CA - Cameco: Bright Near-Term Outlook With Improving Market Fundamentals 20% Upside

2023-09-12 11:41:39 ET

Summary

- Cameco stock has risen by 35% since May, but this analysis suggests a strong near-term outlook.

- Strong uranium prices are expected to drive a 20% share price appreciation.

- The completion of the acquisition of a 49% interest in Westinghouse Electric Company is expected to further increase profits.

When I last examined Cameco Corporation (CCJ) in May 2023, I stated:

"Cameco is a vertically-integrated uranium fuel vendor in an oligarchic industry, making it one of the best-positioned mining companies to benefit from a uranium bull market. Investors seeking to profit from the next up-cycle may want to consider Cameco as their first choice before exploring alternative options. Cameco's share price has been hovering around C$33 or US$25 per share since 2022... Interested investors may want to establish a position before the stock breaks out of its current range."

Since then, several significant developments have occurred. On August 2, 2023, Cameco released its second-quarter results , indicating that 'the broader uranium market is moving toward replacement-rate contracting' and that 'a new long-term contracting cycle is underway.' Additionally, on September 3, 2023, Cameco announced a reduction in its 2023 production guidance for both its Cigar Lake and McArthur/Key Lake uranium operations. This production cut is expected to have a ripple effect on uranium prices, as Cameco will need to enter the spot market to purchase uranium to offset its lost production.

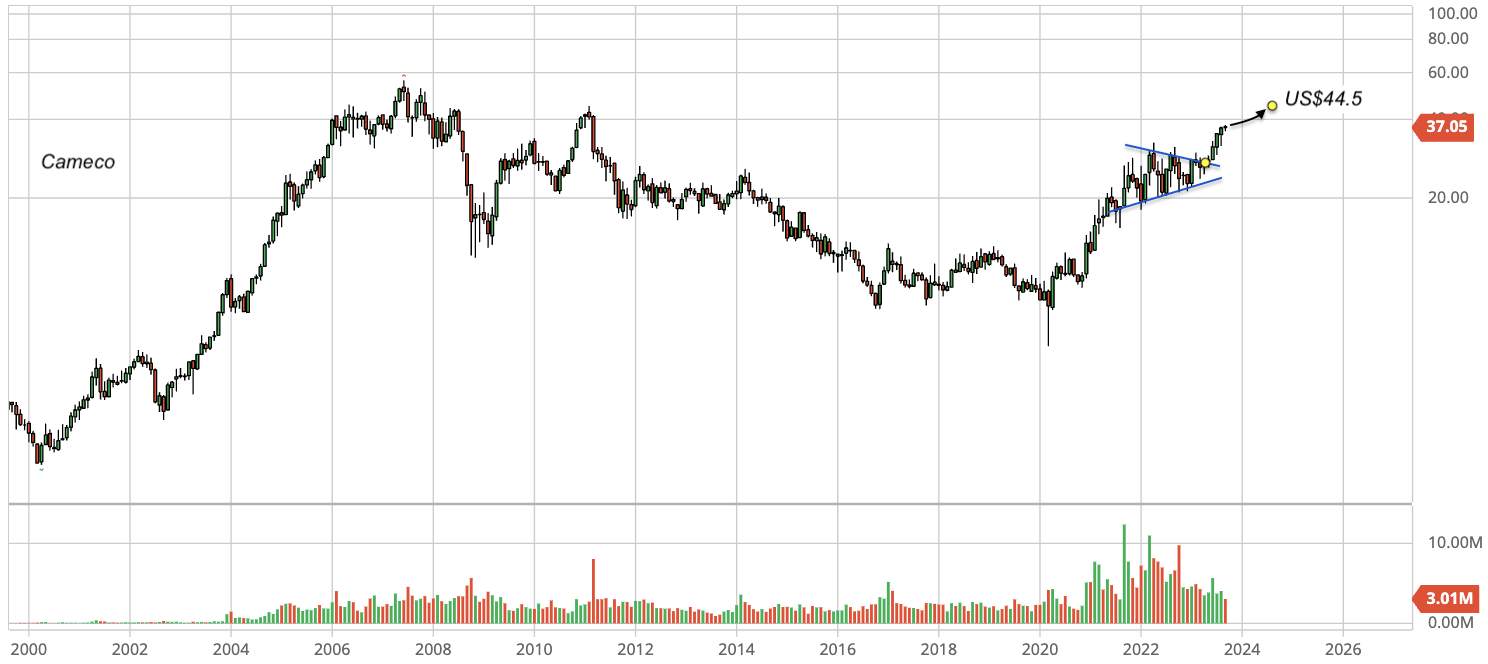

Fig. 1. Stock chart of Cameco Corp. (modified from Barchart of Seeking Alpha)

{kind=link}

In part driven by recent news flow, Cameco's stock has risen by 35% since my last article was published four months ago, as shown in Figure 1.

Now, let's update the investment thesis based on the latest developments.

