CA - Brookfield: Mind The Interest Rate (Rating Downgrade)

2023-10-29 03:21:10 ET

Summary

- Brookfield stock appeals to both value and growth investors due to its low multiples and high revenue growth.

- Rising interest rates pose a significant risk to Brookfield, as it has a large amount of debt, which incurs interest expenses.

- S&P Global has put Brookfield Property Partners under credit review, and threatened to downgrade its debt to 'junk.'

- If S&P Global downgraded Brookfield Property Partners' credit rating to junk, then Brookfield Corp would face a higher cost of capital going forward.

- Despite the risks, Brookfield's stock is still a decent buy due to its low valuation and growth potential.

Brookfield ( BN )( BN:CA ) stock is one of those rare names that has a following among value investors and growth investors alike. The stock trades at low multiples, yet it also has very strong growth in some of its subsidiaries. For example, its insurance subsidiary grew its earnings 245% in the most recent quarter. Its mix of value and growth characteristics has made Brookfield stock appealing to a great many investors.

However, BN stock is also subject to many risk factors, the most dangerous of which is rising interest rates.

Brookfield currently has $13.6 billion in corporate borrowings and $206 billion in borrowings at its managed entities. The 'managed entities' category includes both partially owned and wholly-owned subsidiaries. It is well known that Brookfield subsidiaries have been defaulting on some of their debts. Brookfield Property Partners risks having its credit rating downgraded to ‘junk’ because of these defaults. It’s true that Brookfield today enjoys an A- credit rating from Fitch, but its subsidiaries affect their parent’s earnings, and their ratings affect Brookfield’s cost of capital.

More to the point, Brookfield’s large amount of debt incurs significant interest expenses that are eating into the company’s earnings. In the most recent quarter, Brookfield delivered $1.5 billion in net income, down from $2.9 billion–an 85% decline. A major contributor to the decline in GAAP earnings was a large jump in interest expense, which increased $1.4 billion, from $2.1 billion to $3.5 billion. Some of the jump in interest expense came from new borrowings to finance deals, but the biggest single category responsible for the jump was rising interest rates on existing variable rate debt. We would expect that debt to take a bite out of earnings when Brookfield reports on November 9 .

When I last covered Brookfield, I rated the stock a ‘ strong buy ’ on the grounds that it had high quality assets, was cheap, and enjoyed significant protection from the effects of interest on its non-recourse debt. Today, I still consider Brookfield stock a buy, but with somewhat less conviction than before.

After an extensive review of the company’s debt, I’ve come to the conclusion that Brookfield is not totally shielded from risk, chiefly the possibility of higher rates on variable rate debt. While it is true that only a small proportion of Brookfield’s lenders have recourse to the company’s assets, a significant percentage of the company’s debt is made up of corporate borrowings at Brookfield subsidiaries. In other words, it’s not all “property specific.” If S&P Global ( SPGI ) downgrades Brookfield Property Partners’ debt because of its defaults , then Brookfield as a whole will face higher costs of capital when doing real estate deals, compared to the costs it incurred in the past. So, Brookfield’s debt is a non-negligible risk factor for the company. On the other hand, BN stock is cheap enough at this point that a significant amount of the potential damage is already baked into its price. Factoring in both the risks and the valuation, I still consider BN a buy today.

How Much Does Brookfield Owe?

The reason why Brookfield’s debt situation is tough to wrap one’s head around is because the company’s corporate debt is separate from the debt held by its subsidiaries, as well as that tied to specific properties. The company often touts the fact that it has only a small amount of corporate debt, and that only the corporate debt holders have recourse to the corporation’s total assets. This is technically true, but some of Brookfield’s “non-corporate” debt is the debt owed by subsidiaries–some of them wholly owned–and therefore has recourse to the subsidiary’s assets. By my estimate this type of debt makes up around 8% of Brookfield’s total debt. In the ensuing paragraphs I’ll explain how that breaks down.

