CCJ - Cameco: Keeps Adding To Its Contract Portfolio (Rating Downgrade)

2023-08-18 10:00:30 ET

Summary

- Cameco recently reported some very underwhelming Q2 numbers.

- However, this quarter, Cameco grew its long-term contracting commitments substantially.

- Strong uranium markets are also allowing CCJ to get favorable terms in new contract negotiations.

On August 2nd, Cameco Corporation ( CCJ ) reported some rather disappointing Q2 numbers. Quarterly revenue, which came in at $482 million, was down 14% relative to the same period last year when the company reported revenues of $558 million. And that wasn't the only problem, adjusted non-GAAP earnings even showed a loss; it wasn't much, only $3 million, but a loss it was. That was quite a reversal from Q2 of last year when the company, then firing on all cylinders, reported a very healthy earnings number of $72 million.

However, these quarterly variations don't paint the full picture. As I have discussed in previous articles , a huge source of strength for Cameco is its sizable contract portfolio. In this article, we'll review Cameco's Q2 performance and discuss this very important part of its business.

Revised Guidance

Management attributed the loss to a combination of quarterly variations in contract deliveries as well as unrealized losses due to higher-than-normal U.S. dollar cash balances, these are needed for the pending acquisition of nuclear power plant equipment maker Westinghouse Electric due to close later this year.

When it comes to cash, Cameco is riding heavy; it's carrying about $2.4 billion in cash compared to about $1.1 billion at the end of last year. Given the cross-border nature of the transaction, it comes as no surprise that currency fluctuations would have some impact. CCJ booked almost $44 million in forex losses in Q2 and will continue to be impacted by currency volatility until the Westinghouse transaction closes. The deal, which was discussed in a previous article , will bring long-term value to the company, and forex volatility is just a cost of doing business.

However, if we look past the headlines and check under the hood, we can find a fair bit of good news. Management raised revenue guidance due to higher expected average realized prices in the company's contract portfolio and increased deliveries in its uranium segment.

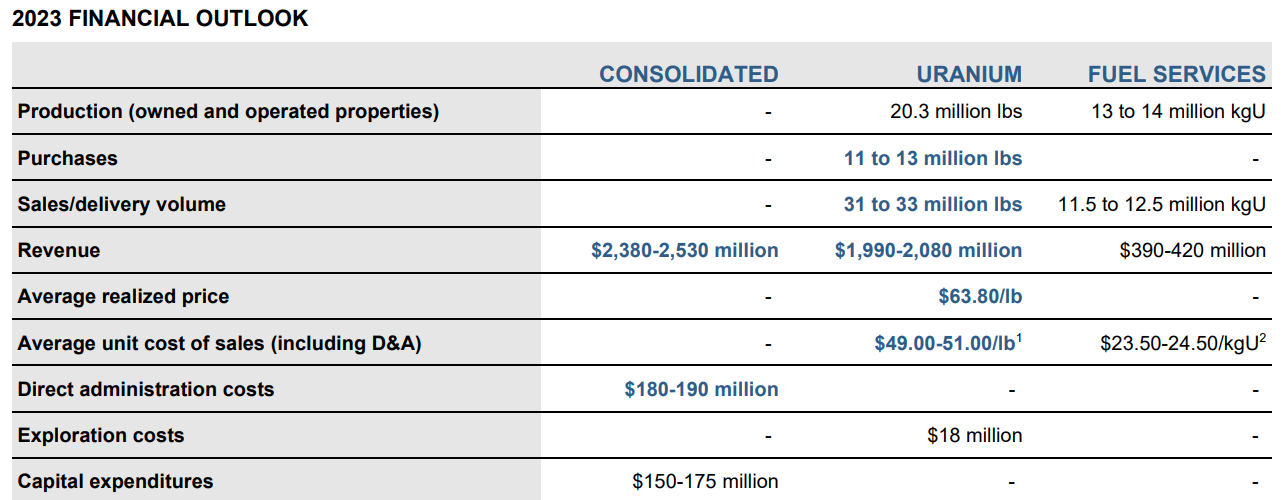

{kind=link}

As shown in the exhibit above, management is now guiding to a 2023 consolidated revenue number of between $2.4 billion and $2.5 billion, a noticeable increase from the previous $2.2 billion to $2.4 billion. A lot of that will be on the back of higher U 3 O 8 deliveries, which management now expects to be between 31 million and 33 million pounds this year (up from the previous 29 million to 31 million pound range). And that brings us to the true value proposition that is embedded within this stock.

