CA - Brookfield Corp.: Once In A Decade Opportunity

2023-05-03 22:31:06 ET

Summary

- Brookfield Corp. is suffering from the perception of office defaults that have little actual bearing on its valuation.

- In attempting to discount low-quality offices, the market discounted the entire real-estate portfolio and insurance business.

- As a result, investors have the chance to get those businesses for free, in addition to large exposure to BAM, the "crown jewel" asset manager.

- Brookfield Corp. represents better risk-reward than Brookfield Asset Manager.

- Brookfield Corp. trades at a valuation last seen in 2011, 2009, and 2002 - all great times to buy - and less than March 2020.

Introduction

Brookfield owns and manages an enormous variety of cash-flowing real-assets, from infrastructure, to real-estate, to renewables, to private credit, to insurance. Global allocation to alternatives such as these has gone from essentially zero 25 years ago, to around 6% today, leaving plenty of room for growth as the alternative asset industry hits its stride.

Global Asset Allocation - lots of room to increase allocation to the alternatives Brookfield specializes in (Data from Wikipedia)

As one of the largest and oldest players in the space, Brookfield benefits from scale, expertise, and global reach keeping competitors few and profits high. Combined with a tremendous track record, compounding at nearly 20% over the last 20 years, and considerable insider ownership, Brookfield’s safety, quality, and growth is hardly in doubt.

When I wrote last, I found that Brookfield Corporation ( BN ), a complicated collection of equity in Brookfield’s various assets, and Brookfield Asset Management ( BAM ), a predictable business that earns fees off the assets it invests on behalf of others, were likely the best ways to invest in Brookfield. At the time, the return potential of both was roughly similar, with BAM being more predictable but with less upside, and BN being less predictable but with potentially more upside.

Since then, fear surrounding commercial real-estate has escalated, negatively impacting Brookfield Corporation’s share price substantially. As a result, at the current price of around USD ~$31/share, BN is valued as if its entire real-estate portfolio (and insurance business) is worthless. Considering these businesses brought in $2.3B worth of cash flow in 2022, I find this hard to justify.

As a result, Brookfield Corporation has become more attractive than Brookfield Asset Management for investors able to wait for a re-pricing, that can bear volatility, and don’t require large dividend yields.

The Opportunity

There’s a famous study on cognitive bias that highlights the “Dilution Effect,” also knowns as the “Less-is-better Effect.” The quintessential example is when study participants were shown two sets of dinnerware and asked to name the highest price they’d pay for them. Both sets of dishes had the same number of functional items, but the second set included 8 broken items.

Participants were willing to pay 29% less for the second set that featured broken items than the first set which contained the same number of functional items but lacked broken items. In short , the presence of low-quality assets dilutes the perception of the value of the whole, despite nothing changing fundamentally. This is happening to Brookfield Corp.:

