CA - BTB REIT: A Whopping 10% Yield But Balance Sheet Concerns Remain

2023-06-26 10:30:00 ET

Summary

- BTB REIT is rotating from offices to industrial properties - I think that's a good move.

- The distribution is very well covered by the AFFO: the payout ratio will likely be less than 75% this year.

- The balance sheet with an LTV ratio of close to 60% is the only worrisome factor.

Introduction

Back in February, I had a ‘hold’ on BTB REIT ( OTC:BTBIF ) ( BTB.UN:CA ) as I wasn’t convinced the REIT’s balance sheet was strong enough to get through the choppy waters we are currently experiencing. BTB was cheap based on the AFFO multiples, but thanks to the rather generous dividend policy, I feared the REIT’s balance sheet wasn’t getting sufficiently stronger. Since that article was published, the stock is down by in excess of 20% and the drop accelerated in the past few days so I thought an update would be a good idea.

The Q1 results: a strong recurring AFFO

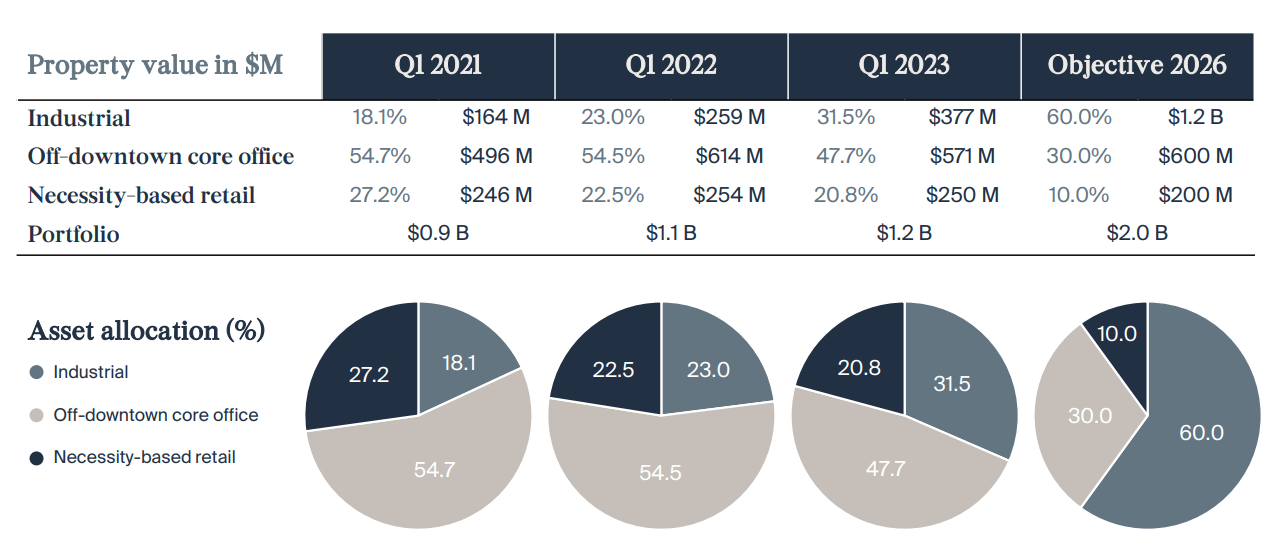

First of all, I think BTB is making the right decision by moving away from being a (predominantly) office REIT towards becoming an industrial REIT. In the past two years, the weight of industrial assets in the portfolio has almost doubled, but unfortunately the office segment remains a very important portion of the total asset base as about 48% of the C$1.2B in assets is still contributed by the office portfolio.

{kind=link}

Fortunately, BTB plans to reduce this pretty fast. Within the next three years, the total weight of the industrial assets should increase to 60% while the office and retail segment should decrease to 30% and 10% respectively. I like those targets but I’m also wondering if BTB is perhaps (a bit too) late to the party when it comes to industrial assets as valuations have held up pretty well in that segment.

