BYDDY - BYD: A 2-Horse EV Race With Tesla - Great Upside Remains

2023-07-07 12:00:07 ET

Summary

- While BYD's valuations may have been geopolitically discounted compared to TSLA's, we believe its NTM P/E of 28.99x still looks promising, compared to F's and GM's.

- Perhaps this has to do with its higher gross margins, thanks to China's lower cost of labor and the automaker's vertically integrated supply chain.

- BYD's stellar management continues to project 3.6M in 2023 deliveries, suggesting a high growth cadence, despite the uncertain reopening demand and macroeconomic outlook.

- Combined with the robust EV sales in the US, EU, and China, thanks to the price war, we believe BYD's prospects remain excellent through the next decade.

- The BYD stock is still a Buy, with a long-term price target of $48, if not $79, once the geopolitical discount is lifted.

The BYD Investment Thesis Remains Stellar, Thanks To TSLA

We previously covered BYD Company Limited (BYDDF) in March 2023, discussing its excellent prospects within China and internationally, thanks to the increased partnerships and dealerships in multiple territories. Additionally, the stock had been rated as a Buy since our first coverage , providing investors with +28.92% of returns since December 2022.

For now, BYD has delivered 703.56K vehicles (+27.4% QoQ/ +98.1% YoY ) in Q2'23, comprising 352.16B EVs (+36.8% QoQ) and 348.08K plug-in hybrids (+22.8% QoQ). International demand appears to be decent as well, at 35.55K vehicles (-8.3% QoQ).

While some bears may assume that much of these are commercial vehicles , we must highlight that the segment only comprises 3.3K vehicles in Q2'23 (-20.4% QoQ), or the equivalent of 0.46%.

These numbers speak volumes about BYD's consumer demand domestically, in comparison to NIO's (NIO) underwhelming deliveries of 23.5K vehicles (-24.2% QoQ/ -6.1% YoY) and XPeng's (XPEV) at 34.41K vehicles (in line QoQ/ +97.9% YoY) in the same quarter.

While the automaker's passenger EV deliveries of 616.78K in H1'23 (+90.6% YoY) may lag behind Tesla's (TSLA) at 889.01K (+57.4% YoY) at the same time, we are not overly concerned for now.

With BYD already delivering a total of 1.25M (EV and plug-in hybrids) vehicles by H1'23 ( +94.9% YoY ), we may see it achieve the aggressive 2023 target of up to 3.6M (+93.5%) indeed, assuming a sustained ramp up with a monthly average of ~391K vehicles delivered for the second half.

The rapid growth in the automaker's production and delivery have also demonstrated the management's mastery by vertically integrating its supply chains across chips, parts, and batteries, despite the country's previous Zero Covid-19 Policy, slower reopening cadence, and uncertain macroeconomic outlook.

However, while BYD may have recorded impressive gross margins of 17.7% (+5.1 points sequentially) over the last twelve months [LTM], compared to TSLA's at 23.1% (-3.7 points sequentially), we must also highlight that both automakers have elected to cut prices to boost delivery volumes.

This aggressive strategy has already impacted the latter's gross margins dramatically to 19.3% by FQ1'23 (-4.5 points QoQ/ -9.8 YoY), with FQ2'23 likely to bring forth similar numbers. The same is also observed with the China based automaker, at gross margins of 17.9% (-0.6 points QoQ) in FQ1'23.

Then again, market analysts are still optimistic about TSLA's and BYD's price war strategy, potentially boosting their market shares ahead:

Loss making independent (new energy vehicle) producers are likely to resist further price competitions, but we believe profitable market leaders such as Tesla and BYD still have the pricing flexibility to balance demand and supply - and both companies will continue to expand production capacity aggressively in 2023. ( Reuters )

In addition, BYD's gross margins are probably aided by China's lower labor costs, in comparison to its US-legacy peers, such as Ford ( F ) at 10.7% and General Motors ( GM ) at 13.4% over the LTM.

TSLA's presence in Shanghai is not by accident as well, with the Gigafactory shipping an annualized total of 1.12M vehicles by June 2023 (+20.5% MoM/ +18.7% YoY), comprising 53% of its total deliveries. This was on top of market analysts' 2020 projection of an increased cost efficiency by up to 28%, compared to the Fremont factory.

