CA - BUI: This Utility Fund Is Worth Watching But It Is Currently Too Expensive

Summary

- Utilities are a great sector for retirees to invest in, but their yields are incredibly low because of today's richly-valued market.

- BlackRock Utility & Infrastructure Trust provides investors with access to a portfolio of utilities and other similar companies and provides a respectable yield.

- The BUI closed-end fund has significantly underperformed the utility index over the past twelve months, which is disappointing.

- It is questionable how long the fund can maintain its distributions since its assets are declining.

- The fund is very expensive relative to its historic price right now, so potential investors should wait for it to become a bit cheaper.

For generations, one of the most popular investment vehicles for retirees and other conservative investors has been utility stocks. This makes a great deal of sense since utilities tend to enjoy remarkably stable cash flows regardless of the conditions in the broader economy. This positions these companies quite well for weathering through recessions or other negative environments, which may be important today as many metrics indicate that the economy in the United States has been weakening. This general stability lends itself well to high dividend payments, which provide a source of income that many retirees need. Unfortunately, the low-interest rate environment that has dominated most of the economies around the world for the past decade has driven up the valuation of most dividend-paying stocks, including utilities, and by extension driven down yields. In fact, the iShares U.S. Utilities ETF ( IDU ) only yields 2.48% today. That is well below the rate that can be obtained on a bank savings account and thus it makes no sense for most conservative investors to take on the added risk of investing in utility stocks.

Fortunately, there is a way around this problem that allows an investor to continue to have exposure to the sector as well as generate a much higher yield than a risk-free asset can offer. This is by investing in a closed-end fund ("CEF") that specializes in the utility sector. These funds are admittedly a somewhat underfollowed asset class but they provide easy access to a professionally-managed portfolio of assets that can utilize a variety of strategies to generate a higher yield than any of the underlying assets possesses.

In this article, we will discuss the BlackRock Utility & Infrastructure Trust ( BUI ), which is one closed-end fund that fits into this category. This fund currently boasts a 6.33% yield, which is clearly superior to the yield offered by the utility index as well as being above the risk-free rate. I have discussed this fund before, but a few months have passed since then, so obviously a few things have changed. This article will, therefore, focus specifically on these changes as well as provide an analysis of the fund's financial condition.

About The Fund

According to the fund's webpage , the BlackRock Utility & Infrastructure Trust has the stated objective of providing its investors with a high level of total return. The fund defines this as a combination of current income, current gains, and long-term capital appreciation. This is not particularly surprising, considering that the name of the fund implies that it invests primarily in common stock. In fact, common stock accounts for 96.86% of the fund's portfolio with the remainder being cash:

CEF Connect

This is admittedly somewhat surprising. Utilities are among the few companies that issue preferred stock and many closed-end funds include that asset class in order to boost their incomes. That is because preferred stock tends to have a higher yield than common stock issued by the same company. Obviously, this fund does not do that, which results in its current income being lower than it otherwise could be. That is admittedly a bit disappointing. With that said though, the common stock does have greater potential for long-term capital gains since its price is theoretically linked with the growth and prosperity of the issuing company. As utilities usually grow their earnings per share at a mid- to high-single-digit rate annually, this should cause utility stocks to increase in price over the long term.