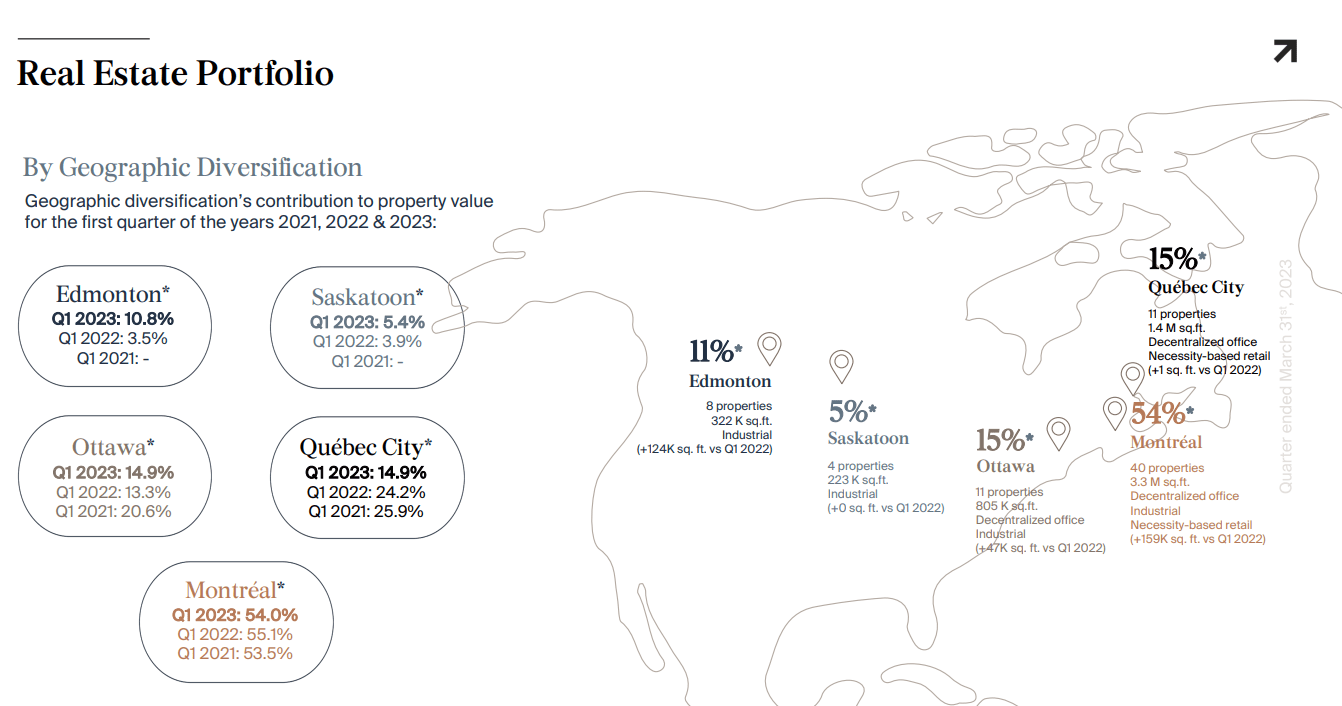

The REIT is focusing on Eastern Canada with Quebec City and Montreal accounting for about 70% of the total property value.

{kind=link}

In my February article, I was fine with the REIT’s earnings performance as BTB was able to report pretty strong FFO and AFFO results. That’s a good start to improve the balance sheet as ‘retaining earnings’ is one of the easiest ways to add some meat to the bone. Of course the shareholders also require a dividend so the REIT has to walk a thin line between keeping the shareholders happy and strengthening its balance sheet.

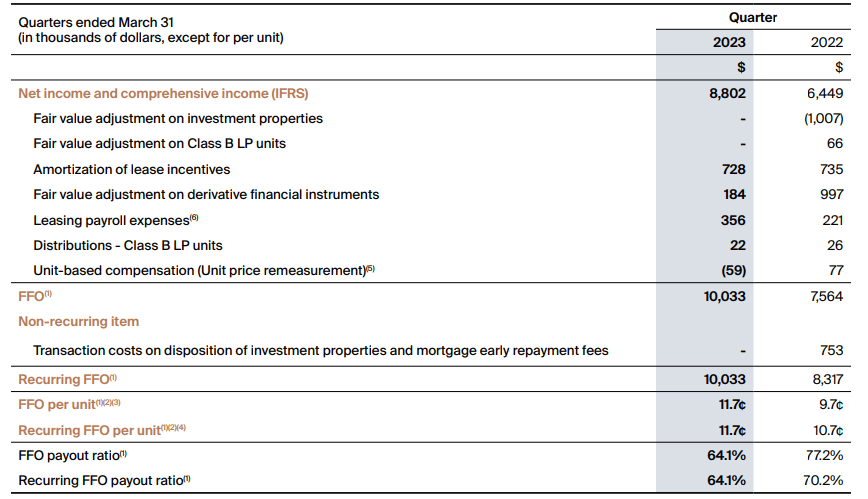

Before diving into the FFO and AFFO calculations, I’d just like to note the interest expenses have increased by approximately C$0.7M in Q1 2023 compared to Q1 2022.

