CCJ - Brookfield Business Partners: A Top Pick For 2023

Summary

- BBU units are trading at an extremely low valuation.

- While there are risks such as high leverage in a rising rates environment, we believe these are compensated by a very discounted valuation.

- We believe a potential catalyst for the valuation to recover will be when the Fed signals it is done with its current interest rate hiking campaign.

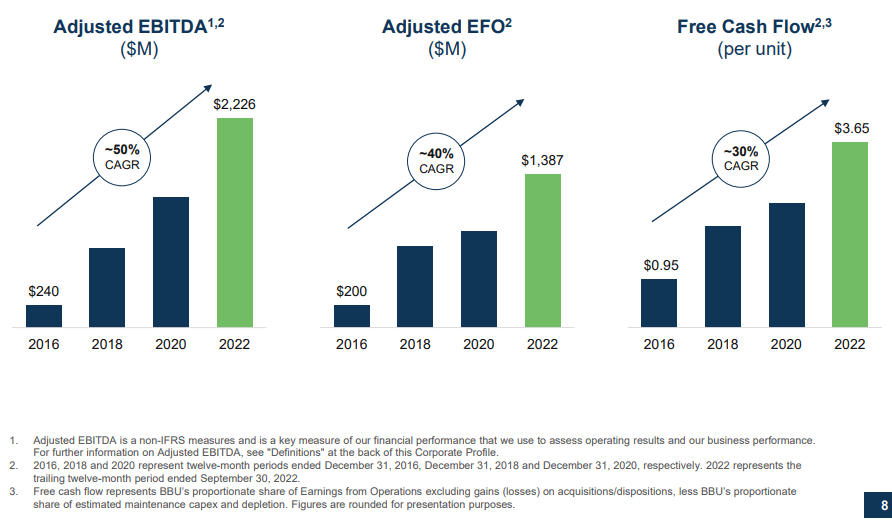

We are surprised to see how low the price of Brookfield Business Partners ( BBU ) units has gotten. While the company is operating in a challenging environment, it has made tremendous progress over the last five years in terms of increasing the EBITDA from its collection of businesses, and the free cash flow per share is much higher. Admittedly, inflation and rising interest rates are big investor concerns, but those headwinds appear manageable and more than discounted at these prices.

During the last earnings call, the company reported that inflation remains a significant issue. For example, most categories that form their cost of delivery, whether it be raw materials, transportation, logistics, labor, energy, remain elevated and above pre-Covid levels. The good news is that they are seeing many of these areas resetting back to the trend line over time. The company has also done a fairly good job of increasing prices to recover from inflationary cost pressure and to maintain margins.

One of the company's biggest wins came in October, when the company reached an agreement to sell Westinghouse to a strategic consortium led by Cameco Corporation ( CCJ ) and Brookfield Renewable Partners ( BEP ) for $8 billion. This is expected to generate about $1.8 billion of net proceeds to BBU and crystallize a 6 times multiple on its investments when combined with all the distributions that the company has received to date. The company expects to close the sale in the second half of next year.

BBU Investor Presentation

A large part of the BBU investment thesis is around operational improvement of the businesses and improving EBITDA. Revenue growth is typically not a large part of the equation. Based on EBITDA growth, we would say the company is doing a good job in general, even if not all of its investments have been widely successful. What is important is that, on average, EBITDA continues to grow, and especially free cash flow per share.

Entering a potentially recessionary environment, the company is focused in at least not losing market share, but it might still experience a reduction in orders, whether it'd be products or services. Mitigating this risk is a good diversification, with Adjusted EBITDA well-balanced between business services, infrastructure services, and industrials. For investors interested in learning more about the different businesses the company owns, we recommend reading our article sharing the BBU Investor Day Highlights.

{kind=link}

Q3 2022 Results

BBU reported strong financial results in the third quarter, with Adjusted EBITDA increasing to $627 million from $443 million last year. The company ended the quarter with $2.8 billion of pro forma corporate liquidity. This takes into account the planned syndication of recently closed acquisitions, as well as the expected proceeds from the sale of its Westinghouse investment.

Balance Sheet

A big concern for BBU investors is the balance sheet, especially given the rising rates environment. While we believe the debt load is currently manageable for the company, especially given that most of it is non-recourse, we would be more at ease if the weighted average maturity was longer and the percentage of fixed borrowings higher. The company currently has a 4.5 years weighted average maturity of debt outstanding, most of it non-recourse debt held at the operating company level. The company claims that it uses appropriate levels of leverage, focusing on serviceability and sustainability. Approximately 40% of non-recourse borrowings are fixed or hedged, with a weighted average borrowing cost of 6.3%. As the debt is refinanced, we would expect the average borrowing cost to move higher in the current environment.

Leverage

During the last earnings call , an analyst asked about the company's strategy to reduce leverage. The answer was that debt to EBITDA should actually come down over time just through improved earnings. CFO Jaspreet Dehl went into more detail regarding how the company thinks about leverage within the business. A particularly interesting data point shared was that the company estimates a 75 basis points increase in interest rates impacts earnings by ~$65 million.

So when we think about leverage within the business, we really think about it from the perspective of each of our operating companies and every business is different. There's some businesses where we've always operated them with a very low level of leverage just given kind of the underlying profile of the business, and there's others, which are kind of more stable, contractual, in some cases, inflation linked businesses that have the ability to service a higher level of debt. We were obviously very closely monitoring the impact of higher interest rates on kind of the serviceability of debt in each of our portfolio companies and also, just in terms of deleveraging or refinancing where it's appropriate. The business is generating a lot of free cash flow today, so it gives us with a lot of flexibility to be able to kind of manage that as it comes up. And based on kind of the current profile and the debt that we have in place, about 75 basis points impact has about $60 million, $65 million impact on EFO, and considering the run rate that's a very small percentage. So we think the portfolio is very well set up to kind of manage through it. There will be some businesses that come up for refinancing that we'll have to work through, but nothing that concerns us at this point, I mean that's not manageable.

Valuation

While rising rates, leverage, and inflation are valid investor concerns, we believe that the valuation is already discounting for these issues and more. According to the company, their operations have generated ~$800 million of free cash flow in the last twelve months. This is after interest, taxes, required maintenance CapEx and depletion. As a result, at current prices, units are trading at around a 5 times multiple of free cash flow. This is extremely cheap, and the main reason why we believe units are set up to perform very well next year, especially if 2023 brings more clarity as to when the Fed will pause its interest hiking campaign.

{kind=link}

Risks

As we've already discussed, the main risk with an investment in BBU is the balance sheet and the considerable leverage. While it currently appears manageable, this could quickly change if the economy deteriorates significantly. This is reflected in a low Altman Z-score, which is below the 3.0 threshold.

Seeking Alpha

Conclusion

We believe BBU is a top pick for 2023 given how cheap units have gotten. Trading at ~5x free cash flow, there is a lot of potential upside. We believe a catalyst for the valuation to recover will be when the Fed signals it is done with its interest rate hiking campaign. We believe that should happen sometime next year. In other words, while inflation, leverage, and a weak balance sheet are reasons for concern, BBU's valuation is extremely low and can make a quick recovery once investors are convinced the Fed is done rising rates.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Brookfield Business Partners: A Top Pick For 2023