CCJ - Cameco's Contract Portfolio Continues To Grow

2023-04-11 10:13:47 ET

Summary

- Cameco is planning to increase production to 20.3Mlbs U3O8 this year.

- The average realized price on contract sales looks set to continue rising.

- The company’s contract portfolio increased substantially last year.

Note: Unless otherwise stated, all references to dollars ($) are to the Canadian currency.

I first began covering Cameco Corporation (CCJ) about a year ago and what a difference a year makes. Last year, uranium prices seem to have finally turned a corner as demand continued to grow. The increased demand was, of course, rooted in the tremendous geopolitical changes that occurred as well as the simultaneous growing acceptance of nuclear energy as a carbon free alternative.

And as those winds of change show no signs of abating, the industry looks ready to make a clean break with its recent past with Cameco leading the charge. Most readers are probably well aware of its announced deal to purchase part of Westinghouse Electric Company, the subject of my last article on CCJ, but what is much less talked about is Cameco's increased sales into the uranium term market, a factor that is just as consequential for the company and the stock. In this article, we'll discuss Cameco's contract portfolio and the impact it will have on the company over the long term.

Company Background

Last year was a good year for Cameco. Revenues increased by over 26% relative to those of 2021, or just under $400 million, going from $1.47 billion to $1.87 billion. Net Earnings showed an even better improvement, going from a loss of over $102 million in 2021 to net positive earnings of $89 million. And while at first glance Cash From Operations may look like somewhat of a sore spot, upon closer inspection one finds that the decrease from $458 million in 2021 to $304 million last year was, in large part, the result of an inventory buildup. So, that's not something to be overly worried about.

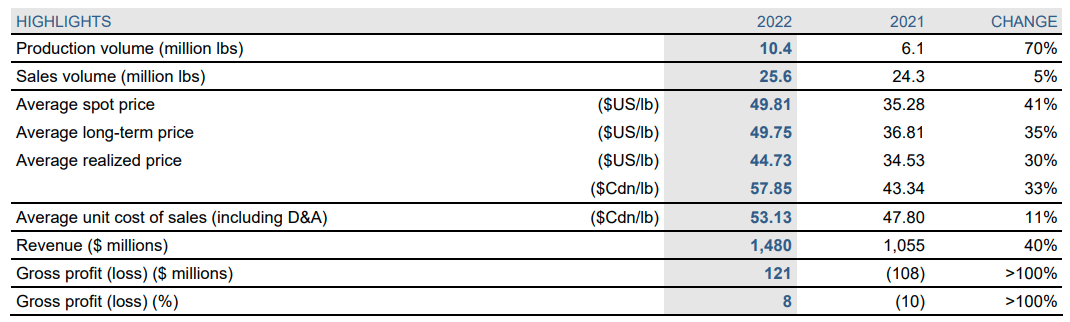

However, revenue from the Fuel Service division did come in about 10% lighter than the previous year, so all the revenue increase was attributable to higher uranium sales. As can be seen in the exhibit below, full-year production of U 3 O 8 continued to climb, going from 6.1Mlbs last year to 10.4Mlbs, but sales numbers increased by a much more modest 5%, rising to 25.6Mlb from last year's 24.3Mlbs. Cameco purchased the 15Mlb difference from other producers but wound up paying them an average price of $51.36/lb, far higher than the $34.96 which it costs Cameco to produce a pound of U 3 O 8 .

{kind=link}

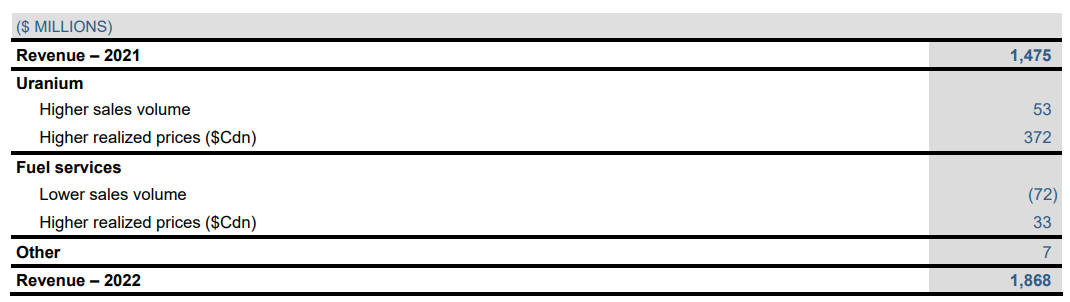

In fact, as can be seen in the exhibit below, almost all of Cameco's increased revenue came from higher realized prices on the uranium it was producing. That's undoubtedly the reason as to why management plans to extract substantially more uranium this year, growing total production from 10.4Mlbs in 2022 to an impressive 20.3Mlbs in 2023. Doing so ought to go a long way in helping the miner score some strong revenue and earnings numbers again this year.

Impact on Revenue of Changes in Price And Volume (Cameco 2022 Financials) Cameco Historical and Planned Production (Cameco 2022 Financials)

{kind=link}

{kind=link}

But before investors start celebrating too much, there's something that needs to be understood about the first table above. The table lists the average spot price of uranium for 2022 as US$49.81/lb and the average term price as US$49.75; meanwhile, Cameco's average realized price is a much more modest US$44.73/lb. That's where the term market and Cameco's contract portfolio comes into play.

