PLTR - C3.ai's Contrarian Strategy Is A Fundamental Short-Seller Trap

2023-10-12 11:44:34 ET

Summary

- C3.ai's stock has been on a winning ride alongside surging AI interest, but the company has underperformed fundamentally compared to industry peers.

- The company's profit margins have diminished due to a transition to a consumption-based revenue model and heavy investment in generative AI capabilities at a time of high capital costs.

- The stock's lofty valuation premium and weak underlying business fundamentals pose imminent downside risks, but its exposure to short-squeeze potential could mean a volatile ride ahead.

C3.ai ( AI ) has been a winning stock amid the AI frenzy since OpenAI's ChatGPT debut in November 2022. C3.ai's stock has more than quadrupled at its year-to-date peak before paring gains in recent months. Yet it still trades comfortably at more than double the value it had kicked off 2023 with, which significantly outperforms the broader market's resilient uptrend this year. And short-seller allegations earlier this year regarding C3.ai's lack of disclosures surrounding its related party transactions, alongside heavily related party revenue concentration, have done little to hold the shares back from their upsurge. Meanwhile, C3.ai's expanding contract portfolio in recent quarters, alongside ex-related party Baker Hughes' ( BKR ) reduction of its stake in the company to under 5% has also helped dissolve investors' concerns over the allegations.

However, despite being one of the biggest gainers this year on the coattails of AI momentum, C3.ai has underperformed fundamentally relative to rivals providing similar AI software and enterprise solutions. Despite generating positive cash from operations, the company remains unprofitable, with profit margins dragged primarily by hefty stock-based compensation expenses in recent years. This largely differs from the ongoing implementation of aggressive cost reduction initiatives and disciplined spend management observed at C3.ai's peers this year, driven by brewing macroeconomic uncertainties and tightening financial conditions. Management's seeming focus on growth at all costs, citing the need to prioritize capitalization of burgeoning AI opportunities, despite ongoing macroeconomic uncertainties also diverges from peers' demonstration of comparable growth in recent quarters, from a Bloomberg piece.

Now after careful consideration with our leadership and our marketing partners, we have made the decision to invest in Generative AI…and to invest in market and customer success related to our Generative AI solutions. The market opportunity is immediate and we intend to seize it. So while we still expect to be cash positive in Q4 this year and in fiscal year '25, we will be investing in our Generative AI solutions and at this time do not expect to be non-GAAP profitable in Q4, '24…but you're going to see this happen in some place in the Q2 to Q4 time frame of fiscal year '25.

Taken together, the combination of weak underlying business fundamental prospects and the stock's lofty valuation premium at current levels makes a recipe for imminent downside risks in our opinion. However, this is likely to be offset by the stock's potential as a prime candidate for an impending short squeeze given underlying market conditions, which underscores its exposure to substantial volatility in the near term.

C3.ai's Fundamental Roadmap is Weak

Disciplined spend management has been a key driver of corporate strategies this year - especially amongst high growth software companies with much of their valuation prospects underpinned by cash flows further out in the future, and high susceptibility to rising borrowing costs. Yet C3.ai strays from this trend.