Operations and financials

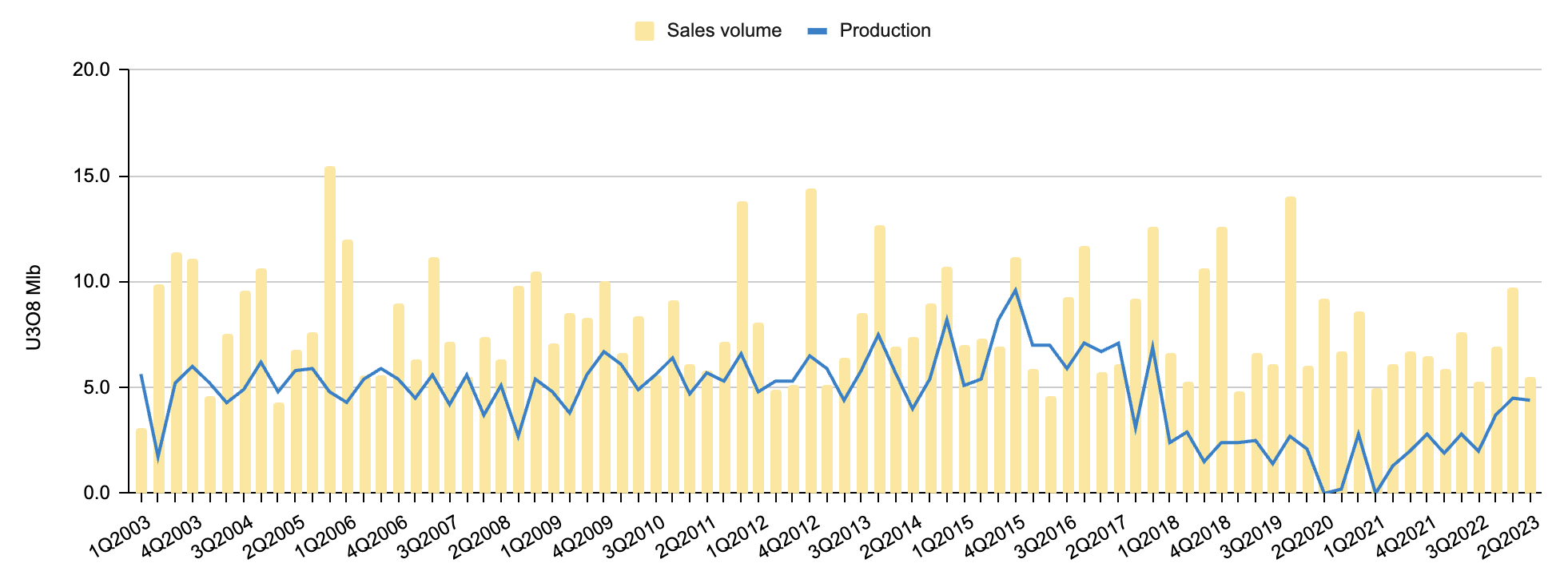

The uranium division of Cameco produced 4.4 Mlb of uranium (U3O8) in the second quarter of 2023, a 57% increase from the same period a year ago, despite a 28% decrease in uranium sales volume, from 7.6 Mlb to 5.5 Mlb, as illustrated in Figure 2.

Cameco's fuel services division produced 3.4 million kgU of uranium hexafluoride (UF6) in the second quarter, marking an 8% decrease compared to the previous year. However, uranium hexafluoride sales volume increased by 14% year over year, as shown in Figure 3.

Fig. 2. Cameco's uranium production and sales volumes by quarter. Note sales tend to spike in the fourth quarters (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco) Fig. 3. Converted fuel production and sales volumes of Cameco. Note sales tend to spike in the fourth quarters (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

{kind=link}

{kind=link}

In the second quarter of 2023, Cameco realized average prices of C$67.05/lb of U3O8 and C$35.63/kgU of UF6, both slightly higher compared to one year ago, as shown in Figure 4.

Fig. 4. Prices of U3O8 and converted fuel realized by Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

{kind=link}

Due to the rise in commodity prices and shifts in sales volume, Cameco generated $482 million in revenue in the second quarter of 2023, marking a 13.6% decrease compared to the same period last year. However, gross profit increased by 13.8% to $110 million, as indicated in Table 1.

Table 1. Selected operational and financial data for the two business segments of Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