Contract Portfolio

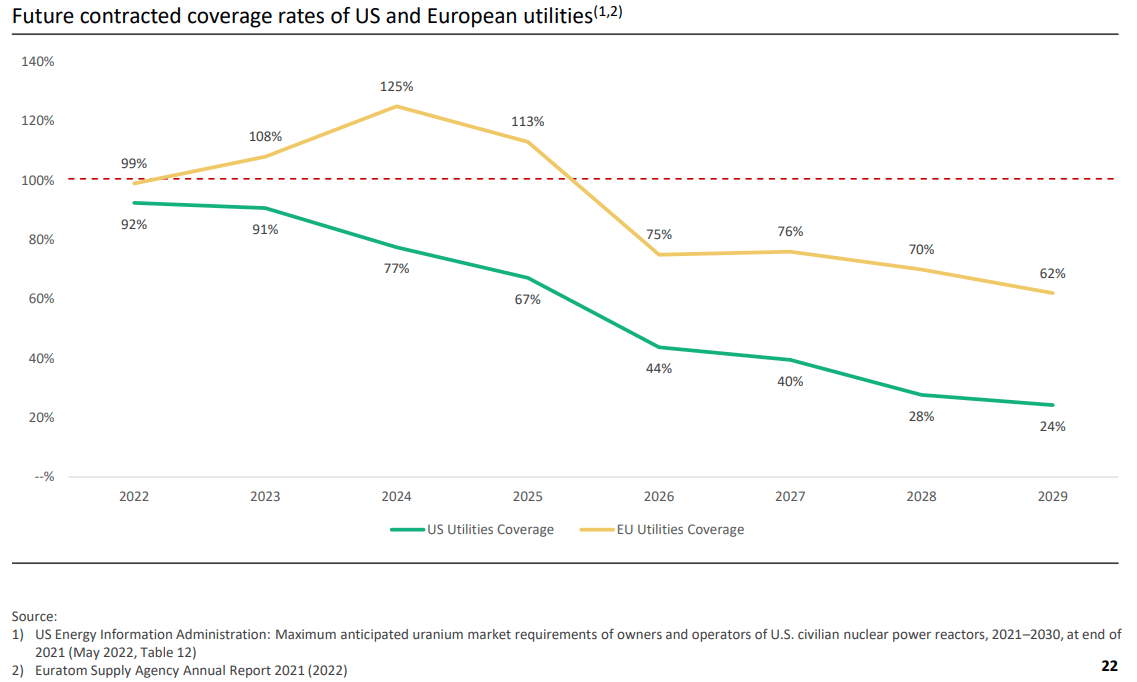

As most readers are probably well aware, a lot of the uranium market tends to trade off the current spot price for U 3 O 8 , but Cameco's management was quick to remind listeners during the company's Q4 earnings call that utilities only bought 8Mlbs in the spot market last year. Granted, Sprott Physical Uranium Trust (SRUUF) has been playing an outsized role in spot uranium purchases during recent years, but as one would expect in an industry dominated by relatively price insensitive utilities worried about securing long-term supply, the action tends to be in the term market. The graph below shows how utilities typically lock in most of their supply many years before it's ever needed.

US and EU Rates of Utility Coverage (Yellow Cake PLC Investor Presentation)

{kind=link}

What that means is that Cameco's Revenue number is not a reflection of current spot or term prices but rather the term price that was prevalent when the contracts were signed, which can be years ago. It also means that the current ~$50/lb term price will only begin to be reflected in Cameco's results gradually over time. But that time will definitely come, and Cameco's management seems intent on making sure of it.

Always Be Closing

Over the last year, management has finalized the sale of 58Mlbs of U 3 O 8 in long-term contracts and is currently working to nail down contracts for an additional 22Mlbs. On the UF 6 conversion side of the business, the company signed long-term contracts for 12MkgU and is advancing on the finalization of an additional 5MkgU.

And all of that activity quickly becomes apparent when one takes a look at the company's contract portfolio. The first of the two exhibits below shows Cameco's Future Sales Commitments as they stood at the beginning of last year while the second exhibit shows the same information a year later.

Future Sales Commitments - Jan 1, 2022 (Cameco FY2021 Financials) Future Sales Commitments - Jan 1, 2023 (Cameco FY2022 Financials)

{kind=link}

{kind=link}

It's quite clear that management has been pounding the pavement. The company's 2022 commitments have not only been fully replaced, but Cameco also managed to grow its overall sales book by over 50% with uranium sales coming in 65% higher. During the Q4 call, management stated that the company currently has about 180Mlbs of uranium and over 55k tons of conversion in long-term commitments.

They also mentioned that the industry as a whole saw about 113Mlbs in long-term contracting during 2022 as geopolitical concerns continue to play a greater role in the purchasing decisions of utilities. That pace should endure, and Cameco continues to position itself for that opportunity. The previously mentioned production increase should help it meet contract commitments, and this is all occurring at a time when it's biggest competitor, Kazatomprom, recently lowered 2023 production guidance.

Risk

Clearly the increased pace of sales, coupled with Cameco's intentions to substantially increase production, is not without its risks. The company may wind up producing more uranium than the market is ready to accept, and, in the process, hammer down the spot price which would, by extension, drag down its stock price.

Takeaway

However, Cameco seems to be very well positioned to take advantage of growth in the uranium space. Management is not sitting around waiting and hoping for prices to go even higher; instead, the company is working to lock down as many long-term buyers as it can. This may have the effect of somewhat weighing down both term and spot prices, but what it loses on price it will make up for in volume. And given the previously discussed lag between current prices and the eventual realized price, the company is setting itself up for continuously rising revenues and earnings in the years to come. For those reasons, I rate the stock a Strong Buy .

For further details see:

Cameco's Contract Portfolio Continues To Grow