NVDA - Camtek: A Growing Semi Niche Player

2023-08-15 06:12:15 ET

Summary

- Camtek produces automated inspection and measuring equipment for high-end chip manufacturing, with a unique product line.

- CAMT got 52 orders for this equipment in a short time span. This is likely downwind of Nvidia’s data center GPUs.

- Camtek's Q2 earnings show sequential growth and positive guidance for the rest of the year. I think 2024 and 2025 will be a lot bigger.

- The big risks they face are future competition, and market saturation in their limited number of customers for this machine.

- It is no longer cheap, but it is also not that expensive. There may be a pullback after a pretty epic few weeks.

Camtek

Camtek ( CAMT ) produces automated inspection and measuring equipment for high end chip manufacturing. Not that they are without competition here, but one of their product lines, Eaglet-AP , is unique for these purposes. In both memory and logic foundries, the little details and defects etched into chips are getting smaller, and the designs more complex. Inspection and measuring requirements are getting higher.

In memory, there is suddenly huge demand for expensive HBM memory after years of slack sales. This is the type that goes in Nvidia ( NVDA ) data center GPUs, from Korean SK Hynix. Each card has 80 GB and each server 640 GB. Hynix has to make a lot more HBM3 than they thought a few months ago. Now, despite the high cost, people are considering HBM for more places to clear bottlenecks between CPUs/GPUs and memory.

High end logic chip design has now moved to "chiplets" that are packaged together. We see this in the best chips from Nvidia, Apple ( AAPL ) and AMD ( AMD ). Apple gives us the best visual:

{kind=link}

The "Ultra" line of M-series Mac chips are actually two "Max" chip dies packaged together with memory. In this image of the M1 Ultra, there are two M1 Max dies top and bottom in the middle attached with a high speed "fabric". The memory is directly attached to either side. Packaging logic with memory increases bandwidth between them and reduces latency, something Nvidia is also doing now.

The advantage to Apple of that center part is that it drastically reduced the development costs of Ultra without compromising on performance, because they've designed their chips to be scalable. The Max and Ultra are chips that go into the most expensive Macs, so the volumes are relatively low for Apple. By doubling up Max chip dies for the Ultra, they get to take advantage of economies of scale for both the Max and the Ultra. Making more smaller chips also improves yields, a constant battle in high end chipmaking. Nvidia and AMD see this same cost advantages in their chiplet designs.

I have been pretty hot on Camtek because of this trend. They are a very small player compared to their competition, but uptake on Eaglet-AP was slow and steady. That abruptly ended in July with the announcement of sales of 42 systems for HBM memory and chiplet advanced packaging applications. I'm going to guess that most of that is going to go to SK Hynix for Nvidia's HBM, and TSM ( TSM ), Nvidia's logic foundry.

I was sure there would be a pullback after that first couple of days, but it just kept going. I think because of their size and domicile in Israel, they were a little off the radar, even for people who followed the semi equipment sector. No longer.

They followed up with their Q2 earnings less than 3 weeks later, where they announced the orders for another 10 machines. Let's talk about that.

Q2 Earnings

Camtek's sector, wafer fab equipment, or "WFE," has been on a roller coaster ride. In 2020 the whole sector was over $90 billion in sales. In 2021 that went up to over $100 billion. As the year turned, predictions for 2022 were as high as $120 billion. But the Fed's hiking cycle got in the way, and it was back to around $90 billion, with a lot of the sales in H1. For 2023, estimates are in the $70-$75 billion range, down a lot from 2022, and even more from the 2021 peak.

There are two exceptions here: ASML ( ASML ), the largest player, and tiny Camtek.

Camtek had a rough Q1 like a lot of the sector, but was back to sequential growth in Q2. Compare those charts to some other names in the sector:

2023 has been rough and guidance from those two was for more of the same in H2. Lam Research ( LRCX ) especially has issues with their exposure to memory manufacturers and China.

