CA - BTB REIT: Debentures Offer Low Risk Play For A 10% Yield (Rating Upgrade)

2023-12-28 10:00:00 ET

Summary

- High leverage and REITs don't mix well, especially when rates are rising.

- But BTB Real Estate Investment Trust has a unique portfolio, and even its office side is looking very resilient.

- Refinancing will push up weighted average interest rates, but we tell you why we still think 20% total returns could be achieved on the stock.

- The debentures are the play if you like low-risk for a 10% YTM.

On our first coverage of BTB Real Estate Investment Trust (BTBIF)( BTB.UN:CA ), we explained why the company was far safer than the market perception. While the fear of "office" ruled the roost, BTB REIT had a nice ace up its sleeve, and there was no real existential risk here. In this article, we review the performance since then and the Q3 2023 results . We go over where we see this headed in 2024 and tell you why the debentures are a sweet joy at the current price.

The Setup

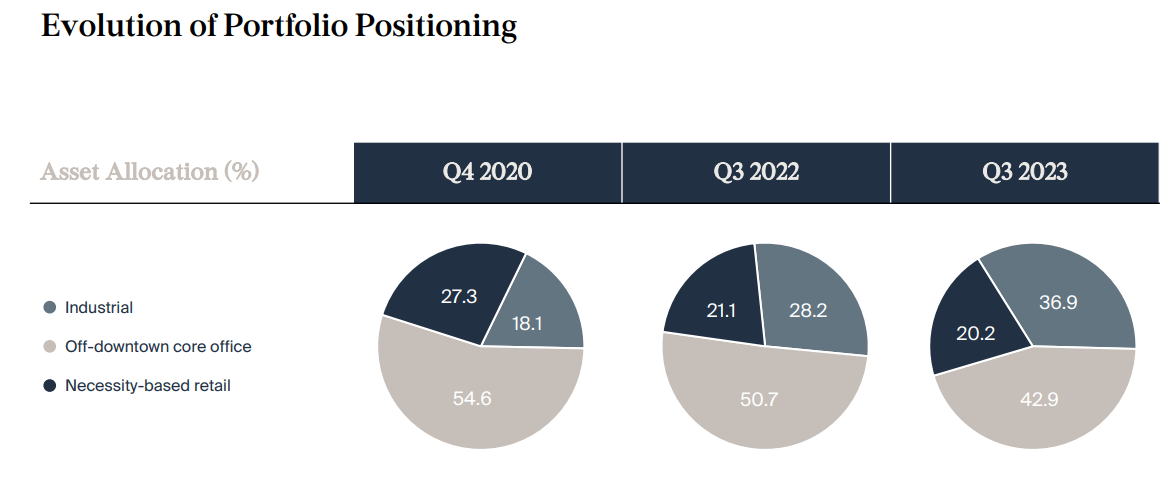

BTB's portfolio has done a steady march towards emphasizing industrial and retail relative to office.

{kind=link}

You can actually see a notable change just from the last quarter.

BTB Q2-2023 Presentation

Some of this evolution has been driven by rent changes as leases come for renewal, and some of it from cap rate changes as BTB has increased the value of industrial relative to office. Investors tend to worry about office, and there are some legitimate concerns in some markets. But whatever concerns may or not be valid, we are certainly not seeing any problems for BTB. This quarter marked a small increase in the overall occupancy levels for the REIT.

{kind=link}

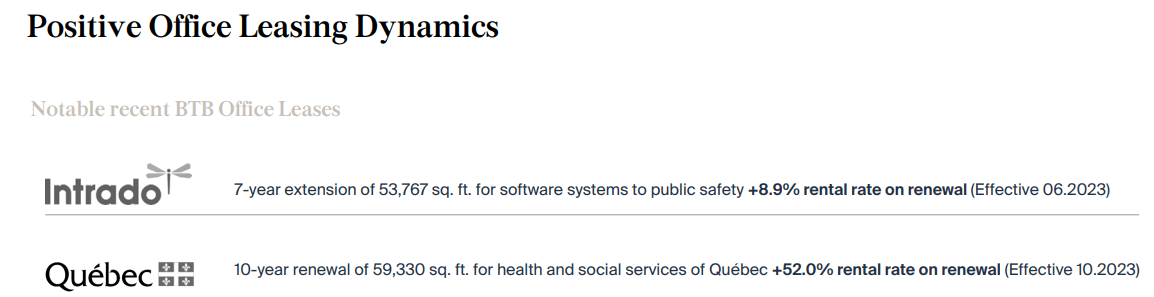

The rent renewals were pretty outstanding. Yes, industrial was the shining star, but office was pretty good, too.