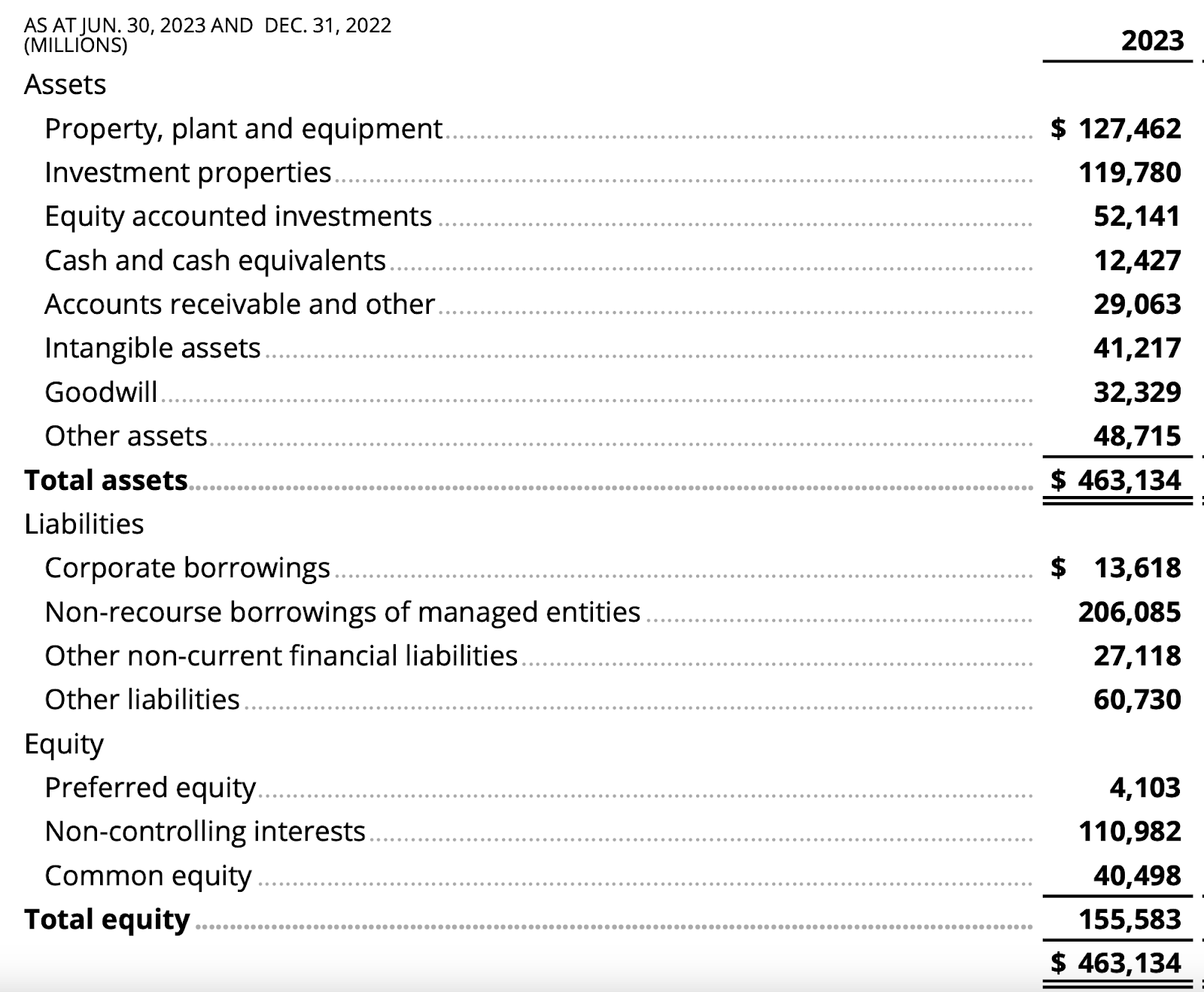

To begin, let’s look at Brookfield Corp’s financial statements. These list three categories of debt-like liabilities:

-

Corporate debt - $13.6 billion at 4.2% interest.

-

Preferred shares: $4.3 billion at 4.6% interest.

-

Non-recourse borrowings of managed entities: $206 billion, variable interest rates.

Brookfield Balance Sheet (Brookfield)

{kind=link}

If we lump all of Brookfield’s different types of debt together and subtract the total from assets (along with non-controlling interests), we still get $41 billion in common equity, or $40 billion if we count the preferred stock as a liability. The debt to equity ratio resulting from this exercise is 5.25, which is extremely high. However, if we use total equity in place of common equity, we get a 1.4 debt/equity ratio, which is only moderately high. As I’ll show shortly, it’s not Brookfield’s debt/equity ratio that is the real problem, but the potential for interest on the company’s debt to increase–with or without additional borrowings.

Brookfield’s Interest Expenses

Knowing the structure of Brookfield’s debt obligations, we can now proceed to a discussion of how the debt will affect the company’s future profits. I’ll start by looking at the effects of the interest rates, and then proceed to examine what percentage of the debt could become a burden to Brookfield at a corporate level.

