BYDDY - BYD: Buy The Dip

2023-12-05 08:04:03 ET

Summary

- BYD's stock has declined due to sentiment toward Chinese stocks, but the company's fundamentals keep improving.

- BYD continues to break production and delivery records and will likely deliver more than 3 million clean energy vehicles in 2023.

- My valuation analysis suggests the stock is almost two times undervalued.

Investment thesis

My initial bullish thesis about BYD (BYDDY) aged poorly, as the stock tanked by almost 17% since early September, significantly lagging the broader U.S. market. However, the decline is mostly due to the sentiment towards Chinese stocks, as the iShares China MSCI ETF (MCHI) declined by 10% over the same period. However, my updated analysis suggests that the adverse movement in the stock price is unrelated to the company's fundamentals. The company continues to break production and financial records, and near-term prospects also look bright. From the secular standpoint, the company is also well-positioned to continue absorbing a massive secular shift towards clean energy. Furthermore, my valuation analysis suggests the stock is about two times undervalued. Investing in Chinese stocks is inherently risky, but I think the upside potential here far outweighs all the risks and uncertainties. All in all, I reiterate the "Buy" rating for BYDDY.

Recent developments

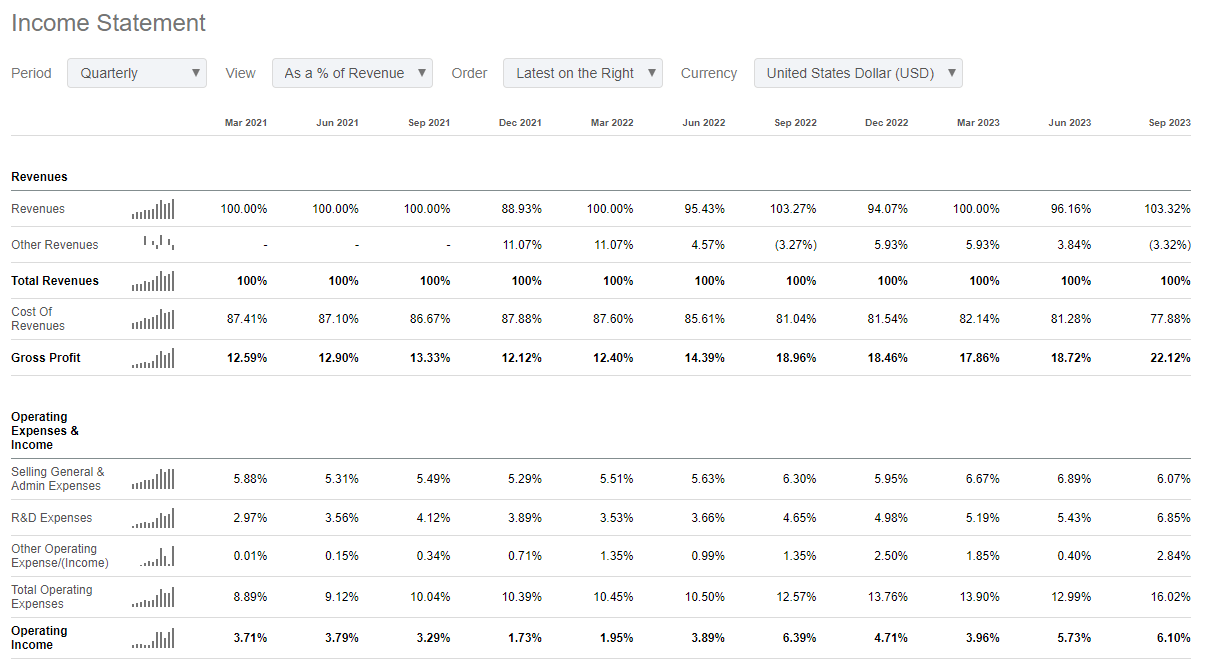

The latest quarterly earnings were released on October 31, when the company missed consensus revenue estimates. Revenue grew YoY by a massive 38%, which allowed it to expand the net profit to around $1.42 billion. This represents a staggering 82% YoY net profit growth. The company continued demonstrating solid operating leverage, with the gross margin expanding YoY from 18.5% to 22.1%. The operating margin was about flat, but this was due to the increased spending in R&D, which offset the improved SG&A to revenue ratio. R&D expenses are investments in innovation, which will highly likely build value for shareholders over the long term. That said, I do not consider YoY stagnation in the operating margin to be a red flag.

{kind=link}

The strong financial performance dynamic is explained by rapid growth in deliveries. The company continued breaking production and delivery volume records in Q3 as the total deliveries surpassed 2 million vehicles during the first nine months of 2023, representing a 76% YoY growth.

A stellar quarter ensured BYDDY continued building up its bulletproof balance sheet. The company has a strong $9 billion outstanding cash position with low leverage. Short-term liquidity also looks solid. BYD's stalwart financial condition makes the company strategically positioned to continue investing substantial amounts in innovation and new model development.