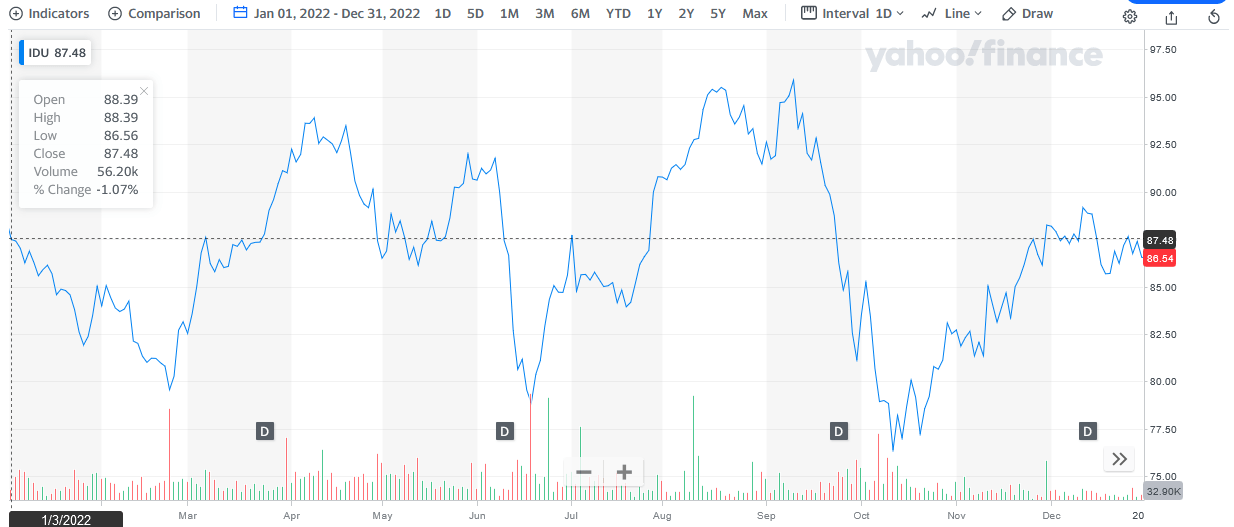

As we saw in 2022, though, this does not always happen during shorter time periods. As we can see here, the U.S. Utilities Index was actually down slightly over that twelve-month period:

{kind=link}

The long-term track record for utility stocks does tend to be positive though. That is why it makes the most sense for this fund to be focusing on total return since common equities are generally purchased for both the dividends that they pay out and the capital gains that they usually deliver.

One of the things that conservative investors tend to like about utilities is that they have remarkably stable and recession-resistant cash flows. This is because of the nature of utilities. These companies provide a service that is generally considered to be a necessity for our modern way of life. After all, how many of us do not have electric service to our homes and businesses or heat for cooking our food? As such, most people will prioritize paying their utility bills ahead of most discretionary expenses during times when money gets tight. As I have discussed in numerous previous articles, money has certainly been getting tight for many American households. According to a recent Prudential Pulse survey , approximately 81% of Generation Z members and 77% of Millennials have either entered the gig economy or are considering doing so as a second job in order to get the money that they need to make ends meet. In addition, we have credit card balances hitting record levels as the current high rate of inflation continues month after month. These are all clear signs that the American consumer is nearing a breaking point and will likely have to cut back on discretionary spending in the near future. Fortunately, the companies in this fund are not providing discretionary items and thus should be relatively immune to any reduction in consumer spending.

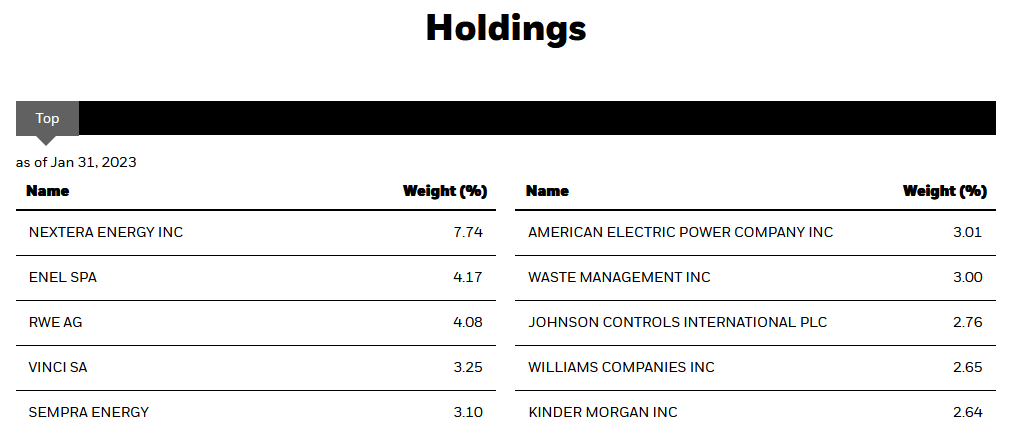

As my regular readers are no doubt well aware, I have devoted a considerable amount of time on this site over the past few years to discussing various utility stocks. As such, most of the largest positions in the fund should be relatively familiar to many readers. Here they are:

{kind=link}

There are some companies that probably will not come to most people's minds when they think of a utility stock. In particular, we see Waste Management ( WM ), Johnson Controls ( JCI ), The Williams Companies ( WMB ), and Kinder Morgan ( KMI ) among the fund's largest positions. The latter two are among the largest midstream companies in the United States, Waste Management is a sanitation company, and Johnson Controls primarily installs and maintains HVAC systems in commercial builds. With that said, Waste Management can be thought of as a utility since the removal of trash from homes and businesses is generally something that needs to be done regardless of any weakness in the economy. It, therefore, has a very similar cash flow profile to a utility company. The Williams Companies and Kinder Morgan also both have remarkably stable cash flows regardless of conditions in the broader economy, which I have discussed in numerous previous articles on both companies.