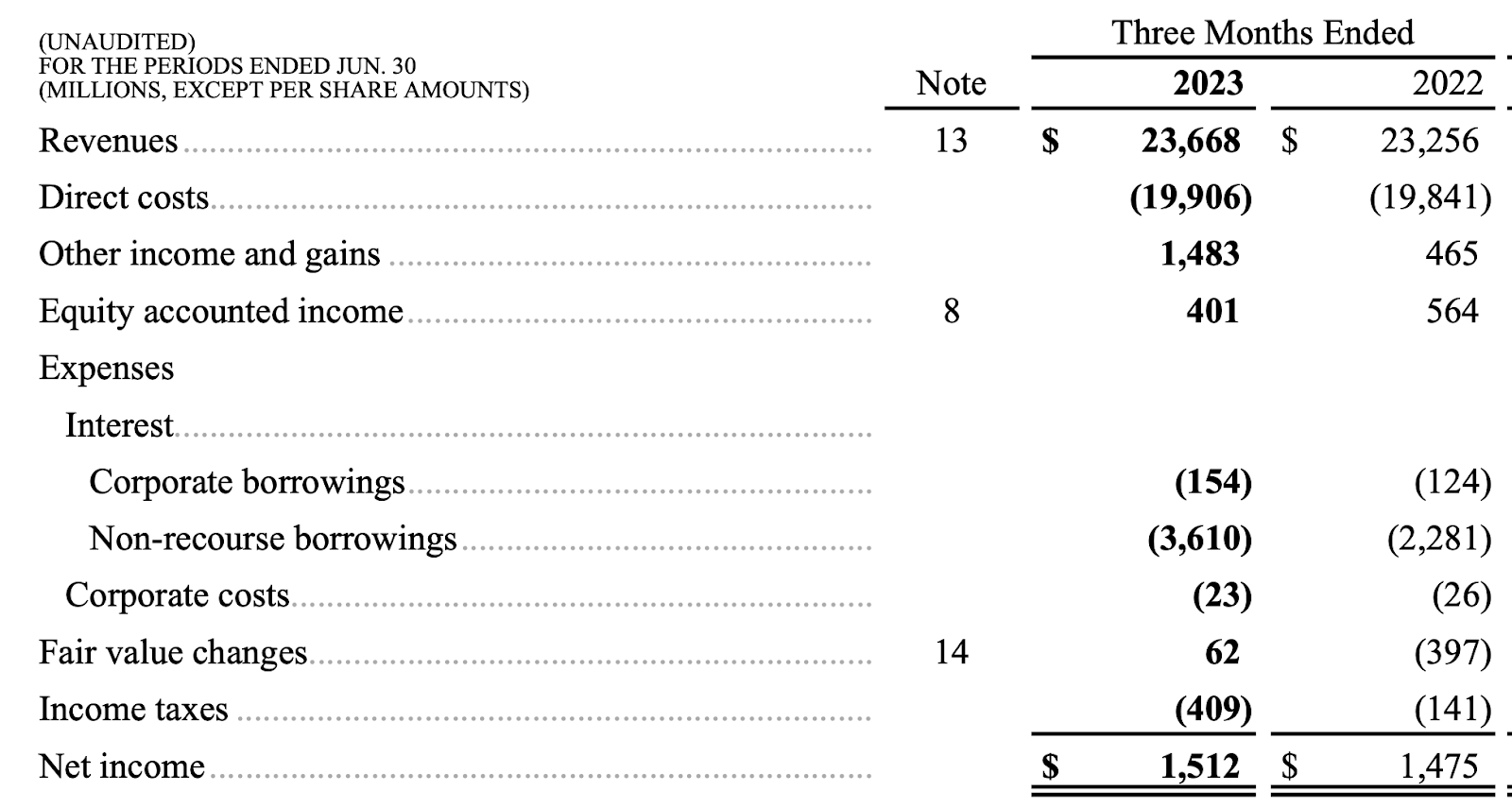

The interest expense resulting from all of Brookfield’s combined debts was $3.75 billion last quarter, or 188% of EBIT (calculated as $1.512 billion in net income plus $409 million in income tax). According to Brookfield, 76% of its debt is fixed rate.

Brookfield Q2 earnings (Brookfield)

{kind=link}

As shown previously, Brookfield’s interest expenses increased $1.4 billion last quarter. $879 million of that increase–the majority of it–was due to higher rates on variable rate debt. This would imply that another two quarters with increases in variable rate interest expense comparable to the one seen in Q2, would turn Brookfield’s net income from a positive figure into a loss. Not only that, but only $81 million of the $1.512 billion in Q2 net income was attributable to common shareholders. So, it looks like Brookfield’s variable rate debt has the potential to reduce its profitability significantly. Granted, the company’s distributable income–the type of income that determines how much it can pay out in dividends–is much higher than its GAAP net income. That figure was $1 billion–higher than net income to shareholders, but lower than net income to the firm. Again, two more quarters of $879 million cost increases would more than cause all of that profit to disappear.

