CCJ - Cameco: Fully Integrated Uranium Producer But At A High Price

2023-12-12 02:03:45 ET

Summary

- Cameco is one of few companies in the industry covering all aspects of nuclear fuel production: mining; refining, conversion, enriching; and fuel fabrication.

- CCJ has an excellent balance sheet with $1.93 billion cash and $830 million of total debt. CCJ credit instruments are with investment grade and positive outlook.

- The rising uranium price improved the company's profitability, as seen in the 3Q23 report. Net Earnings grew from $(20) million in 2Q23 to $148 million in 3Q23, resulting in 0.34 EPS.

- CCJ is overvalued compared to its past multiples and percentile ranks. Price action confirms that fact; the price is overextended above 36MMA.

- Betting on uranium, I prefer cheaper ideas, providing better risk reward. My verdict is a hold rating.

Introduction

Uranium is one of the best energy commodities of the year, realizing 66.7% gains. I came across the uranium bull thesis a few times but did not pay particular attention. Last week, browsing through fuel consumables producers, I started to dig deeper into the industry and picked the major player in the field, Cameco Corporation ( CCJ ), for analysis.

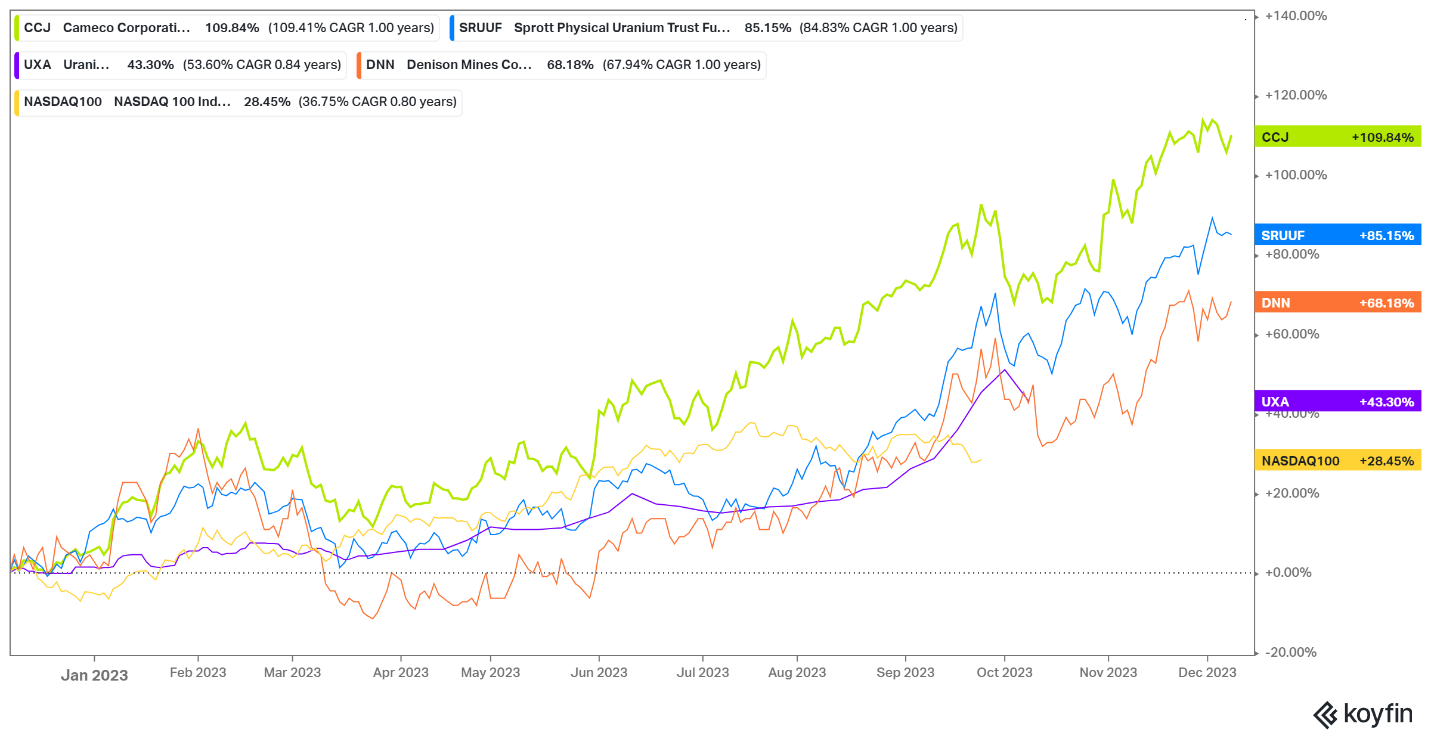

As seen below on the chart, the company outperforms NASDAQ, uranium spot, Denison Mines ( DNN ), and Sprott Physical Uranium Trust ( SRUUF ).

{kind=link}

Cameco has a bulletproof balance sheet with $1.9 billion cash and $830 million total debt. Its debt securities credit rating is adequate, too, A3 with a positive outlook by S&P. The company became profitable in the last quarters following the rise in the price of uranium. The company owns some of the world's best uranium mines with exceptional grade and vast reserves, Cigar Lake and Mac Arthur. They deliver more than ten percent of the annual uranium output combined.

Despite great fundamentals, I give a hold rating. The reason is the overextended price action and high multiples, exceeding the company's average figures, energy sector multiples, and the broad market.

