CA - Canada Goose: They Just Aren't Buying Luxury The Way They Used To (Rating Downgrade)

2023-12-22 02:31:55 ET

Summary

- Consumer spending on luxury goods, including Canada Goose products, may be declining while spending on experiences like travel remains strong.

- Canada Goose shares have dropped nearly 30% this year, and the company has lowered its outlook for fiscal 2024 due to macro uncertainty.

- Trading at ~15x next year's earnings, Canada Goose isn't cheap enough to justify all the top-line risks that have emerged.

Though consumer confidence seems to be rebounding ahead of 2024 on the back of lower interest rate expectations, one theme is still ringing true: people continue to spend lavishly on experiences like travel, but spending on goods - including and especially luxury items - may be waning. It's not that consumers aren't still buying luxury, but perhaps the replacement cycle for these items and the impetus to "treat ourselves" on a spontaneous basis is drying out.

Against this backdrop, shares of Canada Goose (GOOS) have dropped nearly 30% this year, dramatically underperforming the S&P 500's ~20% gain over the same time period. Still, Canada Goose joined other stocks in rallying over the past two months, despite a very weak fiscal Q2 (calendar Q3) earnings print that showcased underperformance ahead of the critical holiday season.

With the guidance cut, I'm no longer hopeful for this stock in 2024

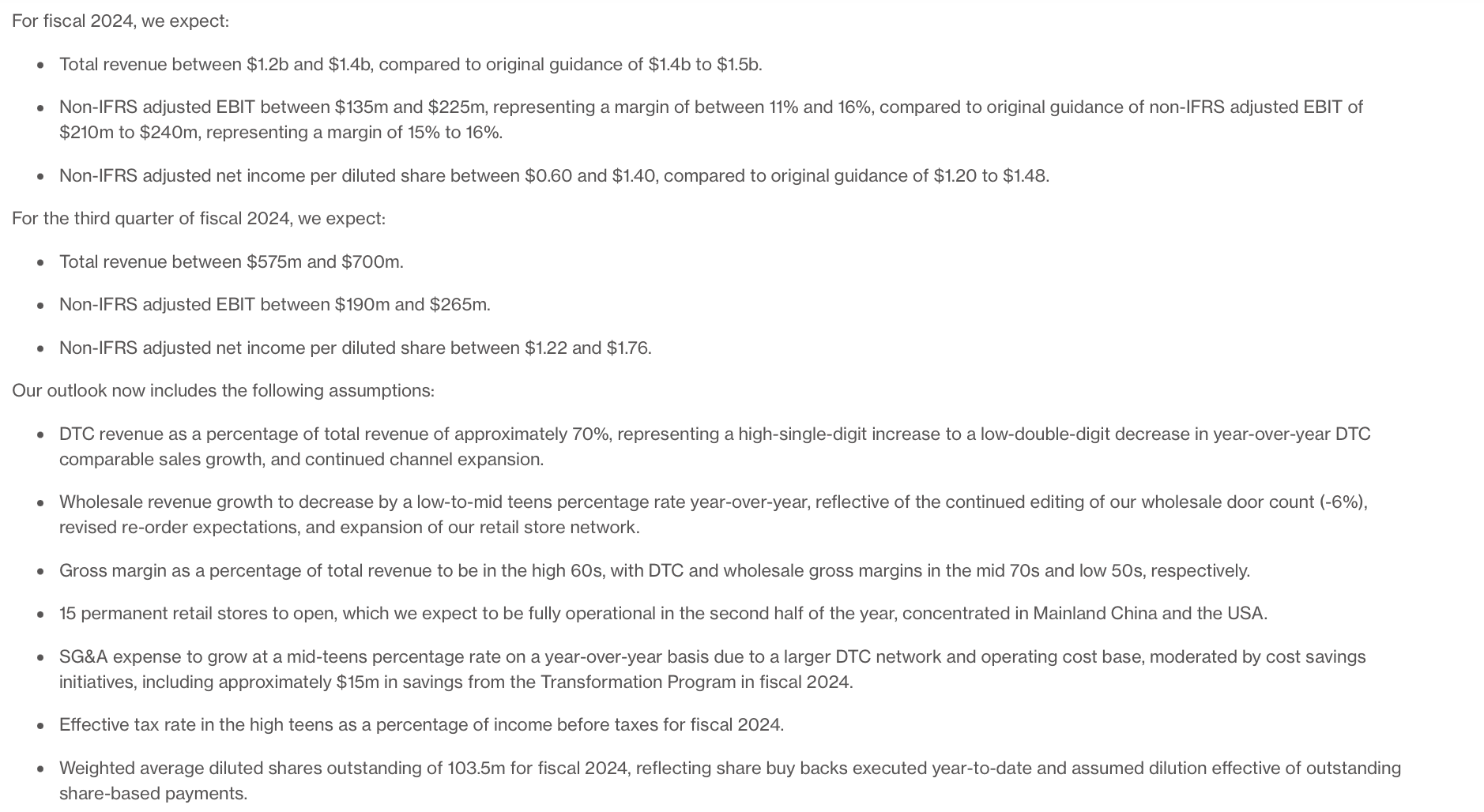

Making matters worse, Canada Goose dramatically lowered its outlook for fiscal 2024 (the year for Canada Goose ending in June 2024, of which there are only two quarters remaining), citing continued macro uncertainty.

Canada Goose FY24 outlook (Canada Goose Q2 earnings release)

{kind=link}

As shown in the chart above, the company reduced its top-line forecast by roughly ~10% at the midpoint, now pointing to a range of C$1.20-$1.40 billion in revenue - which, at the low end of that range, would signal no growth versus FY23.