{kind=link}

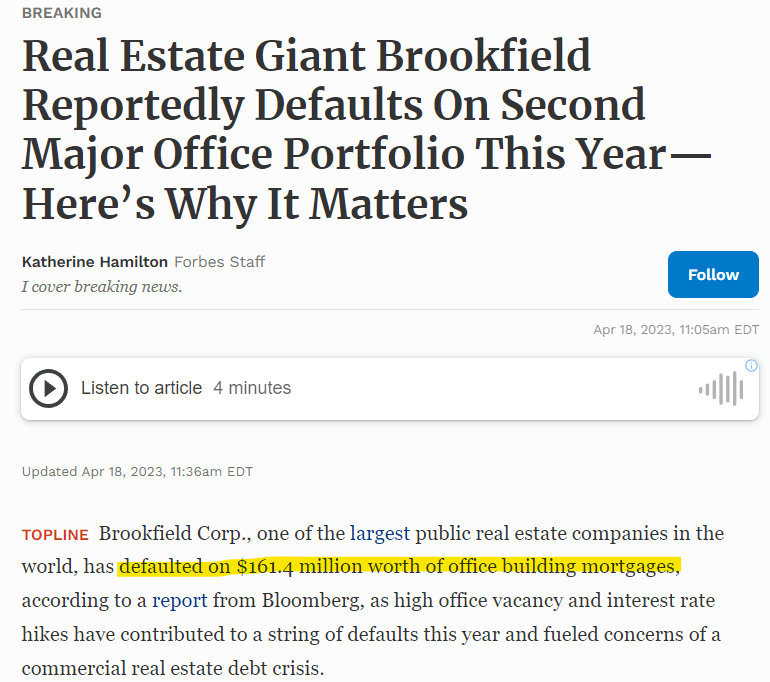

Looks terrible, a default on $161.4M. It’s just a broken plate though. Brookfield likely had very little actual equity in the buildings so are losing little by defaulting on unprofitable real-estate. The buildings are no longer Brookfield’s problem; their lenders are the ones holding the bag. If anything, it’s the banks investors ought to be worried about.

Additionally, low-quality real-estate is a relatively small portion of BN’s real-estate portfolio. In a recent interview, CEO Bruce Flatt suggested 5% of the real-estate portfolio was made up of offices like those being defaulted on, while rents in the high-quality properties in top-tier cities have increased 40% since COVID. It doesn’t feel great to buy broken plates, but if we are conscious of the Dilution Effect, we know that the presence of them doesn’t change the value of the whole.

It’s not easy to overcome the fallacy, however. To do so I find the following fact useful: Brookfield Corporation could default on 100% of the real-estate it owns, and still be undervalued .

I find that really puts the default of a few office buildings into perspective.

Sum of the parts

To demonstrate how little these office buildings matter to Brookfield, I present an updated sum-of-the-parts analysis that attempts to determine what is priced into the stock:

Apply your preferred multiple on the real-estate and insurance business' cash flow to determine the degree of undervaluation (Market Quotes, Company Supplemental)

My first observation is that to arrive at close to the current price we must exclude the value of the entire real-estate portfolio and insurance operations. If BN didn’t own any real-estate and didn’t underwrite anything it would be fairly valued, even at a slight discount to NAV.

But it does own real-estate, including some absolute gems in the downtowns of cities like New York, London, and Sydney. The insurance business is also expanding rapidly, having held cash when rates were low (something most banks didn’t have the wherewithal to do, resulting in the current crisis), and are now reinvesting at high interest rates rather than being in crisis. Combined they generated $2.3B of cash flow in 2023. In short, in attempting to discount the office defaults, the market discounted the entire real-estate portfolio, and insurance business to boot.