Achieved a cumulative average increase of 7.1% in the rent renewal rate since the beginning of the year in the industrial +15.7% (10,831 sq. ft.), off-downtown core office +5.9% (235,800 sq. ft.) and necessity-based retail +10.4% (80,329 sq. ft.). Shortly after the end of the quarter, the Trust renewed a lease comprising 27,638 sq. ft. of leasable area with a tenant in Ottawa, Ontario with an increase in the rent renewal rate of 2.6%. Also, the Trust leased 26,000 sq. ft. to a major Quebec based accounting firm in its office property located in Three-Rivers and leased an expansion space of 16,763 sq. ft. to an office tenant in one of its properties located in Ottawa, Ontario

Source: BTB Q3-2023 Presentation .

These renewals are also longer-term commitments (two examples shown below).

{kind=link}

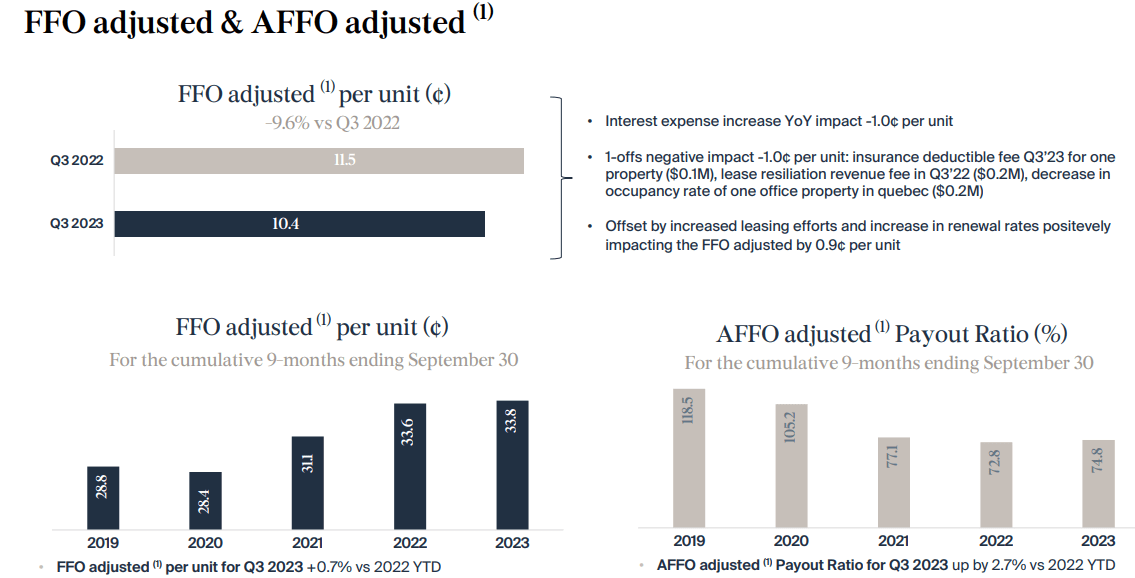

With all of that said, the bulls complaining the market is giving this no respect, have to contend with the declining funds from operations ((FFO)). FFO and adjusted FFO ((AFFO)) but dropped as interest expenses ramped up once more.

{kind=link}

The weighted average rate climbed to 4.29% compared to 4.09% at the end of December 2022. This is a steady climb, albeit a slower one than some other REITs have experienced. The REIT has fortunately stuck primarily to fixed-rate mortgages and its weighted average debt term is low, but acceptable.

As at September 30, 2023, the majority of the Trust's mortgages payable bear interest at fixed rates (cumulative principal amount of $574.2 million) or are subject to floating-to-fixed interest rate swaps (cumulative principal amount of $50.7 million). However, the Trust has three loans that bear interest at floating rates (cumulative principal balance of $19.2 million). The weighted average term of existing mortgage loans was 3.4 years as at September 30, 2023, compared to 4.4 years for the same period last year. The Trust attempts to spread the maturities of its mortgages over many years to mitigate the risk associated with renewals.

