CA - Brookfield Asset Management: Time To Buy This Best-Of-Breed Blue-Chip

2023-12-07 00:19:25 ET

Summary

- The alternative asset management industry is poised to continue growing quickly in the years to come.

- As a leader within its industry, Brookfield Asset Management should greatly benefit from this promising industry outlook.

- BAM's financial fortitude earns it an enviable credit rating from S&P on a stable outlook.

- Shares of the asset manager are priced approximately 27% below fair value.

- BAM could almost 4x the total returns of the S&P 500 index over the next 10 years.

At 26 years old, I hope to have many more decades ahead to invest. I don't want to take anything for granted, so I routinely eat a healthy diet (by American standards anyway), briskly walk/jog at least 150 minutes weekly, and do strength training four days a week. Statistically, these actions should maximize my probability of achieving exceptional longevity.

This is also why my portfolio is focused on buying top-notch companies operating in industries with secular growth catalysts. Since I reasonably expect to be around for a while, it makes sense to prioritize owning best-of-breed businesses in growing industries.

As a leader within the alternative asset management space, they arguably don't get any better than Brookfield Asset Management ( BAM ). This is why I opened a starter position in BAM in August. Right now, BAM is the 38th largest holding within my 101 stock dividend growth portfolio, accounting for 1% of my portfolio by value. I'd ideally like to get that to between 1.5% and 2% of my portfolio over time. Please allow me to discuss why I like BAM's fundamentals and valuation enough to initiate a buy rating.

{kind=link}

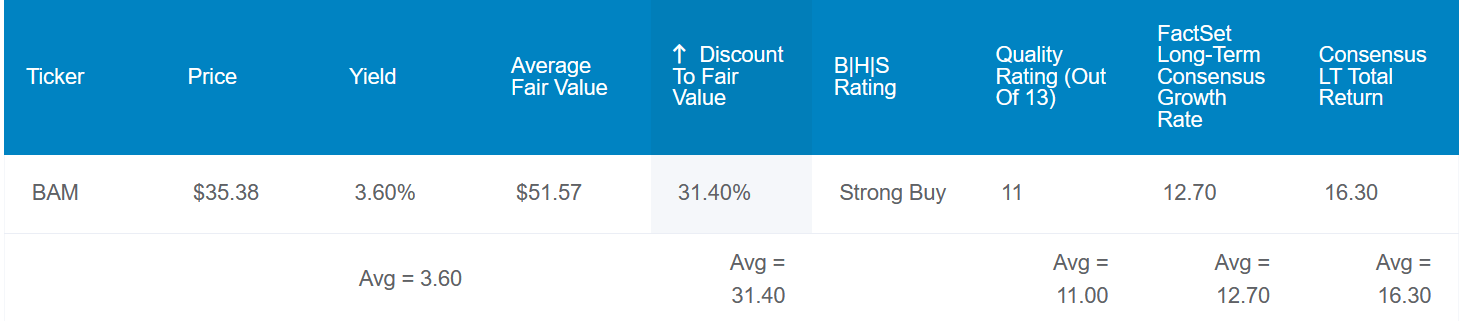

BAM's 3.6% dividend yield is attractive versus the S&P 500 index's ( SP500 ) 1.5% yield. As I'll discuss further below, I also think the stock is more enticing than the 4.1% yield of the 10-year U.S. treasury for my circumstances.

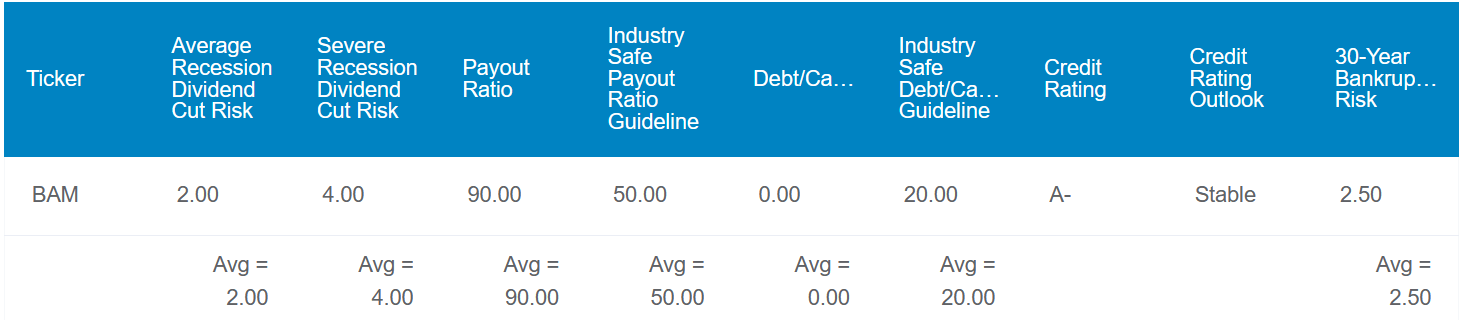

But moving back to the subject of BAM's dividend, it is safer than it may initially appear. The company's 90% payout ratio is elevated versus the 50% payout ratio that rating agencies prefer for its industry. However, BAM shines through as an exception to this rule because it has no long-term debt. The company's immaculate 0% debt-to-capital ratio is far below the 20% that rating agencies consider safe for the asset management industry.

