is a good chance for considerable total returns with Brookfield Asset Management Ltd. stock, between a nice dividend yield that should grow meaningfully and due to the expected earnings growth. Brookfield Asset Management Ltd. remains attractive.

For further details see:

Brookfield Asset Management: Nice Yield And Lots Of Growth