Combined with the nascent EV adoption, we believe the "two horses" may lead the long-term EV race, especially due to the US' government's 2030 goal of achieving 50% in vehicles sales as electric, similar to China's 2035 target . This is on top of the EU targeting zero-emission vehicles from 2035 onwards.

With the EV sales in the US remaining brisk at 257.5K (+63% YoY) in Q1'23, the EU at 197K for plug-in electric cars (+25% YoY)/ 120K for EVs (+50% YoY) in April 2023, China at +88% YoY for plug-in electric cars/ +70% YoY for EVs in Q1'23, we believe the momentum remains tremendous despite the rising inflationary pressure and elevated interest rate environment, thanks to the price war.

EV Adoption Projected To Accelerate Ahead

{kind=link}

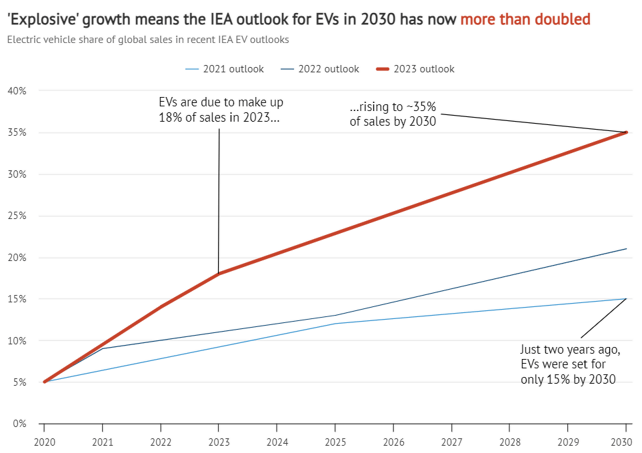

The IEA also expects EV sales to comprise ~36% of the vehicle market share by 2030, compared to the previous 2021 projection of 15%. Combined with the supportive government policie s, sustained transition from the legacy ICE automakers, and normalized spot prices for electrification commodities (lithium/ nickel/ copper), we believe BYD remains well positioned to grow its global deliveries and market share through the next decade.

So, Is BYD Stock A Buy , Sell, or Hold?

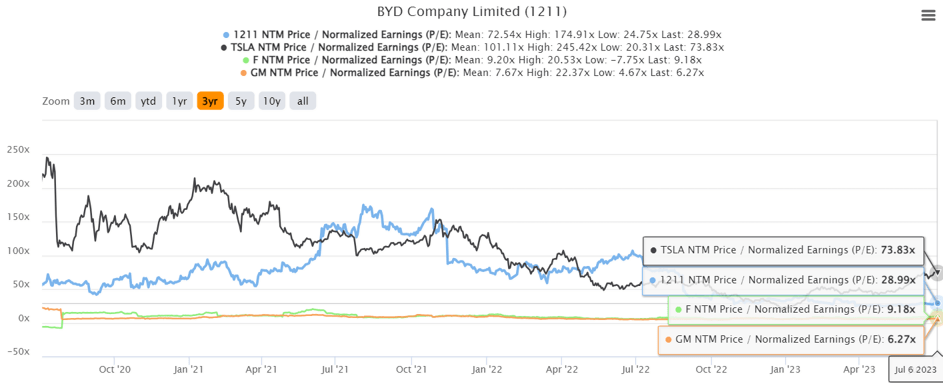

BYD 3Y P/E Valuations

{kind=link}

BYD's valuations are still relatively excellent at NTM P/E of 28.99x, compared to F at NTM P/E of 9.18x and GM at 6.27x. Therefore, while the former's valuations may have been somewhat geopolitically discounted, compared to TSLA's at 73.83x, we believe these numbers still look promising.