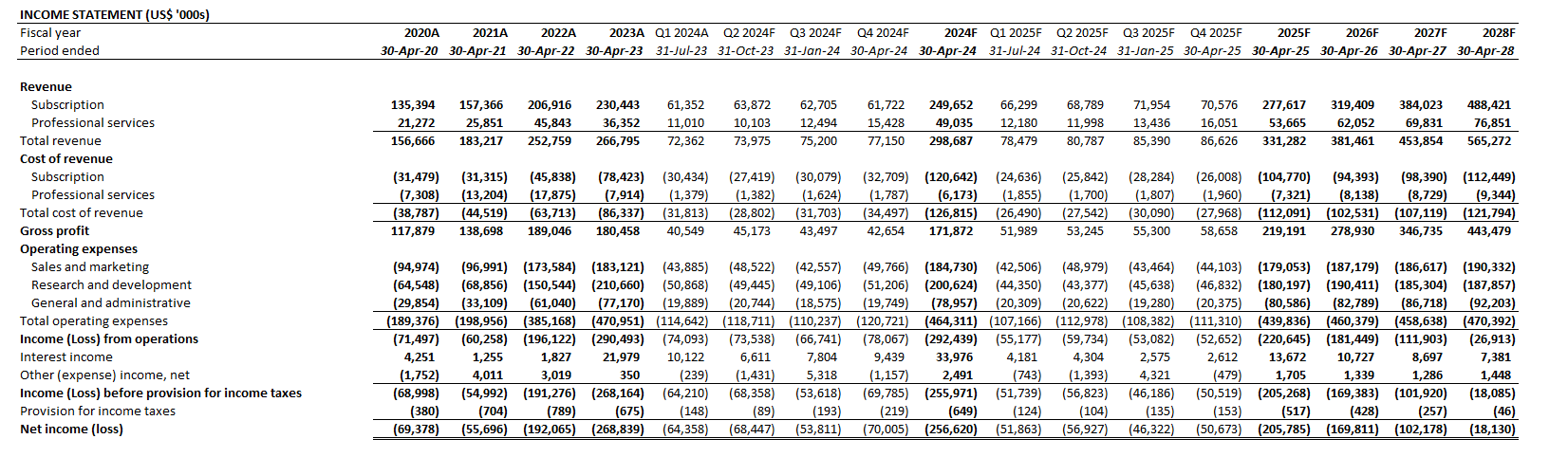

The company's profit margins have diminished in recent quarters, impacted primarily by its transition to a consumption-based revenue model during fiscal 2Q23. And management does not expect these headwinds to subside until the revenue mix becomes consumption-dominant. Although consumption volumes since the transition have performed better than management had initially expected, C3.ai's margin contraction in recent quarters implies continued pressure on profitability over the near term - especially as revenues continue to reflect a higher mix of "pilot phase" customers, with the transition to vCPU consumption-based billing still a few quarters out.

Meanwhile, the company is also undergoing an intensive investment cycle into building out its generative AI capabilities. This includes the recent rollout of a comprehensive suite of C3 Generative AI applications compatible with reputable and commonly used data systems (e.g., Palantir , Salesforce , Snowflake ) across an expansive portfolio of industries and asset bases, serving both the public and private sectors. The C3 Generative AI pilots start at an upfront fee of $250,000 and range up to $500,000 when bundled with the remainder of C3.ai's enterprise products. It takes 12 weeks to fully deploy the applications, and customers are billed $0.35 per vCPU / vGPU hour post-pilot under the consumption-based revenue model. This implies a potentially extended timeline to scale the newly introduced generative AI solutions, while C3.ai transitions its business model at the same time which underscores continued margin pressure within the foreseeable future.

This differs drastically from the high-volume contracts in the past, which provided greater visibility into C3.ai's growth prospects. With TCV expected to diminish over time as the transition to consumption-based billing takes place, C3.ai's growth trajectory will become increasingly dependent on customer adoption of incremental vCPU / vGPU volumes post-pilot, and more exposed to risks of fluctuations. Recall from our previous discussion on the pros and cons of consumption-based revenue models that they are inherently recession-prone, given the flexibility provided to customers to easily scale up/down usage volumes. This effectively drives up the execution risks of C3.ai's ongoing transition, as it coincides with an economic downturn, which would inadvertently impact its timeline to alleviate the relevant near-term margin pressures.

Prospects for achieving non-GAAP operating profitability, which is critical for bolstering C3.ai's fundamental self-sufficiency, are also further complicated by its surging SBC expenses. The company currently extends SBC in the high double-digit percentage range of revenues, which is substantially greater than industry averages . The acceleration observed in recent quarters is largely in line with management's increasing focus on the development and deployment of enterprise AI software, which suggests incremental SG&A and R&D spend within the foreseeable future, with much of it likely attributable to personnel costs and, inadvertently, SBC.

