CA - BSR REIT: Cheap But Not Much Cheaper Than Sunbelt Multifamily Peers

Summary

- BSR is a multifamily REIT that owns affordable, Class B suburban apartments, primarily in Texas.

- BSR has strong management and a strong balance sheet, but so do its larger, US-listed peers.

- BSR suffers the disadvantage of not being listed on a US exchange and not having an in-house development arm like some of its larger peers.

- The REIT does look slightly cheaper than those larger peers, but not enough to make it the best pick in the space.

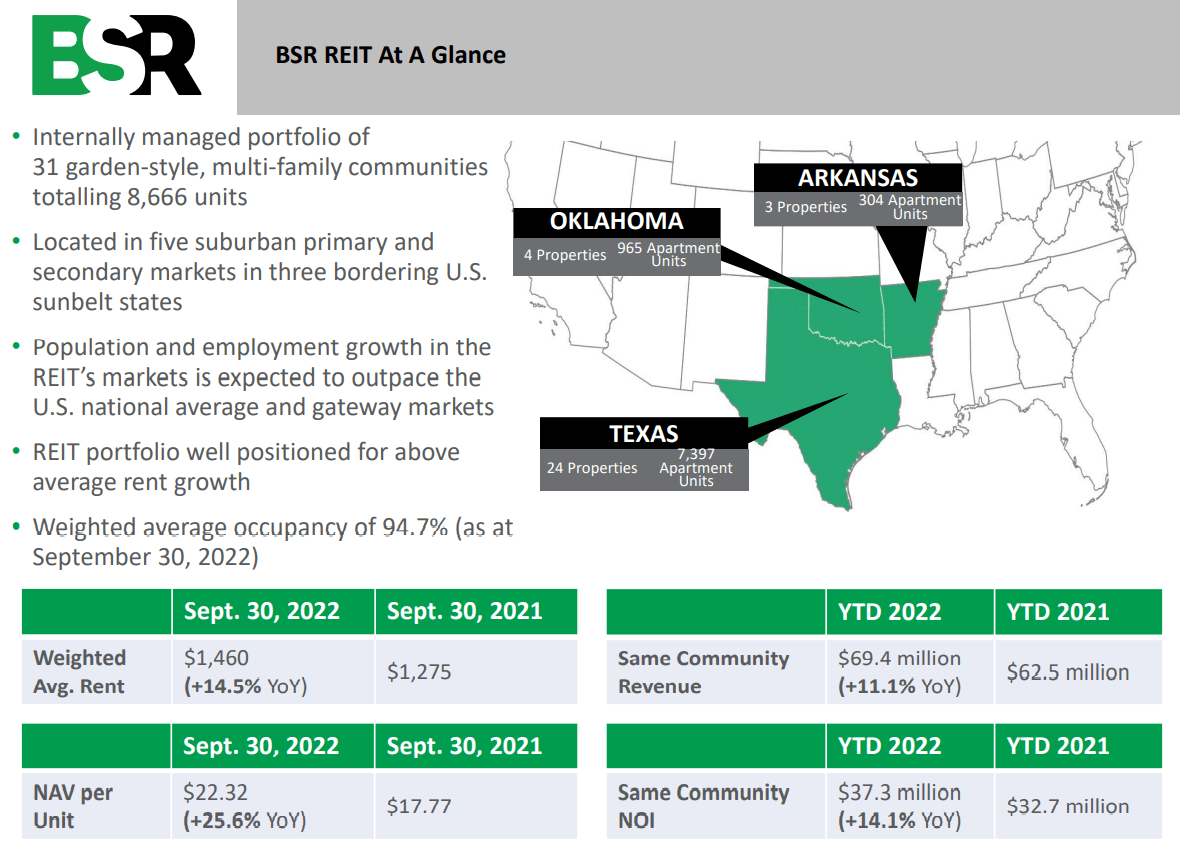

BSR REIT (BSRTF) is a multifamily real estate investment trust ("REIT") that owns Class B, garden-style, suburban apartment communities in three Southern States, primarily Texas. This is essentially workforce housing for middle-income individuals and families, with a median income of incoming residents in Q3 2022 of $84,000. But given BSR's weighted average rent rate of $1,460 per month ($17,520 per year), the REIT's portfolio rent-to-income ratio sits at a mere 21%.