Seeking Alpha

The earnings release for the upcoming quarter is scheduled for March 25, 2024. Quarterly revenue is expected by consensus at $25.73 billion, indicating a solid 13% YoY growth. The bottom line projections are not indicated, but given the company's strong track record of delivering operating leverage, I expect profitability metrics to follow the top line.

Seeking Alpha

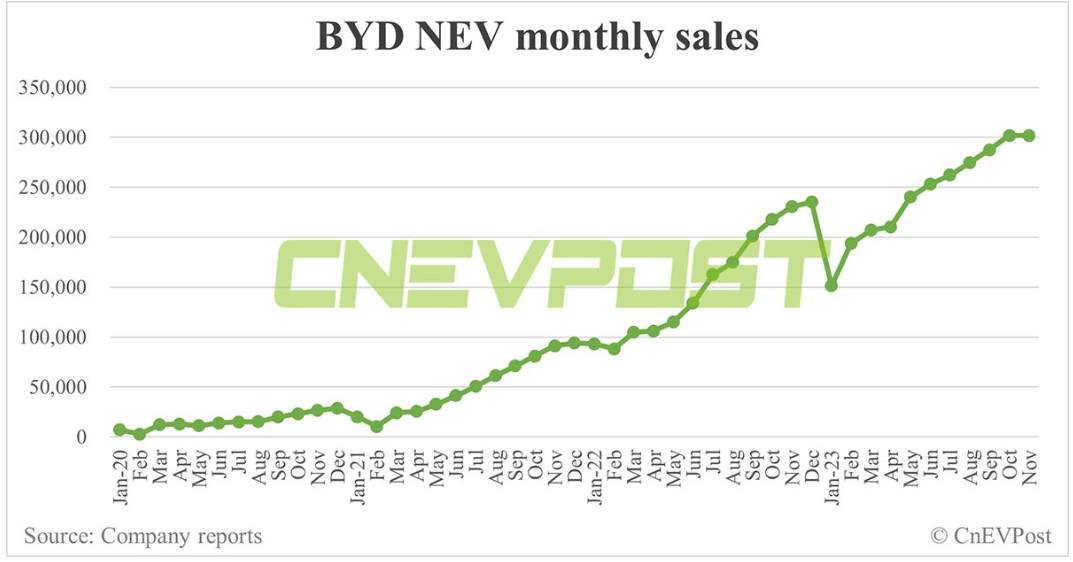

I like analyzing automotive companies because they share their monthly volume sales, and all substantial price changes can also be seen on the Internet. That said, it makes it easier for an analyst to forecast whether the company will be able to deliver stellar quarters again or not. October sales were strong again, with the company surpassing 300 thousand vehicles in quarterly deliveries for the first time in history, representing a 38% YoY growth. November deliveries were approximately flat sequentially but represented a 31% YoY growth.

{kind=link}

The momentum for BYD vehicle deliveries is strong, and based on the trendline above, we can see that last year's December deliveries were slightly above November. I am a conservative investor, so I assume BYD will deliver the same 300 thousand vehicles in December 2023, which will mean about 28% YoY growth compared to 235 thousand vehicles delivered in December 2022. That said, around a 30% quarterly YoY boost is expected from the volume side of the revenue equation. Now let me look at the recent developments from the selling price side. As the competition and the price war with Tesla intensified, BYD cut prices in Q4 on average at about 10% . That said, even if we offset the average selling price decrease against the volume growth, the YoY Q4 revenue growth is expected to be around 17%. While my calculations are rough and high-level, BYD will likely surpass Q4 consensus revenue estimates. Given the company's strong operating leverage demonstrated in recent quarters, I also expect profitability metrics to expand.

While my initial thesis was called "BYD: Poised To Be King In The Chinese EV Market", recent developments suggest that the company also has very ambitious overseas plans. According to electrek.co , BYD aggressively expanding into international markets and is already leading in overseas markets like Thailand, Brazil, and Columbia. The company also shared its bold plans over the long term to outsell Toyota ( TM ) in Australia, one of the world's top 15 largest economies and one of the world's top wealthiest countries. For BYD pessimists, comparisons with Toyota, who sold more than 10 million vehicles globally in 2022, might look very funny. But let us not forget that the gap between BYD and TM is closing rapidly. The Chinese giant will likely achieve 3 million deliveries in 2023, which looks unbelievable compared to less than 600 thousand NEVs delivered in 2021.

