CCJ - Cameco: Uranium Production Challenged Customer Demand Increasing

2023-09-08 10:14:30 ET

Summary

- Cameco will benefit from the long-term worldwide nuclear electric renaissance.

- In the short term, a production shortfall could occur in their key uranium mines that may affect 2023 financial performance.

- If properly managed, I believe Cameco can overcome this challenge to meet its 2023 delivery commitments.

Investment Thesis

Cameco (CCJ), as a world leading supplier of uranium to nuclear utilities, is in a favorable market for the demand of uranium by electric nuclear utilities. Production from its Canadian mines has returned from COVID impacts and low customer demand. Both short- and long-term demand is robust.

But, on September 3, 2023 (Labor Day weekend) CCJ announced that they now expect a 2023 shortfall from their Cigar Lake and McArthur River/Key Lake mines.

This may have an adverse effect on 2023 revenue, margin and profit. In this article we will examine the potential impact of a production shortfall in two scenarios. First the current status promulgated in the press release.

CCJ now estimates Cigar Lake production to be 16.3 million lbs. vs 18 million lbs. CCJ owns 54.547%. Thus, their share is 8.8 million lbs. vs 9.8 million lbs.

McArthur River/Key Lake product estimate is now 14 million lbs. vs 15 million lbs. CCJ owns 69.805%. Here the shortfall may be in processing the mined uranium from McArthur River at the Key Lake facility. Thus, their share is 9.8 million lbs. vs 10.5 million lbs.

And the Kazakhstan Inkai Joint Venture (40% owned) has been challenged with transporting uranium from Kazakhstan to Western countries. From the Q2 financial CCJ release “To mitigate this risk, we have inventory, long-term purchase agreements and loan arrangements in place we can draw on. Depending on when we receive shipments of our share of Inkai’s production, our share of earnings from this equity-accounted investee and the timing of the receipt of our share of dividends from the joint venture may be impacted.”

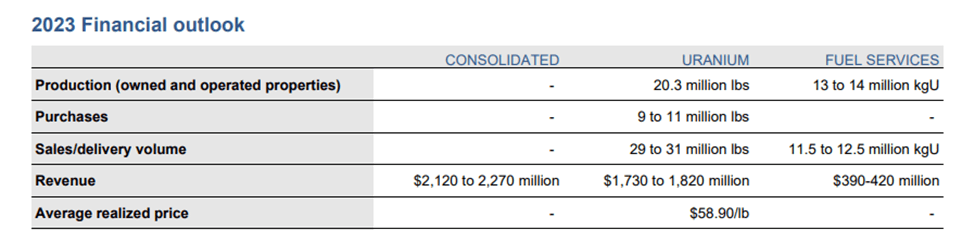

Here’s their production estimate in the 2022 Annual Report - 20.3 million lbs.

{kind=link}

If we assume the production delivery from Inkai is minimal or non-existent in 2023 this totals 18.6 million lbs, not the original estimate of 20.3 million lbs CCJ potentially may be 1.7 million lbs short of their 2023 projection.

CCJ believes they can still meet customer commitments by obtaining uranium via other sources in the short term if needed, (e.g., buy in the open market, check inventory).

On September 5, CCJ stock opened about 4% below the previous session close. But in midday it recovered to about 1% below the previous close. The daily volume is 3.9 million shares. On September 5 it was 4.6 million, about 18% higher than the average. Here’s the six-month chart. No super large impact occurred.

{kind=link}

Going Forward Risk

Using Q2 financial results we can examine two scenarios to see the effect of a possible 1.7 million lbs shortfall of uranium may have on the full year revenue.

From their August 2 press release "With improving market fundamentals, for 2023 we have increased our consolidated revenue outlook to between $2.4 billion and $2.5 billion (previously $2.2 billion and $2.4 billion), which is primarily driven by higher expected average realized prices under our contract portfolio and increased deliveries in our uranium segment.” Notice the press release states they may have "increased deliveries" assumed beyond the 20.3 million lbs projected in their 2022 annual report. This may not occur in my view.