Hurting perhaps even more (especially as the primary draw to Canada Goose was a cheap P/E multiple) is a heavy slice in its EPS forecast, to just C$0.60-C$1.40. Bear in mind that is a very wide range that reflects heavy uncertainty over product mix, channel mix and overall margins, as well as opex growth from new store openings - but the key thing to be aware of is that the low end of that range is exactly half of its prior outlook. The core message rings clear: Canada Goose is still citing a lot of uncertainty over its performance this year, and it appears that with DTC results slowing ahead of the holiday season, the company was right to slash its outlook.

I last wrote a bullish outlook on Canada Goose in October, when the stock was trading at similar ~$13 levels - but before this guidance slash. Now, with the lower results expected for this year plus the weakening trends that we've observed in the most recent quarter, I am now bearish on Canada Goose - a two-step downgrade that reflects the sharp reversal in expectations for this company, with little corresponding drop in share price (thanks to the market rally that happened during Canada Goose's earnings cycle, offsetting the company-specific bad news).

While I still remain moderately hopeful that Canada Goose's push toward direct-channel sales and its expanding lineup of products (the company released its first-ever sneaker product, the Glacier Trail, in Q2) will continue to diversify its revenue base and improve margins, I'm worried about long-term buying trends for Canada Goose - especially as the world's biggest luxury consumer, Mainland China, continues to face economic hardship that may permanently change consumer buying patterns.

Consensus expectations are calling for $0.64 in pro forma EPS for Canada Goose this year (in USD), and $0.86 for next year FY25, representing 34% y/y earnings growth on 12% y/y expected revenue growth. It will be a challenging path to get there (revenue is now flat y/y, driven by retrenching wholesale sales), but even if we assume FY25 consensus holds, Canada Goose still trades at ~15x FY25 P/E - which, to me, is now nearly enticing enough to warrant buying a stock with risky near-term trends.

All in all, I'm content to move to the sidelines here until Canada Goose either falls to a ~12x FY25 P/E multiple (or a ~$10 price target; ~20% downside from current levels) or fundamental conditions improve.