The outlier here is Johnson Controls, as it may not be completely recession-resistant. We do see companies close down offices, retail stores, and other operations during times of economic turmoil, which would reduce the demand for the company's services. We may also see some businesses skimp on HVAC maintenance during such a situation. However, it is probably still more insulated from a recession than a restaurant or a company selling high-priced gadgets or something like that, though.

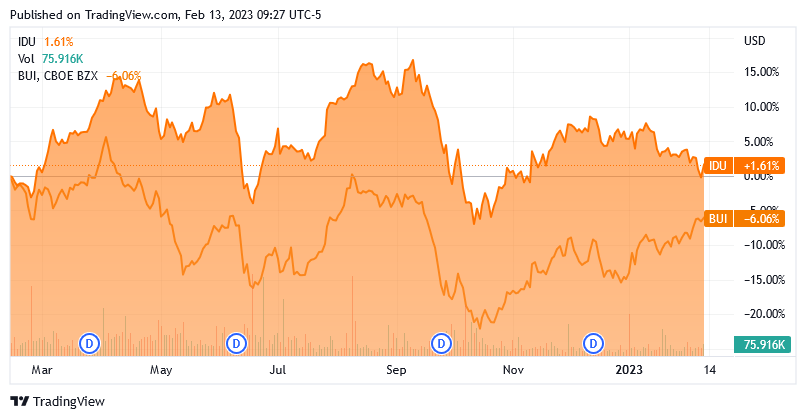

There have been surprisingly few changes to the fund's holdings over the past few months. The only major change is that Waste Connections ( WCN ) was removed and replaced with Vinci SA ( VCISF ). There were numerous changes to the weightings of the various stocks, but that could simply be caused by one company outperforming another in the market. The fact that there have been so few changes may lead one to assume that this fund has a very low annual turnover. This is actually the case as its 20.00% annual turnover is one of the lowest among equity funds. The reason that this is important is that it costs money to trade stocks or other assets. These expenses are billed directly to the fund, which creates a drag on its performance. After all, the added expenses mean that the fund's management needs to earn sufficient excess returns to both cover these added expenses and still deliver a return that is reasonably in line with the benchmark index. That is a very difficult task for any manager and as a result, most actively-managed funds fail to match their indices over extended periods of time. This one is certainly no exception to that as it has significantly underperformed the utility index over the past year:

{kind=link}

Although the closed-end fund does have a higher yield, that cannot make up for the performance difference here. An investor in the index fund a year ago would have significantly more money today than an investor in the closed-end fund who bought at the same time. With that said though, the BlackRock Utilities, Infrastructure, & Power Opportunities Trust does invest in a wider range of companies than the index fund does so this is not a perfect comparison.

One thing that we may conclude from looking at the largest positions in the fund is that the BlackRock Utilities, Infrastructure, & Power Opportunities Trust invests its assets globally. After all, there are a few foreign companies on the ten largest positions list. This continues to be true across the fund's entire portfolio. As we can see here, only 55.04% of the fund's assets are invested in American companies:

CEF Connect

The United States only accounts for a bit less than a quarter of the global gross domestic product. As such, the fund is overweighted to this country based on its actual representation in the global economy. However, most global funds have an American allocation of more than 60% so this fund is doing better than most at achieving international diversification. This is nice because of the protection that it provides us against regime risk. Regime risk is the risk that some government or other authority will take an action that has an adverse impact on our investments in that country. The only real way to protect ourselves against that risk is to ensure that only a relatively small proportion of our portfolios is exposed to any given nation. This fund is doing that to a point, although we do see a lack of emerging market securities in its portfolio as there are only very small allocations to China and Brazil.

