CCJ - Cameco: First Half Results Robust But The Stock Is Richly Priced

2023-08-02 21:30:24 ET

Summary

- Cameco Corporation's stock, which has seen a strong performance this year, up by almost 45%, fell after Q2 2023 results today.

- Revenue contracted and profits fell, but not for fundamental reasons. The big picture still looks good as H1 2023 numbers are robust.

- Cameco has upgraded its outlook for the second time too, expecting over a 30% rise in revenues in 2023. But with steep market valuations, it's one to Hold and buy once it dips enough.

The Canadian uranium miner Cameco Corporation ( CCJ ) has seen an exceptional performance this year, up by almost 45% year-to-date. However, the stock wasn’t doing well when I started writing it this Wednesday. Its price had dropped by almost 8% following its second quarter (Q2 2023) results . If it had ended the day with these losses, it will have been the worst single-day fall of 2023 for it.

{kind=link}

It didn’t. By the end of the day, it was down by a relatively smaller 3.8%. And this in a nutshell explains the story of its latest results and the stock as such. The headline figures look bad, but the bigger picture is alright, pretty good, in fact. At the same time, the stock is still overvalued. Let me explain in detail.

Weak Q2 figures…

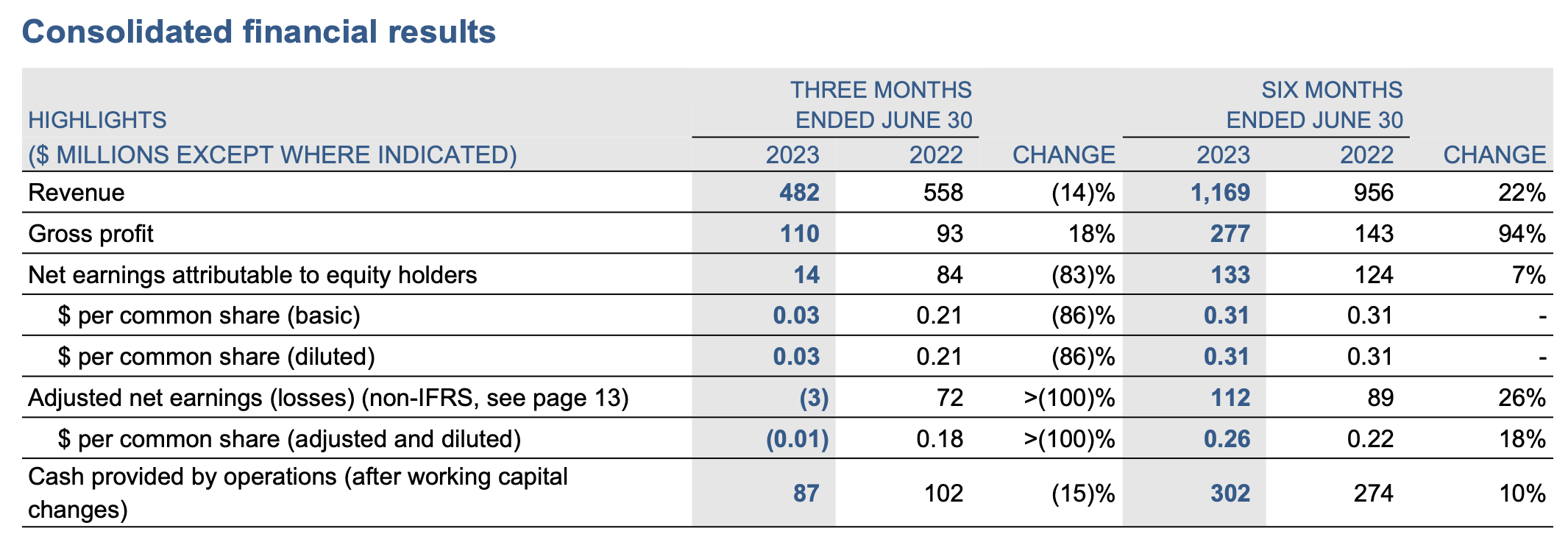

Cameco’s Q2 2023 figures show a revenue contraction of 14% year-on-year (YoY). This sounds disappointing after a particularly robust Q1 2023 , but there’s a good reason for this. As it happens, the company delivered a third of the total expected amount under its big uranium segment in 2023, which accounts for 80% of its revenue.

As background, it has two streams of revenue, the first is uranium, under which it mines and trades uranium. The other one is fuel services, where it provides refining, conversion, and fuel manufacturing services. So essentially, the numbers for the last quarter were better than usual, and the reverse is the case now. Additionally, there’s a high base effect from last year too. Q2 2022 saw a spike in revenue, with 55% YoY growth, the biggest quarterly rise seen in 2022.