Company Overview

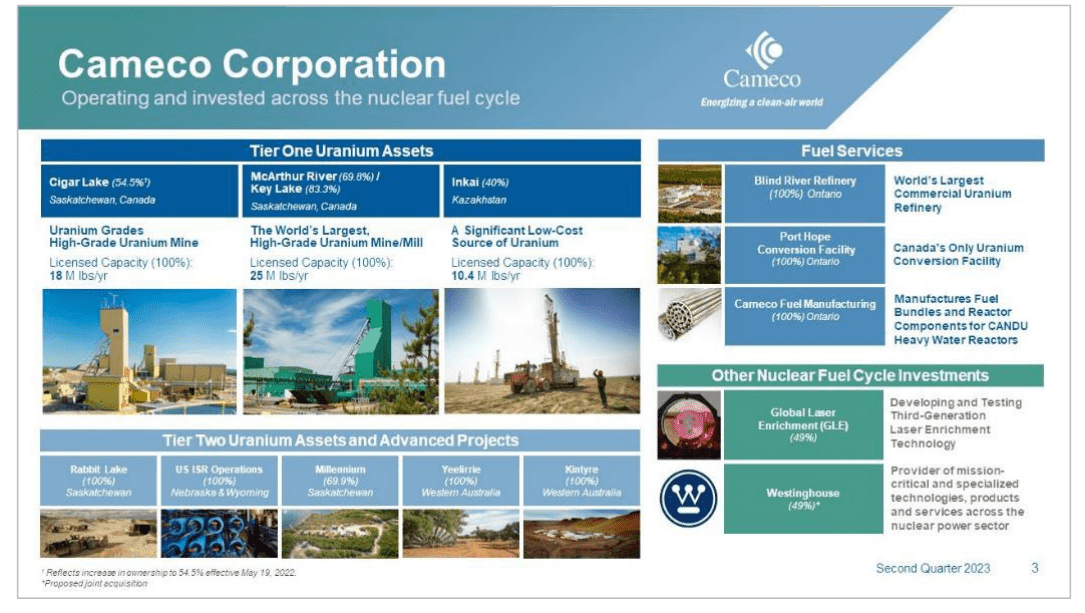

The chart below from the last corporate presentation shows CCJ assets at a glance.

{kind=link}

CCJ has a few Tier One assets in Canada and a Joint Venture with Kazatomprom in Kazakhstan. All Canadian mines are in Saskatchewan province, home to the largest underdeveloped uranium deposits. CCJ's flagship assets are Cigar Lake , with 84.4 M lb Proven and Probable ((PP)) reserves and 17.2% ore grade, and McArthur , 275 M lb PP and 6.7% grade. The company operates the Inkai mine in Kazakhstan with Kazatomprom. The mine has 108.7 M lb PP with 0.04% ore grade.

Apart from uranium mining, CCJ is involved in the whole process of nuclear fuel production. The company`s Port Hope facility is Canada's sole uranium conversion installation. Blind River is the largest uranium refinery in the world. Cameco owns a nuclear fuel production facility , too. It is one of only two such facilities in Canada.

CCJ acquired a 49% stake in Westinghouse Electric Company, one of the leading nuclear reactor manufacturers. The remaining 51% are acquired by Brookfield Renewable Partners (BEP). The deal with Westinghouse and BEP transformed CCJ into the first fully integrated uranium producer. The company covers all the steps, from greenfield exploration and uranium mining through uranium refining and fuel fabrication to nuclear reactor design and maintenance.

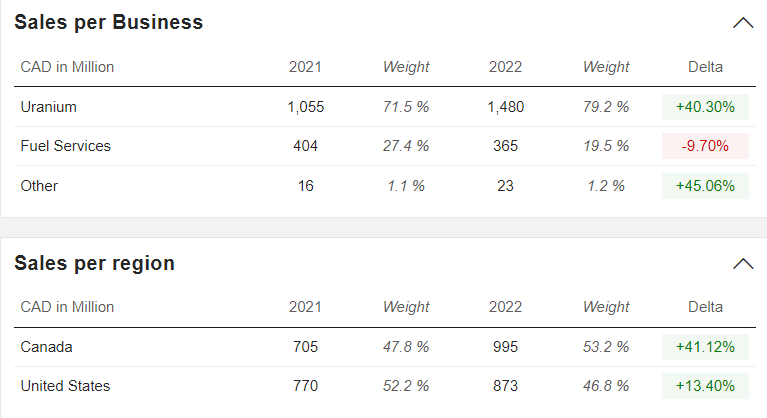

The company revenue derives 79.2% from uranium mining, 19.5% from fuel services, and 1.5% from others. Geographically, 53.2% of the revenue comes from Canada, and 46.8% comes from the US.

{kind=link}

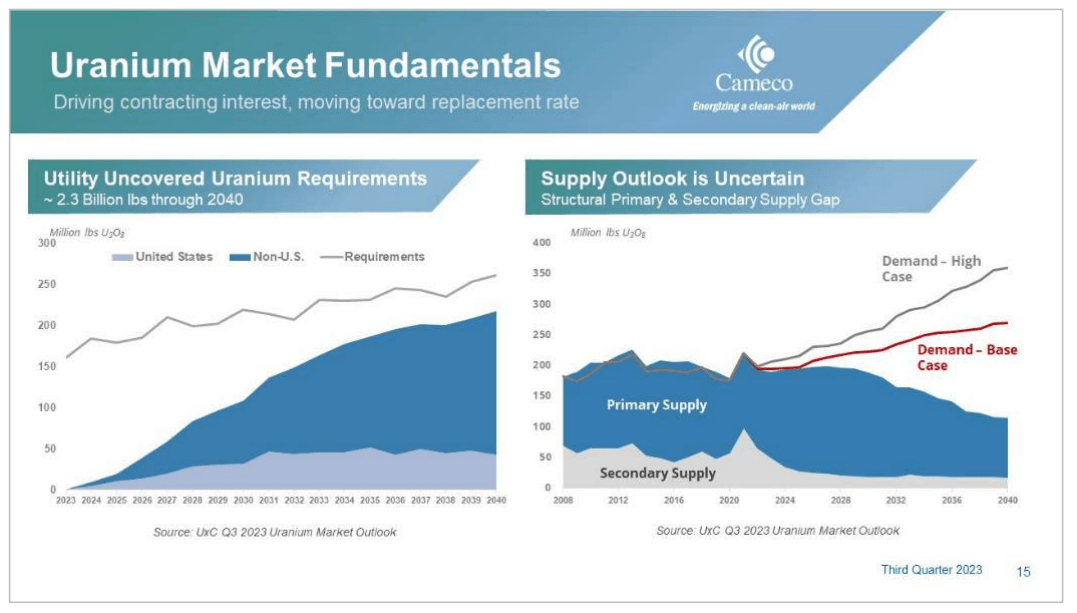

CCJ and uranium miners are entering their roaring 20s. According to multiple analysts, the uranium deficit is imminent due to declining supply and growing demand. The chart below shows the supply outlook and utility uncovered uranium requirements.