Moreover, the internal management team is long-tenured and strongly shareholder aligned with heavy insider ownership, and the balance sheet strong with debt to gross book value of 34% and 100% of debt fixed or hedged at a weighted average interest rate of 3.4%.

BSR trades at a discount to its own net asset value ("NAV"), although its price/FFO is roughly in line with its peers.

Compared to NAV per share of $22.32 in Q3 2022, BSR's current price of $14.28 trades at a 36% discount. Although the price to estimated 2023 FFO and dividend yield is roughly in line with its closest peers:

| Price / FFO (2023e) |

| Dividend Yield |

| BSR REIT |

| 16.0x |

| 3.6% |

| Mid-America Apartment ( MAA ) |

| 17.1x |

| 3.6% |

| Camden Property Trust ( CPT ) |

| 16.1x |

| 3.3% |

| NexPoint Residential ( NXRT ) |

| 13.7x |

| 3.7% |

BSR does look attractive at its current price, but it does not necessarily look any more attractive than its peers. In fact, at this point, as BSR's portfolio metamorphosis is complete, its larger peers MAA and CPT look more attractive given their internal development arms. And NXRT also looks more attractive with its strong track record of value additions and capital recycling.

Unless one specifically wants exposure to Texas Class B apartments, MAA would be my pick for the best buy for a sleep-well-at-night Sunbelt multifamily REIT, and NXRT would be my pick for a higher risk, higher reward strategy focused on the same asset type.

BSR REIT Vs. Peers

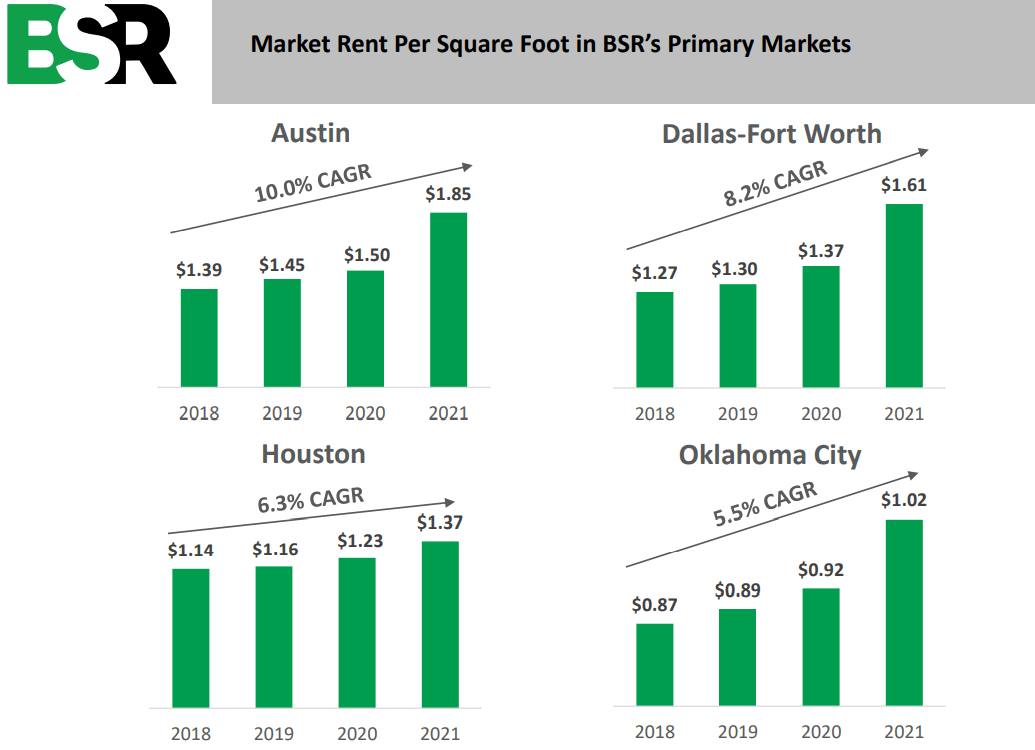

BSR's portfolio of mid-tier, affordable apartments is located overwhelmingly in Texas, especially Houston, Dallas/Fort Worth, and Austin. These were fast-growing markets before the pandemic, but their growth only accelerated over the last several years during the COVID-era population reshuffling.

{kind=link}

These three cities, and to a lesser extent BSR's 4th largest market of Oklahoma City, have seen strong rent growth in the last five years.

