BACRP - BTZ: Multi-Sector Bond Fund At A Discount

2023-04-03 13:01:42 ET

Summary

- BTZ invests with a split between investment-grade and below-investment-grade debt with a multi-sector approach.

- The fund's latest discount has dropped into the double-digit area, where it becomes a more appealing investment option.

- A big drawback here is the fund's distribution coverage is severely lacking.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 20th, 2023.

BlackRock is the world's largest asset manager, offering funds in almost any flavor you can imagine. With their far reach and significant size, they can offer many different types of funds and put the right teams together to manage them.

One of their closed-end funds is a diverse approach to the fixed-income space utilizing a multi-sector bond fund approach. That would be BlackRock Credit Allocation Income Trust IV ( BTZ ). This fund is spread across both investment-grade and below-investment-grade debt, venturing into developed markets, securitized products, emerging markets and bank loans. The managers running this fund have a lot of flexibility in where they can invest as a multi-sector bond fund.

That means there is some higher quality there that could be particularly attractive during this period of financial uncertainty we are going through. On top of this, the fund's discount has also widened into double-digit depths, which could present another opportunity now. Some of this was continued expansion into a deeper discount than our previous coverage . Since then, the fund has experienced some losses, primarily due to this discount widening.

BTZ Performance Since Prior Update (Seeking Alpha)

Today, it looks like we could move it up to a potential "buy" from a "hold." With that, the big caveat is that the distribution is unsustainable and is unlikely to be smooth sailing in that department. The distribution coverage is severely lacking. Seeing a distribution cut wouldn't be all that surprising. This is potentially why we've seen the double-digit discount open up once again - beyond just additional market volatility.

The Basics

- 1-Year Z-score: -1.41

- Discount: 10.72%

- Distribution Yield: 9.99%

- Expense Ratio: 0.94%

- Leverage: 35.56%

- Managed Assets: $1.055 billion

- Structure: Perpetual

BTZ invests with an objective to "provide current income, current gains, and capital appreciation." They intend to achieve this through investing "...under normal market conditions, at least 80% of its assets in credit-related securities, including, but not limited to, investment-grade corporate bonds, high yield bonds, bank loans, preferred securities or convertible bonds or derivatives with economic characteristics similar to these credit-related securities."

The fund is quite large, which isn't too surprising for a BlackRock fund. This can help with having a relatively lower expense ratio in the CEF space. However, the total expense ratio comes to 1.79% when including interest expenses for their leverage.

When using leverage, the fund can earn additional income for shareholders. Whatever the difference between what the bonds are earning and what they are paying for, the leverage is passed onto shareholders. However, it can also make the fund riskier due to increased volatility and amplified moves to the downside. As interest rates are rising, the cost of these borrowings is also rising, cutting into the spread that they can earn.

BTZ utilizes reverse repurchase agreements. At the end of 2022 , the interest rates on these were around 4.5%. A year prior, at the end of 2021 , these were around 0.30% roughly. That really highlights the impact of higher interest rates for this fund.

Interestingly, note that last year they had interest rate swaptions to help mitigate and act as a hedge against the rising interest rates. At the end of 2022, they show centrally cleared interest rate swaps instead, where they are actually paying the floating rate and receiving the fixed rate. This has ended up being a losing trade so far. However, if rates are cut, it could pay off.

{kind=link}

Performance - Discount Pushing It To A Buy Area

The fund's losses in the last year might seem shocking. However, these were amplified not only by being leveraged - which always adds more risk - but also due to rapid discount expansion. When comparing the fund to its benchmarks over the longer term, the results have been much more competitive, even if those results were rather lackluster across the board.

Here are the results at the end of 2022, where they list the comparison to several benchmarks in their annual report.

{kind=link}

Investment-grade debt with rapidly rising interest rates will not produce attractive results. We can clearly see that in the performance of the last year. Those results were so horrific that they've taken the longer-term average results down with them. As an example, at the end of September 30th, 2021 , the annualized 10-year total NAV return was 8.72%, and the total market return was 10.21%.

More recent results are displayed on their website, but they don't include the benchmarks.

BTZ Annualized Returns (BlackRock)

However, the overall takeaway that I see here is the fund's total market price results have been much more of a driving factor lower. The current discount is around the fund's decade-long average but off significantly from the premiums it was flirting with in 2021.