Leverage

In the introduction to this article, I stated that there are some strategies that closed-end funds can use in order to boost the effective yields of their portfolios. One of these strategies employed by the BlackRock Utility & Infrastructure Trust is the use of leverage. In short, the fund borrows money and uses that borrowed money to purchase the common stocks of utilities or of other companies that share many of the characteristics of utilities. As long as the interest rate on the borrowed funds is less than the total return provided by the purchased assets, the strategy works pretty well to boost the overall return of the portfolio. The fund can then pay out those higher returns to its investors, effectively boosting its yield. As the fund can borrow money at institutional rates, which are significantly lower than retail rates, this will usually be the case.

Unfortunately, the use of leverage is a double-edged sword because it boosts both gains and losses. Thus, we want to ensure that the fund is not employing too much debt since that would expose the investors to too much risk. I generally like to see a fund's leverage be under a third as a percentage of its assets for this reason. The BlackRock Utilities, Infrastructure, & Power Opportunities Fund certainly fulfills that requirement as its levered assets currently comprise 0.11% of the portfolio. In other words, the fund is barely using any leverage at all and certainly has room to increase it. In fact, it probably should increase the leverage in order to boost the returns to investors, especially considering that it is investing in reasonably safe assets. However, investors should probably not have to worry too much about the risks involved with the fund's use of this strategy.

Distribution Analysis

As stated in the introduction, one of the reasons that investors buy utilities is the high yields that they often possess. For example, the U.S. Utilities Index yields 2.48% as of the time of writing, which is quite a bit above the 1.55% yield of the S&P 500 ( SPY ). The midstream and energy infrastructure companies held by the fund tend to have a higher yield, so they will boost the effective yield of the portfolio. In addition, the fund applies a small amount of leverage to boost the yield but as the leverage is negligible, we should not expect this to have a huge effect. Thus, we can expect the fund to have a reasonable yield but not a very high one.

This is certainly true as the BlackRock Utility & Infrastructure Trust pays a monthly distribution of $0.121 per share ($1.452 per share annually), which gives it a 6.33% yield at the current price. This is admittedly not as high as many other closed-end funds manage to achieve but the fund's low leverage and its emphasis on the common stock, as opposed to other high-yielding assets, make this understandable. Its yield is still well above the risk-free rate, which is more than can be said for most index funds today.

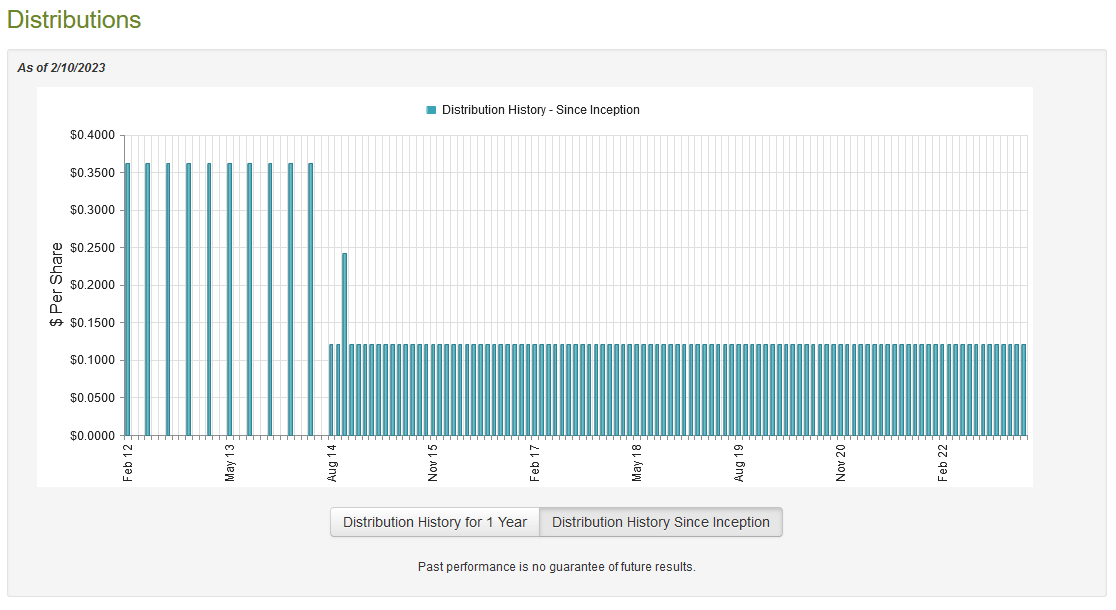

The fund has been fairly consistent about its distribution over the years:

{kind=link}

There may be some that notice the significant decline in the distribution that occurred back in 2014. That does not alter the fact of this statement as the fund converted from a distribution of $0.3625 per share quarterly to $0.1210 per share monthly. That is actually a very small increase when measured on a quarterly basis. This general consistency will likely endear the fund to conservative investors that are likely to be interested in a utility fund.