The Q1 2023 FFO was pretty strong . The starting point was the C$8.8M net income and after making the relevant adjustments, the quarterly FFO came in at C$10M. Divided over the 86 million outstanding units (including the impact of the Class B units that can be converted into common units), the FFO per share was C$0.117.

{kind=link}

The AFFO calculation (shown below) uses the FFO as its starting point and after deducting the relevant amounts (like capex and unrecovered rental fees), the AFFO for the quarter was C$8.9M which works out to C$0.103 per share. If we would ‘annualize’ the Q1 results, BTB REIT’s full-year AFFO would come in at C$0.41.

BTB REIT Investor Relations

That’s great news for the distribution as BTB is currently paying a monthly distribution of C$0.025/share , which means the full-year distribution is C$0.30 per share and the payout ratio based on the annualized AFFO is less than 75%. That’s excellent, and the current 10% dividend yield remains fully covered.

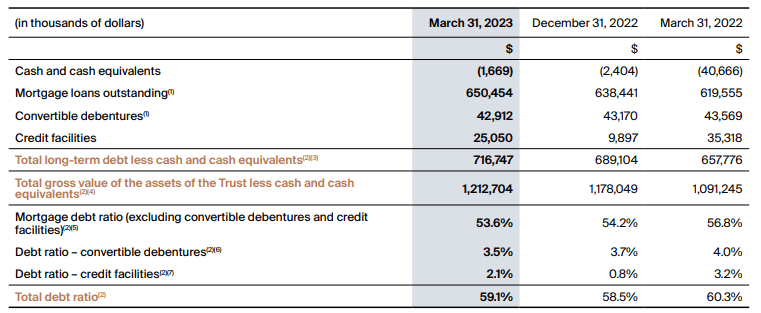

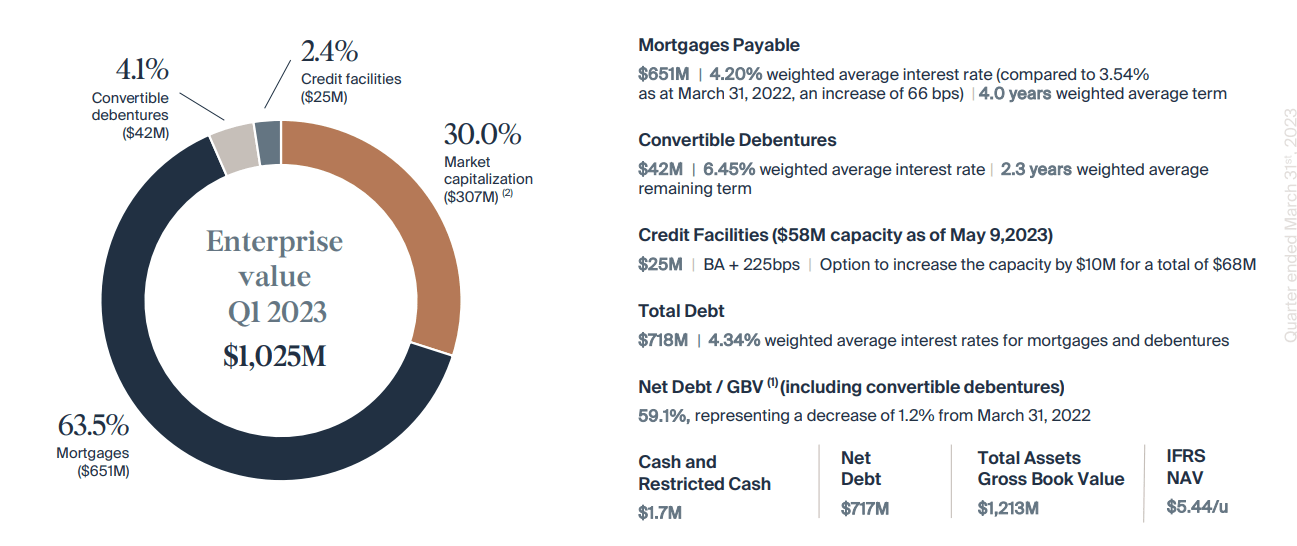

The balance sheet remains a sore point. As of the end of Q1, the total debt ratio came in at 59.1% (as you can see below).