{kind=link}

Both charts paint the same picture: insufficient uranium to cover the growing demand, and the deficit has just started. Like all miners, the supply side has been constrained by an acute deficiency of capital investments. On the other hand, the demand is driven by the transition to clean energy. A week ago, at the last COP28, 22 countries pledged to triple their nuclear power until 2050. The uranium deficit was already apparent before that declaration, but now it might take epic proportions.

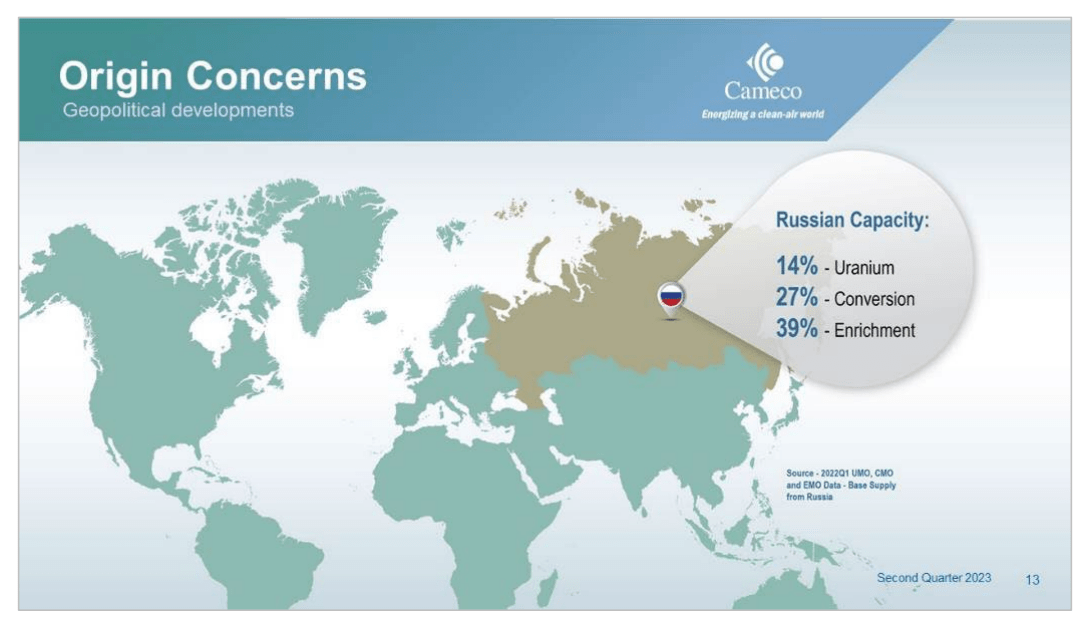

The uranium market is very niche, dominated by a handful of companies exploiting several mines in a few countries. One of the top players is Russia. The chart below shows how crucial is its role in the nuclear fuel cycle.

{kind=link}

Today, the US House will vote on H.R. 1042 – Prohibiting Russian Uranium Imports Act, as amended ( Sponsored by Rep. Rodgers (WA) / Energy & Commerce Committee ). If the bill becomes fact, the uranium market goes into the parabolic regime. Interesting times ahead.