{kind=link}

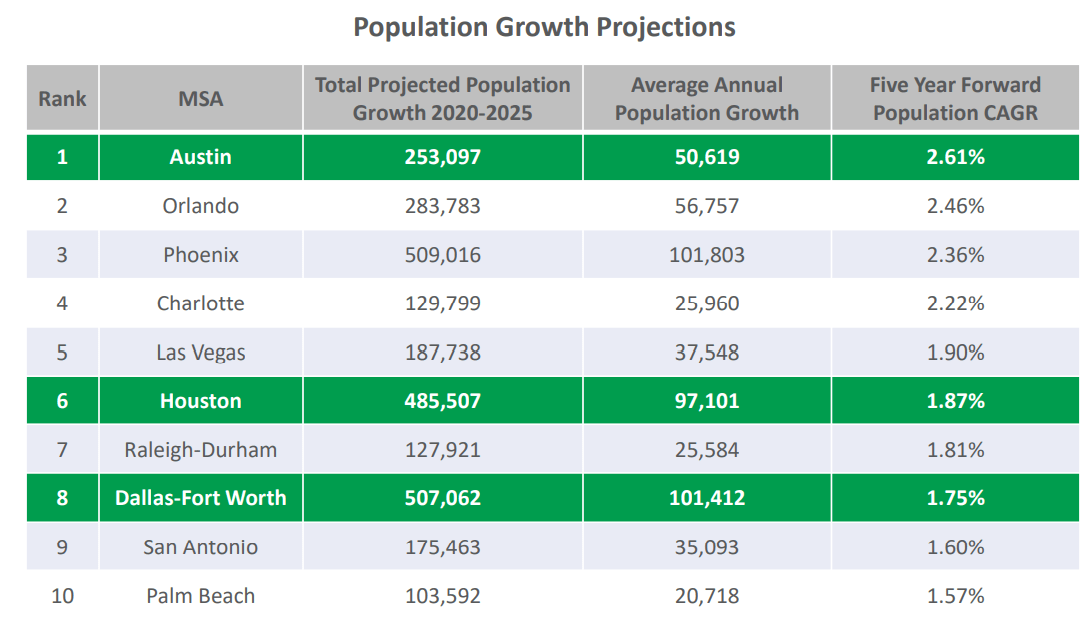

Generally speaking, rent growth flows from population and job growth, because the growth in new supply of apartments typically lags the growth in people and jobs.

Here are population growth projections from Oxford Economics for the five years from 2020 to 2025, showing the top 10 fastest growing markets by percentage growth rate:

{kind=link}

What do all 10 metro areas have in common? They are all located in the Sunbelt.

BSR's three core markets in Texas are certainly well-positioned within this top ten list, but so are the top markets of BSR's Sunbelt multifamily REIT peers.

For example, 6 out of MAA's top 10 markets are in the above list of fastest growing cities. The same is true of CPT's top 10 markets, although the mix of cities is slightly different. Meanwhile, 7 of NXRT's 11 total markets on the Oxford Economics list of fastest growing cities.

