CA - BTB REIT: A Well-Covered 8% Yield But Balance Sheet Concerns Are Real

Summary

- BTB REIT focuses on industrial, office and retail assets.

- The monthly distribution of C$0.025 per share is well-covered thanks to the AFFO of in excess of C$0.40 per share.

- BTB is attractive from an AFFO multiple and yield point of view.

- The LTV ratio on the balance sheet comes in around 60%, and that's a bit too high for me.

- As soon as the REIT takes action to reduce the LTV ratio, I could be very interested.

Introduction

BTB REIT ( BTB.UN:CA ) ( BTBIF ) is a Canadian REIT focusing on managing industrial, office and necessity-based retail assets in certain Canadian provinces. Headquartered in Montréal, it's not a surprise to see about 75% of the leasable area is located in the province of Québec, with Ontario coming in as distant second with just over 18% of the leasable area (as of the end of 2021). As of the end of the third quarter of 2022, just over 20% of the leasable area was classified as necessity-based retail while off-downtown core office buildings represented almost half of the leasable are.

{kind=link}

BTB has its primary listing in Canada, and as that clearly is the most liquid listing and as BTB reports its financial results in Canadian Dollar, I will refer to that listing in this article. Unfortunately, as of the time of writing this article, the 'English' button on the BTB website does not work and all documentation is in French. Readers can find all relevant information in English on the SEDAR website .

While the FFO and AFFO remain strong, the balance sheet will need some attention

BTB isn't a big REIT. The total amount of assets on the balance sheet are just over C$1.2B while the REIT generates approximately C$30M per quarter in rental revenue.

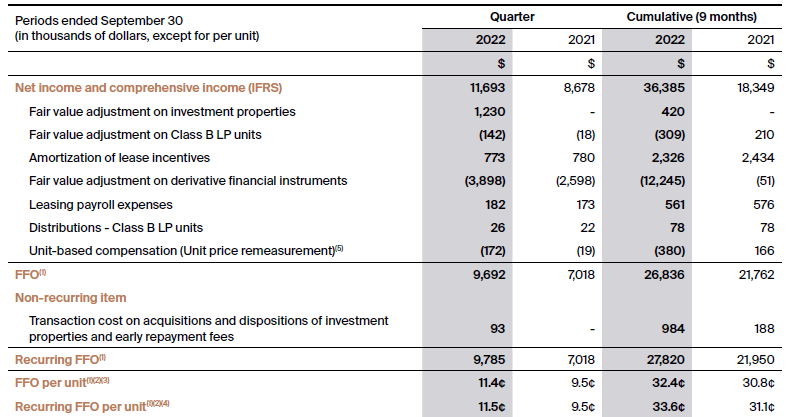

Looking at the REIT's Q3 results, we see the total net income came in at C$11.7M but this result was fueled by a positive impact of the fair value adjustment of derivatives to the tune of almost C$4M. That is obviously not an element that should be taken into consideration in a FFO calculation, and that contribution was removed from the equation. The total FFO result during the third quarter came in at C$9.7M while the recurring FFO was C$9.8M or C$0.115 per share.

{kind=link}

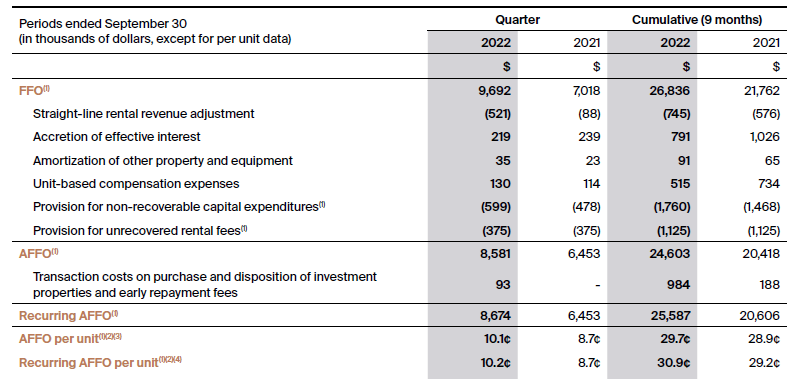

That was a good result, but as BTB REIT has quite a few office buildings in its portfolio, I think the AFFO result is a better metric.

As you can see below, the starting point is the FFO result and the total amount of adjustments is just C$1.1M. I am pleasantly surprised the capex is pretty low at just C$0.6M and this helped to report an AFFO of C$8.6M and just under C$8.7M on a recurring basis.

{kind=link}

The recurring AFFO was approximately C$0.102 per share, and the recurring AFFO in the first nine months of 2022 came in just below C$0.31. This means a full-year AFFO of just over C$0.40 appears to be a given.

That would indicate the stock is currently trading at just 9.5 times the AFFO, and it also means the current distribution of C$0.025 per month is pretty well covered as the payout ratio based on the recurring AFFO will likely come in below 75%.