Cameco Financial

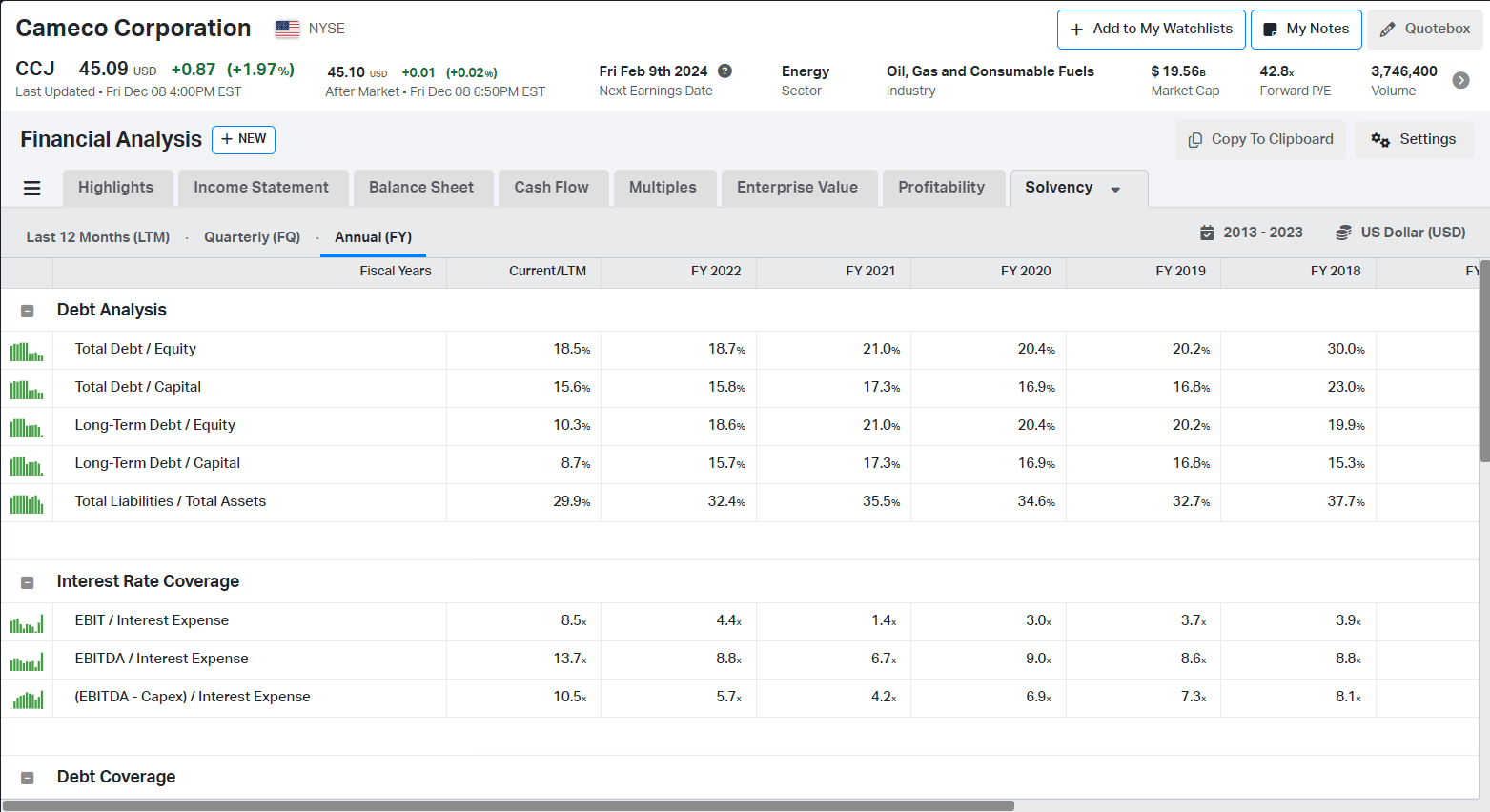

CCJ has an excellent balance sheet with $1.9 billion cash and $830 million total debt. The table below shows the company's capital structure and interest coverage.

{kind=link}

CCJ, even at the bottom of the uranium price, maintained low leverage. 2019, the company had 30% total debt/equity and 8.8 EBITDA/interest expense. For five years, CCJ reduced total debt to equity by 38%. Let's discuss other companies in the Consumable fuel industry.

Uranium Energy Corp. ( UEC ) has $45 million cash and $1.4 million debt; CONSOL Energy ( CEIX ) has $2428 million cash and $220 million debt; Peabody Energy has $985 million cash and $352 million. I picked coal miners against Cameco because the uranium sector is tiny, and CCJ is the sole US-listed producing company. Kazatomprom is listed on the LSE, and the other major producers are not public companies. Even “large cap” uranium miners are at different stages of developing their projects.

S&P gave an investment grade credit rating (A3 and BBB-) to CCJ debt securities with a stable outlook. Given the company’s liquidity position, I expect no difficulties servicing its debts.