Now, I don’t find it likely that Brookfield’s variable rate interest expense will increase by $879 million once more. Remember, corporate financial statements compare the current period to the same period a year before–so Brookfield gained $879 million in interest expenses through the entire 2022/early 2023 period of aggressive rate hiking, not from Q1 to Q2. Interest expenses may rise, but not by $879 million per quarter.

The ‘Non-Recourse’ Topic

Having discussed the matter of Brookfield’s interest expense, we can now explore how exposed Brookfield itself is to all of this debt. Brookfield’s executives like to point out that the company’s debt is mostly non-recourse and property specific. It is true that only a small $13.6 billion sliver of Brookfield’s total debt is at the level of Brookfield the company, but not all of the remainder is tied to specific properties. Some of it is subsidiary-level corporate borrowing.

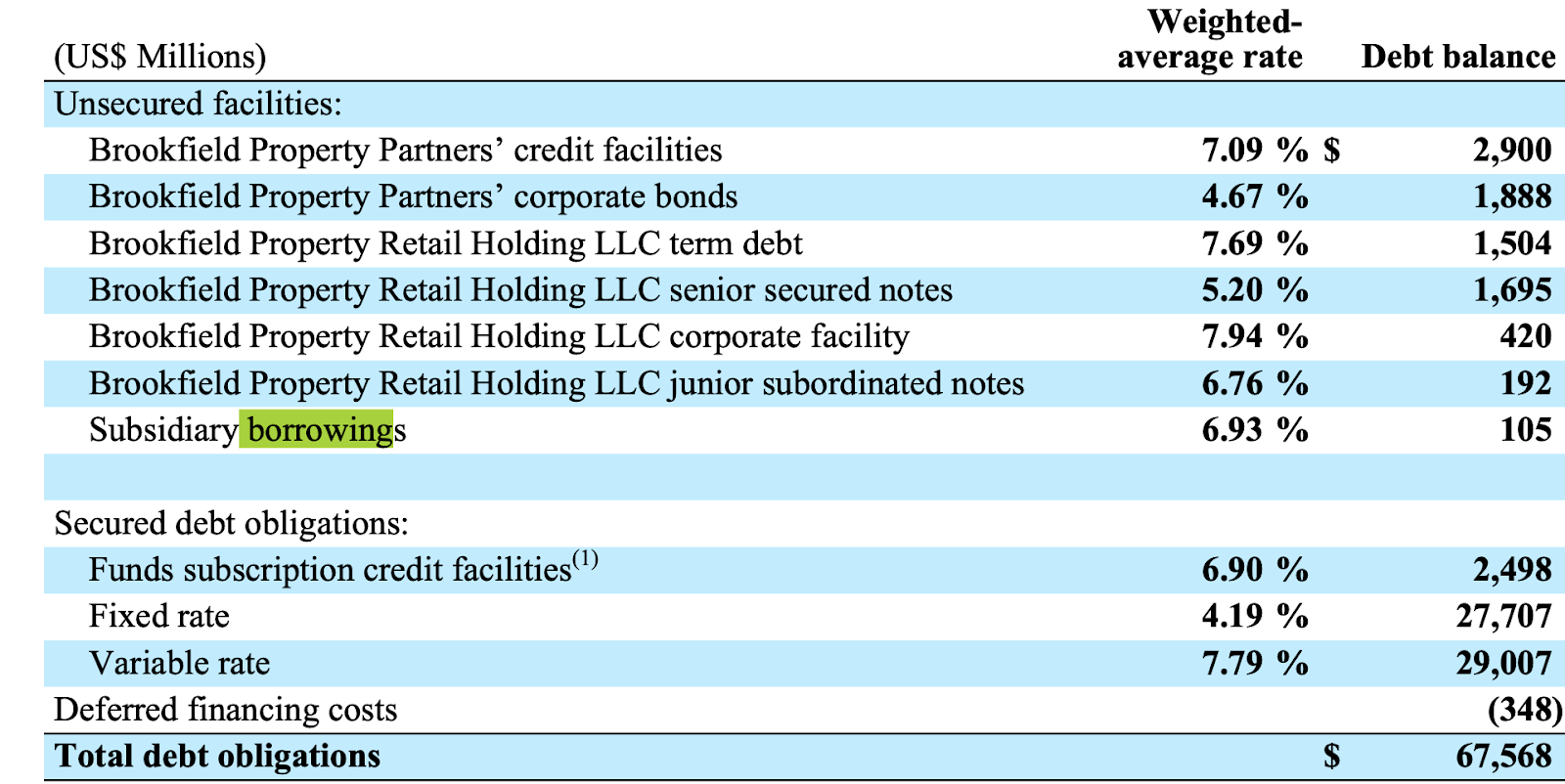

According to Brookfield’s Q2 earnings release, about $16 billion of the “non-corporate borrowing” is subsidiary borrowings. $4.7 billion of that is corporate level Brookfield Property Partners debt–the remainder of that company’s debt (everything with “Brookfield Property Retail Holding” attached to its name) is likely property specific. In the table below, you can see two bonds/LOCs that are corporate-level Brookfield Property Partners ( BPY ) borrowings, and $67 billion in total BPY debt. Apart from the $4.7 billion in subsidiary-level debt at BPY, there is also $11.3 billion from other Brookfield entities. Brookfield Asset Management ( BAM ) has only $930 million in total liabilities, and is not part of Brookfield’s debt problems, as it hasn’t defaulted on anything.

Brookfield Property Partners borrowings (Brookfield Property Partners)

{kind=link}

S&P Global recently put Brookfield Property partners under credit review . The company’s debt is already at the lowest investment grade rating, and could be downgraded to junk. This is a wholly owned Brookfield subsidiary, so every penny of its debt is also Brookfield’s debt. That means that $67.5 billion out of Brookfield’s $223.6 billion in total debt could face higher costs when it has to be refinanced.

So we have two potential sources of increased interest expense at Brookfield: the 26% of its debt that is variable rate, and the 30% attributable to BPY that will be financed at higher rates if BPY’s rating is downgraded to junk. True, the vast majority of BPY’s debt is non-recourse, but $4.7 billion of it is corporate-level (i.e. owed by a corporation that is a Brookfield subsidiary), and $16 billion out of Brookfield Corp’s $210 billion in “non-corporate non-recourse debt” is in fact corporate borrowings at various subsidiaries. So we have between 30% and 56% of Brookfield’s debt that could see its interest expense rise either from variable rate increases or refinancings (the exact percentage depends on the overlap between BPY debt and Brookfield Corp’s variable rate debt), and another $16 billion that has recourse to assets beyond just individual properties. So a significant percentage of Brookfield’s debt could cause problems for the company in one form or another.