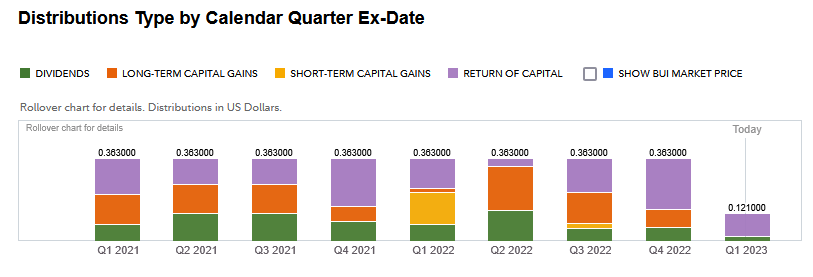

This same group of conservative investors may be quite concerned about the fund's recent return of capital distributions, though:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors' own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be considered a return of capital, such as the distribution of unrealized capital gains. That is clearly something that this fund might be doing so it is important that we investigate its finances in order to determine exactly how it is paying for these distributions and how sustainable they are likely to be.

Unfortunately, we do not have a particularly recent document that we can consult for this task. The fund's most recent financial report corresponds to the six-month period that ended on June 30, 2022. This is disappointing as it will not include any information regarding the fund's performance in the second half of 2022. As this is when we start to see it making a substantial return of capital distributions, it would be nice to have that information so that we can figure out how exactly it is getting the money to pay us. Nonetheless, we have to go with what we have now and hope that the fund soon releases a more current report. During the six-month period, the BlackRock Utility & Infrastructure Trust received a total of $7,919,124 in dividends and surprisingly nothing in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources and net out foreign withholding taxes, the fund reported a total income of $7,459,964 during the six-month period. The fund paid its expenses out of this amount, which left it with $4,667,626 available for the shareholders. That was nowhere close to enough to cover the $15,992,324 that the fund actually paid out in distributions during the period, however. At first glance, this is likely to be concerning as the fund clearly failed to cover its distributions out of net investment income.

However, there are other ways that the fund can get the money that is needed to cover its distributions. For example, it may have capital gains that can cover it. As might be expected from the market volatility that occurred during the first half of 2022, though, the fund generally was not successful at this task. During the period, it managed to achieve net realized gains of $13,333,209 but this was more than offset by $94,366,463 net unrealized losses. Overall, the fund's assets declined by $81,161,745 after accounting for all inflows and outflows.

Thus, the fund clearly failed to cover its distributions during the period. With that said, it did manage to have sufficient net investment income and net realized gains to cover everything. The big concern is that the smaller asset base will likely make it more difficult for the fund to generate sufficient capital gains to maintain the distribution going forward. This is something that we need to keep an eye on going forward.

Valuation

It is always critical to ensure that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Utility & Infrastructure Trust, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all of the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of February 10, 2023 (the most recent date for which data is currently available), the BlackRock Utility & Infrastructure Trust has a net asset value of $22.77 per share but the shares currently trade for $23.18 per share. That gives the fund's shares a 1.80% premium to the net asset value at the current price. This is substantially more expensive than the 3.56% discount that the shares have traded at on average over the past month. Thus, potential investors should wait to see if a more attractive entry price presents itself in the near future.

Conclusion

In conclusion, utilities have long been a fairly popular investment choice among risk-averse investors due to their high yields and general stability. Unfortunately, the richly valued market today has significantly reduced the yields of these stocks so that they are now yielding less than a regular bank savings account.

The BlackRock Utility & Infrastructure Trust provides a way to boost this yield significantly and diversify your portfolio at the same time. The fund is generally good, although it has underperformed the broader index over the past year. There are also some questions about its ability to maintain its distribution going forward, although it does appear okay for now.

The BlackRock Utility & Infrastructure Trust price is a bit high, though, so investors really should wait for a more attractive entry price before purchasing the fund's shares. It would be a reasonable addition to a portfolio if purchased at a discount to the net asset value.

For further details see:

BUI: This Utility Fund Is Worth Watching, But It Is Currently Too Expensive