BYDDY - BYD Took Tesla's EV Crown With More Growth To Come

2024-01-12 09:40:03 ET

Summary

- BYD outperformed Tesla in Q4 2023, becoming the world's leading EV manufacturer with record-breaking sales of 526,000 BEV units.

- BYD's strong performance was driven by a supportive EV backdrop in China and successful international deliveries.

- The company is expected to see further growth upside in 2024, with supportive EV demand in China and potential margin expansion.

- Anchored on a residual earnings model, I argue that BYD shares could be about 70% undervalued.

In Q4 2022, I argued that BYD is a "Buy", given the company's exceptional growth outlook and cost advantage over Western carmakers. Since then, the stock has not performed so well, although the underlying fundamentals improved as projected. Today I provide an update on my BYD thesis.

BYD Company Limited (BYDDF) saw robust growth in 2023, outperforming Tesla in the December quarter and claiming the title of the world's leading EV manufacturer. This surge in performance was propelled by both a supportive EV backdrop in China, as well as success in international deliveries. Heading into 2024, BYD is poised to see further growth upside, as EV demand in China is expected to remain supportive, while macro variables gradually improve. Moreover, I am bullish on BYD's ability to expand margins, as battery input prices drop and economies of scale effects kick in. I recommend shares as a "Buy".

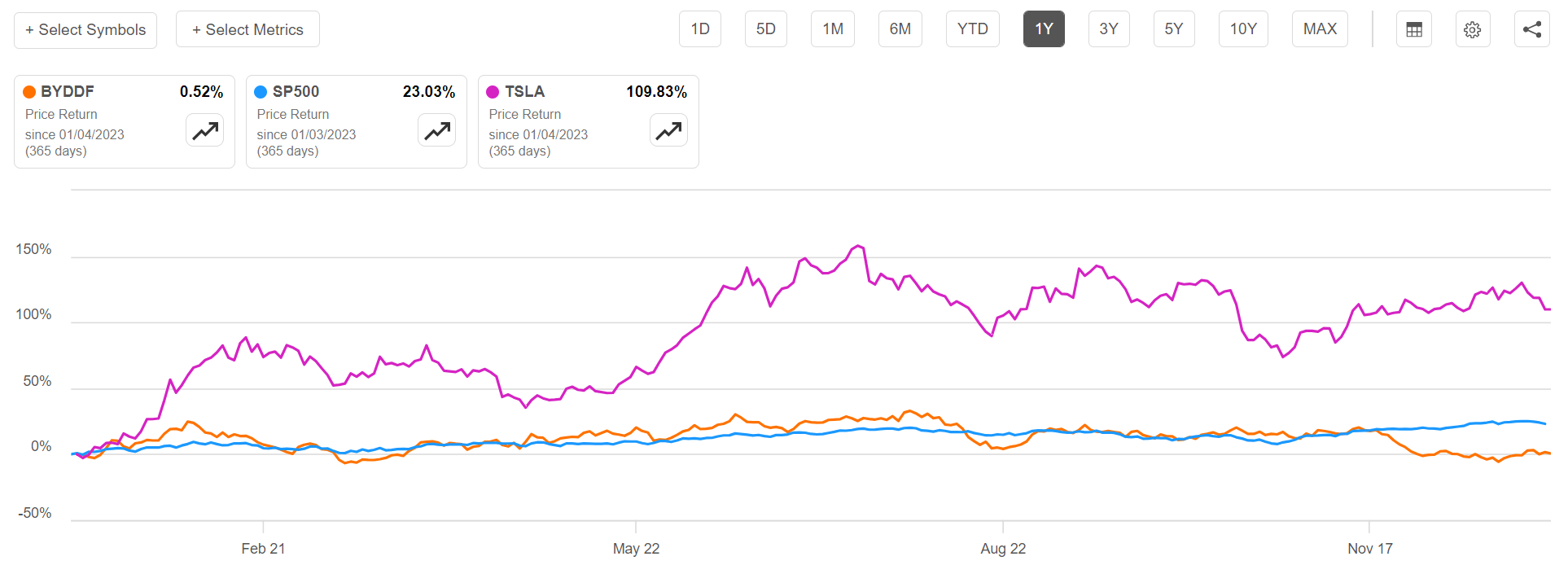

For context, BYD stock has underperformed in 2023. For the trailing twelve months, BYD shares have traded about flat, compared to a gain of approximately 23% for both the S&P 500 ( SP500 ) and a crushing gain of about 110% for key U.S. competitor Tesla, Inc. (TSLA).

