BYDDY - BYD: Poised To Be King In The Chinese EV Market

2023-09-01 15:49:27 ET

Summary

- BYD has surpassed Tesla as the largest EV maker in the world in terms of deliveries in 2023.

- BYD's wide variety of vehicle models and affordable options cater to a large audience in China.

- According to my valuation analysis, the stock is massively undervalued.

Investment thesis

BYD Company Limited ( BYDDF ) (BYDDY) in 2023 overcame Tesla ( TSLA ) as the global largest EV maker from the number of deliveries perspective. For me, as a big Tesla bull, it is impressive. I like BYD's strong market position, and I believe the moat is wide enough to absorb secular tailwinds related to the global shift to clean energy. The company's wide variety of vehicle models enables it to target a vast audience, and this year's stellar revenue growth suggests that such a broad diversification is a great asset for BYD. The company offers several cheap models, which are in high demand given the large portion of Chinese people being price sensitive due to relatively low salaries. Since shifts in the salary statistical distribution over the Chinese population are unlikely, I believe the demand for BYD's low-end models will remain consistently high over the long-term. BYD generates wide free cash flow and has a strong balance sheet, meaning the company is well-positioned to continue reinvesting in growth. The valuation is very attractive and I believe the upside potential significantly outweighs the risks of investing in Chinese stocks.

Company information

BYD Company Limited and its subsidiaries are involved in the automobile business, which mainly includes new energy vehicles, handset components and assembly services, rechargeable batteries, and photovoltaics business.

The company's fiscal year ends on December 31. BYD disaggregates its revenue into two product categories: "Automobiles and related products" and "Mobile handset components, assembly service, and other products". In FY 2022, automobiles and related products represented almost 77% of the total sales. According to the latest annual report , the company generates about 22% of its sales outside China, Hong Kong, Macau, and Taiwan.

Financials

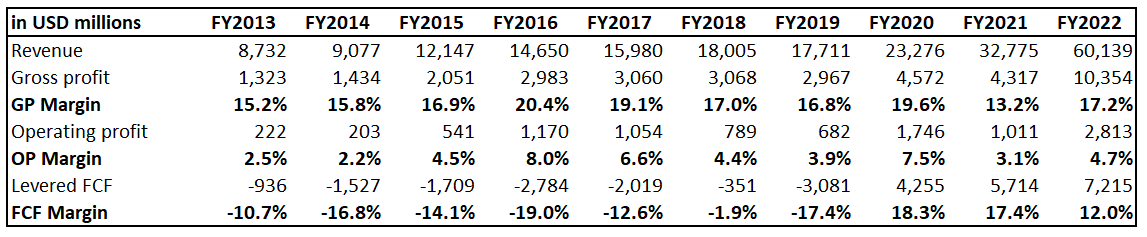

BYD is a hyperscale company with $60 billion in revenue in the latest fiscal year. Over the past decade, revenue compounded at an impressive annual 24% rate. The operating margin is razor-thin at mid-single digits, but I like how the free cash flow [FCF] margin has expanded, especially in the last three years.

{kind=link}

Having a solid FCF margin means the company is able to accumulate financial resources and build up a solid balance sheet. BYD is in a substantial net cash position with prudent leverage. Short-term liquidity metrics also look solid. The company pays out dividends, though payout history has been volatile over the past decade.

Seeking Alpha

BYD demonstrates strong revenue growth momentum with $19.2 billion in sales in Q2 FY 2023, which indicates a 58% YoY growth. The momentum is expected to continue in Q3. Quarterly revenue is expected at $23 billion, which is a 44% YoY growth. As the business scales up, profitability metrics also demonstrate expansion. The gross margin expanded YoY from 14.39% to 18.72%. The operating margin also followed, expanding from 3.89% to 5.73%. As a result, quarterly operating cash flow doubled, from $4.6 billion to $9.3 billion. The levered FCF in the last quarter was close to $6 billion, which is also massive.

The company's revenue expansion looks impressive, especially considering the softness of the broader Chinese economy and a price war from Tesla. I like that the company successfully responds to the rising demand for its vehicles and converts revenue growth into profit growth. In the first half of 2023, net profit has tripled . Revenue grew 73% in H1 of 2023 compared to the year earlier.