{kind=link}

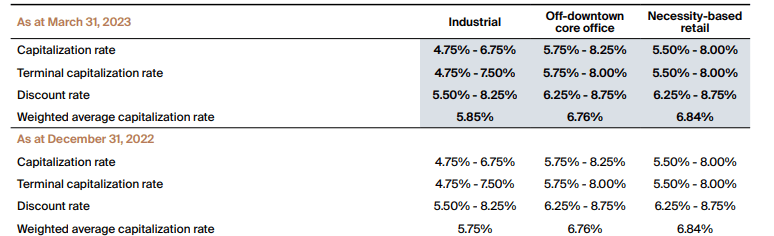

59% is pretty high, especially when you know the weighted average capitalization rate of the portfolio was approximately 6.49% (with the lowest cap rate for the industrial properties).

{kind=link}

While I’m fine with the cap rates used for the industrial and retail assets, I’m not convinced 6.76% is high enough for off-downtown offices. Increasing that cap rate to approximately 7.75% while keeping everything else equal would reduce the fair value of the assets by approximately C$90M. In that case, the debt ratio would increase to 64% and I’m not too keen on REITs with a high debt level where the pain of increasing interest rates still has to be ‘felt’. The weighted average cost of debt is approximately 4.34% right now , and an increase to 5.5% would increase the interest expenses by C$8.3M per year and this would reduce the AFFO per share by almost C$0.10 (excluding the positive impact from future rent hikes).

{kind=link}

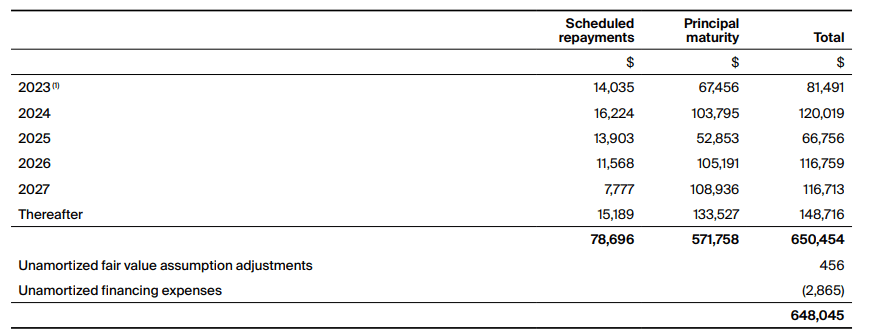

Fortunately the maturity dates of the fixed rate debt are well spread out in time so the interest expenses will only gradually increase.

{kind=link}

This means BTB REIT has a fighting chance and the rotation away from office space towards industrial properties. Additionally, the debt that will be maturing first has a relatively high average interest rate, so I only expect BTB’s interest expenses to increase by a few million dollar per year between now and the end of 2024. This means the impact on the AFFO could be lower than I had previously feared.

Investment thesis

If you’d just look at an earnings multiple, BTB REIT is very cheap as the stock is currently trading at just 7.5 times the AFFO. And while the exposure to the office segment could be a reason for a discount, let’s not forget BTB is rotating into industrial assets.

It looks like the market is agreeing with my assessment the balance sheet poses the main risk. And as BTB REIT has recently filed a base shelf prospectus, odds are the REIT will want to raise money sooner rather than later. While theoretically the REIT could also use the base shelf to issue new debentures, I think it is more likely we will see an equity raise as on the conference call, management mentioned ‘ our intent is not to issue other debentures’ .

That could be a tremendous help for the REIT and send a signal to the market the acute balance sheet risk is no longer a pressing matter. While it wouldn’t be great to issue stock at a steep discount to the current NAV/share (C$5.44) , it would take the pressure off the balance sheet. In an ideal world, the pressure would be reduced by selling some office properties at or close to the fair value as that would also show strength. On the conference call, management indicated it expects to sell C$40-60M in office properties before the end of the third quarter.

I still don’t have a position in BTB REIT but after the recent 20% share price decrease, the risk/reward ratio is improving, and a speculative long position could be warranted. I haven’t made up my mind yet but the share price decrease since February does make the stock more attractive.

For further details see:

BTB REIT: A Whopping 10% Yield But Balance Sheet Concerns Remain