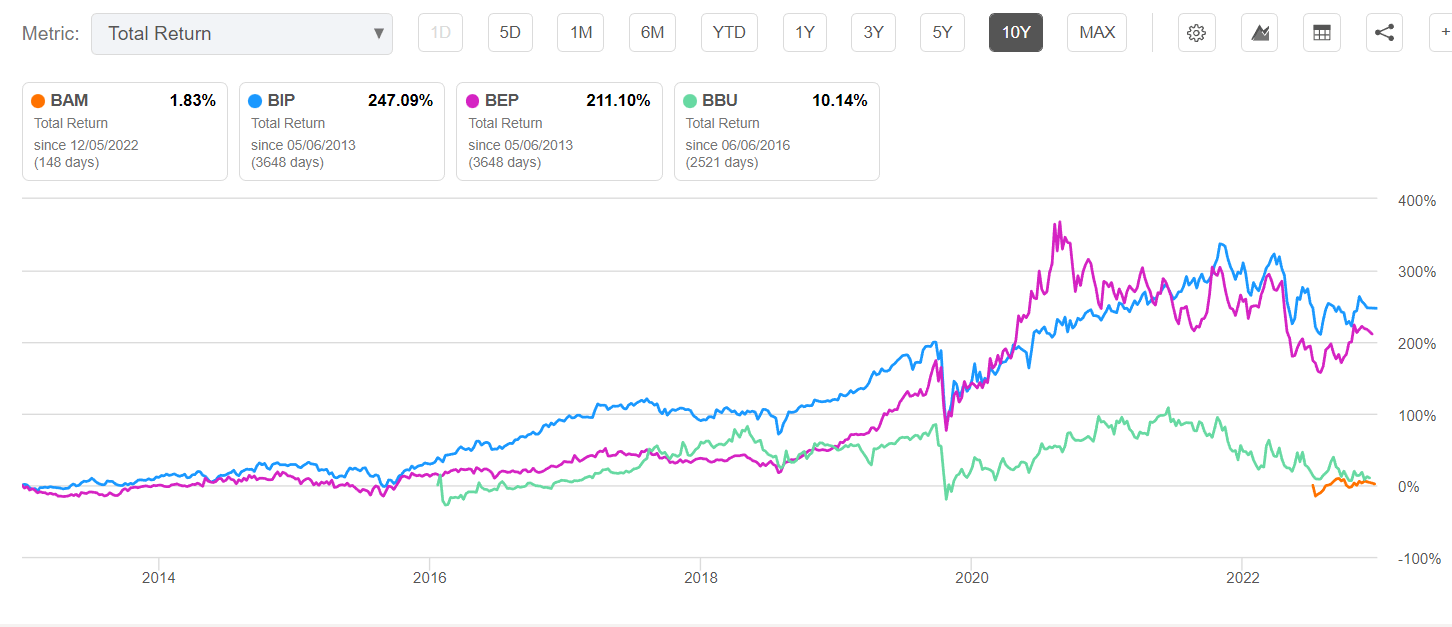

We could also challenge the Dilution Effect by looking at just the value of BN’s stake in its publicly traded entities, namely Brookfield Asset Management ( BAM ), Brookfield Infrastructure Partners ( BIP ), Brookfield Renewable Partners ( BEP ), and Brookfield Business Partners ( BBU ). Brookfield’s management is often criticized for overvaluing its assets, but with these entities the market is determining the value, so their valuations are confirmation bias-free. Net of cash, debt, and working capital, these entities are valued at ~$27/share, only 13% below the current price of BN.

The historic returns of Brookfield's publicly traded entities. If we allow ourselves a little optimism and say they are likely undervalued in the current market pessimism, just the shares BN owns in these is worth the ~$31/share BN trades at. (Seeking Alpha)

{kind=link}

Any way we parse it, whether by looking at BN’s publicly traded equity or its value ex real-estate and insurance, a lot is priced into BN shares.

Returns

To estimate returns, I arrived at a $47 NAV/share for BN by applying a 10x multiple to the cash flows from the insurance and real-estate business. I get the following possible returns:

Given that Brookfield is currently trading at ~40% discount to NAV (more if you want to be more aggressive) and the assumed discount to NAV in five years is only 15% (around the historical average), a fair amount of multiple expansion is implied in this valuation. (Author's Calculation)

For investors who have the time to wait for BN to be more fully valued, don’t mind a lower dividend yield, and can stomach short-term volatility, BN offers a very solid margin of safety with the potential for large upside should anything go right for Brookfield Corp.

On the other hand, investors who prefer to buy dinnerware sets without broken items can opt for Brookfield Asset Management; it has no offices, let alone equity of any kind, just simple fees that we need only apply a multiple to:

25x FRE seems high, but it works out to around a 4% dividend yield, which is the average for other stocks like it. (Author's Calculation)

If you believe management’s 2027 earnings projections, BAM looks like a great investment as well, especially if you like simplicity and dividends.

However, I believe BN has become better on a risk-reward basis. BAM must grow earnings at 15% for the next five years and trade at 25x those earnings for investors to receive a solid return. I don’t doubt it can do it (I own it as well), but high expectations are built-in, there is no more upside than this. Should growth be lower than expected or valuations decline, there is downside. BAM may be convenient, but it lacks a margin of safety.

Compare this to BN, from which 50% of its value is derived from the BAM shares it holds, but trades at a large discount. By owning BN we have significant exposure to BAM but with a margin of safety . In addition, we get world-class real-estate, a quickly growing insurance company, and much more. It might come with a few broken plates, but we shouldn’t let their presence dilute our perception of the value of the whole.