Ycharts

One ugly year can bring down the results this dramatically from what could be seen as a solid performer to now mediocre within such a short period. The discount expansion is exacerbating these results too. However, this is also the time that can indicate a much more lucrative time to buy. Generally, it's at the time when no one wants to invest. We could most definitely go lower, and the discount could expand even further. We've certainly seen that be the case, but for a longer-term investor, it could be worth nibbling in.

Distribution - A Cut Could Be In The Future

I know a lot of investors don't want to hear that a fund could cut their distribution, but with BTZ, it could take place. We are simply looking at the facts with realistic expectations. The 9.99% distribution rate here is quite attractive; it might not be something that can be entirely relied upon.

{kind=link}

As we touched on above, the leverage costs for this fund (and all leveraged CEFs) have really exploded. That is eating into the net investment income generated from the fund. Thus, why we see the distribution coverage fall quite dramatically.

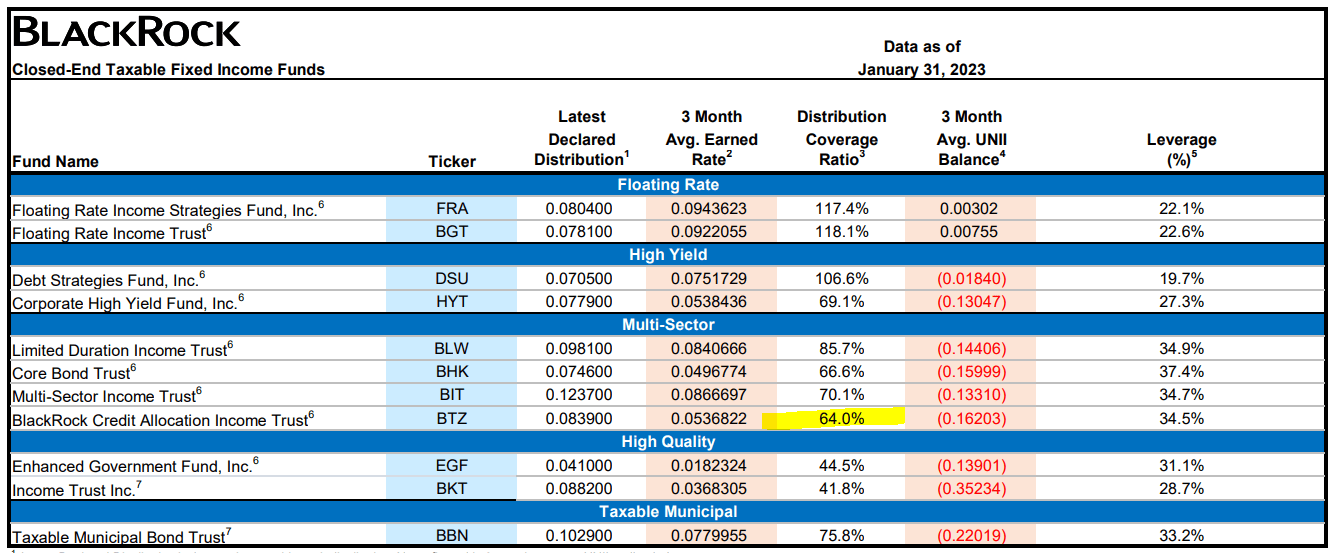

The latest UNII report shows only 64% NII distribution coverage for the last three months. That was a decline from the 76.4% coverage we saw in our previous update for the end of September 2022.

{kind=link}

This was a continued deterioration of the coverage from the prior year of 83.67%.

{kind=link}

As a fixed-income fund, we would ideally want to see NII coverage over 100%. Funds can also pay their distributions from capital gains. The various derivatives they use could be a source of gains.

However, BTZ had mixed results. The losses were limited in their futures contracts and swaps, but they are losses nonetheless. On the other hand, the options they had written contributed to some gains and reduced the realized losses to a small degree.

BTZ Realized/Unrealized Gains/Losses (BlackRock)

Since the fund's already trading at a rather attractive discount usually when they cut, we don't often see a significant reaction. So a cut could be met with a fairly neutral reaction.

BTZ's Portfolio

While the distribution being on shaky ground might be a negative for the fund, the higher quality exposure in BTZ could be seen as a positive. The fund incorporates investment-grade debt, which is fairly different from other CEFs that only focus on junk-rated debt. During times of uncertainty, looking for higher-quality credit could be beneficial.

If interest rates stabilize or we see cuts, that could eventually benefit the fund too. At this time, the fund's effective duration is 6.20 years. This is relatively higher due specifically to the investment-grade exposure that often sees more duration risk. So for every 1% increase in interest rates, it would be assumed that the underlying portfolio would drop 6.2%. What was a headwind in the last year resulting in the fund's sizeable drop could become a tailwind in the future. Not to mention that it could benefit the fund's distribution coverage as well as the reverse repurchase agreements should see costs drop if rates are cut.