Taken together, C3.ai's uncertain trajectory to sustained profitable growth makes it an underperformer among peers like Palantir, which has pulled off an impressive turnaround in cost management this year. Its rivals have also been able to maintain a similar path of revenue growth enabled by AI-driven TAM expansion over the past year, while implementing a measured cost structure. Considering C3.ai's differentiated take under the current market climate, we expect the company to turn only nominally profitable on a non-GAAP basis exiting fiscal 2025. Although the assumption is relatively conservative compared to management's target for positive non-GAAP operating income by mid-fiscal 2025, it already considers significant operating leverage improvements over the next four to six quarters. Our base case forecast estimates significant reductions in SG&A and R&D expenses entering fiscal 2025 based on the expectation that generative AI deployment ramp-up efforts will start to normalize as a greater volume of customer agreements enter post-pilot phase, while relevant SBC spend will also start to scale.

{kind=link}

{kind=link}

C3.ai_-_Forecasted_Financial_Information.pdf

Despite management's expectations for C3.ai's cash flows from operations to stay positive going forward, their margins relative to the company's near-term growth prospects also underperform peers'. Specifically, elevated capex spend on generative AI investments as well as the build-out of C3.ai's new headquarters in the near term will remain a headwind to cash flows. This is corroborated by already negative FCF observed in recent quarters, which bodes unfavourably for the stock's lofty valuation premium at current levels.

Weak Durability to C3.ai's Valuation Premium

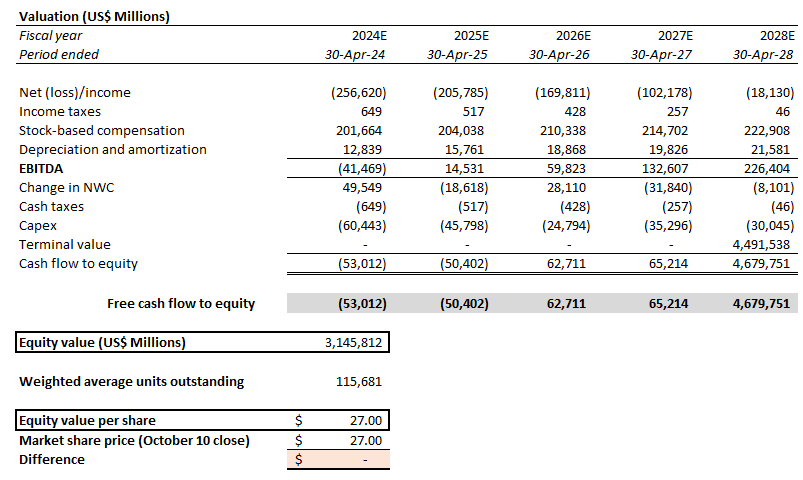

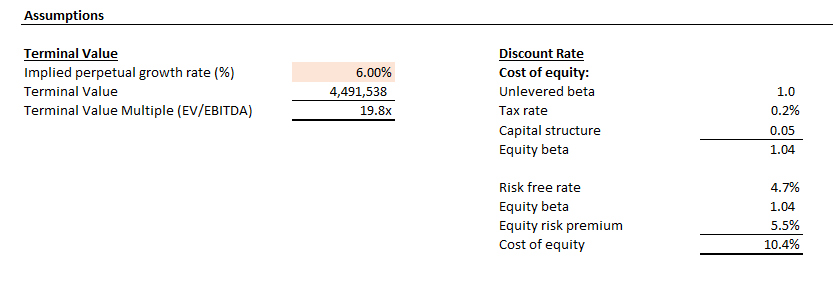

Under the discounted cash flow valuation approach, the stock's current price in the $26 range implies a perpetual growth rate of 6%, or terminal valuation multiple of almost 20x. The computation applies projected cash flows taken in conjunction with our fundamental forecast for C3.ai discussed in the foregoing analysis, and assumes a WACC of 10.4% in line with the company's capital structure and risk profile.