That's why S&P is confident enough to rate BAM's debt A- on a stable outlook. This implies that the risk of the company defaulting on its debt in the next 30 years is just 2.5%.

As I'll discuss below, BAM also has some of the most stable cash flows in its industry. For these reasons, the probability of a dividend cut in the next average recession is modest at 2%. Even in the next severe recession, Dividend Kings estimates the chance of a dividend cut at 4%.

{kind=link}

Fundamentally, BAM is a blue chip, possessing an 11/13 quality rating from Dividend Kings. Not to mention that with the current valuation, it is a world-class business trading at a wonderful price.

According to historical dividend yield and valuation multiples, Dividend Kings values shares of BAM at about $52 each. Using the following inputs in the dividend discount model, I get a similar fair value of $47 a share: A $1.28 annualized dividend per share, a 10% discount rate, and a 7.25% long-term annual dividend growth rate.

Averaging these two fair values together, shares of BAM could be worth roughly $49 a share. From the current $36 share price (as of December 6, 2023), that suggests the stock is trading at 27% less than fair value.

If BAM can grow as expected and return to fair value, here are the total returns that could lie ahead for shareholders in the coming 10 years:

- 3.6% yield + 12.7% FactSet Research annual growth consensus + a 3.2% annual valuation multiple upside = 19.5% annual total return potential or a 494% cumulative 10-year total return versus the 9% annual total return potential of the S&P 500 or a 137% cumulative 10-year total return

A Trusted Alternative Asset Manager With Stable, Recurring Revenue

{kind=link}

Before diving into the specifics of BAM, let's take just a moment to define alternative assets. Alternative assets are any asset that isn't stocks, bonds, or cash. This includes real estate, commodities, and farmland.