Q2 recap

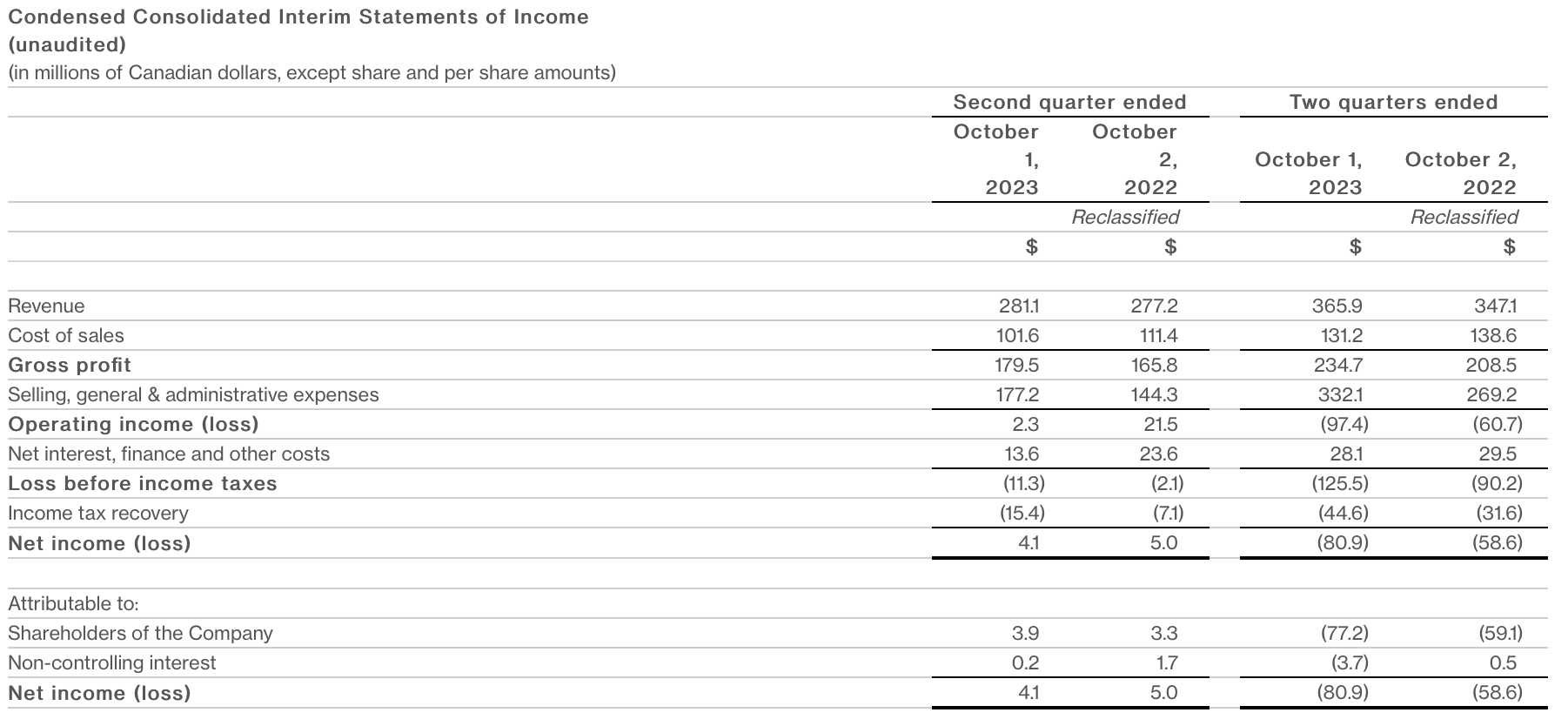

Let's now go through Canada Goose's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

Canada Goose Q2 results (Canada Goose Q2 earnings release)

{kind=link}

Canada Goose's revenue grew just 1% y/y to $281.1 million, missing Wall Street's expectations of $282.2 million (+2% y/y) by a one-point margin.