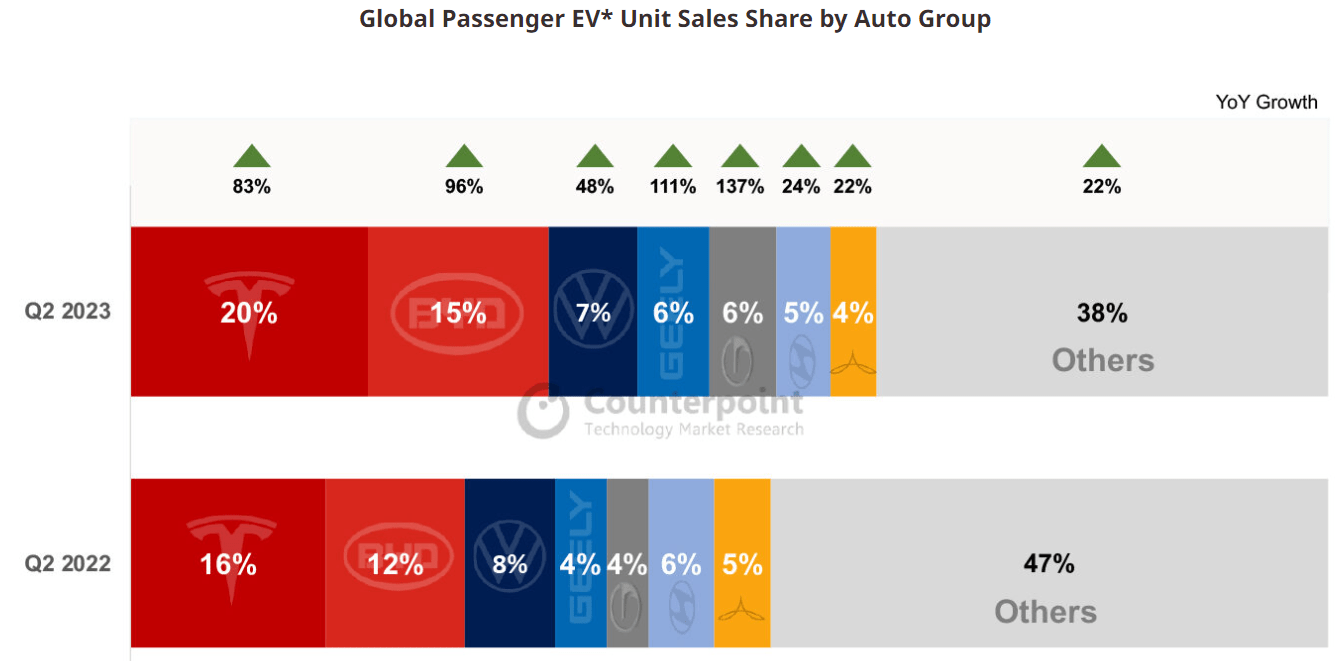

BYD operates in a booming market, demonstrating a 50% YoY growth globally in Q2 2023. The Chinese EV market underperformed due to macro challenges, but the growth rate was still strong at 37%. A booming market means there are a lot of players who are willing to bite a big piece of the rapidly increasing pie. But Q2 global market share dynamics suggest there are two beasts that are notably expanding their market shares: BYD and Tesla.

{kind=link}

I think BYD's success is explained by the broad portfolio of offerings, including the "Seagull" model, which costs only $11 thousand and is one of the cheapest vehicles overall. Apart from "Seagull" BYD offers customers various vehicles, including sedans and SUVs of different sizes. That said, the company targets a considerable audience, considering the above one billion people Chinese population. The distribution of salaries in China is also an important factor. According to worldsalaries.com , 25% of the population earns less than 208,000 CNY annually, which is about $28,000. That said, a huge portion of the population is very price-conscious, and BYD's budget models look like a good choice. The company's mega scale with high production capacity also gives the company a solid moat. Therefore, I believe the company is well-positioned to outperform the Chinese EV market growth, which is projected to compound at 18.4% over the next five years.