Source: BTB Q3-2023 Presentation.

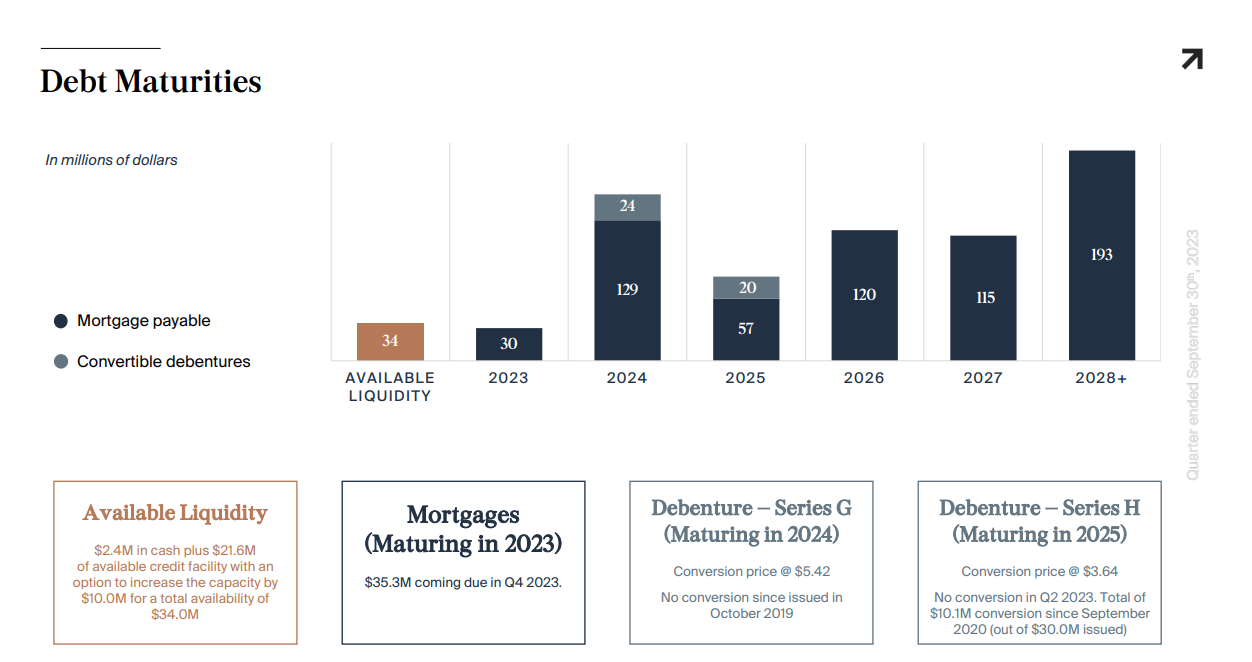

BTB's work is cut out for it again over the next 12 months. From September 30, 2023, until the end of 2024, the REIT had $183 million up for refinancing.

{kind=link}

That is not a small amount when you throw the market capitalization in there.

There was some attempt to deleverage over the last couple of quarters, but the wide bid-ask spreads prevented transactions.

Tom Callaghan

Got it. That's helpful color. Maybe switching gears just a bit. I know you mentioned last call, the potential for some asset dispositions, and I think you had a few properties on the market. Just any update there or thoughts?

Michel Leonard

Well, we put some properties on the market. And right now, the acquirers are basically bottom feeders. So there are purchasers out there, but I don't -- they don't recognize the quality of the assets that we do own. And as a result, they treat the assets as common properties. Obviously, they like to nitpick and so on. So we did put some properties on the market. We were not successful, in the sense that we didn't want to basically sell at a huge discount that a property that produces good income for us, good NOI. So why would we basically sacrifice a property in order to use that money, redeploy the capital, but then incur a loss as a result of it or the downgrade of our AFFO.

So I think that it's better to look carefully at the portfolio. If there are opportunities to sell at a decent price, we'll sell it. But if it's not the case, then we're not going to sacrifice any of our assets on that front.

Source: BTB Q3-2023 Conference Call Transcript .