{kind=link}

Despite this, in an interesting development, its gross profit was actually higher due to rising uranium prices. Prices are up by over 15% in 2023 so far and nearing 14-month highs now. As a result, the gross margin rose to 22.8% from 16.7% in Q2 2022.

However, due to notional exchange rate losses on US dollar cash balances, the net earnings saw a massive drag. Not only was the exchange rate unfavourable in the latest quarter, but the company was also holding more than usual amounts of cash for its pending acquisition of the nuclear services provider Westinghouse, which hurt its earnings.

… but the big picture still looks good

So, in effect, we have a situation where the company has performed badly in the quarter, but there don’t seem to be any fundamental reasons for it. Especially not, considering its performance for the first half of 2023 (H1 2023) and its outlook for the full year 2023.

In H1 2023, Cameco actually did pretty well, with a 22% revenue increase and a 7% growth in reported net earnings, while the corresponding adjusted figure grew by 26%. This was the outcome of larger than expected deliveries during the first quarter, coupled with higher realised prices, as discussed above.

Outlook upgraded

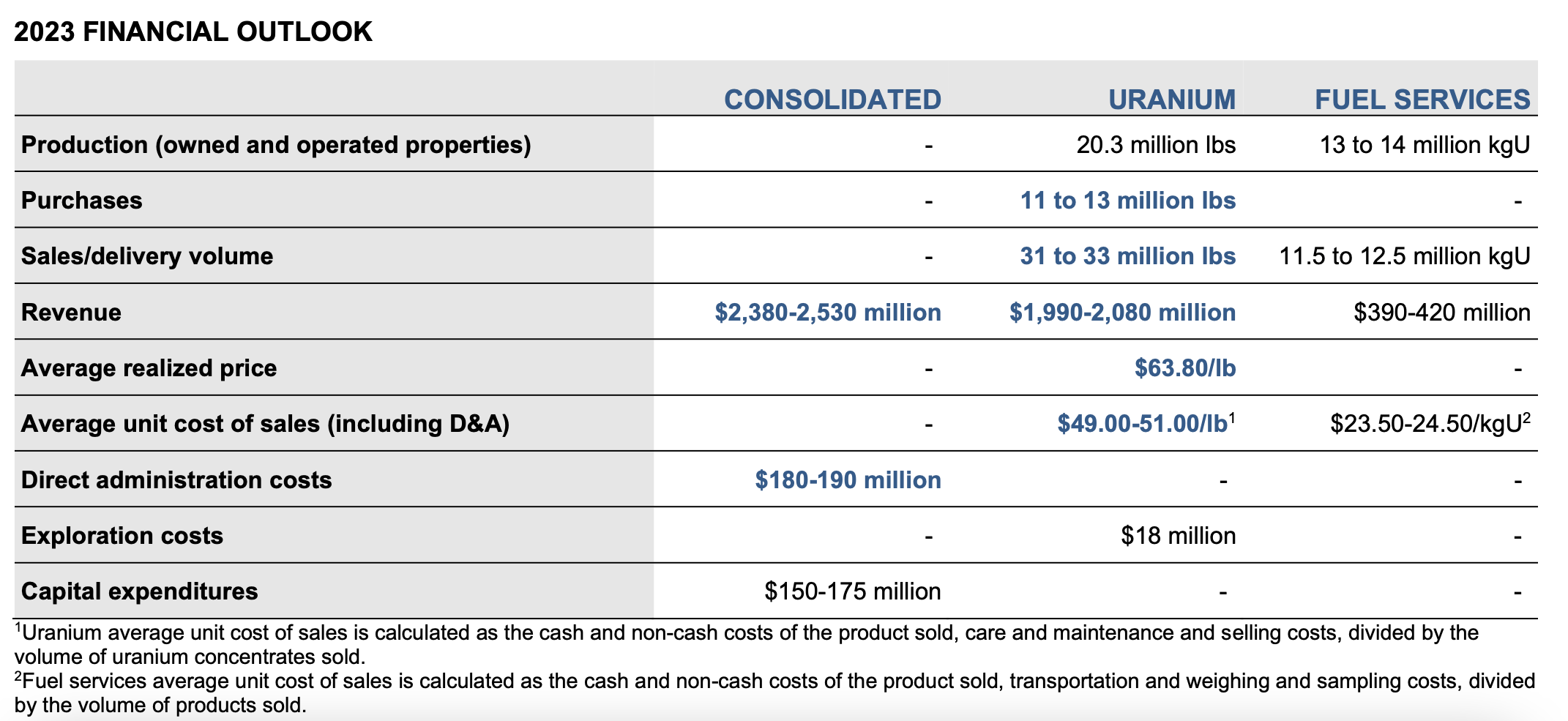

Further, the company has upgraded its outlook for the second time this year. Even its initial outlook was healthy, with the expectation of a 17.5% revenue growth from 2022. But now, it actually expects over 30% rise in revenues. This is one, because of improved expectations for realised prices for uranium. These have risen by 8% from its initial outlook to USD 63.8 per pound now. Two, it has also upgraded guidance for uranium delivery volume by 6.7%, since the first projection, to 32 million pounds.