Conclusion

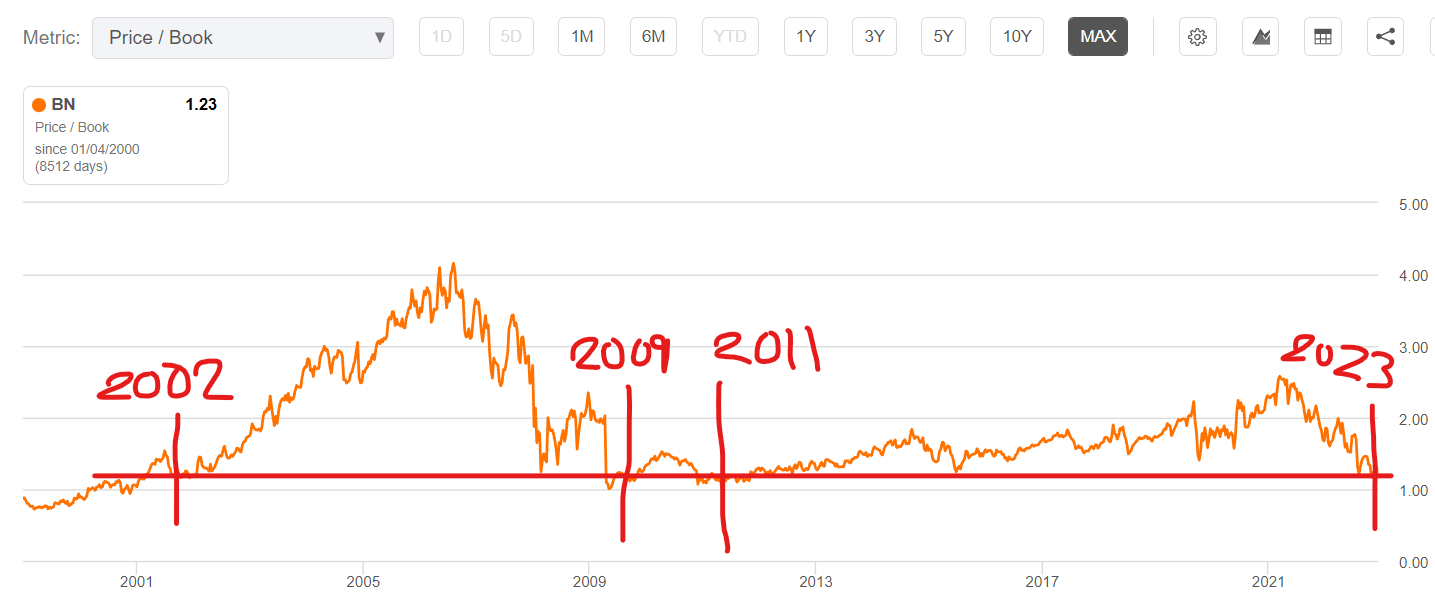

Brookfield Corp. has rarely been this cheap. In fact, the only other times it was this cheap on a price-to-book basis were 2002, 2009, and 2011, all of which were following crises and in hindsight excellent times to buy BN stock.

I find this graph illuminating, putting the opportunity into perspective. (Seeking Alpha)

{kind=link}

Significantly, Brookfield is even cheaper than it was when COVID began, we had no vaccine, and it seemed like the world was going to end. In 2020, offices were literally empty with no idea when or how they might be filled again, and BN was more expensive than it is now. The current hoopla over Brookfield Corporation’s commercial real-estate exposure doesn’t make sense.

Moreover, in the last 20 years Brookfield Corporation’s business has grown its asset management platform considerably, making a strong argument that BN should trade at a premium to its historical P/B, not at historical lows.

Brookfield's value is decreasingly correlated to its equity, as it generates an increasing amount of cash from fees that require limited equity. (Brookfield 2022 Supplemental)

The market is overreacting, and investors have a once-in-a-decade opportunity to take advantage.

For further details see:

Brookfield Corp.: Once In A Decade Opportunity