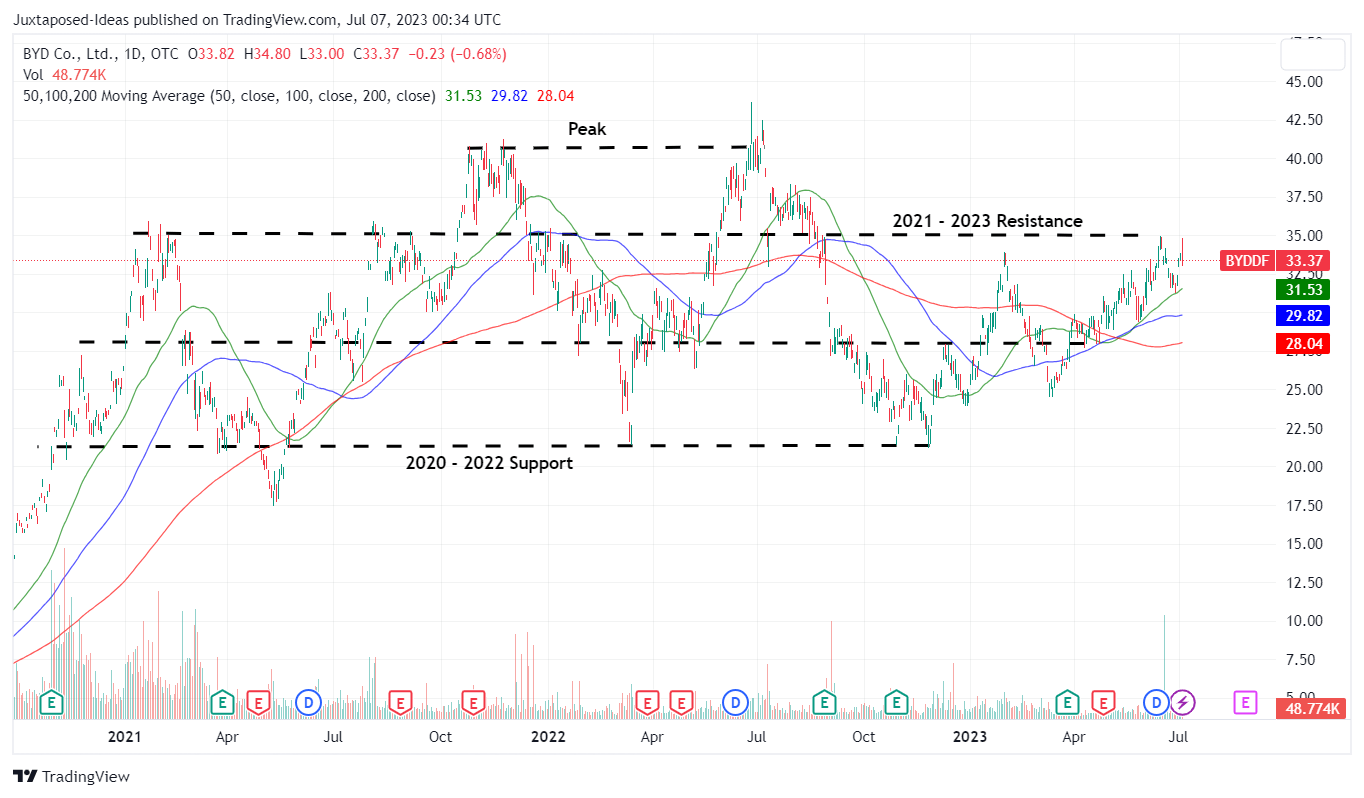

BYD 3Y Stock Price

{kind=link}

The BYD stock continues to climb as well, likely to retest the 2023 resistance levels of $35 in the near term. Then again, given our long-term price target of $48.41, based on its NTM P/E and the market analysts' FY2025 EPS projection of $1.67, we believe that there is still excellent upside potential from here.

While an upward rerating in its valuations nearer to TSLA's 1Y P/E mean of 47.71x is unlikely, the former's speculative price target may more than double to $79.67, implying an extremely attractive value play, despite the rally thus far. That may be great news indeed.

Naturally, these estimates are hypothetical, due to BYD's Chinese ADR status and the volatile geopolitical situation. Therefore, the stock's performance may remain subpar compared to TSLA's, with Warren Buffett's Berkshire Hathaway ( BRK.A ) ( BRK.B ) continuing to sell its existing stake down from the original 7.7% to 3.4% by June 27, 2023.

As a result, while we continue to rate BYD stock as a Buy, investors must also calibrate their expectations accordingly.

For further details see:

BYD: A 2-Horse EV Race With Tesla - Great Upside Remains