BYD stock valuation

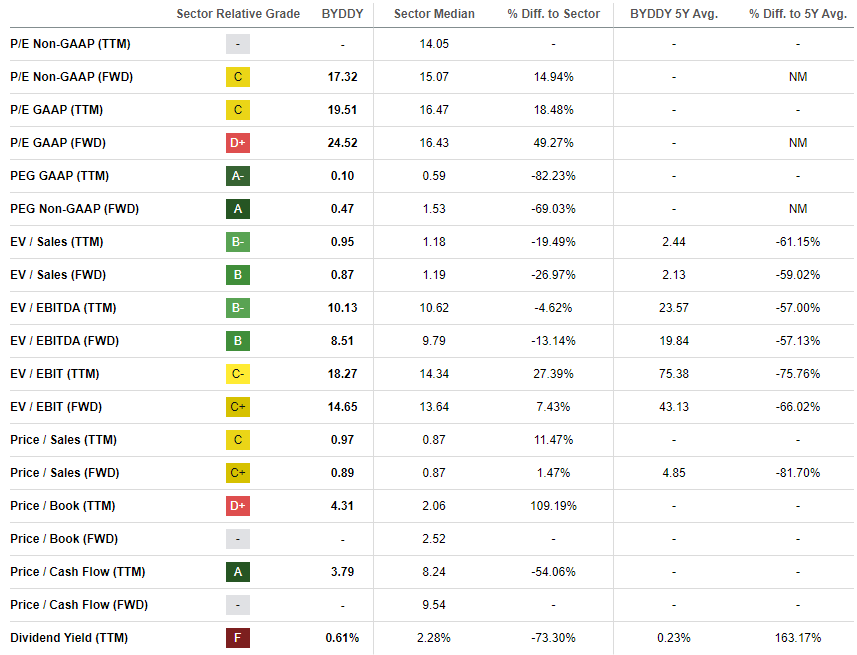

BYDDY rallied by a modest 3.7% year-to-date, significantly underperforming the broader U.S. stock market. However, BYDDY's performance has been strong this year compared to MCHI, which declined by 15% year-to-date. The stock looks very attractive from the perspective of valuation ratios , especially compared to BYDDY's historical averages.

{kind=link}

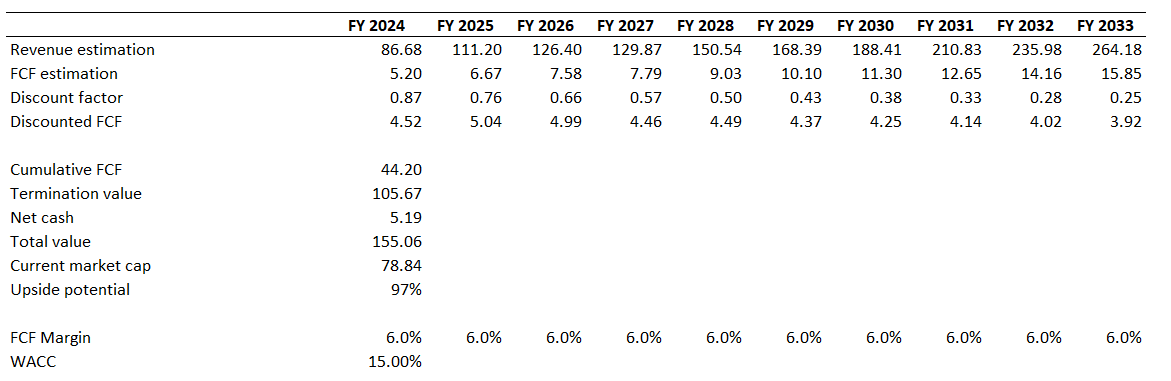

I want to proceed with the discounted cash flow [DCF] simulation. I use a very high 15% WACC for discounting due to inherent political risks related to investing in Chinese companies. Consensus revenue estimates forecast a 13% CAGR for the next decade, which I consider fairly conservative for my calculations. I use a flat 6% FCF margin for the whole decade, which is very conservative considering the expected revenue growth.

{kind=link}

According to my DCF valuation, the business's fair value is $155 billion. This is two times higher than the current cap, with an upside potential of 97%. That said, my target price for BYDDY is $105.

Risks update

As a Chinese company, BYDDY faces substantial political and geopolitical risks. China is not a democratic country since the political system is a one-party system, where the Chinese Communist Party [CCP] is the sole ruling party. In a one-party system, the political power is concentrated in a limited number of hands, meaning that decisions can be made quickly without the need for extensive consultation or consensus-building. That said, adverse changes to laws and regulations for companies like BYDDY might occur suddenly. For instance, the Chinese government's generous policy concerning subsidies for EVs could undergo rapid revisions, potentially moving towards a reduction. Such a shift would be a significant adverse catalyst for the company."

Geopolitical factors, especially tensions between China and the U.S., also bring high uncertainty for potential investors. Several technological bans prohibiting investments and exports from the U.S. to China are already working, and there is little certainty regarding the battle in the EV field. Some bans and restrictions from the U.S. government can expand into the EV industry, which will also not benefit BYDDY.

Bottom line

To conclude, BYD is a "Buy". My valuation analysis suggests that the recent pullback in the stock price provides an appealing investment opportunity, as the stock price has the potential to almost double in the foreseeable future. BYD's fundamentals keep improving, and the company's financial position makes it well-positioned to continue investing in growth and innovation. Political and geopolitical risks related to investing in Chinese stocks are significant, but the upside potential outweighs these risks, in my opinion.

For further details see:

BYD: Buy The Dip