Valuation

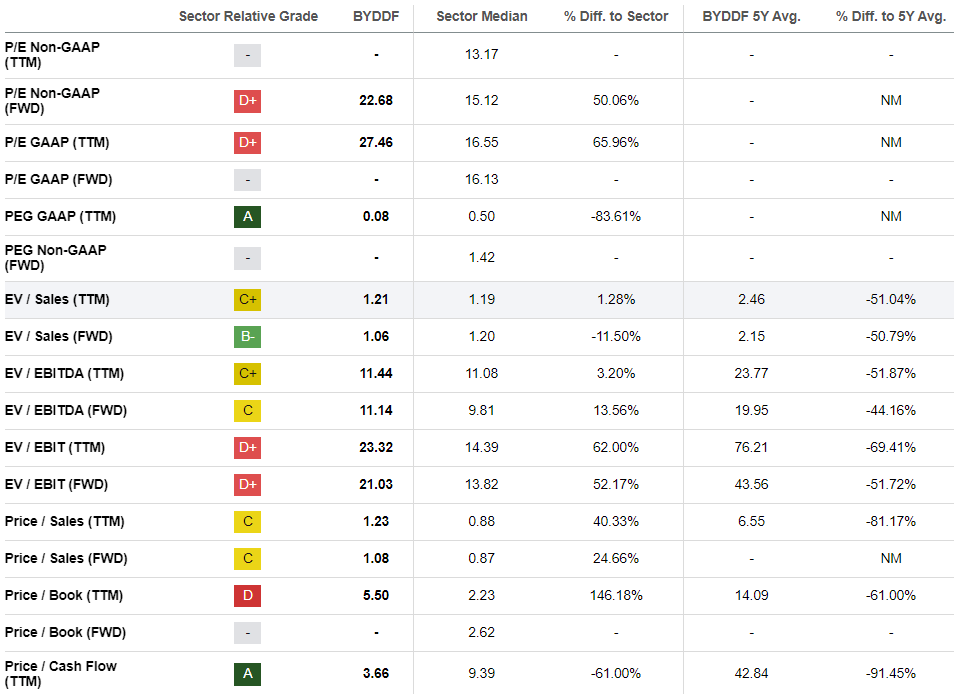

The stock rallied 23% year-to-date, significantly outperforming the iShares MSCI China ETF, which declined about 8%. Seeking Alpha Quant assigns BYD a low "D+" valuation grade despite its current multiples being substantially lower than historical averages. On the other hand, the company's valuation ratios are notably higher than the sector median.

{kind=link}

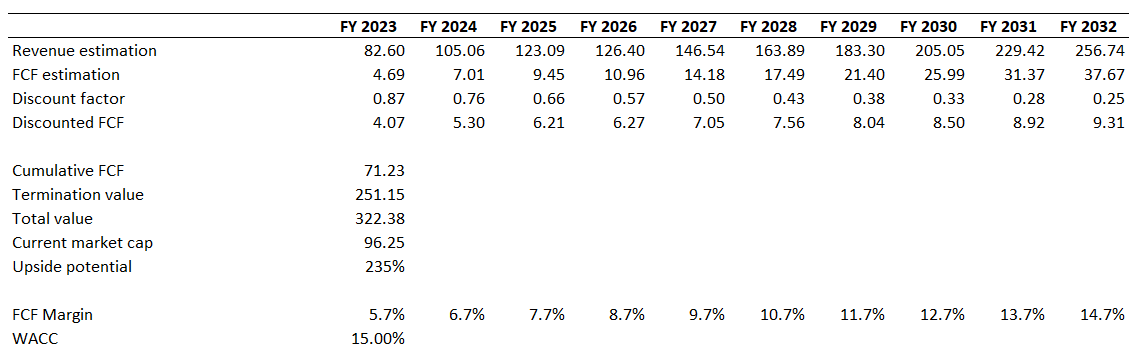

I want to continue my valuation analysis with the discounted cash flow [DCF] approach. I usually use a high 15% WACC for discounting for Chinese companies due to country-inherent risks. Consensus revenue estimates project a 13% revenue CAGR for the next decade, which I consider fair given the EV industry's tailwinds. I use the last five years' average for the FCF margin and expect it to expand yearly by one percentage point.

{kind=link}

According to my calculations, the company's fair capitalization is above $300 billion. That said, I believe the stock has an upside potential to more than triple since its current market cap is slightly below $100 billion.

Risks to consider

As a Chinese company, BYD faces significant political risks. China is not a democratic country, meaning that vast political power is concentrated in the hands of a small group of individuals. This creates vast uncertainty for companies like BYD because policy changes and regulatory decisions might be made without public discourse or clear justifications in non-democratic regimes. The absence of public discourse means there is a high probability that shifts in policies and regulations might be sudden, and it will be difficult for a large company like BYD to adapt in a timely manner. Failing to comply with changes in regulations on time might lead to litigations and penalties.

Geopolitical tensions between China and the developed economies, which we have seen in recent months, might mean that BYD's international expansion opportunities might be limited. Tensions between China and the developed world might also weigh on the company's ability to innovate over the long term.

Bottom line

To conclude, BYD is a "Buy". I like the company's strong positioning in the largest EV market in the world. BYD demonstrates stellar revenue growth amid vast macroeconomic uncertainty in China, which is a solid bullish sign. The company is able to absorb the increased demand due to its extensive production capacities. I am highly convinced that the company can absorb secular industry tailwinds. Last but not least, the company's fair value is far above the current market cap, meaning the stock price has a massive upside potential in my view.

For further details see:

BYD: Poised To Be King In The Chinese EV Market