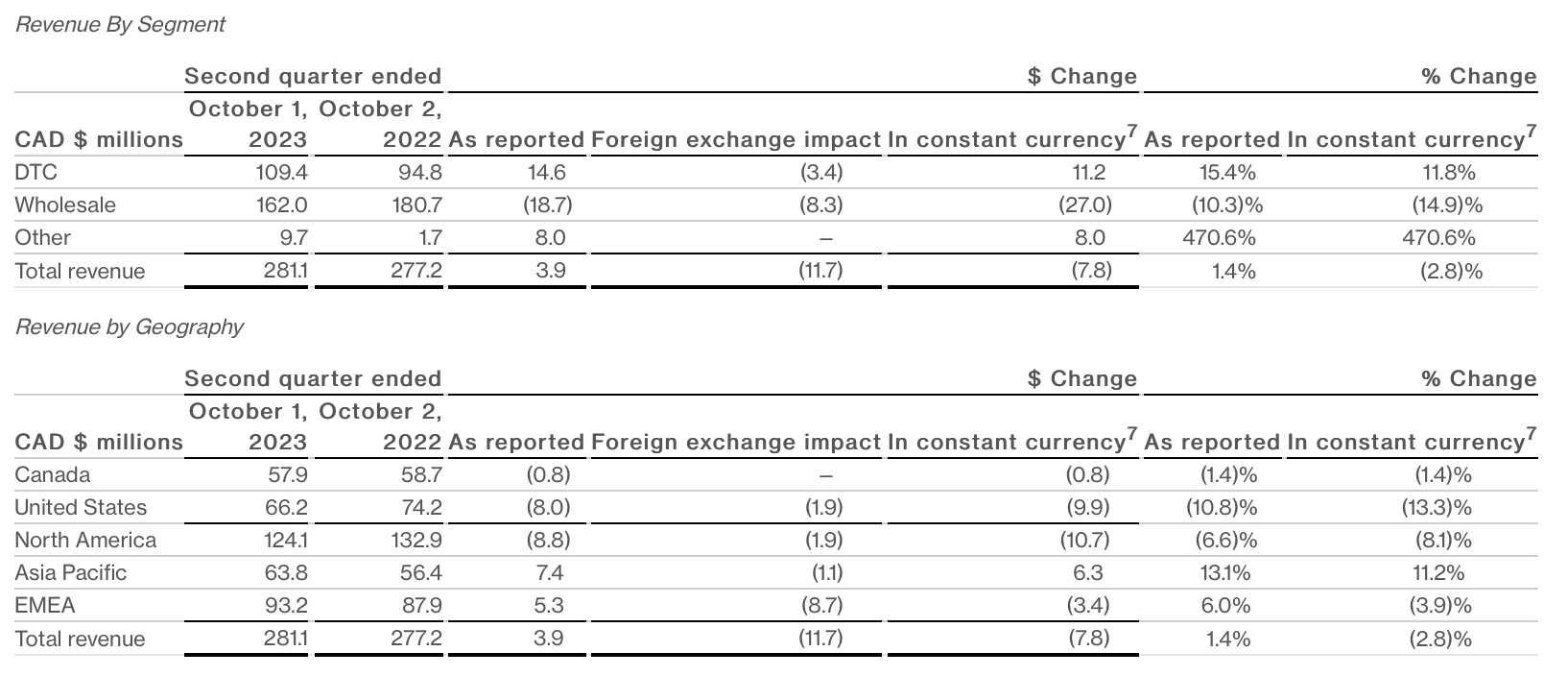

Segment results are shown in the chart below, and they help to illustrate a lot of the key themes that are driving Canada Goose at the moment.

Canada Goose segment results (Canada Goose Q2 earnings release)

{kind=link}

DTC (direct to consumer) revenue grew 15% y/y (or 12% y/y on a constant-currency basis, as the Canadian dollar's weakness vis-a-vis international currencies including the U.S. dollar has benefited Canada Goose's as-reported financial). Note that this is a declaration versus Q1's 54% y/y DTC growth rates, though there's an asterisk over Q1 results as it doesn't represent a key buying period for Canada Goose's primarily winter wear (DTC results in Q2 are still roughly double that of Q1 on a nominal basis). Wholesale, meanwhile, declined -10% y/y as Canada Goose both shrinks its partner network to focus on higher-margin DTC sales, and as partners pull back on buying inventory in the expectation of a softer holiday season.

On a geographical basis, meanwhile, the core thing to note is that Asia Pacific was the strongest-growing region at 13% y/y - but note also that growth is decelerating quite sharply versus 52% y/y growth in Q2.

The company is still optimistic on China. Per CEO Dani Reiss' remarks on the Q2 earnings call :

In late October, we held our largest event to date in China as we celebrated our fifth anniversary of our first brick and mortar store in the region. We welcomed nearly 500 guests to our event held in Shanghai, during which they took in our first ever fashion show in the country, which was held outdoors. The event was one of the most successful activations in the market so far, resulting in over 3 billion media impressions.

Chinese shoppers continued to be a driver of our growth, both inside and increasingly outside of the country. As of Q2, we had 21 stores in China, a position that we have got opportunistically backed by strong demand for our brand in this market, and knowing that this will position us well following the pandemic.