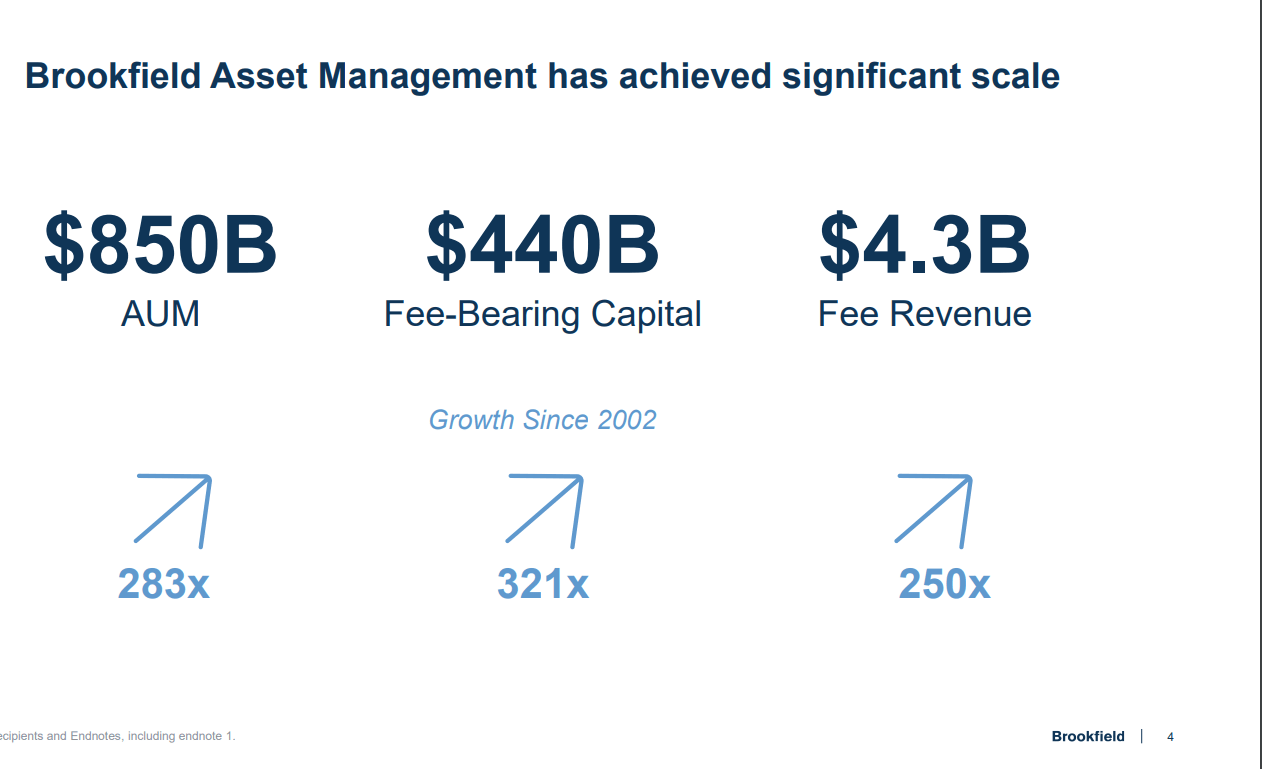

BAM's $850 billion in assets under management as of September 30 position it as the third largest publicly traded alternative asset manager. This has rocketed higher by 283-fold in just the last 21 years. The company's AUM is diversified through a variety of investments with promising tailwinds, such as renewable energy, data centers, and artificial intelligence.

For context, BAM's AUM is narrowly behind the $854 billion in AUM that Hamilton Lane ( HLNE ) oversaw as of Sept. 30. It's also moderately behind Blackstone's ( BX ) $1 trillion in AUM as of that date.

In an industry as large as alternative asset management, there is plenty of room for each of these players to generate outsized returns. This is because as investors seek superior returns and diversify their portfolios, alternative assets are playing an increasing role. That is why Ernst & Young thinks that the global alternative asset management industry is expected to grow from $10 trillion in 2019 to a staggering $23 trillion by 2026.