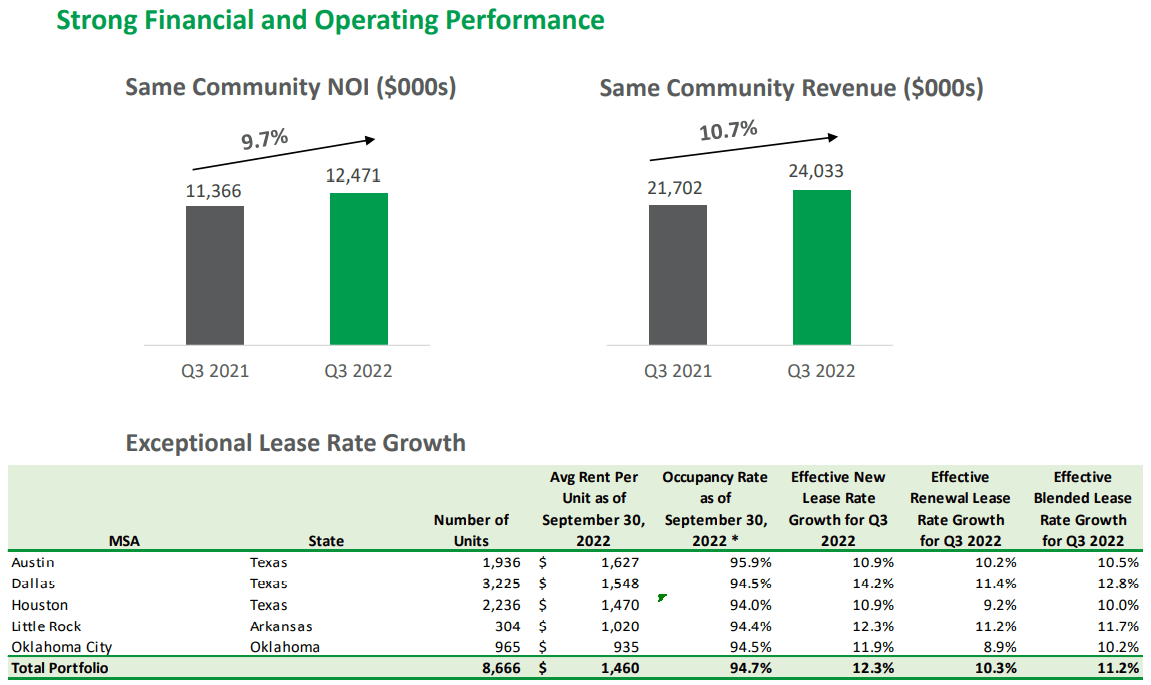

With such strong population growth in Texas, BSR has naturally enjoyed strong rent and NOI growth as well:

{kind=link}

But BSR's peers have been enjoying similarly strong rent and NOI growth. In fact, in the third quarter of 2022, BSR turned in the lowest same-property NOI growth of any Sunbelt multifamily REIT.

| Q3 2022 |

| Same-Property NOI Growth |

| Rent Growth |

| BSR REIT |

| 9.7% |

| 14.5% |

| Mid-America |

| 17.4% |

| 14.6% |

| Camden |

| 16.3% |

| 11.7% |

| NexPoint |

| 13.1% |

| 15.0% |

It should be noted that 9.7% YoY same-property NOI growth is nothing to sneer at! But at least in this case, Sunbelt multifamily peers' diversification outside of Texas proved a strength rather than a weakness.

Another potential weakness of such a high concentration in Texas, as I discussed in " American Homes 4 Rent: A Sunbelt SFR REIT Doing Its Part To Alleviate The Housing Shortage ," is the risk of higher property taxes than other states.

The state of Texas has no income tax, so in lieu of that, property taxes are higher. The state government appears to be targeting single-family rentals in particular, but the state might also look to garner its share of rent growth in the form of higher taxes on multifamily landlords as well.

As such, BSR's incredible run from early 2021 through the Spring of 2022 is unlikely to be repeated in the near future, unless interest rates drop back to near-zero levels.

Unless interest rates decline considerably or cap rates rise considerably, BSR's cost of capital makes further acquisitions unattractive. That is why the REIT has turned to share buybacks (along with NXRT) instead of investing in new properties.

Let's take another look at BSR's valuation compared to peers, this time using 2022 AFFO or core FFO per share:

| Price to AFFO/Core FFO (2022) |

| BSR REIT |

| 17.9x |

| Mid-America Apartments |

| 20.3x |

| Camden Property |

| 19.7x |

| NexPoint Residential |

| 13.0x |

BSR is cheaper than MAA or CPT, but there is a good reason for that. Both MAA and CPT have in-house development arms capable of delivering new properties at stabilized NOI yields at least 100 basis points higher than market cap rates.

In short, then, while BSR does look cheap, it does not look cheap enough relative to peers (given their specific strengths) to make it preferable to those peers.

That is especially true given the limited options American investors have to invest in BSR - either over-the-counter via BSRTF or on the Toronto Stock Exchange, if one's brokerage service gives that option. Some brokerages, like Vanguard, do not allow investors to purchase BSRTF at all.

To my knowledge, there are no signs that BSR is likely to become listed on a major US exchange anytime soon, which means that it is unlikely to become included in US REIT indexes anytime soon either. If BSR did become listed on a US exchange, I would see that as a catalyst for better stock price performance than peers, but in lieu of that it does not appear to be much more attractive than those peers.

My top picks in the multifamily REIT space are MAA and NXRT for the reasons stated above. Although I do believe BSR should perform well from its current level as well.

For further details see:

BSR REIT: Cheap, But Not Much Cheaper Than Sunbelt Multifamily Peers