{kind=link}

BYD Performs Strongly: Topping Tesla As The Leading EV Maker

Despite a challenging macro backdrop, BYD has performed exceptionally well in 2023. In fact, in the December quarter, BYD even managed to take Tesla's crown as the world's leading EV manufacturer. While, Tesla delivered 484,000 cars in the fourth quarter, surpassing analysts' expectations, BYD shipped a record-breaking 526,000 BEV units to customers. In all of 2023, BYD sold a total of 3.02 million vehicles, showing a remarkable 62% increase from the previous year and meeting the company's ambitious 3 million unit target. Moreover, investors concerned about BYD's exposure to China will certainly appreciate that sales outside of China were especially good, hitting a new high of 36,000 units in December, totaling 243,000 units for the entire year, and surpassing the company's 200,000 unit goal.

For the trailing twelve months, BYD's sales surged to $78 billion, compared to $46.5 million for the respective trailing 12-month period benchmarked September 2022, a 68% YoY jump. Meanwhile, operating profits jumped to $4.1 billion, a more than 100% YoY growth on positive operating jaws. Investors should consider that BYD has leveraged years of state support and strategic planning in Beijing to control the supply chain through nearly every resource necessary for manufacturing electric vehicles, including raw materials, battery components, and chips. BYD's full vertical value chain integration will likely be a key competitive strength vs. peers, as the price war in the industry intensifies.

Macro Backdrop Supportive Heading Into 2024

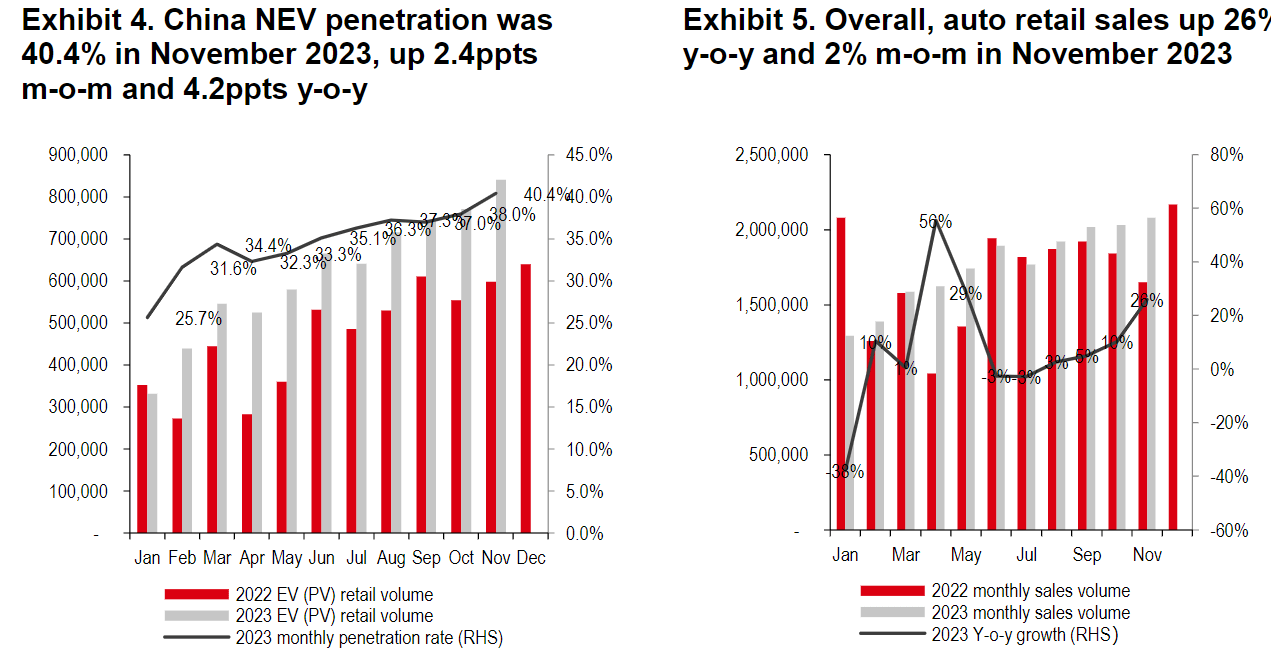

Looking into 2024, I remain bullish on BYD. And there are a few driving variables to this: First, I argue that pending interest rate cuts are supportive of demand, as investors should take into account that a significant portion of automobile purchases rely on credit financing. Therefore, reduced credit costs may positively impact consumer confidence and financing accessibility. Second, I continue to expect a very supportive EV demand backdrop in China, even amidst broader macro challenges. I point out that in November 2023, electric vehicle sales in China hit 840,500 units, equal to a 41% jump from the previous year. Month on month, growth was 9%, suggesting that demand is accelerating on an annualized basis ( Source: HSBC, equity research note dated 20th December: China EV Tracker). Notably, even if growth would slow vs. 2023, the market would likely still grow at a proud 20-30% YoY, providing an enormous volume tailwind to BYD.