{kind=link}

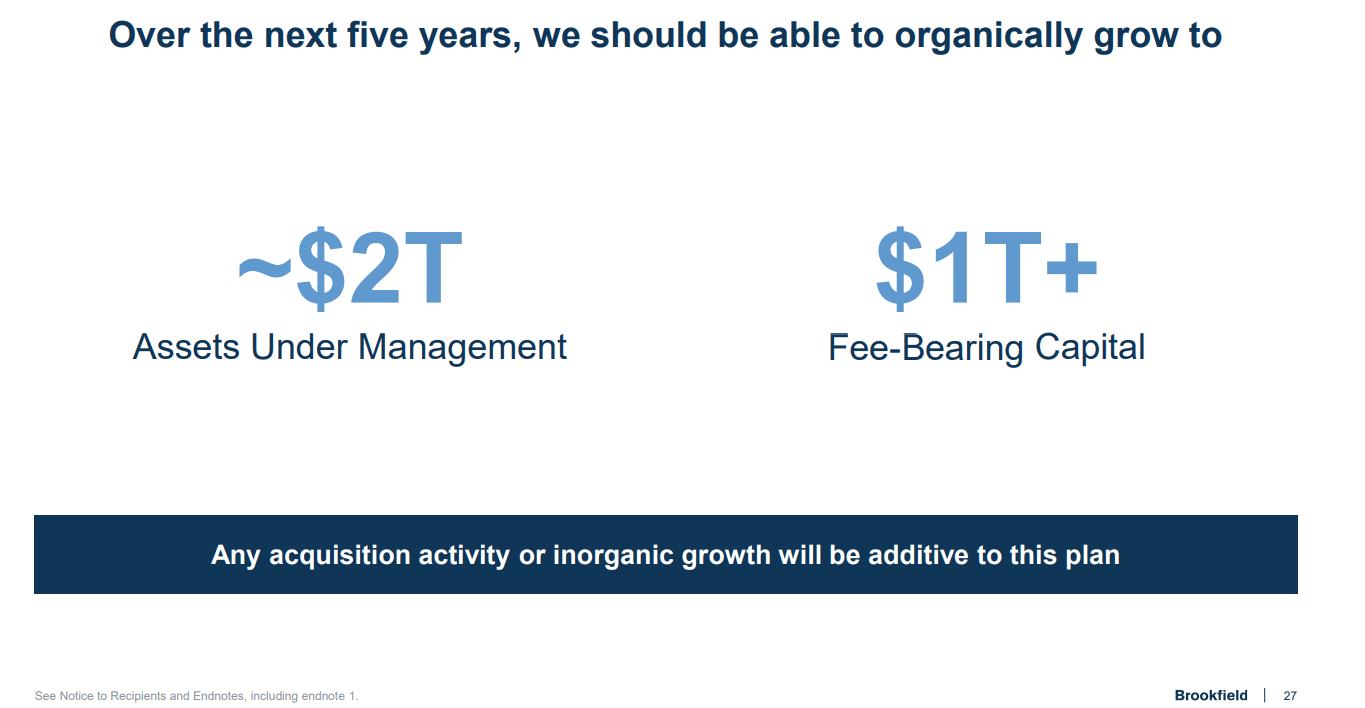

BAM itself expects its total AUM to reach $2 trillion in the next five years. In addition, the company projects it will hit $1 trillion in fee-bearing capital (more than double its current mark) within the next five years. Sure, a skeptic would argue that management is wearing rose-colored shades.

However, there are two reasons to believe that the company can deliver. For one, BAM is on pace to add $150 billion of new capital to its AUM base in 2023 alone. On top of organic AUM growth, this puts the company on track to achieve these targets.

Not to mention that we have already seen this movie before. In 2018, BAM planned to double its fee-bearing capital from $129 billion to $245 billion by 2023 - - a 14% compound annual growth rate. As it stands, the company's $440 billion in fee-bearing capital (a mindboggling 27% CAGR) far exceeds that projection. If anything, BAM has a reputation for being a conservatively run company as it relates to financial projections. Thus, FactSet Research anticipates that the company can compound its earnings by 12.7% annually long term.

All the while, 86% of BAM's fee-bearing capital is long-dated or perpetual, which translates into revenue and earnings stability (page 12 of 85 of BAM 10-Q ). The fact that thousands of institutional investors (e.g., smart money) agree to these terms is a testament to the company's ability to generate spectacular returns for decades.

Best of all, BAM carried $2.9 billion on its balance sheet as of Sept. 30 and no debt. That's why it isn't a surprise that S&P awards the company with an A- credit rating on a stable outlook.

A Sizable Dividend Hike Could Be Around The Corner

Aside from BAM's market-beating yield, another characteristic that I like about the company is its dividend growth potential.

When asked by JPMorgan's ( JPM ) Ken Worthington about dividend policy, CFO Bahir Manios had this to say in the Q3 earnings call :

Hi, it's Bahir, I'll take a stab at that one. So look, our stated target when we spun off the company is to return 90% plus of the total distributable earnings that we generate in the business back to our owners, predominantly through dividends, but also through stock buybacks. Look, we've gone through the momentum that we have on the fundraising side with a path to getting somewhere close to $150 billion.

I would note 80% of that is capital where we make fees on committed capital versus on deployment. So with a lot of visibility on that, in addition to the remarks I made earlier around margins and having that expand going into next year, we believe that 2024 could be a step change year with respect to growth from an FRE and distributable earnings perspective.

And so based on that, and you can deduce that the dividend growth for next year could be quite sizable, and we'll get that all approved at our February board meeting and announce it with our February results.

BAM's significant growth in its AUM base could justify a double-digit raise in its quarterly dividend per share from the current level of $0.32 . The analyst consensus is that BAM will grow its fee-related earnings by 14.1% year-over-year to $1.54 in 2024. This is why I am predicting that BAM will boost its quarterly dividend per share by 15.6% to $0.37 come February.

Risks To Consider

As great of a company as BAM is on paper, it's still not perfect or for everyone.

In the alternative asset management industry, reputation is everything. BAM will have to continue to deliver competitive investment results to its clients to keep money flowing into its funds. If the company can't keep this up, it could risk losing out to competitors. This could harm BAM's growth prospects and weigh on dividend growth as well.

Having less than 18 months under its belt as an independent publicly traded company, BAM doesn't have the track record that some investors may prefer.

A general operating risk that applies to all companies these days, and BAM especially, is the potential for a breach of its IT systems. If this were to occur, scores of proprietary data and sensitive client data could become compromised. This could result in disruptions to BAM's operations, as well as result in lawsuits and damage to its reputation.

Readers who would like a more comprehensive discussion of the company's risks are encouraged to visit the risk factors section of its most recent annual report .

Summary: BAM Is An Appealing And Cheap Dividend Growth Stock

BAM is a dividend growth stock that I would like to build my stake in over time. I like the company's leadership in a steadily growing industry. I also appreciate the conservative balance sheet. Finally, though BAM doesn't yet have its own reputation for dividend growth, the commitment to shareholders appears to be there.

Finally, shares could be 27% undervalued relative to fair value. These reasons underscore my bullishness toward the stock as a pick for dividend growth and total returns.

For further details see:

Brookfield Asset Management: Time To Buy This Best-Of-Breed Blue-Chip