Profitability

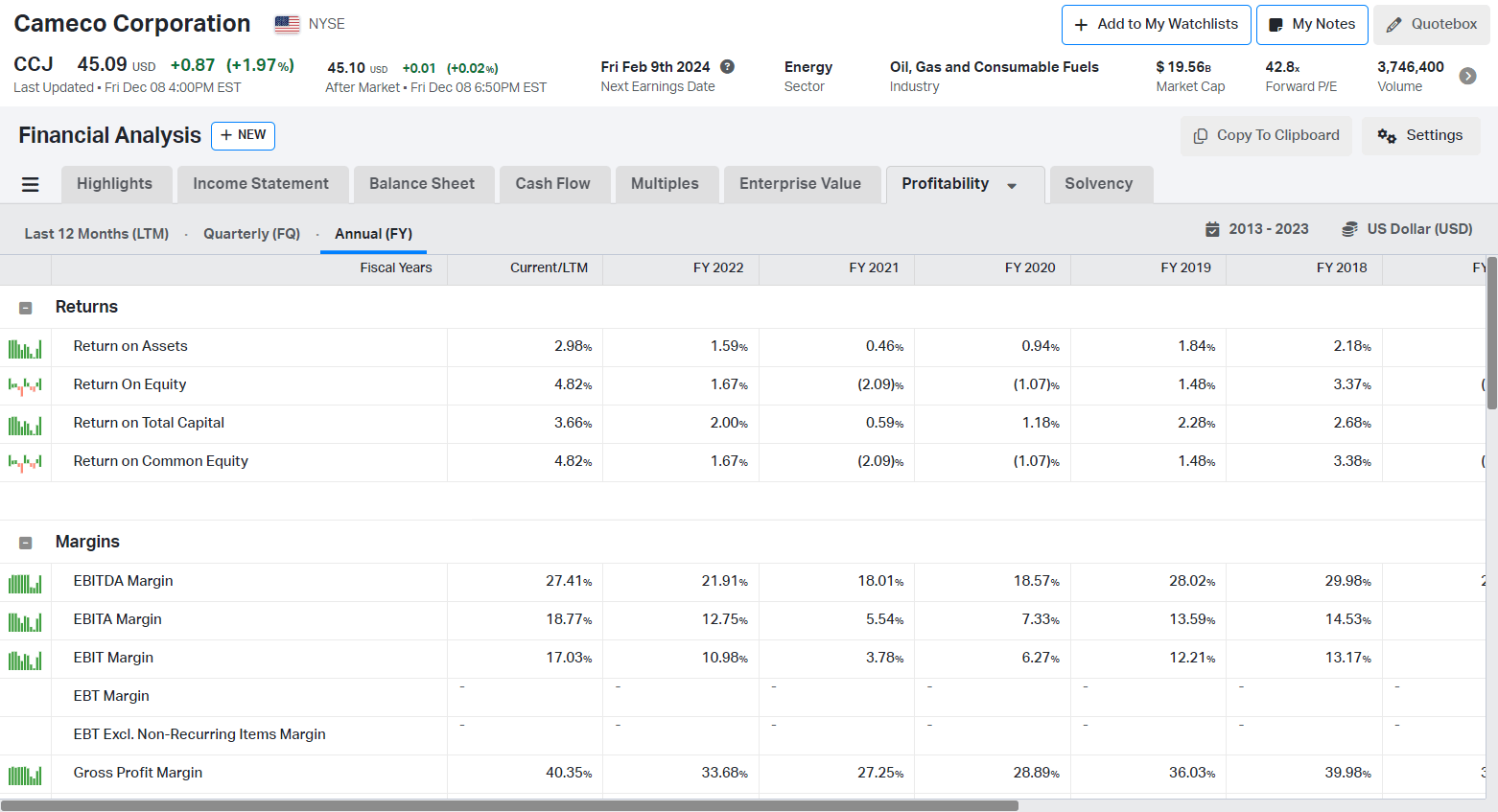

CCCJ became profitable in the last months following the growing price of uranium. The table below shows company margins and returns in the previous five years.

{kind=link}

Among its peers in the Coal and consumable fuel industry, CCJ lags significantly. The coal miners have been offering double-digit returns and margins. On the other hand, CCJ, compared to other uranium miners, is profitable.

There is no company for direct comparison to CCJ. For oil, it is easy to pick fully integrated oil companies: Petrobras ( PBR ) vs Ecopetrol ( EC ) or Exxon ( XOM ) vs Occidental Petroleum (OXY). Knowing it is imperfect, I compare CCJ`s profitability with those of UEC, CEIX, and BTU.

- CCJ 40.3% Gross Margin, 27.14% EBITDA Margin, 4.82% ROE, 3.6% ROTC

- UEC 18.9% Gross Margin, 6.6% EBITDA Margin, (0.69)% ROE, 1.15% ROTC

- BTU 35.5% Gross Margin, 32.7% EBITDA Margin, 40.7% ROE, 24.8% ROTC

- CEIX 46.7% Gross Margin, 43.0% EBITDA Margin, 62% ROE, 36.3% ROTC

Cameco performs well but is not impressive. The coal miners have been highly profitable for several quarters despite the depressed coal prices. In other words, there is more efficient business if one can mint cash even in declining commodity prices.

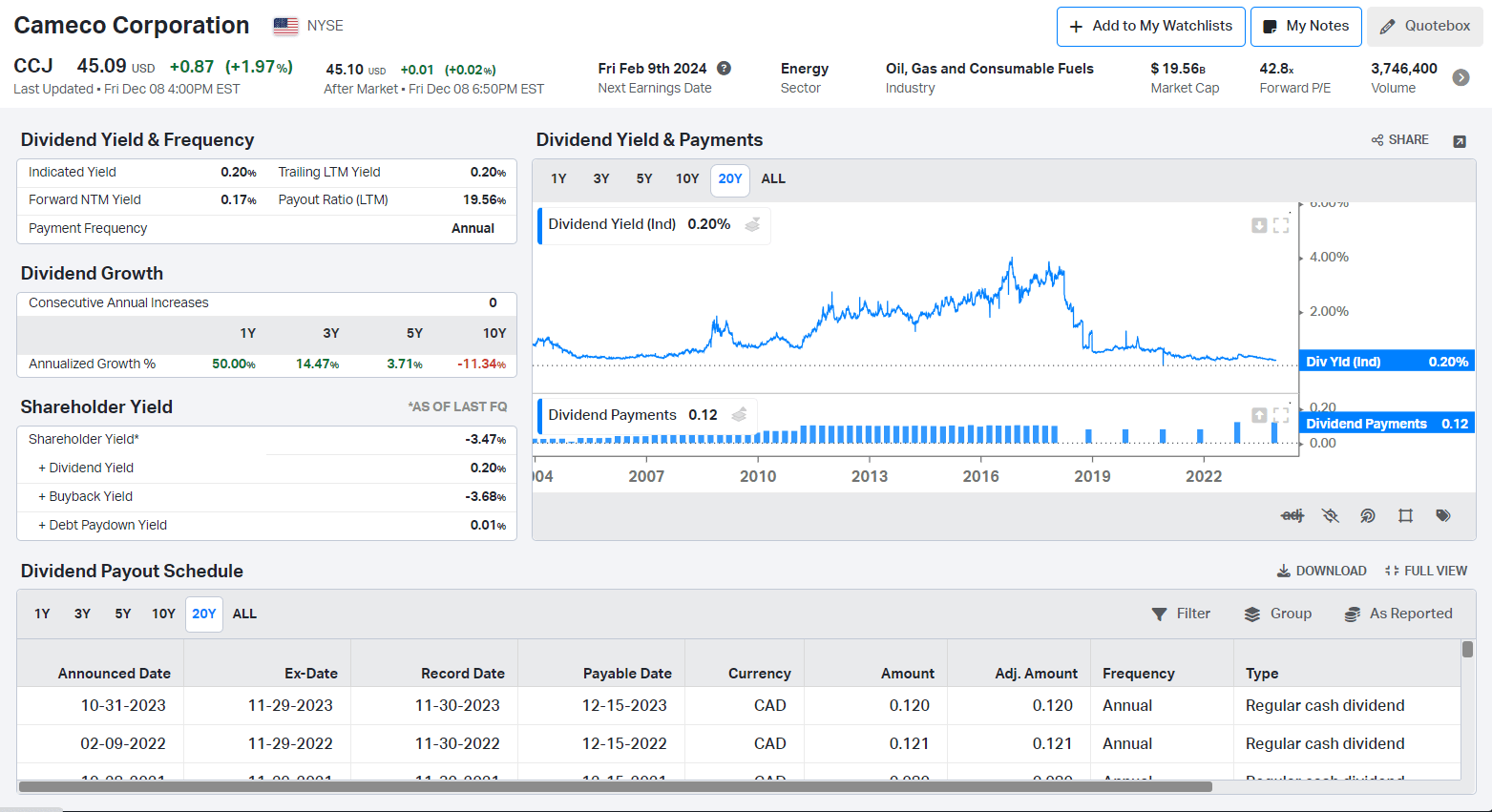

CCJ declared dividends in the last 3Q23 report. However, the company does not have a strong tradition of paying dividends. The buybacks have not been popular, too, among CCJ management.