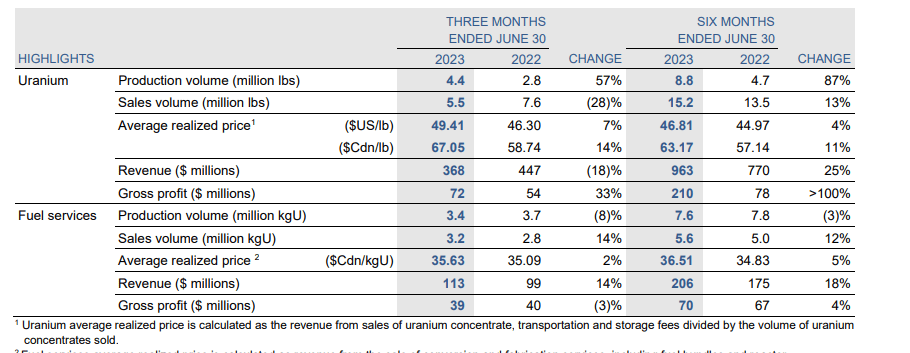

It remains to be seen if CCJ will have increased revenue as a result of the shortfall in deliveries. Currently uranium is the bulk of their revenue as noted in the Q2 statement.

{kind=link}

The six months revenue was $963M (82%) from uranium and $206 (18%) from fuel services.

Scenario One: CCJ meets the delivery commitments by purchasing uranium on the open market at minimal or no additional cost impact. Supply could also be obtained from inventory. In this scenario CCJ meets commitments and has minimal impact on revenue, margins and profit.

Scenario Two: CCJ meets delivery commitments but at an increased cost. Assume the open market price is higher than the mined costs. For the first six months of 2023, in the Q2 table above, the Gross Profit was 22% of revenue. If we assume the increased cost for uranium supply is 20%, the Gross Profit margin could be reduced to about 6%. This would be a notable effect.

This is all in the short-term, 2023. I believe the future of the uranium business in the long term is bright.

Uranium Business

Uranium, unlike other natural resources such as oil and copper, is not traded in the open financial markets. Instead, the price for uranium is influenced by the demand from nuclear utilities and the production and supply. The demand for the resource influences the price. 80% of the utility purchases are on long term contracts. Only about 20% is from the spot market. CCJ deals almost exclusively in the contract market, not the spot market. And these long-term contracts, perhaps five to eight years, or more, include a price adjustment provision.

Utilities are contracting for the remainder of the decade. Supply appears tight, thus putting upward pressure on price.

The underlying driver is demand. Supply is fragile, demand is growing.

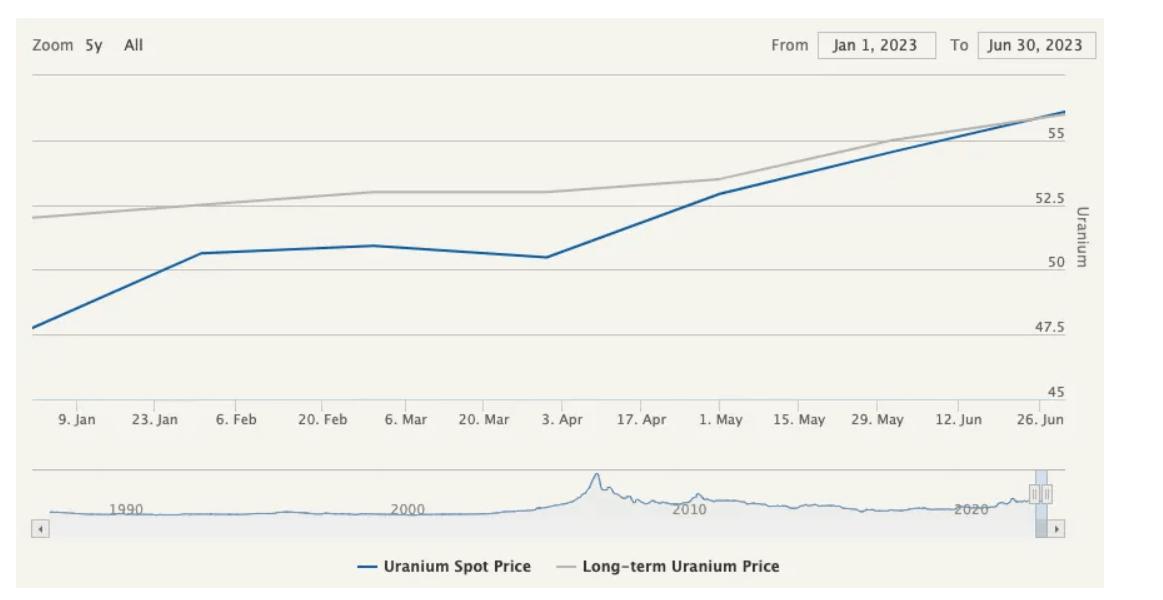

Today, and in the future, demand is increasingly impacting the price as seen here.