I was in China last month for our five year anniversary celebration and visited our stores and met with top customers and I was pleased to see the level of profits in their stores and truly impressed with the guest experience our customers are receiving."

Still, I am concerned about the long term here - especially as multiple headlines call out a slowdown in spending, that may become instilled in longer-term buying habits.

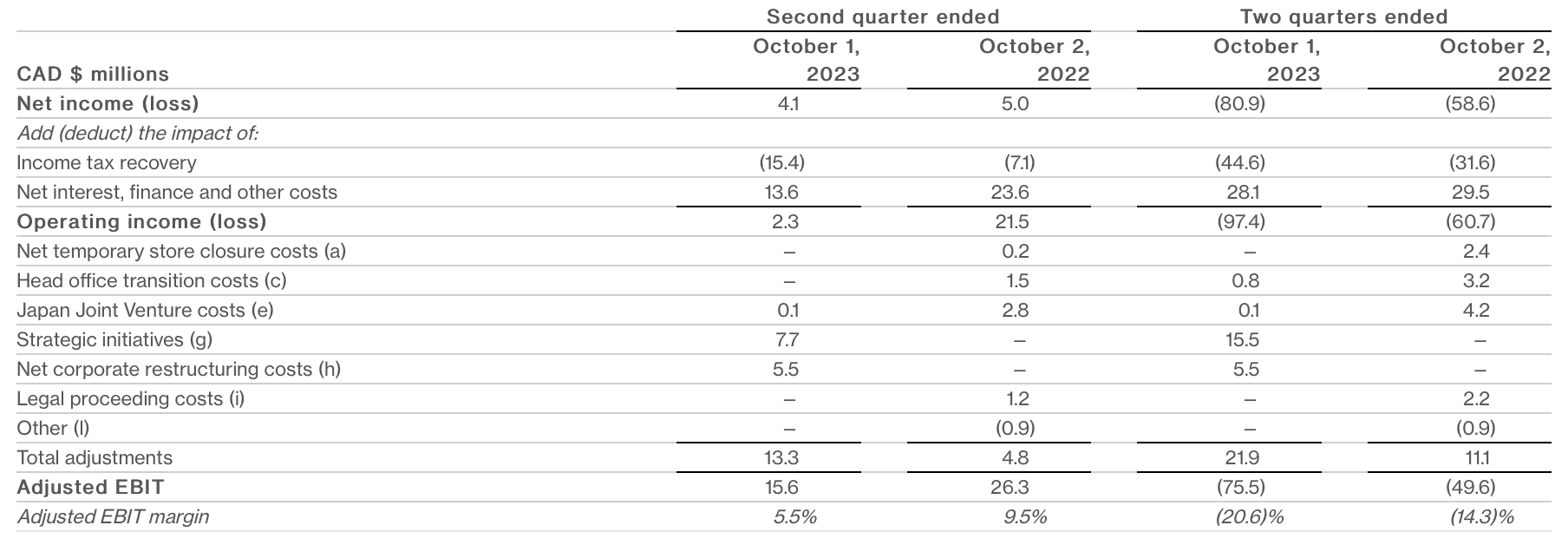

From a profitability standpoint, Canada Goose's adjusted EBIT shrunk -41% y/y to $15.6 million, representing a 5.5% margin - down 400bps y/y.

Canada Goose EBIT margins (Canada Goose Q2 earnings release)

{kind=link}

A four-point jump in gross margins (driven by a greater mix of higher-priced products, plus the channel mix shift into DTC) was more than offset by a 23% y/y jump in selling, general and administrative expenses, primarily associated with the company's broader retail network. The company opened six new stores in the quarter; three in the U.S., two in China, and one in Japan. In spite of double-digit DTC growth, however, the company has been unable to stimulate total top-line growth - and my fear is that profitability will continue to decline on dis-economies of scale.

Key takeaways

With top-line weakness, profit deterioration, and a large cut to current-year expectations, it's a good time to get out of Canada Goose stock. Still trading at ~15x next year's earnings, I'd need to see either a sharp decline in stock price or a meaningful turnaround in fundamentals to be interested in this name again.

For further details see:

Canada Goose: They Just Aren't Buying Luxury The Way They Used To (Rating Downgrade)