{kind=link}

The nuclear energy premium

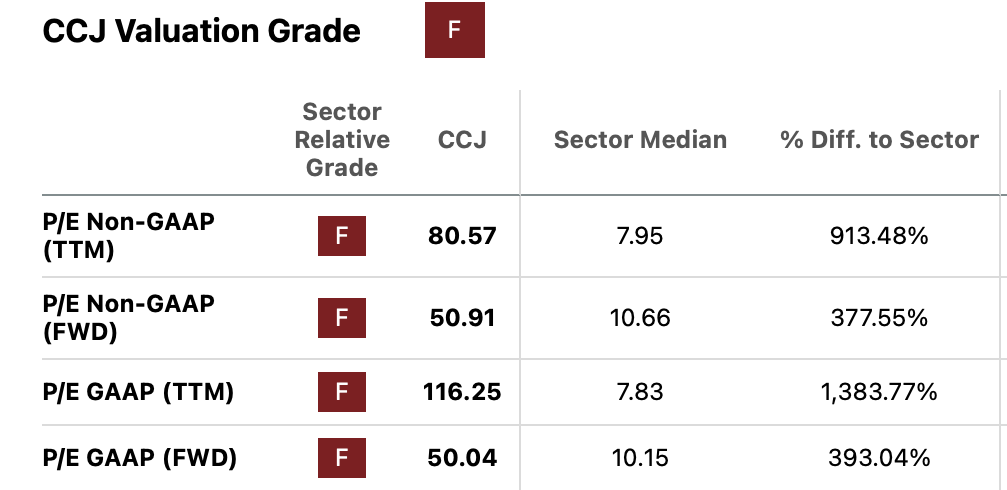

In essence, there’s nothing not to like about the Cameco stock. Except maybe, its market valuations (see table below), which I come to next. Its various price-to-earnings (P/E) ratios are so high, they are nowhere even comparable to that of the Energy sector. There’s a very good reason for this, of course. Nuclear energy has received a huge fillip in the past year because of a variety of developments.

{kind=link}

There’s a greater need for energy security now than ever after Russia’s war on Ukraine. This specifically spills over into nuclear energy, because Russia is among the critical suppliers of refined uranium in the world. The Inflation Reduction Act and the energy security reserve in the US are some of the policy actions that have impacted the sector positively in the last year. But the revival of nuclear energy can also be seen in the policies of countries from Japan to Canada .

Comparison with own past multiples

With the future of the sector suddenly looking brighter than it has for a long time, it’s little wonder that Cameco Corporation’s valuations are off the charts. Given the unlikelihood of its valuations being in line with the energy sector anytime in the near future because of this, it’s best to compare it to its own past multiples.

Its trailing twelve months [TTM] GAAP P/E, is at 116.2x compared to the ten-year average of 49.9x . Further, its TTM price-to-sales (P/S) ratio at 9x also reflects some overvaluation, considering that the average of five years stands at 5.4x. In fact, both the TTM ratios taken together indicate that price levels can drop to half their current levels.

I very much doubt if that will happen though. Not with the current bullishness about the sector. I do believe some more short-term correction is likely, of at least 15% going by its relatively more subdued P/E levels in the past few months.

But the tendency of the stock over time is more likely upwards than not. Moreover, the forward P/E at 50.9x already looks far better than the TTM P/E and looking beyond this year into 2024 reveals that the forward figure drops to half its current levels.

What next?

So we are looking at some correction in the short-term, but in the medium to long-term, Cameco Corporation still looks very good. As one of the biggest global uranium producers, with solid financials at a good time for nuclear energy, it holds a lot of potential.

For investors that are willing to wait for a continued dip, it might be just the thing to do. Especially given the big gap between its past and current TTM valuations. From a medium to long-term perspective, it's still a Buy. Typically, I would go with a Buy rating in a situation like this, but considering its rather big multiples right now, I'd say it's better to Hold now and buy it on a dip.

Finally, it being part of the nuclear energy sector, I have to mention that if anything goes wrong, there is the risk of the sector reeling back into a slump. But if all stays well, with it's one to own, either now or after it has corrected some.

For further details see:

Cameco: First Half Results Robust, But The Stock Is Richly Priced