BYDDY - BYD Company Limited: Poised To Weather The Chinese EV Price War

2023-06-06 09:56:31 ET

Summary

- BYD continues to engage in a fierce price war with its Chinese EV peers.

- Early signs indicate BYD is winning, with volumes again up significantly in May.

- Having lagged the broader EV rally, valuations screen very reasonably here.

BYD Co Ltd (BYDDF), the Chinese market leader in electric vehicles and the #2 player in EV batteries, has seen its shares underperform over the last year amid concerns over demand headwinds and heightened competitive pressures throughout the industry. With valuations down to ~20x fwd earnings, though, BYD stock may already have discounted a pessimistic view of its mid-term earnings growth path (EPS on track to nearly double through 2025).

Yet, the qualities that made BYD a great investment haven't changed - the company remains the most competitive EV player in China, supported by its integration across the EV value chain and robust pipeline. Ongoing price cuts are a near-term concern for margins, but it's important to remember that BYD is triggering these cuts, helped by cost savings from lower lithium prices. Based on recent months' sales numbers, the price/volume tradeoff is working in its favor, allowing it to gain mass market share vs. its peers through a downcycle. Plus, there remains ample room for growth externally (i.e., via exports), while further lithium price downside should continue to boost margins and pricing power. Investors may have to endure some pain in the meantime, but given that BYD's earnings power remains intact (potentially even enhanced once the dust settles and the Chinese EV market consolidates), those willing to stick it out should be well-rewarded.

Price Cuts Boost Volumes Again in May

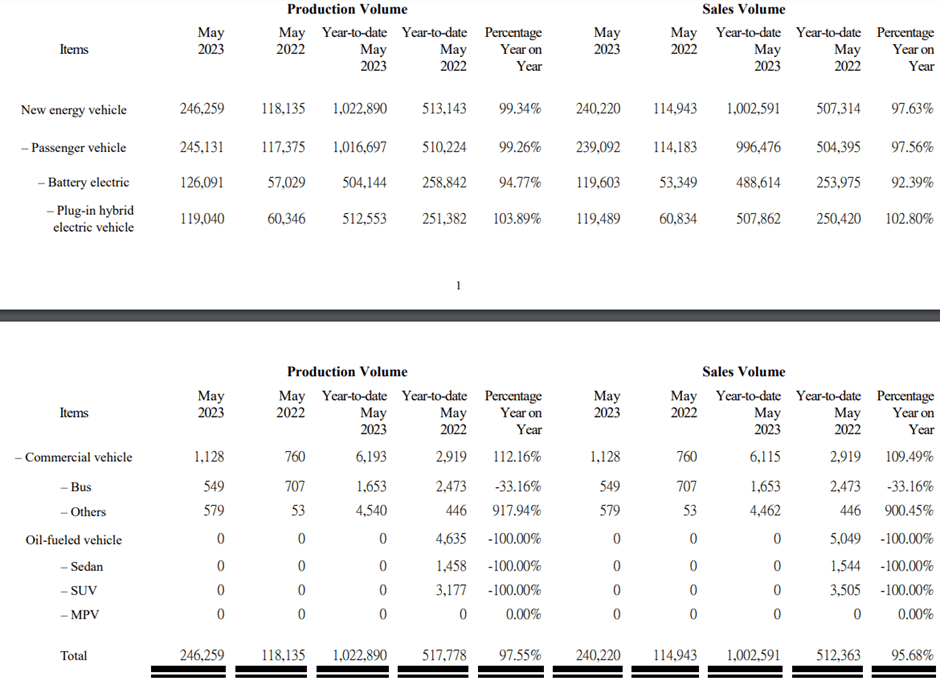

Having started the year facing domestic retail volume pressure, BYD management began a series of price cuts across its model lineup, starting with a low-teens percentage cut to its 'Qin plus' sedan. With the <RMB100k price point making the 'Qin plus' now the lowest-priced plug-in hybrid in China, the model has since emerged as China's best-selling PHEV at >40k unit sales in April. Since then, BYD has implemented similar price cuts to boost volumes across its lineup, most recently, the Song pro DM-i SUV (by a low-single-digit percentage) in May. The cuts are beginning to yield outsized volume gains across the board - BYD's May EV sales hit ~240k units, while on a YTD basis, EV sales are already up to ~1m units. Similarly, BYD continues to make inroads on the EV battery side, growing its installed capacity at a high-double-digits percentage YoY pace and gaining share vs. the market leader CATL.