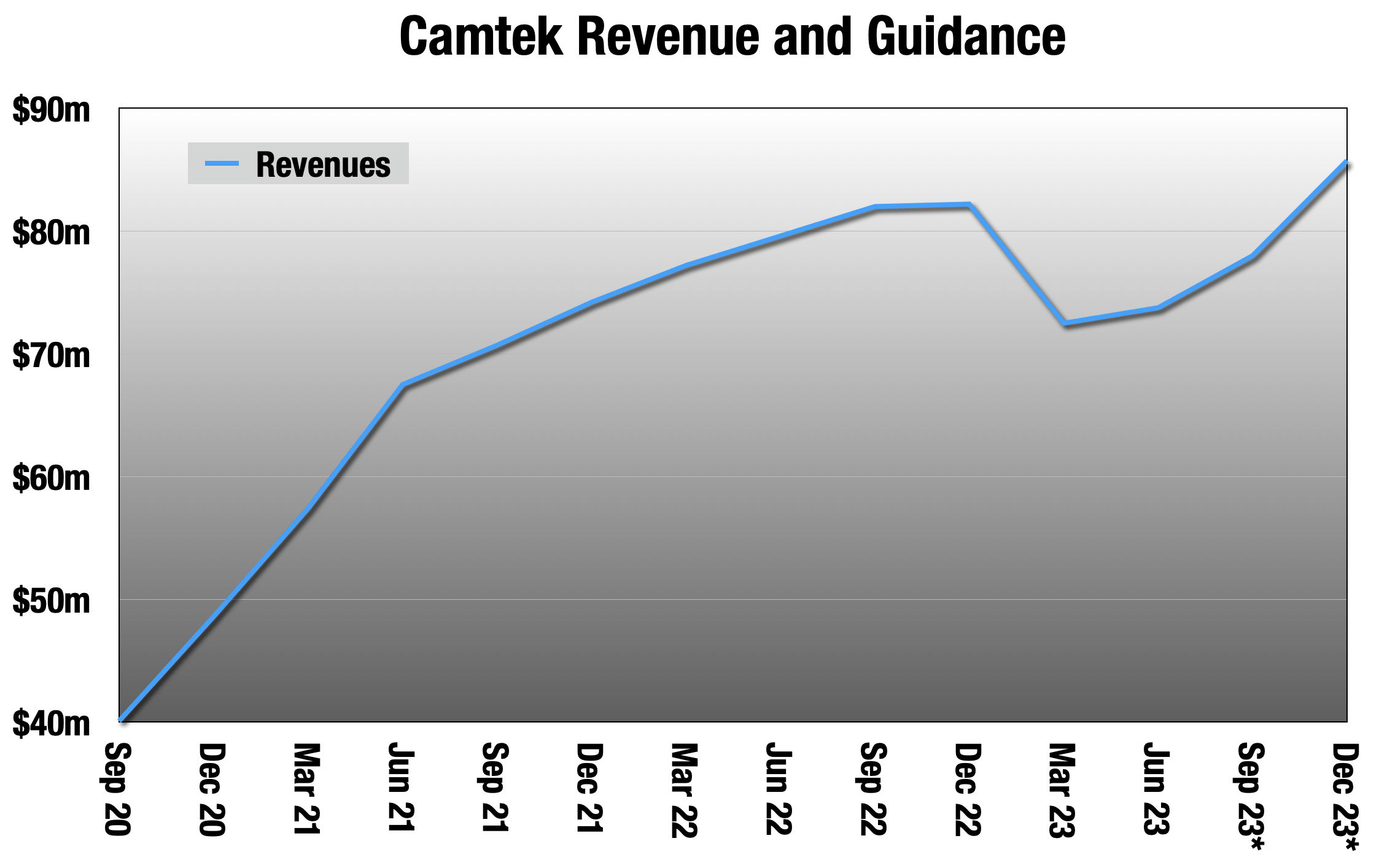

In contrast, Camtek's guidance for the rest of the year is far more encouraging after that bad Q1:

*From guidance and analyst calculations (Camtek quarterly reports and 2023 guidance)

{kind=link}

Despite that H2 guidance, 2023 annual will be down from 2022, but Q4 should be up YoY. That's a lot of momentum headed into 2024. The 52 Eaglet-AP systems they announced will begin shipping in Q1. My modeling is for significant growth in 2024 and 2025 as that AP line takes over the operating statement, but there is one substantial risk, and we'll talk about that in the next section. Eaglet-AP systems are only about 15% of revenue right now, and they are projecting that to double next year.

Like a lot of the sector, Camtek gained a ton of operating leverage in 2021, but that has come off from a combination of slowed sales, increased R&D, supply chain inflation, and engineer wage inflation.

Again, that recovery in Q2, returning to gaining leverage with revenue growth. I think they will be back at 25% in H1 next year, if not Q4 this year. The biggest drag on that going forward will be R&D expense:

I think we'll also see that turn up because of the big risk to this story: competition.