Investing News Network 7/18/23

{kind=link}

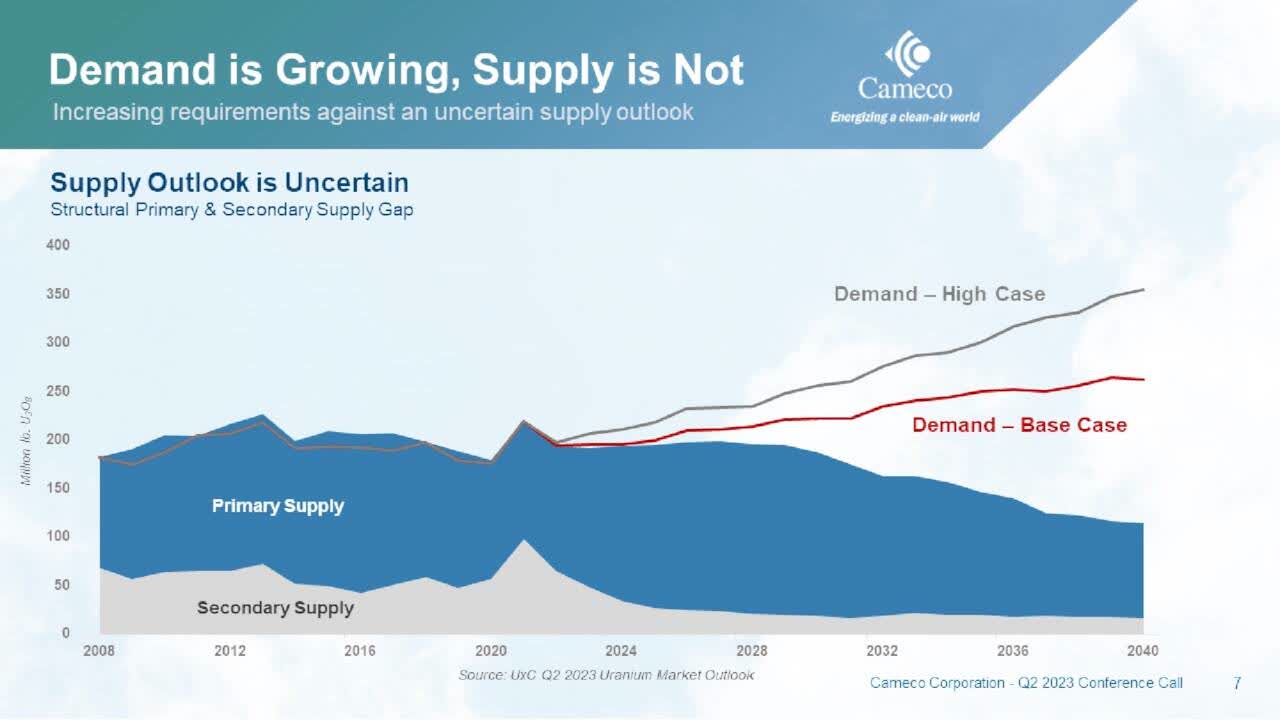

And utilities have an abundance of uncovered need per CCJ.

{kind=link}

An agreement between the US and Russia to reprocess nuclear weapons to lower the enrichment for use in commercial power plants decreased the need for large amounts of mined uranium in the US beginning at the turn of the century. This is likely coming to an end.

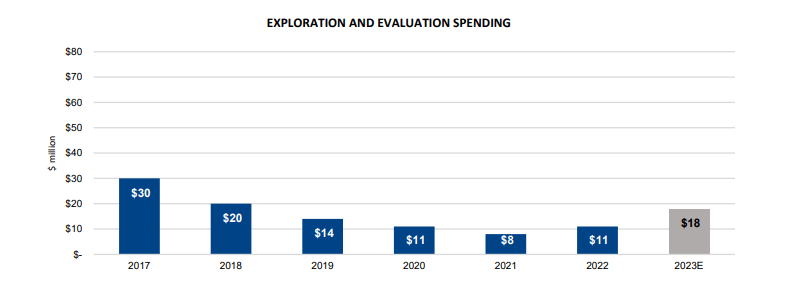

More companies are getting into the uranium mining business, including small mining start-ups. Although the time to explore, recover and make a dent in the marketplace could be on the order of five years or more. Mining can be a capital-intensive business. These companies require capital either from equity or debt. And with interest rates high opening new mines are more capital intensive. Here’s CCJ’s exploration spending history.