{kind=link}

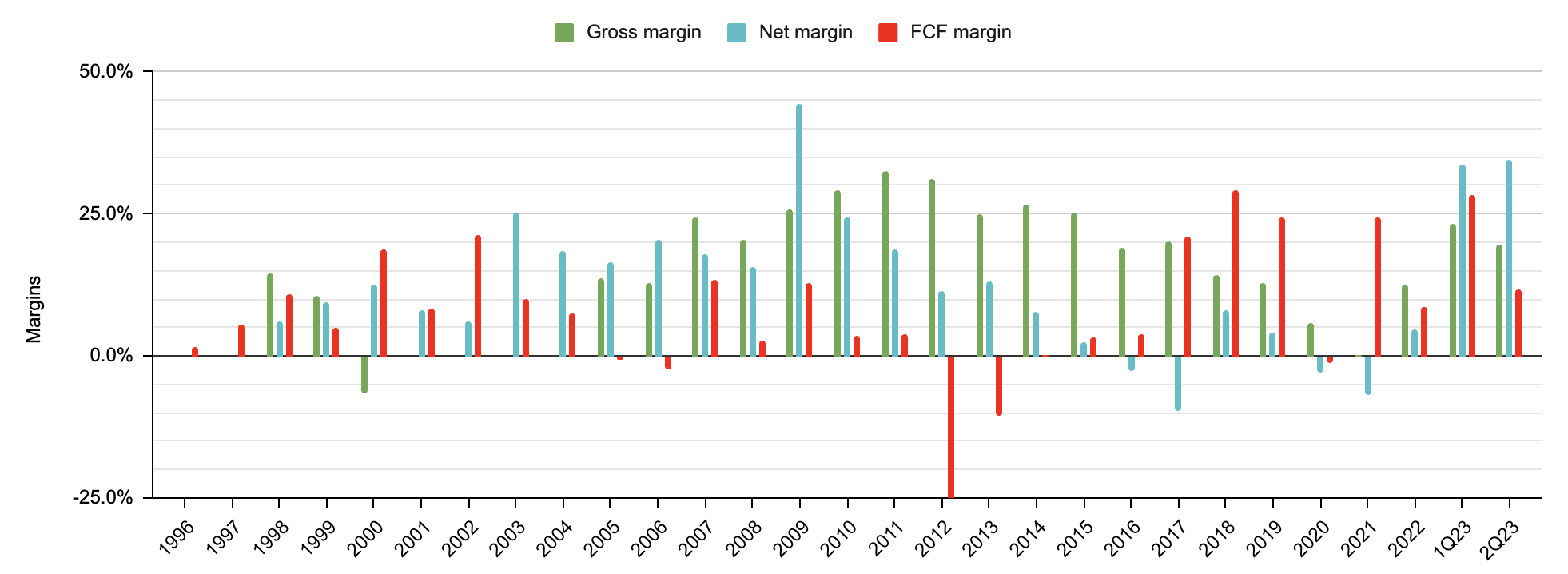

Gross margin, net margin, and FCF margin remained robust in the second quarter of 2023, although they were lower than the previous quarter, as shown in Figure 5.

Fig. 5. Gross margin, net margin and FCF margin of Cameco (compiled by Laurentian Research for The Natural Resources Hub based on data released by Cameco)

{kind=link}

Outlook

The production reduction at both Cigar Lake and McArthur/Key Lake uranium operations is expected to lower Cameco's 2023 production guidance to 18.7 Mlb, down from 20.3 Mlb. This implies that Cameco aims to produce 4.7 Mlb in each of the remaining two quarters of 2023, still reflecting significant year-over-year production growth. The impact of the production cut on this year's earnings is expected to be offset by the potential strength in uranium prices resulting from Cameco's entry into the spot market to purchase uranium and compensate for the lost production.

Tim Gitzel, Cameco's president and CEO, said

"...for 2023, we have increased our consolidated revenue outlook, which is primarily driven by higher expected average realized prices under our contract portfolio and increased deliveries in our uranium segment."

It's worth noting that sales of uranium and converted fuel historically spike in the fourth quarter, as shown in Figures 2 and 3. Considering the ongoing strength of uranium prices, I maintain confidence in Cameco's ability to achieve robust results in the remaining two quarters of 2023.

In 2024 and beyond, the acquisition of a 49% interest in Westinghouse Electric Company is expected to lead to an increase in profit.

Gitzel commented on uranium fundamentals,

"We are seeing improving market fundamentals with prices for uranium rising, and UF 6 conversion prices hitting new record-highs... With over 118 million pounds of long-term contracting industry wide so far this year, we are happy to say that we believe there is clear evidence that the broader uranium market is moving toward replacement-rate contracting. Based on the rate of contracting seen year-to-date, we expect industry long-term contracting volumes in 2023 to exceed those in each of the last 10 years. We believe this is a good indication that a new long-term contracting cycle is underway."

Downside risks

Cameco exposes investors to multiple risks. Firstly, a delay in the restart of the Japanese nuclear fleet could negatively impact uranium prices and shift sentiment toward nuclear energy unfavorably. Secondly, any production problems at the Cigar Lake mine may result in a further decrease in production. Thirdly, there could be delays in the Westinghouse acquisition as per the terms outlined in the acquisition agreement.

Investor takeaways

Despite the recently announced production reduction, Cameco's uranium franchise has a bright near-term outlook. Although the share price has appreciated significantly since my last article, Wall Street analysts have set 12-month price targets that are 20% above the current share price, as shown in Figure 1. Interested investors still have an opportunity to establish a position before the release of the third and fourth quarter results, which are expected to be an improvement over the second quarter.

For further details see:

Cameco: Bright Near-Term Outlook With Improving Market Fundamentals, 20% Upside