{kind=link}

{kind=link}

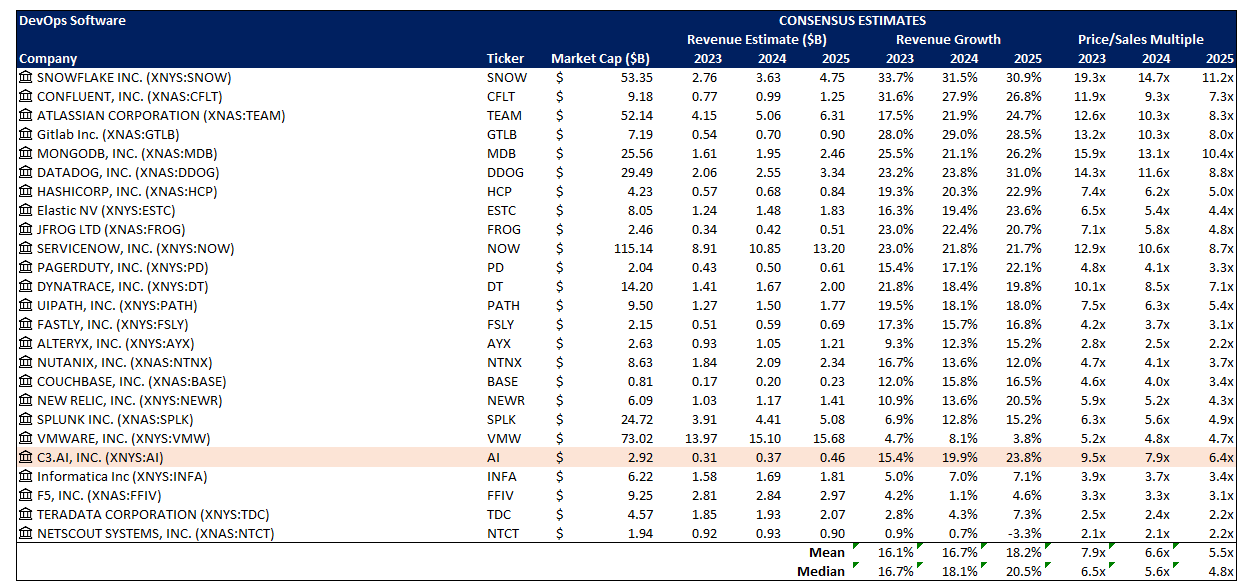

The implied growth rate of 6% significantly exceeds the 3% to 3.5% range typically attributable to the pace of economic expansion in C3.ai's core operating regions, and outperforms the average premium observed in its high growth software peers. Instead, implied multiple is closer to some of the market's biggest AI gainers this year like Nvidia ( NVDA ), or C3.ai's more comparable industry peer Palantir. However, C3.ai faces substantially softer fundamental prospects, which drives incremental caution over the durability of the stock's lofty premium at current levels.

Based on the consideration of C3.ai's peer multiple, the divergence of the company's underperforming growth from its valuation premium to peers is more evident:

{kind=link}

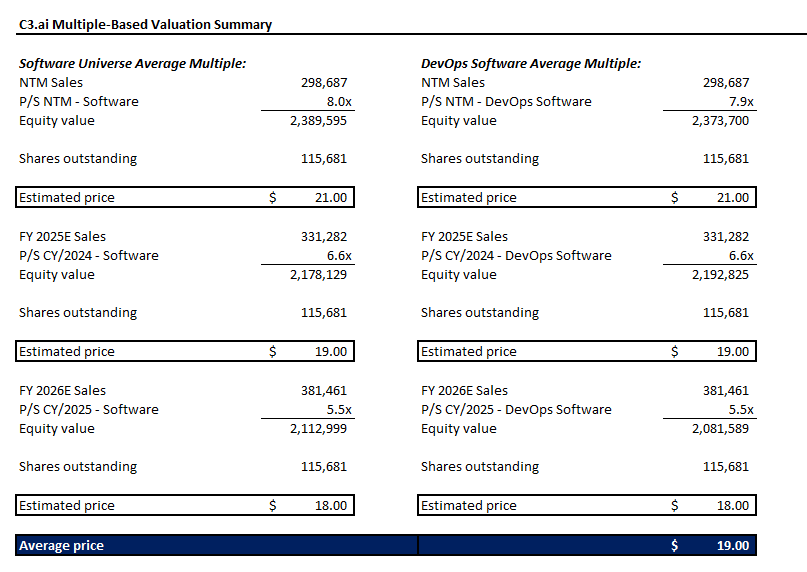

With consideration of the market's "AI premium" awarded to companies with direct exposure to impending secular opportunities in the nascent technology, we believe C3.ai's stock, at best, should trade closer to the software sector's average multiple at $19 apiece. Specifically, the company's relatively weaker fundamental prospects underscore multiple compression risks, especially considering the broader impact of an uncertain macroeconomic backdrop.

{kind=link}

Volatility Remains the Near-Term Theme

Admittedly, C3.ai has already become one of the market's most heavily shorted stocks despite its resilient upsurge this year. The stock's short percentage of float is near 40% , making it a prime candidate for a potential short squeeze within the foreseeable future. Specifically, we see several potential market catalysts in the near term that could turn this scenario into a reality:

Moderating Treasury yield : The benchmark 10-year Treasury yield has come down by more than 20 bps this week after forging new 16-year record highs north of 4.8% in early October. The accelerated pace of yield normalization, falling 9 bps overnight on Tuesday, comes as a result of recent geopolitical turbulence escalated by the Israel-Hamas conflict. Although Fed Chair Jerome Powell's " higher for longer " narrative reiterated during last month's policy meeting had encouraged markets to dial back on optimism for rate cuts, the recent geopolitical headwinds pave the way for otherwise.

Specifically, almost a third of outstanding U.S. government debt is set to mature within the next 12 months, and more than half over the next three years. And refinancing this debt will entail a significant cost increase of more than double from current levels , given the elevated rate environment. With incremental pressure from Israel's war, the U.S. is bound to allocate incremental support as a critical ally, adding further pressure to the ever-increasing federal debt burden at a time of high borrowing costs.

As a result, the Federal Reserve may need to provide room for dovishness in the near term, in line with recent commentary from policymakers that surging long-end yield may be sufficient on its own to tighten credit conditions enough and slow the economy as needed. Market expectations have also accordingly pivoted starkly from just a week ago, and now anticipates the incremental 25 percentage point rate hike before year-end, which was previously implied by the Fed's latest projections, to be off the table. The swift moderation in long-end yield is likely to be reflected in a downward adjustment in equity risk premiums, alleviating multiple compression risks on stock valuations and potentially squeezing the shorts on C3.ai out of their positions.

Diminishing leveraged trades : Normalizing long-end yield on U.S. Treasury could also discourage net carry trades. Specifically, traders that have been shorting equities like C3.ai have benefitted from a favourable mathematical set-up on the position over the past year. The differential between surging Treasury yields and fees paid on shorts has resulted in a positive net carry, which makes downside bets on stocks, such as C3.ai, all the more attractive. But expectations for normalizing Treasury yields, especially considering recent macroeconomic and geopolitical factors, could potentially remove this incentive and squeeze the heavy short interest in C3.ai out of their positions, unleashing greater volatility to the broader markets.

The Bottom Line

We expect volatility to remain the near-term theme on C3.ai's stock, as investors grapple with the conflicting combination of AI tailwinds, weak underlying business fundamentals, a lofty valuation premium, and the impact of external market-driven mechanisms (e.g., potential short squeeze, normalizing long-end yield, etc.). Although we remain incrementally cautious on C3.ai's uncertain growth and profitability prospects, which typically harbinger downside risks to the stock, broader market factors in the near term could potentially be favourable enough to net out the impact. We would recommend prospective investors in the stock to stay on the sidelines in the meantime, until the fluid macroeconomic backdrop offers greater clarity, with C3.ai's business transition delivering restoration to growth and margin expansion.

For further details see:

C3.ai's Contrarian Strategy Is A Fundamental Short-Seller Trap