Outlook

The refinancing environment should be materially better today, than what we saw in Q3 2023. Longer-term Government Of Canada bond yields have come down, and we are seeing junk bond spreads also moving lower. At present, it looks like BTB should be able to breeze through the next 6 months, considering its portfolio strength and the macro environment. The stock remains cheap as you assess it versus its own estimated NAV levels.

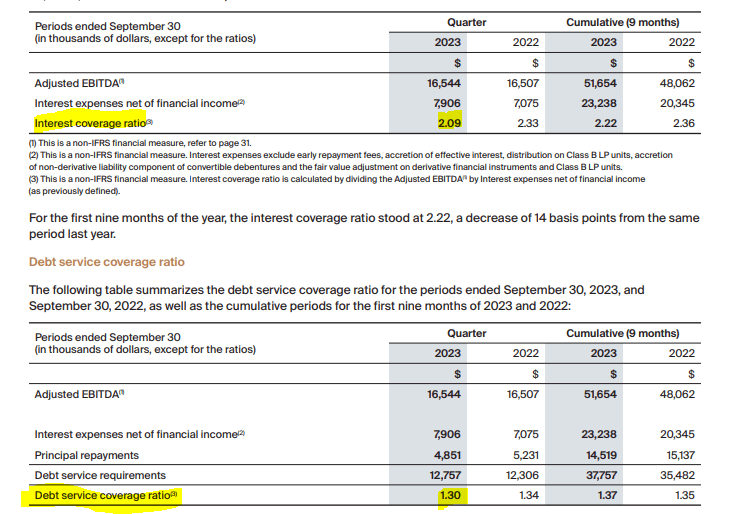

Relative to where everything else stands today, this is definitely cheap. The bear arguments likely pertain to the leverage with interest and debt service ratios on the low side.

{kind=link}

Verdict

Even in the most generous of assumptions, these ratios will go lower over the next 12 months as the interest rates on the portfolio have nowhere to go but up. BTB does have almost exclusively property level mortgages, and that means the odds of a wipeout are effectively zero. We think we will get a higher price from here and are giving this a Buy with a $3.25 price target in 1 year. Alongside the distributions, this creates a 23% total return over 1 year.

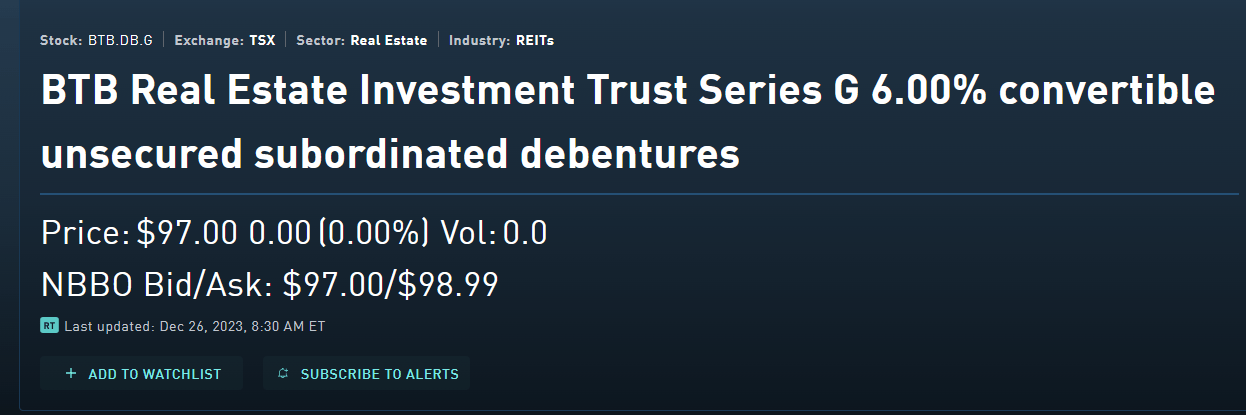

We are personally playing it a bit more defensively. BTB Real Estate Investment Trust Series G 6.00% convertible unsecured subordinated debentures (BTB.DB.G:CA) mature in October 2024.

{kind=link}

We will ignore the convertible strike price of $5.42, as there is no chance of that happening. But the yield to maturity with a $97 price is about 10.00%. These trade the solid average volume (about 37,000 a day). We rate these a strong buy for the low-risk setup over the next 10 months.

For further details see:

BTB REIT: Debentures Offer Low Risk Play For A 10% Yield (Rating Upgrade)