{kind=link}

The current dividend is $0.12/share, resulting in a 0.2% yield based on the current market price.

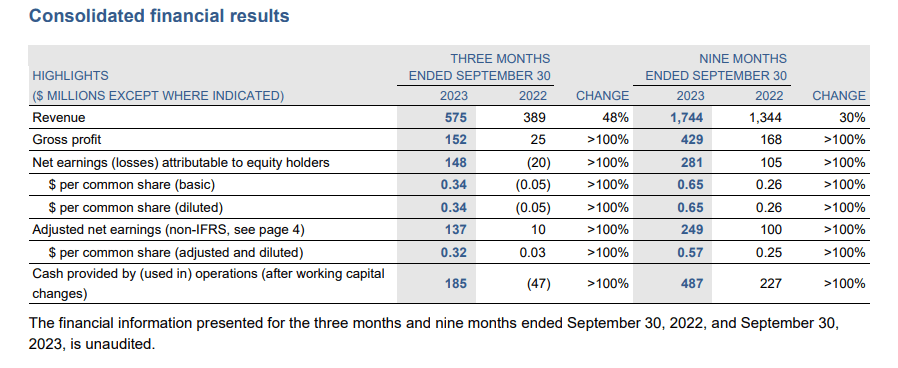

3Q23 recap

CCJ reported solid quarter results . Across all metrics, company profitability shows improvement.

{kind=link}

Revenue grew 48% YoY to $575 million in 3Q23 from $389 million in 3Q22. Gross profit increased by over 100% YoY to $152 million in 3Q23 from $25 million in 3Q22. Net Earnings, too, realized extreme growth from $(20) million in 2Q23 to $148 million in 3Q23, resulting in 3Q23 EPS of 0.34.

The primary driver is the growing price of uranium. The quote below from the 3Q23 report summarizes the recent developments in the company:

We are seeing durable, full-cycle demand growth across the nuclear energy industry. These factors lead us to believe we are experiencing the industry’s best market fundamentals ever. These dynamics have also prompted the World Nuclear Association (WNA) to increase its demand forecast in its latest Nuclear Fuel Report to an average annual growth rate of 3.6%, compared to 2.6% in the 2021 report. Furthermore, the WNA has issued a call to action to triple nuclear capacity by 2050 to help the global drive to net-zero greenhouse gas emissions.