Contract Portfolio

Cameco finds itself to be a dominant player in an industry that is on the up; it has active uranium mines; it has customers that are ready, willing, and able to sign extended multi-year contracts; and it has a Reserve of 464Mlbs (P&P). So, that means the company has to get out there and sell.

Investor Presentation

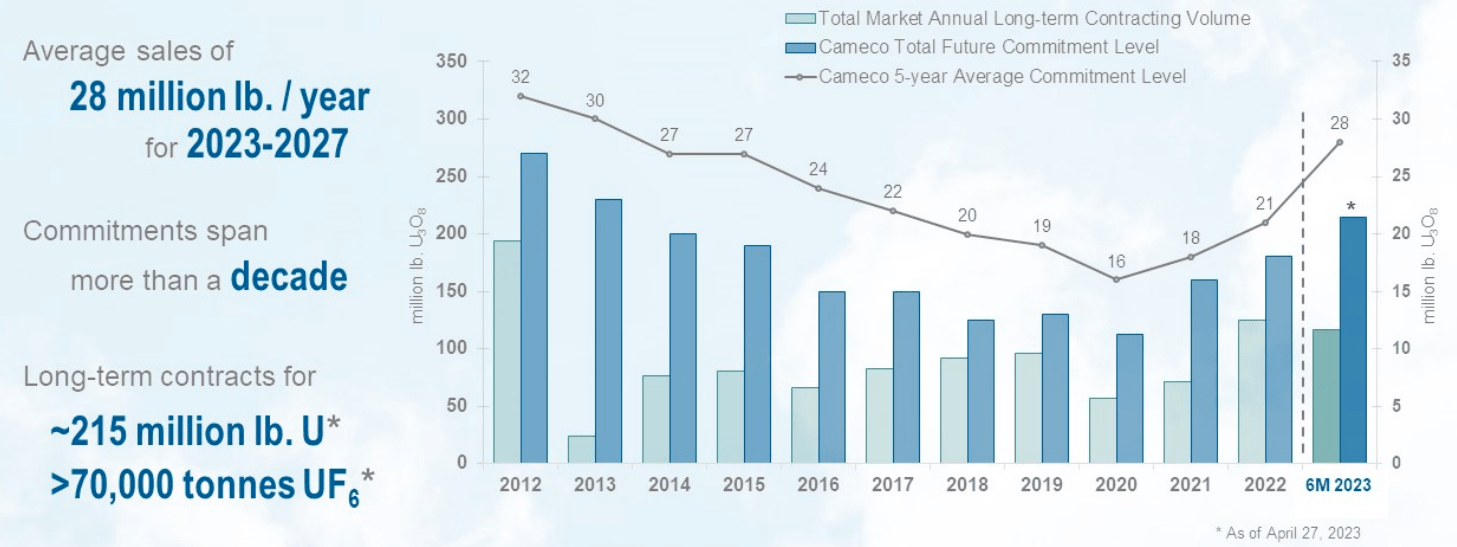

Luckily, the company's alert management is doing exactly that. As can be seen in the exhibit below, Cameco continues to grow its contract portfolio. As of June 30, it had long-term contracting commitments requiring the delivery of 28M lbs per annum over the next five years. That's a notable improvement over the 26M lbs in commitments it had just 3 months prior, at the end of March. Five years was the time interval provided in management's presentation, but some of Cameco's contracts run well beyond that. In fact, Cameco has lined up total future commitments of over 215M lbs.

{kind=link}

Some of those are fixed-price commitments, meaning that they won't be able to partake in any increase in uranium prices; however, a growing proportion are market-related contracts. In fact, during the Q2 earnings call, Grant Isaac, Cameco's Chief Financial Officer, mentioned that the company now has a preference for market-related agreements. He went on to explain that these are often collared with escalated price floors and ceilings. The terms of which he described are as follows: "For Cameco, in today's market, mid 50 spot, we can drive $50 escalated floors, and we can drive $80 escalated ceilings".

These terms provide the company, and by extension shareholders, with the ability to benefit from any appreciation in the price of uranium while simultaneously giving downside protection from any sharp pullbacks.