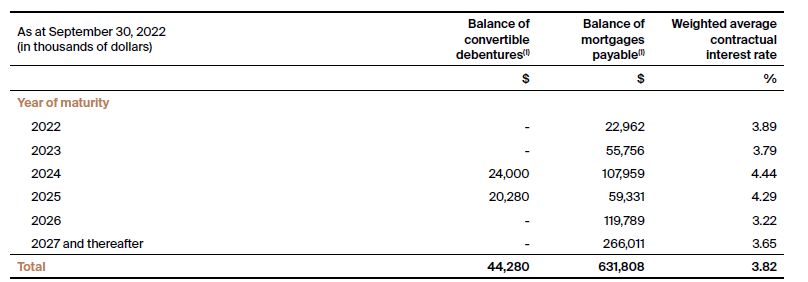

I was also very interested to see how the increasing interest rates on the financial markets would impact BTB's FFO and AFFO. The REIT has approximately C$632M in mortgages payable (based on the situation as of the end of the third quarter). Fortunately in excess of 90% of the mortgages have a fixed interest rate or a floating interest rate that has been hedged. As of the end of Q3 2022, the total amount of unhedged and floating loans was just C$45M.

{kind=link}

This means we shouldn't see any sudden shocks but we should be mentally preparing for BTB having to pay much higher interest rates when mortgages have to be refinanced. This calendar year, in excess of C$55M in mortgages will have to be refinanced and a 150 basis point increase would increase the interest expenses by almost C$1M per year. That's still fine, but then in 2024 another C$108M in mortgages (and C$24M in debentures) will have to be refinanced, so we will likely see a continuous increase in the interest expenses over the next few years. Fortunately these gradual increases indicate BTB has a good chance to mitigate the impact by hiking the rent. Although this likely means the AFFO growth will be pretty weak in the next few years (if there even is any growth), but I am confident BTB REIT can avoid sudden shocks - on the condition it can keep the occupancy ratio at its current levels.

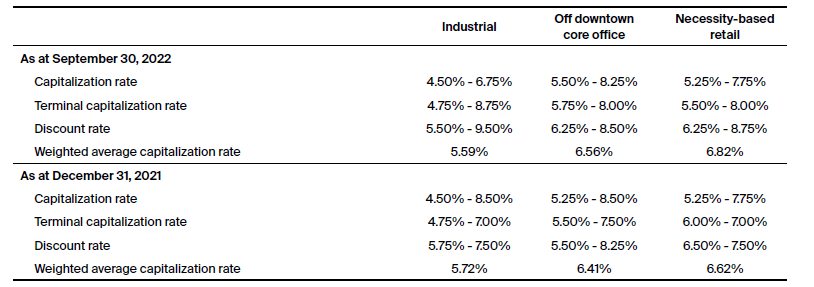

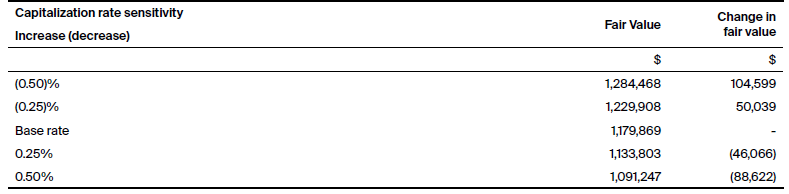

The book value of the assets was C$1.18B as of the end of September, and considering the NOI was C$18M in Q4 and we can likely expect a full-year NOI of C$70M and perhaps a small increase of a few million dollar. The weighted capitalization rates for the assets were established at 5.59% for the industrial assets, 6.56% for the office assets and 6.82% for the retail assets.

{kind=link}

It's hardly a surprise to see increasing capitalization rates in the majority of the asset classes, but I admit I was a bit surprised to see the capitalization rates in the industrial portfolio decreased. When BTB REIT publishes its full-year results, I will be focusing on the remaining lease terms across the portfolio as I think that could be a key element in determining how attractive BTB is.

I'm not too worried. The sensitivity analysis indicates that applying a 50 basis points increase in the capitalization rate, the fair value of the assets would decrease by less than C$90M. And even at that C$1.09B (which excludes the impact of rent hikes and a higher NOI).

{kind=link}

As of the end of September, BTB had C$10M in cash, C$630M in mortgage debt, C$37M in bank loans and C$42M in debentures outstanding. This means the net debt level was C$699M resulting in an LTV ratio of 59%. And that is the main reason why I don't have a position in BTB. Even at the current payout ratio and assuming C$9M per year is retained on the balance sheet, the LTV ratio decreases by less than 1% per year. That's too slow and if we would see a C$90M value decrease if a higher capitalization rate would have to be used, the LTV ratio would immediately increase to 64% and that's alarmingly high.

Investment thesis

The high LTV ratio is the main reason for me to stand on the side lines. There's a reason why the stock is trading at just over 9 times the AFFO. The dividend yield is very appealing and well-covered, but I personally just don't feel comfortable enough to entertain an LTV ratio of almost 60%. The REIT sold two assets in December for a total of almost C$11M, but it recycled those proceeds to purchase a C$28M industrial property so I expect the LTV ratio to still come in around 60% once the full-year results will have been published.

The REIT also has two series of convertible debentures outstanding but I haven't made a decision yet.

For further details see:

BTB REIT: A Well-Covered 8% Yield, But Balance Sheet Concerns Are Real