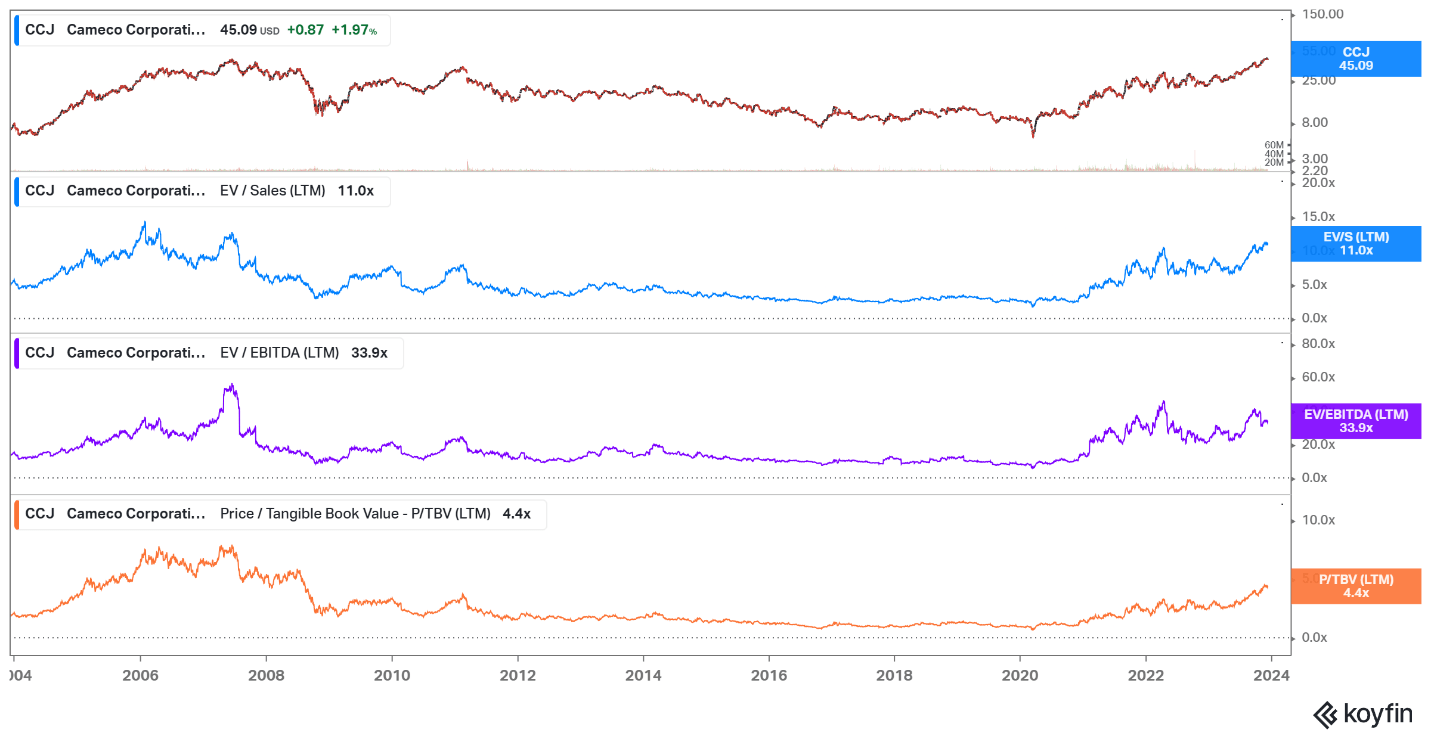

Cameco Valuation

CCJ is expensive compared to its past multiples. The chart below shows CCJ EV/Sales, EV/EBITDA, and P/TBV over the last 20 years.

{kind=link}

All three multiples (11 EV/Sales, 33.9 EV/EBITDA, 4.4 P/TBV) significantly exceed their 5Y average values (5.45 EV/Sales, 24.46 EV/EBITDA, 2.13 P/TBV). However, they were below CCJ's peak level (12.2 EV/Sales, 56.7 EV/EBITDA, 7.5 P/TBV) in 2007, the last uranium bull market.

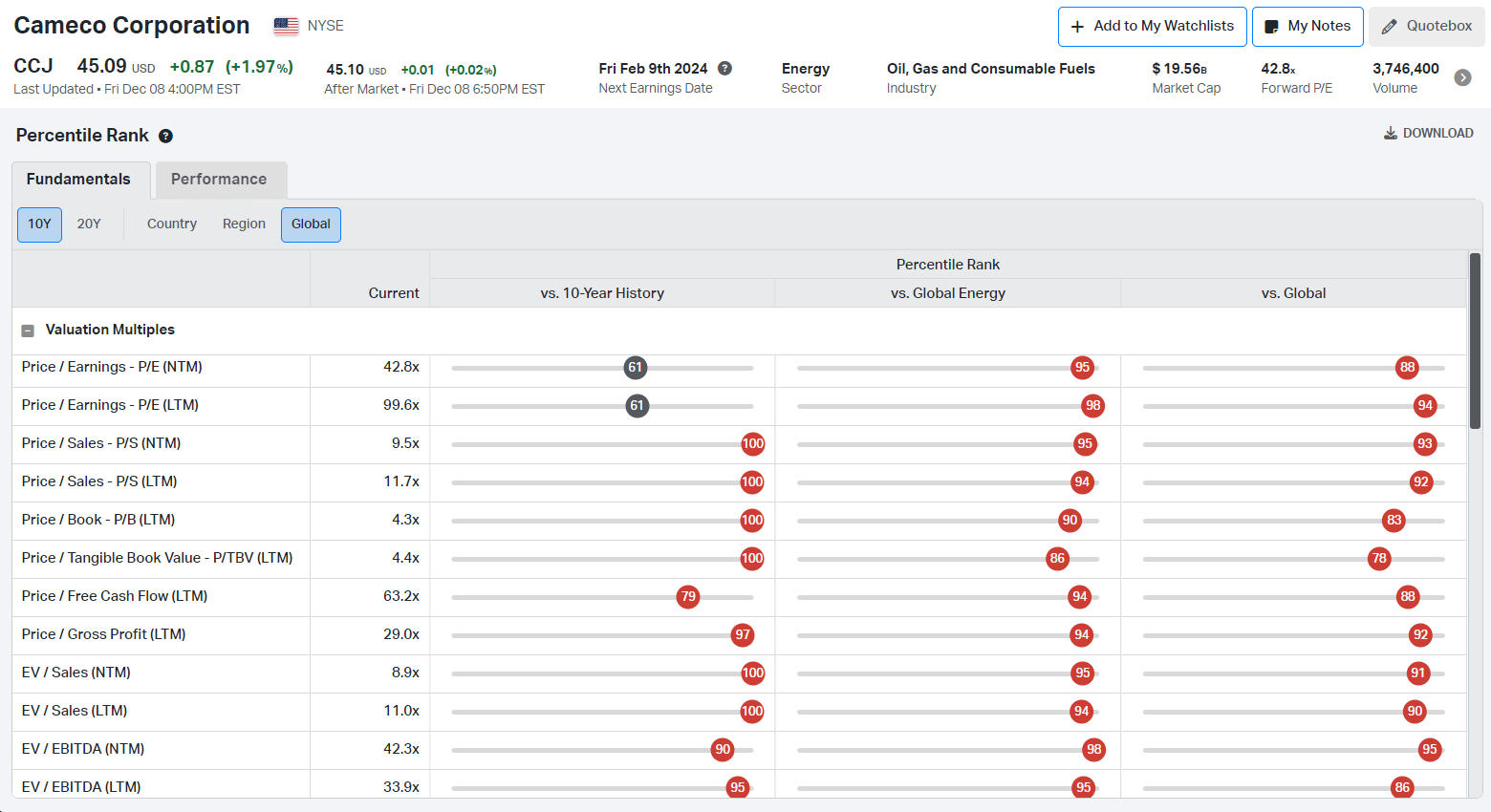

The situation is the same compared to global energy and global equities, but CCJ is very pricey.

{kind=link}

CCJ trades in the highest percentiles in all three sections, using the exact three multiples. The company is overvalued. Of course, that does not mean it cannot go higher. Given the emerging uranium deficit, I guess it will go higher, but there are cheaper opportunities to bet on the uranium thesis or, more generally, on consumable fuels.