Two Risks

The first and largest is competitive. Plenty of companies make inspection and measurement equipment; it's very important at multiple stages of the wafer fabrication process. Camtek identified a high-end niche that they could exploit with little competition. That was a small niche, and the large players were uninterested. But their competitors also saw that they sold 52 of these machines in a short span of time. The playing field could get crowded.

That big risk came up in the Q2 earnings call:

Charles Shi [Needham]

Do you expect competitors to catch up? And given how strong this market is, I mean, is it becoming a lot more attractive?

Ramy Langer [COO]

So, first of all, yes, you're right, it's a lot more attractive as the volume goes up. Definitely, we are a very strong market leader. And I think today with our market position, our understanding of the customer requirements, I think the barrier for entry is much higher than it used to be previously. So yes, there is going to be competitors, but, you know, I think that we understand the market, and moving forward, I think we will continue to hold a major market share in the future as well.

Charles Shi

Why you think the barriers to entry is higher today?

Ramy Langer

Because I think we have learned a lot of things that the application requires. We have very close relationships with the customers. We provide very good customer support, and we are really entrenched in the processes, how to inspect things, how to measure things. And I think to replace Camtek today with all the understanding and the experience that we have accumulated over the last few years, I think it's not an easy task.

Rafi Amit [CEO]

Yes, I would like to add, there another issue very typically to the semiconductor industry. I think that the key - one of the major issue is maintaining high yield in general in this industry. If you cannot do it, you're out of the business. Now, when customers using, you know, equipment and they get good result, high yield, very good support, they have no good reason to replace it with other competitors.

So, we work very hard, number one, to be all the time very competitive in performance. Number two, to give an excellent support to customer and support is not just to fix machine and application, it's a lot of special feature, new R&D, whatever is needed and do it quickly. So, when you provide to a customer such services, he really has no any good reason to go and to look for another competitor. This is very obvious in this industry.

Sorry for the long quote, but this is an important question asked well, and I don't think they have the greatest answer. Amit is absolutely right that his customers are risk-averse. Semi fabrication is like alchemy, and once a manufacturer get a process that works with high yields, they are loathe to change it. That's a real moat, but it may not be deep enough to defend.

Camtek is a small fish in a big pond. I already mentioned KLA ( KLAC ). Let's look at what they sell.

{kind=link}

All that stuff KLA sells, and Camtek only competes in the highlighted part. I think Camtek has a shot at $500 million in revenue run rate in 2025, and that's about 2-3 weeks of revenue for KLA. If KLA were to develop a competing machine, they could bundle it with their other process control equipment customers were already buying, undercutting Camtek on price. Essentially, it's what Microsoft ( MSFT ) has done over and over to incipient competition, most recently with Slack, Zoom and Teams.

So we really want to be on the lookout for competing machines and who is making them. For now, they have an open field. But returning to R&D, Camtek is going to have to keep advancing and expanding the Eaglet-AP product line in the face of competition, and that will drive up operating expenses.

The other risk is the same one ASML faces with their EUV machines: there are a limited number of companies playing in this very deep end of the pool, and so a limited number of customers for Eaglet-AP. There are 5: TSM, Samsung, Intel ( INTC ), SK Hynix and Micron ( MU ). They have the fabs making chiplet advanced packaging, and HBM memory. Camtek does not face export controls to China like ASML does for EUV, but it's sort of besides the point. Chinese fabs have been cut off from the other equipment needed to play in this deep end, so they have no need for this type of inspection equipment. Camtek still sells plenty of their lower-end product lines in China.

So the second risk is that the market gets saturated quickly. I rate this as low, because I think that deep end will keep getting deeper. This is the high margin part of the business, and the strongest long term driver of the semi industry.

Valuation

Any time a stock shoots up like that, at a minimum it is not cheap anymore. But Camtek was so ignored before, it's also not very expensive.

The 52 Eaglet-AP machines they booked in June and July will mostly ship in H1 2024. Camtek is not widely covered, but my read on analyst estimates for 2024 and 2025 is that they are skeptical that there is much behind that - the fast saturation scenario of the second risk. Those 52 machines are priced in now, but I do not think much more is. I think this is just beginning. The deep end of the pool will keep getting deeper.

After the big price surge, I was surprised that it kept going, and that we never really saw a profit-taking pullback. I still think there may be a pullback waiting for us. It did shave some in the last week, and is finally underperforming the rest of the sector after a few weeks of large overperformance.

So there may be a cheaper price in the near term, but I remain bullish long term.

For further details see:

Camtek: A Growing Semi Niche Player