{kind=link}

The wave of BYD price cuts isn't over just yet - the company began last month with the launch of a facelifted 'Seal ' electric sedan (the 'Championship version'), with price cuts taking the headline price point to a highly competitive <RMB190k starting point ( ~18% below the Tesla ( TSLA ) Model 3). Competitors will inevitably respond, though BYD's scale and integration across the value chain mean few will be able to match these price adjustments sustainably. Also, expect BYD's price points to begin to eat into the internal combustion engine share of the overall auto vehicle market in China, moving the company closer to its #1 volume ambition across all segments. Still, reaching the 2023 volume target of 3m units (vs. 1.86m in 2022) will be a challenge; with BYD's Chairman also describing China's EV price war as approaching a 'knockout stage,' more aggressive price cuts are likely on the horizon. Going forward, I'd keep an eye out for any price adjustments at the higher-margin brands (e.g., Denza and the upcoming 'F-brand') , in addition to the mass market BYD brands, where volume contribution is the clear priority (over maximizing profit).

Profitability Unsurprisingly Down QoQ; Margin Outlook Helped by Lithium Price

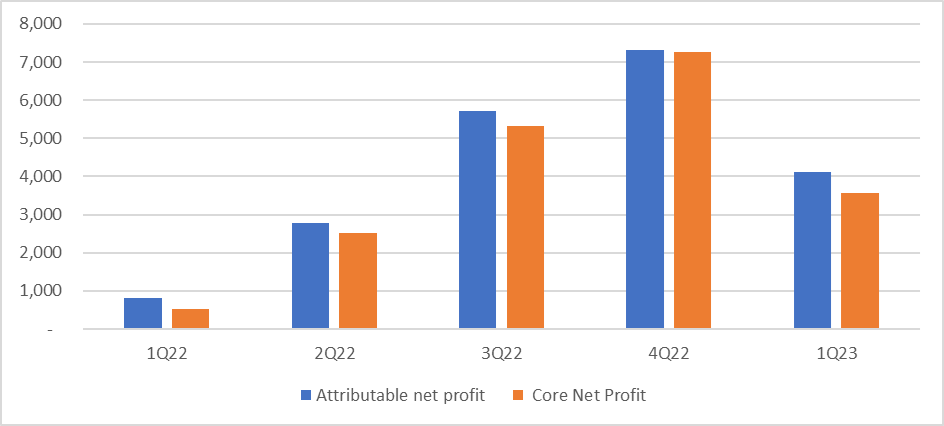

Of note, BYD's May sales report came on the heels of a sequential net profit decline in Q1 (~30% QoQ on a per unit basis; ~44% QoQ reported). There were several one-offs weighing on the bottom line, though, including impairments, investment gains, and FX, among others. Beyond these, the sequential profit decline was also caused by volume headwinds (wholesale), as well as lower gross margins from the government EV subsidy removal and BYD's retail price cuts. The biggest P&L reprieve, on the other hand, was lithium carbonate prices, which declined in the low-double-digits sequentially, allowing for the massive price cut/share gain strategy implemented through Q1.

{kind=link}

Given the tailwind from continued lithium carbonate price weakness through Q1, which should unlock significant battery cell cost savings, BYD should post higher sequential gross profits in the coming quarter. How much of the cost savings from lithium and parts components will be passed on via price cuts is the key question, though, as management has been explicit about its focus on market share this year, particularly for its mass-market products. Also in question is how the competitors will respond - key rival Great Wall Motor (GWLLF), for instance, has recently started a regulatory tit-for-tat with BYD, filing complaints about the emissions standards of its 'Qin Plus' and 'Song Plus' hybrid models. For now, supported by its scale and cost advantages, it's hard to look past BYD emerging as the winner from the ongoing EV price war in China.

Poised to Weather the Chinese EV Price War

With BYD now trading down to a very reasonable ~20x P/E despite retaining its mid to long-term earnings power ( consensus EPS on track to hit >RMB15/share through 2025), the stock is worth a look. To be clear, there are near-term EV headwinds, including on the policy (lower subsidies from the Chinese government) and demand sides (due to the sluggish post-reopening recovery in China). The latter has even triggered a price war, with poor volumes earlier this year pushing BYD into passing on lithium-driven cost savings via price cuts across its product lineup. Yet, the structural tailwinds remain. BYD, helped by its integration across the EV value chain, remains China's most competitive EV manufacturer and is, thus, best positioned to ride out the near-term turbulence. In the meantime, incremental export contribution and accretive new product launches present revenue upside into Q2, while continued lithium price weakness is the key tailwind on the cost side.

For further details see:

BYD Company Limited: Poised To Weather The Chinese EV Price War