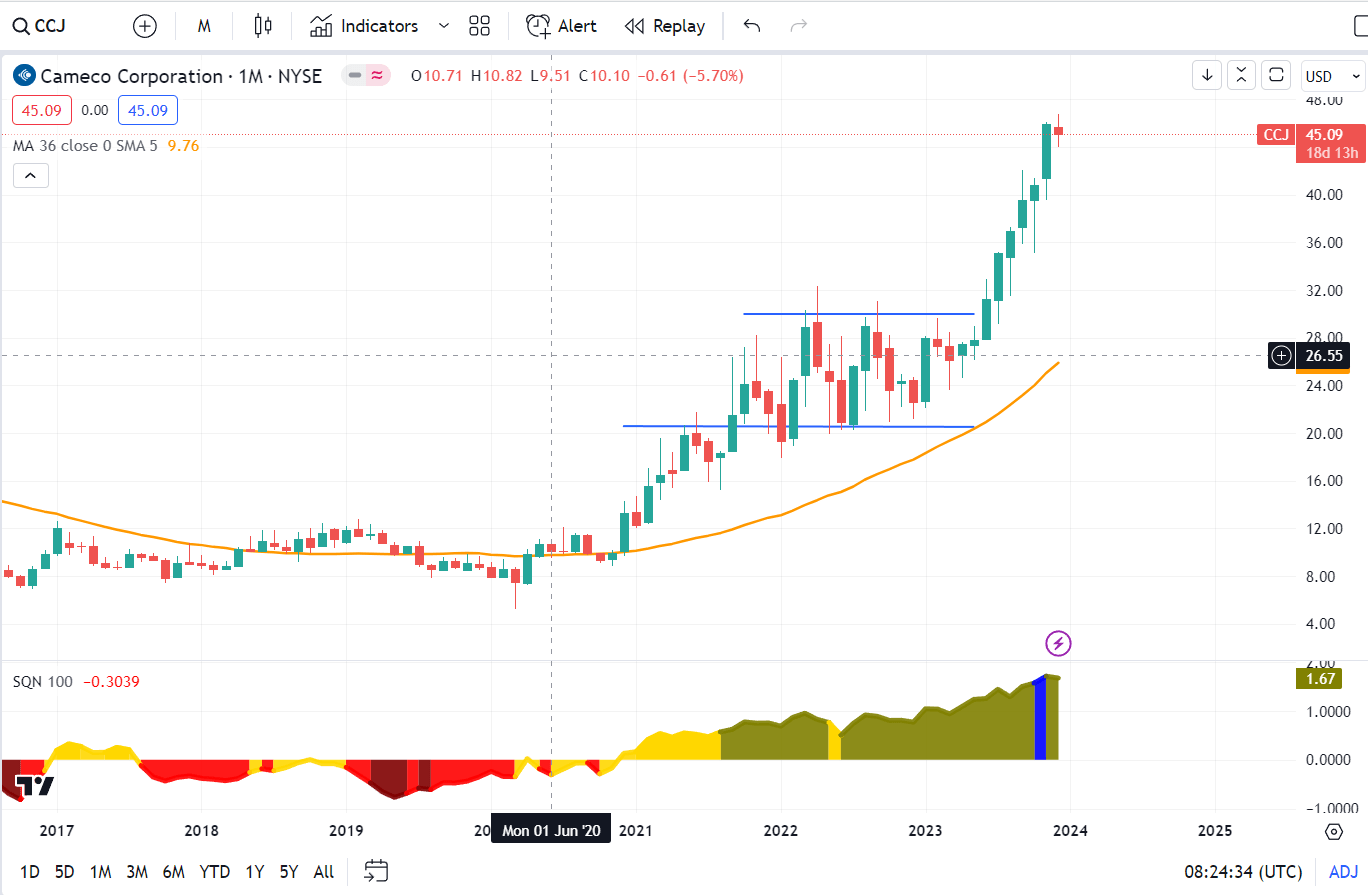

Price Action

CCJ seems expensive not only for its multiples but also for its chart.

{kind=link}

The stock price is over-starched above the 36 simple monthly moving average ((MMA)). It made six consecutive bull candles, meaning the trend is strong and probably will continue, however, after a retracement. SQN is a bull-quiet regime, but I expect soon to move into bull volatile (blue). This is not the best regime for long positions. His price action is erratic and too often punishes impatient investors.

Risks

Uranium is a curious industry because it is indifferent to the economic cycles. On the other hand, it is one of the most geopolitical commodities (besides oil). A handful of players across the globe run the uranium market. The tensions between the great powers create potential supply constraints. Ban on Russian uranium imports is such an example. Geopolitical risk has an inverse correlation with the uranium price due to uranium market peculiarities.

The market risk is always present. CCJ is an exception among uranium equities, surpassing uranium spot performance. The remaining uranium miners are lagging to a different degree uranium spot. The reason, I believe, is the NASDAQ rally diverting funds flown into large-cap tech stocks. Last week the flow seemed to move into small caps, but not into energy yet.

Conclusion

CCJ is one of few companies in the industry covering all aspects of nuclear fuel production (mining; refining, conversion, enriching; fuel fabrication). The company has an excellent balance sheet with $1.9 billion cash and $830 million total debt. The rising uranium spot significantly improved the company`s profitability. 3Q23 results are proof of that statement. The tailwinds support the uranium equities; however, CCJ is overvalued compared to its past multiples and percentile ranks. Price action confirms that fact; the price is overextended above 36MMA.

I firmly believe we are in the first leg of the bull run, and I am planning to buy some uranium stocks. I prefer to pick cheaper stock with better risk rewards to play the theme. Moreover, if I want to bet on the consumable fuel sector, I will use coal, which I have been doing for the last several quarters. Some of the coal miners are generating astounding returns. I give CCJ a hold rating.

For further details see:

Cameco: Fully Integrated Uranium Producer But At A High Price