Valuation

As we’ve seen, Brookfield Corp’s debt has the potential to cause serious problems for the company. Namely, it has the potential to increase the company’s interest expenses, and cause a credit rating downgrade for BPY. This is a serious risk; in my opinion, a more serious risk than Bruce Flatt’s public statements would have you believe. Nevertheless, I still consider the company’s stock a buy at today’s prices.

The reason is that Brookfield owns many good assets, and its rock-bottom valuation now ‘prices in’ a significant amount of trouble.

At today’s prices, Brookfield trades at :

-

18 times estimated forward earnings.

-

0.51 times sales.

-

1.21 times book value.

-

7.3 times operating cash flow.

These are pretty low multiples. Additionally, I worked out from earnings releases that BN had $2.91 in funds from operations per share in the trailing 12 month period. If you assume no growth and simply discount that at 10% (the five year treasury plus a 5% risk premium), you get a $29.10 price target, about the same as today’s share price.

Now, this “no growth scenario” does not give us actual upside here. But consider that Brookfield:

-

Owns “trophy” properties whose rental income is stable .

-

Has an insurance business that grew 245% last quarter

-

Owns 67% of the extremely well-regarded Oaktree Capital management, which has delivered 19% CAGR returns (net of fees) for its clients.

-

Owns 75% of BAM, which has a 53% net margin .

-

Bought AEI for $4.3 billion, which is only $300 million or 7.5% higher than a $4 billion offer AEI executives said “ undervalued ” the company.

This is quite an impressive collection of assets, which provides hope that BN may be able to start growing again in the future if it can keep its interest rate exposure under control. Over the last five years, Brookfield and its predecessor company have grown revenue at 12.7% CAGR . If the company could grow its distributable earnings at that pace, then the discounted cash flow exercise above would produce a $48.51 price target, implying significant upside. Management believes that it can hit a 36% growth rate in carried interest from now until 2028. That would produce a measurable impact on the company’s overall distributable earnings growth. While I can’t say that I fully endorse Brookfield’s own assessment of its growth potential, I think it could reasonably hit the low double-digit growth it needs to be worth the investment at today’s price. So, I continue holding BN, though with less conviction than before.

For further details see:

Brookfield: Mind The Interest Rate (Rating Downgrade)