Competitors

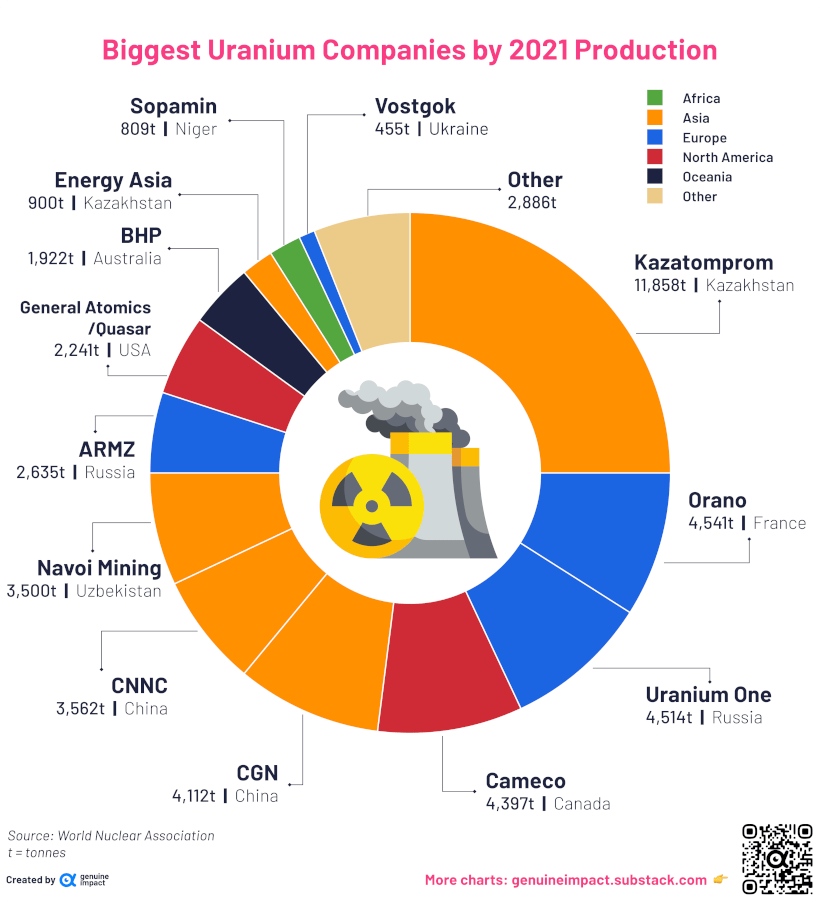

Comparing Cameco to its main competitors is a difficult proposition. Uranium is not some frivolous consumer good but rather a strategic resource required by many nations. The world's largest producer, Kazatomprom (KAP.L), is located in Kazakhstan, which brings with it the geopolitical risks of Central Asia. Orano SA is owned by the French government and is largely focused on France's energy needs. The situation is quite similar with Chinese producers. And that leaves us with the Russian producers, which bring with them obvious geopolitical risk. Therefore, much of Cameco's value comes from non-quantifiable factors such as jurisdictional certainty and its strong position in an oligopolistic market.

{kind=link}

Risk

A sharp and extended pullback in the price of uranium would still have a negative impact on CCJ's stock as management would no longer be able to sell future production at such elevated prices.

Cameco is also subject to the same operational risk that all mining projects are subject to. Floods, fires, accidents, or any of a whole host of other operational problems can have a profoundly detrimental impact on the company's stock price.

Takeaway

If we focus exclusively on the numbers, we see that Cameco is still slightly undervalued at these prices. Its current Enterprise Value is US$13.8 billion, which on a per-pound basis (using only the 424M pound Reserve) is about US$30/lb. And during its recently held Q2 earnings call, Grant Isaac stated that cash costs came in at about US$18/lb. This would imply that Cameco is currently trading at about US$48/lb. Granted, this is a quick and cursory valuation as it ignores the non-quantifiable factors listed above, which are extremely important, as well as Cameco's Fuel Services business, which makes a smaller, but still very meaningful, contribution to Cameco's bottom line.

But despite that, it appears that Cameco is trading well below uranium's current spot price of about US$57/lb. However, it is trading only a couple of dollars below the US$50/lb floor price at which most of its current contracts are being set. And given the run that spot uranium has been on over the last few months, having a margin of safety makes sense.

Therefore, CCJ's shares appear to be somewhat undervalued but not enough to give it a Buy rating at these prices. The stock is a top holding, and I would be open to adding to my position in the event of a meaningful pullback, but at these levels, I rate the stock a Hold .

For further details see:

Cameco: Keeps Adding To Its Contract Portfolio (Rating Downgrade)