{kind=link}

Exploration by CCJ and its competitors will yield more supply. But it takes time and money to open a new, uranium productive mine.

New Plant Update around the World

Here's a short summary of new nuclear power activity throughout the world. This is a positive environment for CCJ.

Japan

12 years after the 2011 Fukushima accident, Japan continues to restart reactors and may even build new ones. Some plants are being upgraded and are planning on extending their life to 60 years. (Some plants in the US have life extension to 80 years). At one time Japan had over 50 nuclear power units in operation. Today 10 are back in operation. Many plants are old and will eventually be decommissioned or are too expensive to make upgrades after the Fukushima accident. As I have written in my previous two CCJ articles, nuclear power is slowly returning in Japan. Restarting plants provides a near term demand.

Canada

Today nuclear provides about 15% of Canada’s electricity. Like elsewhere in the world (except in Germany) new plants are in the planning stages. Ontario Power plans to build four Small Modular Reactors of 300 MWe each at its Darlington plant. The reactors will be designed and supplied by the General Electric (GE), GE Hitachi Nuclear Energy. These will be operational in the mid 2030’s.

Ontario Power had a few plants in major refurbishment which are now coming back online creating near-term demand.

France

France has about 56 operable plants. France is planning to build six new plants, known as the European Pressurized Reactor – EPR. As a side note, France obtains much of their uranium from Niger, currently undergoing political instability.

United Kingdom

Two large units are in the site preparation and design phase for Sizewell C. While the construction is still to be determined, this represents moving ahead with more nuclear in the UK.

United States

After many years and higher than expected costs, the Vogtle 3 (1100 Megawatts electric) nuclear plant is now in commercial operation. On July 31 electricity from Vogtle 3 was on the grid. With a majority ownership by Georgia Power, it is the first nuclear power plant to go into operation in the US is three decades. Vogtle 4 is in the startup phase and will become operational at the end of 2023 or early 2024.

Per the July 31 press release by Westinghouse Electric Company “The AP1000 units at Plant Vogtle, located near Waynesboro, GA, are Generation III+ pressurized water reactors with fully passive safety systems, modular construction design and have the smallest footprint per MWe on the market. Four AP1000 units are currently setting operational performance records in China with six additional reactors under construction. Poland recently selected the AP1000 reactor for its nuclear energy program, Ukraine has made firm commitments for nine AP1000 units and Westinghouse announced in June that Bulgaria will construct an AP1000 unit at the Kozloduy nuclear site. The technology is also under consideration at multiple other sites in Central and Eastern Europe, the United Kingdom, India and in the United States.”

TerraPower, a company with funding from Bill Gates and with Department of Energy funding, is designing and building an advanced demonstration reactor in Wyoming. Its capacity will be about one-third of Vogtle’s and a little more power (345 MWe) than a Small Modular Reactor.

Poland

In order to reduce its dependence on coal, Poland plants to build six large Pressurized Water Reactors by 2040. The initial construction is planned to start in 2026 with operation in 2033. While it will not affect short term uranium supply it is another example of worldwide expansion in nuclear power.

Poland is also planning to build some Small Modular Reactors.

I could fill up this article with further information regarding potential worldwide nuclear power projects, but we will leave it at that. This is all great for the nuclear renaissance, but it mostly provides long-term demand, not demand in 2023/2024.

Conclusion

The CCJ August press release, noted above, signals the 2023 production outlook from owned and operated facilities of 20.3 million lbs may not be achieved. As stated in that press release customer delivery commitments may need to be augmented from other sources (i.e., open market purchases). The cost to CCJ may be impacted.

Due to the increased worldwide nuclear power environment CCJ should prevail in the long-term but I would assess the impact of the production shortfall prior to immediately buying additional shares. I have defined two possible scenarios that provide a range of impact. The Q3 earnings call, probably in November, should provide further management input. I would continue to monitor the stability of the stock price.

For further details see:

Cameco: Uranium Production Challenged, Customer Demand Increasing