{kind=link}

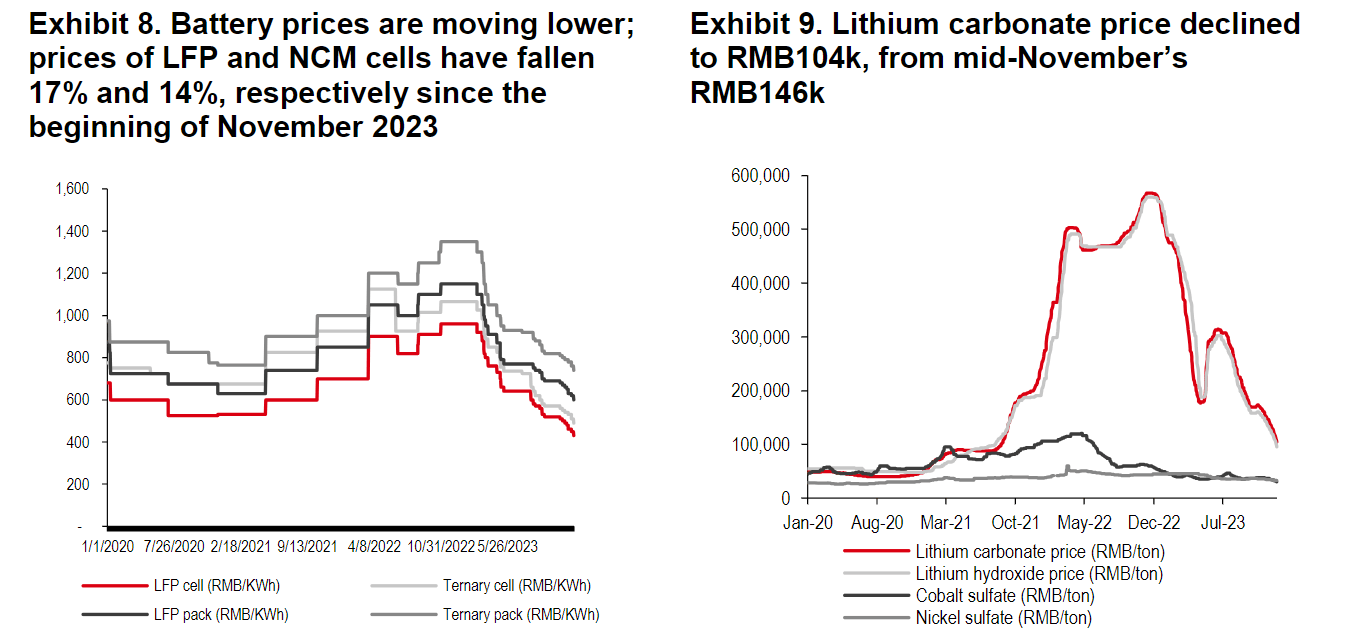

Admittedly, much of the strong EV volume growth in 2023 was attributable to various promotions and price reductions, as both the government and carmakers tried to render EVs more accessible to buyers. While I expect a similar trend in 2024, I see margin headwinds from price discounts offset by a lower cost base. Specifically, there's an expectation that the cost of EV batteries will improve further due to a correction in lithium prices, which have now dropped to around 100,000 per ton ( Source: HSBC, equity research note dated 20th December: China EV Tracker) . Moreover, as BYD's volume is growing, the company is in a position to leverage scale effects for a more supportive cost backdrop, e.g., through increased bargaining power vs. suppliers.

{kind=link}

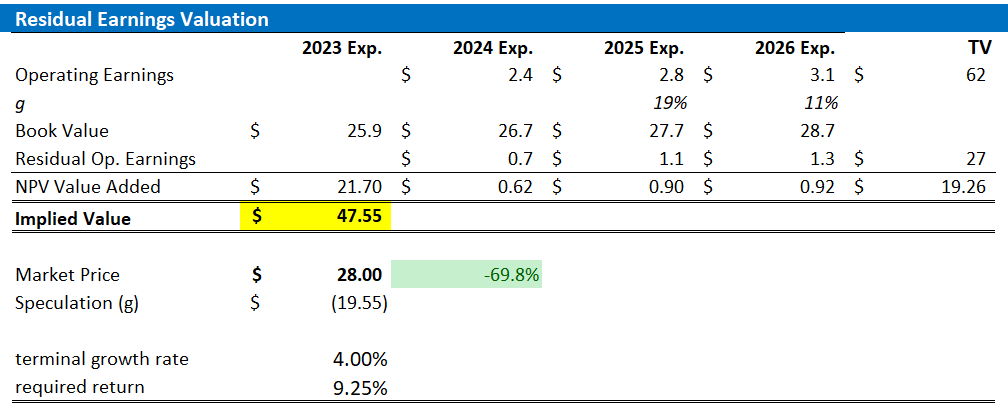

Valuation: Set TP At $47.55

Reflecting strong 2023 delivery and a bullish backdrop heading into 2024, I update my EPS projections for BYD in alignment with the latest analyst consensus estimates: For FY 2024, I now estimate that BYD's EPS will likely fall within the range of between $2.3 and $2.5 (non-GAAP). For FY 2025, and FY 2026 I set my EPS expectation at $2.8 and $3.1, respectively. Lastly, while I maintain my terminal growth rate input at about 150 basis points above the expected nominal U.S. GDP growth, at 4.0%, I raise my cost of equity assumption by 75 basis points, to 9.25%, mostly as a consequence of geopolitical tensions and concerns about the likelihood of acceleration price competition in the EV market. Moreover, I also think BYD's required return for investors should reflect a premium for geopolitical tensions.