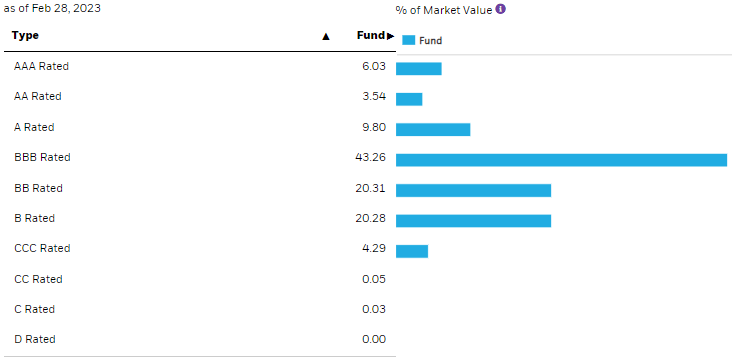

Investment-grade debt represented 62.63% of the portfolio at the end of February, with the remainder in BB or lower.

{kind=link}

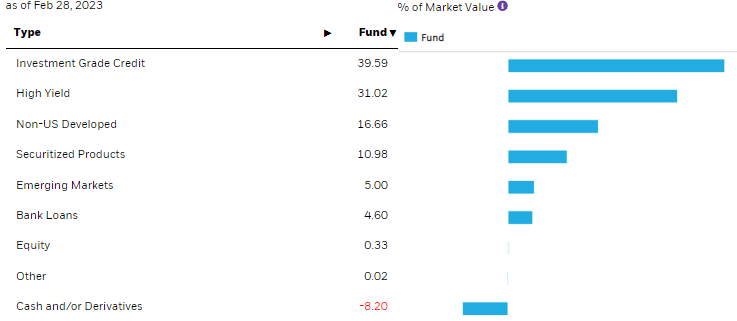

The fund is quite flexible in where they might be able to invest, but they largely stick with corporate bonds in both investment-grade and high-yield categories. That flexibility also expands into geographic exposure, but they also stick to a fairly narrow focus there, too, by investing mostly in U.S. exposure. U.S. exposure represents just under 85% of the fund's portfolio.

{kind=link}

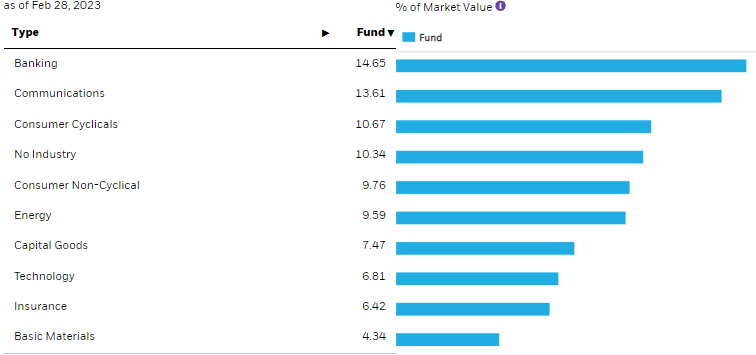

The fund's largest industry exposure here is to banking. Banking and financials can be a pretty unnerving area of exposure at this time.

{kind=link}

However, some of those fears should be assuaged when looking at the top holdings.

{kind=link}

None of the largest exposure is to banks currently facing significant pressures, which have mostly been contained to regional entities. While the whole banking space might be feeling the pressure, it is the names such as Wells Fargo ( WFC ), Bank of America ( BAC ) and Citigroup ( C ) that could be the ultimate beneficiaries in the long run. As depositors may permanently be damaged from working with regional banks and sticking with the larger, most established banks, that should drive further business to these banking giants.

Conclusion

BTZ is a multi-sector bond fund. While the future is uncertain, what is certain is that the fund's discount has now dropped to much more appealing levels. In the last couple of years, since I've been covering BTZ, I couldn't see it as a buy and went with a neutral "hold" rating.

Now that we have experienced sizeable losses due to the ratcheting up of interest rates aggressively, it's looking much more appealing. The overall market volatility has also likely contributed to the fund's sizeable discount opening. Still, we might not yet be out of the woods in this environment, so using a dollar-cost averaging approach could be appropriate.

For further details see:

BTZ: Multi-Sector Bond Fund At A Discount