Against the backdrop of the adjustments highlighted above, I now calculate a fair implied stock price for BYD stock equal to $47.55, suggesting approximately 70% upside based on fundamentals.

BYD financials, author's estimates and calculation

{kind=link}

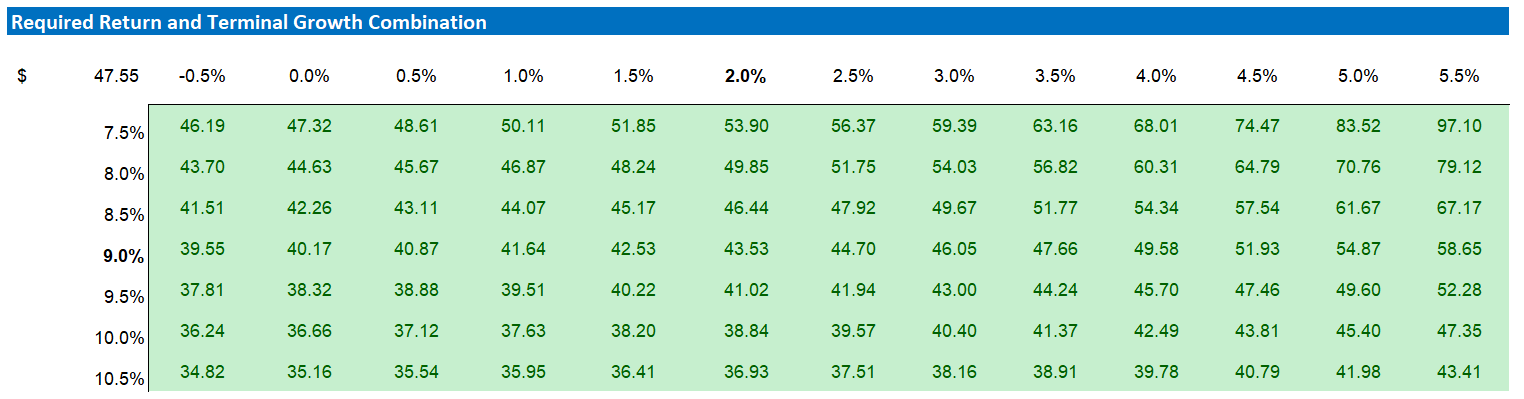

Below also the sensitivity table, which tests different assumptions for the cost of equity (row) as well as terminal growth rate (column).

BYD financials, author's estimates and calculation

{kind=link}

A Note On Risks

Like every equity investment, buying BYD stock comes with risks. Specifically, I highlight that the company is headquartered in China, which exposes the company not only to regulatory risks but also to geopolitical tensions. Moreover, investors should note that although BYD is internationalizing, the company still generates a large share of its sales in China, which exposes the company also to a somewhat weaker macro backdrop vs. the U.S. (as of early 2024). Furthermore, the EV landscape, both globally and in China, is witnessing intensified competition, with both new startups (NIO, XPeng, Lucid, Baidu, Xiaomi) and established automotive giants (Volkswagen, General Motors, Toyota) venturing into this market. If competition escalates, especially relating to pricing, the attractiveness of the EV sector from an economic standpoint will likely overshadow its robust growth. Lastly, fluctuations in BYD's stock price are largely influenced by investor sentiment toward Chinese ADRs and overall risk assets. This volatility might persist despite the company's unaltered business fundamentals.

Investor Takeaway

BYD outperformed Tesla in Q4 2023, becoming the world's leading EV manufacturer with record-breaking sales of 526,000 BEV units. BYD's strong performance was driven by a supportive EV backdrop in China and successful international deliveries. Heading into 2024, BYD is expected to see further growth upside, capturing a supportive EV demand in China and strong international sales traction. Additionally, I am optimistic about BYD's prospects for margin expansion, attributing it to decreasing battery input costs and the effects of economies of scale. Anchored on a residual earnings model, I argue that BYD shares could be about 70% undervalued. As a function of both commercial momentum and valuation, I assign a "Buy" recommendation.

For further details see:

BYD Took Tesla's EV Crown, With More Growth To Come